Corporate profits have skyrocketed in recent years while workers’ wages have stagnated and families struggle to keep up with the rising costs of living. Despite these disparities, large tax breaks, such as the “Water’s Edge” loophole, remain in place. Big corporations have also benefited greatly from the 2017 Trump tax cuts and stand to receive more benefits from the federal tax package recently signed into law. Corporate tax breaks largely benefit corporate shareholders, who are disproportionately wealthy and white, widening economic and racial inequality.

California policymakers should ensure that profitable corporations pay their fair share in state corporate taxes — which represent a tiny share of their expenses — to support the public services that Californians need. This is especially urgent to help mitigate the harms of the harmful federal cuts to health care, food assistance, and other basic needs programs.

State leaders should end the state’s most costly corporate tax break — the water’s edge loophole, which allows corporations to avoid around $3 billion in California taxes each year and deprives the state of needed resources to address the most pressing concerns facing Californians.

As state leaders look to blunt the harm of the federal budget on Californians with low incomes and the state’s finances, it’s clear that California’s corporate tax structure is in need of repair. While large, profitable corporations benefit from new federal tax breaks, California policymakers must ensure these businesses pay their fair share in state taxes. There is no one-size-fits-all solution: different options can all complement each other. For example, limiting corporate tax credit usage will raise revenues by itself but will also prevent erosion of the revenue potential from ending the water’s edge loophole.

The Problem: Multinational Corporations Avoid Billions in State Taxes by Shifting US Profits Offshore

Large corporations that have affiliated companies outside of the US can use a variety of mechanisms to artificially shift hundreds of billions in US profits to foreign jurisdictions with low tax rates — known as tax havens — to reduce their federal and state taxes. In fact, corporations report to federal tax authorities that their profits in some well-known tax havens are multiple times larger than the entire economies of these places, indicating that most if not all of those profits are only there on paper.

As one example of how a corporation might accomplish this, a US corporation can transfer ownership of intellectual property like patents or trademarks to a foreign affiliate and pay the affiliate for the right to use them, effectively moving income off the books of the US corporation while keeping it within the larger corporate group. This is a tactic that industries such as tech and pharmaceuticals can easily employ, but corporations across the board have options to engage in offshore profit shifting and tax avoidance.

