Table of Contents

- Key Takeaways

- California’s Counties: The Basics

- Key Facts About County Revenues and Spending

- The State Rules That Determine Counties' Revenue-Raising Authority

- The County Budget Process: State Rules and Local Practices

- Three Versions of Annual County Budget

- The Timeline of the County Budget Process

- Appendix

Every year, California’s 58 counties adopt local budgets that provide a framework and funding for critical public services and systems — from health care and safety net services to elections and the justice system.

But county budgets are about more than dollars and cents.

A county budget expresses our values and priorities as residents of that county and as Californians. At its best, a county budget should reflect our collective efforts to expand opportunities, promote well-being, and improve the lives of Californians who are denied the chance to share in our state’s wealth and who deserve the dignity and support to lead thriving lives.

Because county budgets touch so many services and our everyday lives, it is critical for Californians to understand and participate in the annual county budget process to ensure that county leaders are making the strategic choices needed to allow every Californian — from different races, backgrounds, and places — to thrive and share in our state’s economic and social life.

This guide sheds light on county budgets and the county budget process with the goal of giving Californians the tools they need to effectively engage local decision-makers and advocate for fair and just

policy choices.

Key Takeaways

the bottom line

- County budgets are about more than dollars and cents.

- Crafting the annual spending plan provides an opportunity for county residents to express their values and priorities.

- County and state budgets are inherently intertwined because counties are legal subdivisions of California and perform functions as agents of the state.

- To a large degree, county budgets reflect funding and policy choices made by the governor and the Legislature as well as by federal policymakers.

- However, county budgets also reflect local choices, as counties allocate their limited “discretionary” dollars to local priorities.

- Counties’ ability to raise revenue to support local services is constrained.

- For example, counties cannot increase the property tax rate to boost support for county-provided services.

- Counties may increase other taxes to establish or improve local services, but only with voter approval.

- Both state law and local practices shape the county budget process.

- State law establishes minimum guidelines that counties must adhere to in developing their budgets.

- Counties can — and often do — exceed these state guidelines in crafting their budgets and sharing them with the public.

- The county budget process is cyclical, with decisions made throughout the year.

- The public has various opportunities for input during the budget process.

- This includes writing letters of support or opposition, testifying at budget hearings, and meeting with supervisors, the county manager, and other county officials.

- In short, Californians have the opportunity to stay engaged and involved in their county’s budget process year-round.

California’s Counties: The Basics

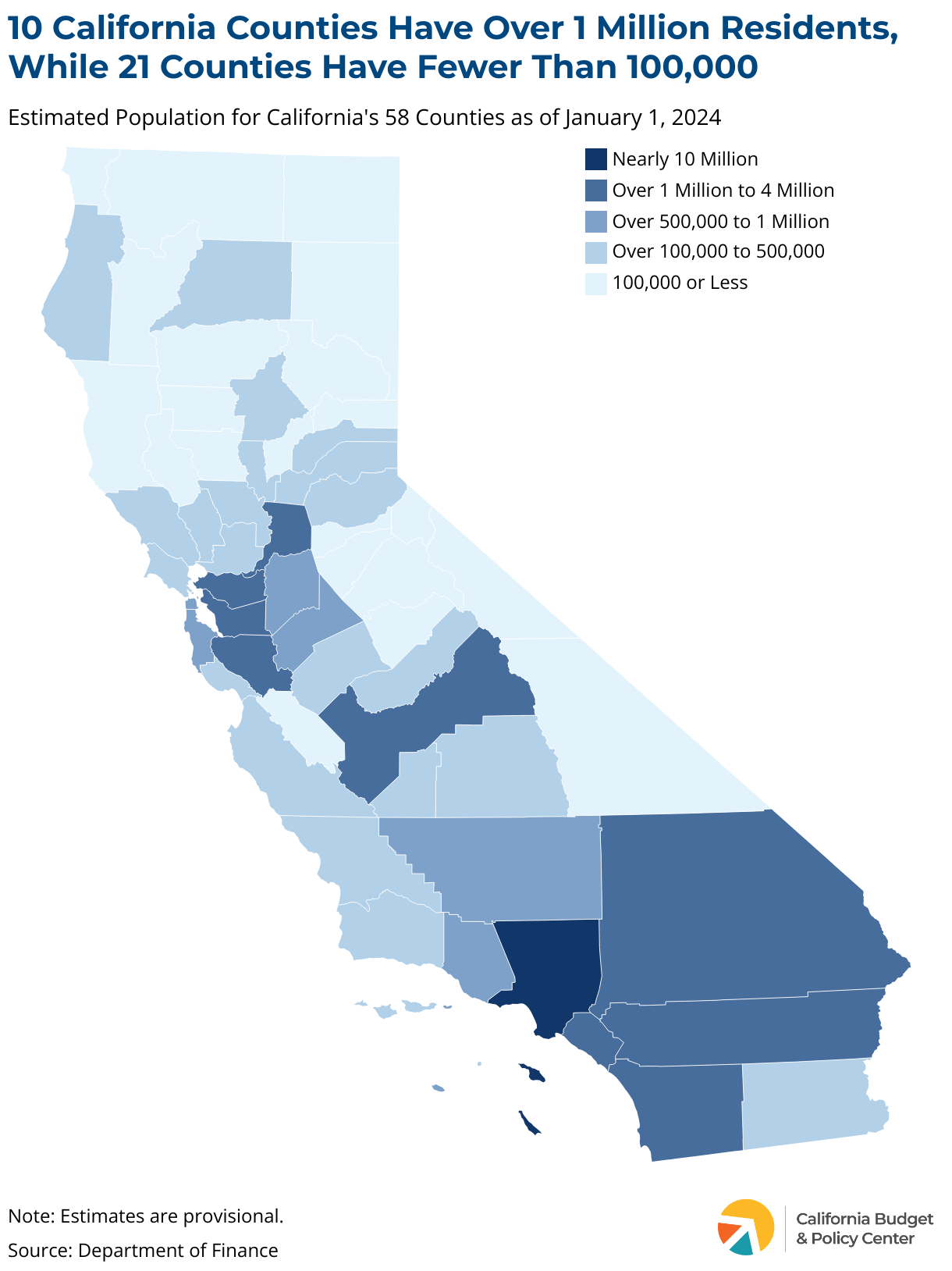

California Has 58 Counties That Vary Widely In Population and Size

California’s counties range widely in population.

- 10 counties have more than 1 million residents, and 21 counties have fewer than 100,000 residents.

- Los Angeles County has the largest population of any county in the state (9.8 million).

- Alpine County has the smallest population (less than 1,200).

California’s counties also differ considerably in size.

- San Bernardino is California’s largest county (20,057 square miles).

- San Francisco — which has the state’s only consolidated city and county government — is the smallest county (47 square miles).

California's Counties Are Legal Subdivisions of the State

California’s Constitution requires the state to be divided into counties. Counties’ powers are provided by the state Constitution or by the Legislature.

- The Legislature may take back any authority or functions that it delegates to the counties.

There are 44 general-law counties and 14 charter counties.

- Unlike general-law counties, charter counties have a limited degree of independent authority over certain rules that pertain to county officers. However, charter counties lack any extra authority with respect to budgets, revenue increases, and local regulations.

Counties Have Multiple Roles in Delivering Public Services

- Counties operate health and human services programs as agents of the state.

- Counties carry out a broad range of countywide functions.

- Counties provide some municipal-type services in unincorporated areas.

Other Types of Local Agencies Also Deliver Public Services

Counties provide public services alongside other agencies that operate at the local level. A wide array of local services are delivered by:

- More than 2,000 independent special districts, which provide specialized services such as fire protection, water, or parks.

- More than 900 K-12 school districts, which are responsible for thousands of public schools.

- More than 480 cities, which provide policing, fire protection, and other municipal services.

- More than 70 community college districts, which oversee 113 community colleges.

Counties Are Governed By an Elected Board of Supervisors

The Board of Supervisors consists of five members in all but one county.

- The City and County of San Francisco has an 11-member Board and an independently elected mayor.

Because counties do not have an elected chief executive (except for San Francisco), the Board’s role encompasses both executive and legislative functions.

- These functions include setting priorities, approving the budget, controlling county property, and passing local laws.

Boards also have a quasi-judicial role.

- For example, Boards may settle claims and hear appeals of land-use and tax-related issues.

A Number of Other County Officers Also Are Elected

Along with an elected Board of Supervisors, the state Constitution requires counties to elect:

- An assessor.

- A district attorney.

- A sheriff.

Although not required by the state Constitution, a few other key county offices are typically filled by election, rather than by Board appointment. These include:

- The auditor-controller.

- The county clerk.

- The treasure-tax collector.