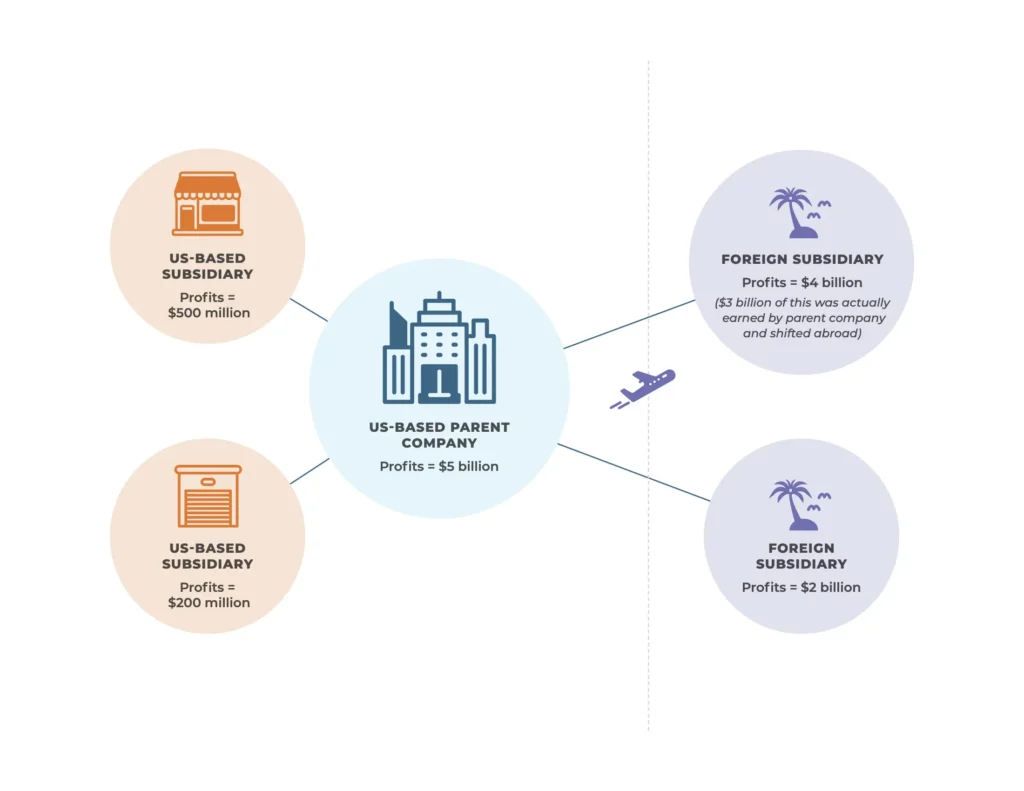

Corporations Can Greatly Reduce Profits Subject to Taxation — and Their Taxes — by Shifting Profits Abroad and Using the Water’s Edge Election

CORPORATE GROUP TOTAL PROFITS

If the example corporation above uses the default Worldwide Combined Reporting method, all worldwide profits are included: $5B + $500M + $200M + $4B + $2B = $11.7 Billion.

If the corporation chooses to use Water’s Edge Election, only domestic profits are included (yellow oval): $5B + $500M + $200M = $5.7 Billion.

Note: This is a simplified example.

California’s “water’s edge election” allows corporations to choose whether or not to include the profits of their foreign affiliates when they report their total profits that can be divided up among, or “apportioned” to, the states where they are subject to tax.1Additionally, while some groups of related corporations may elect to file a group tax return in California, each corporation may file separate returns but are still required to combine profits at the corporate group level first, before apportioning profits between taxing jurisdictions and individual corporate entities.Generally, profits are apportioned to states by multiplying the total profits by the “sales factor”, which is determined by dividing the corporation’s sales into the state by its total sales. For filers electing the water’s edge method, the denominator is only domestic sales.

The water’s edge election creates several issues:

- Smaller, domestic businesses likely pay higher shares of their income in taxes than large multinational corporations because they are unable to shift profits overseas.

- Giving corporations the option of two filing methods means they will always choose the one that lowers their tax bill. For corporations with significant offshore profits, the water’s edge method will likely result in lower taxes. If corporations have domestic profits and foreign losses, using the “worldwide combined reporting” method — where all worldwide profits and losses are combined — would result in a lower tax bill.

- Allowing corporations to ignore foreign profits can encourage them to shift profits to foreign tax havens and avoid state taxes by using the water’s edge election.

Maintaining the water’s edge election will cost the state an estimated $3.1 billion in 2024-25, increasing to $3.5 billion by 2026-27, according to the Department of Finance.

The Solution: Close the Water’s Edge Loophole and Require Worldwide Combined Reporting

Requiring large multinational corporations to use the worldwide combined reporting method would eliminate the state tax benefit of shifting profits abroad and close this loophole, resulting in additional revenue for California. Under this method, corporations are required to include the income of all their domestic and foreign affiliates in their total profits before determining what share is taxable by each state. This is already the default tax filing method for corporations subject to tax in California that don’t elect the water’s edge method, so some corporations currently use this method when it is beneficial for them.

In tandem with requiring worldwide combined reporting, policymakers could take steps to prevent corporations from underreporting their sales into California, driving down the “sales factor” used to determine the share of their profits that can be taxed in California, and ultimately reducing their state taxes. For example, policymakers can clarify state law to ensure corporations report the final destination of their sales — not the location of intermediaries — for the purpose of the sales factor, and require more robust reporting on the locations of sales to allow tax authorities to better identify cases when a corporation may be underreporting. This is a reform that should generate additional revenue on its own, but would also help prevent the erosion of revenues that could be gained from requiring worldwide combined reporting, as requiring corporations to report their global profits may lead them to find other ways to reduce their California tax bill, like underreporting sales into the state.

Ending the water’s edge loophole for large corporations and requiring worldwide combined reporting is a common-sense reform to ensure corporations contribute a fair share of their profits in California taxes to support the state services and infrastructure that allow companies, their workers, and their consumers to thrive.

Want to Better Understand

the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.