The County Manager Oversees the Daily Operations of the County Government

The top administrator in each county is appointed by the Board of Supervisors.

- Counties have various titles for this position. This guide uses the generic term “county manager.”

- San Francisco, with an independently elected mayor, does not have a county manager position.

The county manager:

- Prepares the annual budget for the Board’s consideration.

- Coordinates the activities of county departments.

- Provides analyses and recommendations to the Board.

- May hire and fire department heads, if authorized to do so.

- May represent the Board in labor negotiations.

Key Facts About County Revenues and Spending

County Budgets Reflect State and Federal Policy Priorities and Local Policy Choices

To a large degree, county budgets reflect state and federal policy and funding priorities.

- As agents of the state, counties provide an array of services that are supported with state and federal dollars and governed by state and federal rules.

- This means that a large share of any county budget will reflect priorities that are set in Sacramento and in Washington, DC.

County budgets also reflect the policy and funding priorities of local residents and policymakers.

- Counties can use a portion of their locally generated revenues to fund key local services and improvements.

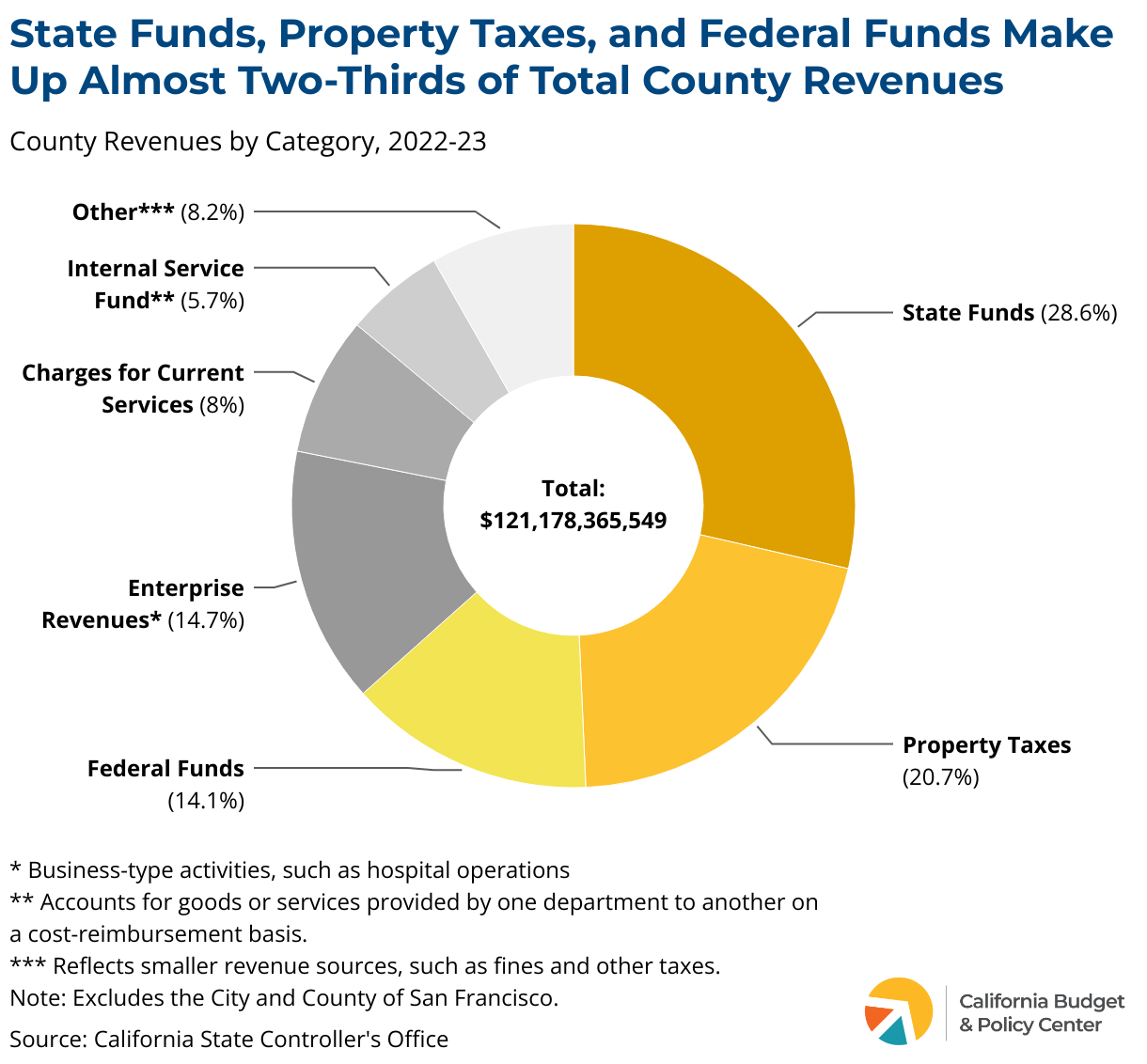

County Revenues = State Funds + Federal Funds + Local Funds

County revenues consist of state and federal dollars along with locally generated funds.

- State and federal revenues pay for health and human services, roads, transit, and other services.

- Local revenues, particularly property tax dollars, are important because they are mostly “discretionary” and can be spent on various local priorities.

In 2022-23, almost two-thirds of county revenues statewide came from the state government, the federal government, and local property taxes.

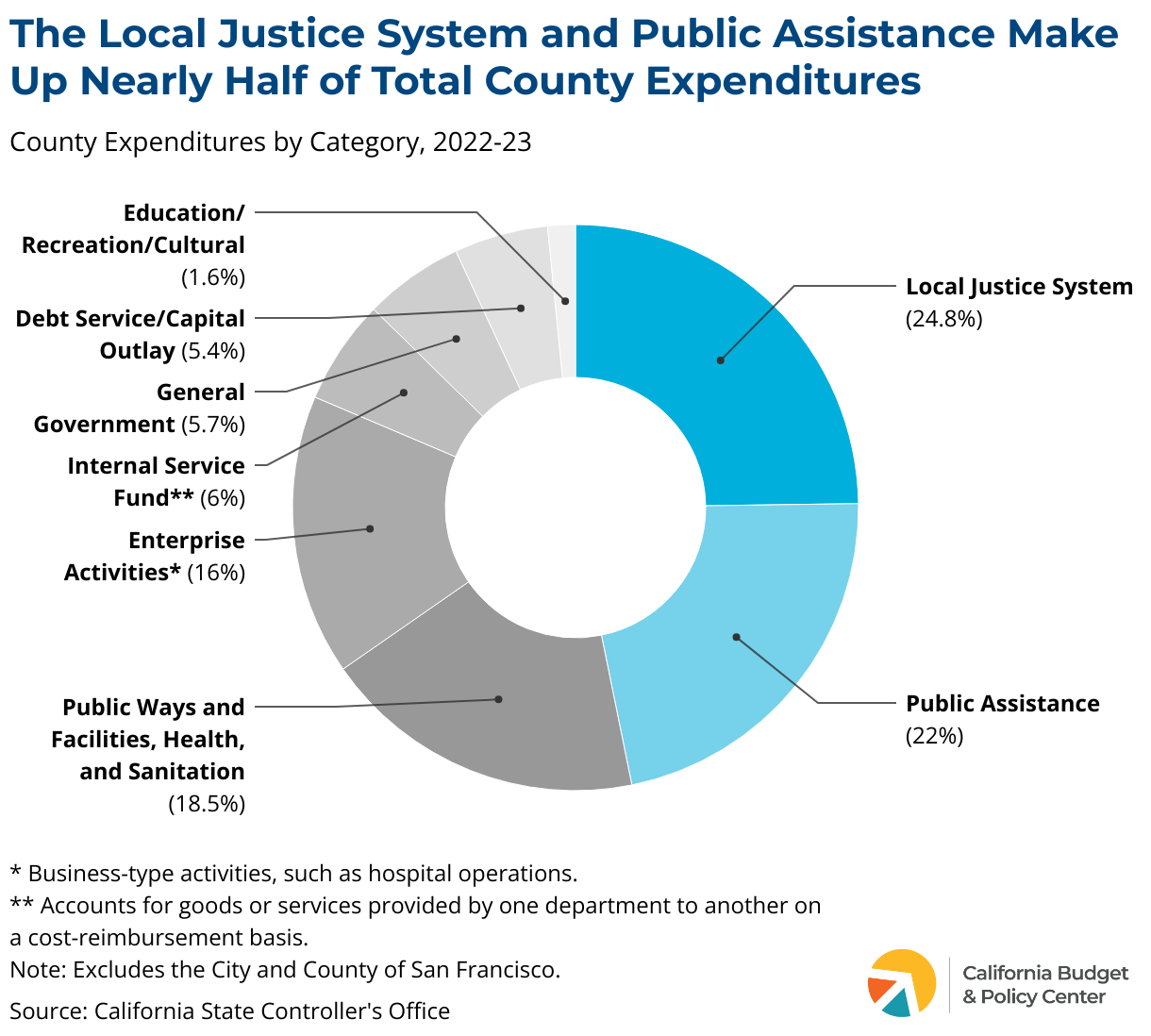

County Budgets Support a Broad Range of Public Services and Systems

In 2022-23, nearly half of all county spending across the state funded the local justice system or public assistance.

- The local justice system includes the district attorney, adult and youth detention, policing provided by the sheriff’s department, and probation.

- Public assistance includes spending on cash aid for Californians with low incomes, including families with children in the CalWORKs welfare-to-work program.

Large shares of county spending in 2022-23 also supported either 1) public ways and facilities, health, and sanitation (18.5%) or 2) enterprise activities (16%), which include airports, hospitals, and golf courses.

The State Rules That Determine Counties' Revenue-Raising Authority

State Rules Establish Counties' Authority to Raise Revenue

Counties can levy a number of taxes and other charges to fund public services and systems.

- The rules that allow counties to create, increase, or extend various charges are found in state law — as determined by the Legislature — as well as in the state Constitution.

Statewide ballot measures approved by voters since the late 1970s have constrained counties’ ability to raise revenues.

- These measures are Proposition 13 (1978), Prop. 62 (1986), Prop. 218 (1996), and Prop. 26 (2010).

Counties Can Increase the Property Tax Rate Solely to Pay for Voter-Approved Debt

Prop. 13 (1978) limits the countywide property tax rate to 1% of a property’s assessed value.

- Each county collects revenues raised by this 1% rate and allocates them to the county government, cities, and other local jurisdictions based on complex formulas.

- Revenues from the 1% rate may be used for any purpose.

Local jurisdictions may increase the 1% rate to pay for voter-approved debt, but not to increase revenues for services or general operating expenses.

- Most voter-approved debt rates are used to repay bonds issued for local infrastructure projects.

- At the county level, bonds must be approved by a two-thirds vote of both the Board of Supervisors and the voters.

Counties Can Raise Other Taxes, But Only With Voter Approval

In contrast to counties’ limited authority over property taxes, counties may levy a broad range of other taxes to support local services. These include taxes on:

- Retail sales.

- Short-term lodgings.

- Businesses.

- Property transfers.

- Parcels of property.

However, county proposals to increase taxes generally must be approved by local voters. These voter-approval requirements vary depending on whether the proposal is a “general” tax or a “special” tax.

Counties Also Can Levy Charges That Are Not Defined as "Taxes"

In addition to taxes, counties can establish, increase, or extend other charges to support local services. These are:

- Charges for services or benefits that are granted exclusively to the payer, provided that such charges do not exceed the county’s reasonable costs.

- Charges to offset reasonable regulatory costs.

- Charges for the use of government property.

- Charges related to property development.

- Certain property assessments and property-related fees.

- Fines and penalties

The state Constitution, as amended by Prop. 26 (2010), specifically excludes these charges from the definition of a “tax.”

Charges that are not defined as “taxes” can be created, increased, or extended by a simple majority vote of the Board of Supervisors. A countywide vote is not required.

However, Prop. 218 (1996) does require the Board of Supervisors to consult property owners regarding two types of charges.

- Property assessments, which pay for specific services or improvements, must be approved by at least half of the ballots cast by affected property owners, with ballots weighted according to each owner’s assessment liability.

- Property-related fees — except for water, sewer, and garbage pick-up fees — must be approved by 1) a majority of affected property owners or 2) at least two-thirds of all voters who live in the area.

The County Budget Process: State Rules and Local Practices

State Law Shapes the County Budget Process

Counties develop and adopt their annual budgets according to rules outlined in state law.

- Rules pertaining specifically to county budgets are found in the County Budget Act (Government Code, Sections 29000 to 29144).

- The Ralph M. Brown Act (Government Code, Sections 54950 to 54963) includes additional rules that county officials must follow when discussing official county business.

State law delineates:

- The process by which county budgets must be developed and shared with the public and the information that must be included in these budgets.

Local Practices Also Shape the County Budget Process

Counties have some discretion in how they craft their annual spending plans.

- For example, the Board of Supervisors may hold more public hearings than state law requires and/or convene informal public budget workshops. Some counties also begin developing their budgets earlier than others do.

Counties have some leeway in how they structure their budgets and share them with the public.

- County budgets may include more information and provide a higher level of detail than the state requires.

- Counties may make their spending plans and other budget-related materials widely accessible to the public in multiple formats, including online.

Three Versions of Annual County Budget

At all stages, the county budget must be balanced (funding sources must equal financing uses).

Counties Must Adopt Their Budgets Using One of Two Models

State law provides two models for adopting the annual county budget.

- One model — called the “two-step” model in this guide — requires the Board of Supervisors to first approve an interim budget by June 30 and then formally adopt the budget by October 2.

- The other model — called the “one-step” model in this guide — allows the Board to formally adopt the budget by June 30 of each year, with no need to first approve an interim budget. This alternative process was created by Senate Bill 1315 (Bates, Chapter 56, Statutes of 2016).

Each county decides which model to follow in adopting its annual budget.

Two-Step Model (Step 1): Board Approves the Recommended Budget By June 30

The Board of Supervisors must approve — on an interim basis — the Recommended Budget, including any revisions that it deems necessary, on or before June 30.

- The Board must consider the Recommended Budget, as proposed by the county manager, during a duly noticed public hearing.

- The Recommended Budget must be made available for public review prior to the public hearing.

- At this stage, the Recommended Budget is essentially a preliminary spending plan, which authorizes budget allocations for the new fiscal year (beginning on July 1) until the Board formally adopts the budget.

Two-Step Model (Step 2): Board Adopts the County Budget by October 2

The Board of Supervisors must formally adopt the county budget on or before October 2.

- On or before September 8, the Board must publish a notice stating 1) that the Recommended Budget is available for public review and 2) when a public hearing will be held to consider it. At this stage, the budget reflects the preliminary version

approved by the Board along with any changes proposed by the county manager. - The public hearing must begin at least 10 days after the Recommended Budget is made available to the public.

- The Board must adopt a balanced budget, including any additional revisions that it deems advisable after the public hearing has concluded, but no later than October 2.

One-Step Model: Board Adopts the County Budget by June 30

The Board of Supervisors must formally adopt the county budget on or before June 30, with no need to initially approve the Recommended Budget on a preliminary basis.

- On or before May 30, the Board must publish a notice stating that 1) the Recommended Budget (as proposed by the county manager) is available for public review and 2) when a public hearing will be held to consider it.

- The public hearing must begin at least 10 days after the Recommended Budget is formally released to the public, but no later than June 20.

- The Board must adopt a balanced budget, including any revisions that it deems advisable, after the public hearing has concluded, but no later than June 30.

County Budget Actions Require a Simple Majority Vote or a Supermajority Vote

State law allows the Board of Supervisors to make certain budget decisions by majority vote.

- These include approving the Recommended Budget and/or the Adopted Budget as well as eliminating or reducing appropriations.

However, a four-fifths supermajority vote of the Board is required for a number of budget actions, including to:

- Appropriate unanticipated revenues.

- Appropriate revenues to address an emergency.

- Transfer revenues between funds or from a contingency fund after the budget has been formally adopted.

- Increase the general reserve at any point during the fiscal year.

The Timeline of the County Budget Process

The County Budget Process is Cyclical and Interacts With the State Budget Process

County budgets are developed, revised, and monitored throughout the year.

Because counties perform functions required by the state and receive significant state funding, county budgets are shaped by state budget choices.

- County officials must take into account decisions made as part of the state’s annual budget process. Federal policy and funding decisions also affect county budgets.

The budget process varies somewhat across counties.

- For example, counties can hold more public hearings than required, and some counties start developing their budgets earlier than others do.

Appendix

How to Find Your County's Budget

Counties generally make their budget documents available on the internet.

- Online budget materials are typically located in a “budget and finance” section of the county’s website or the county manager’s webpage.

- Perhaps the fastest way to find a county’s budget is by using an internet search engine and entering a phrase like “Kern County budget.”

In addition, counties make their budget documents available in county buildings and local libraries.

Additional Resources

- California State Controller: Extensive county revenue and expenditure data.

- California State Association of Counties: Information on counties’ history, structure, and powers along with links to all 58 county websites.

- California Government Code, Sections 29000 to 29144: State rules governing the county budget process.

- Institute for Local Government: Resources to promote effective governance in California’s communities, including a section on budgeting and finance.

- National Association of Counties: Extensive data for all US counties.