Corporate profits have soared in recent years, especially among a small share of large corporations. Yet because California does not have a graduated corporate income tax, large corporations pay the same tax rate as smaller ones and often have more resources to exploit tax loopholes.

Big corporations have also benefited greatly from the 2017 Trump tax cuts and are poised to receive more benefits from the federal tax and budget bill recently enacted by the Trump administration and congressional Republicans. Large tax breaks for corporations widen economic and racial inequality because they largely benefit corporate shareholders, who are disproportionately wealthy and white.

At the same time, workers’ wages have stagnated, families struggle to keep up with the rising costs of living, and funding for federal programs like Medicaid and food assistance have been slashed.

California policymakers can ensure that profitable corporations pay their fair share in state corporate taxes — which represent a tiny share of their expenses — to support the public services that Californians need and help mitigate the harms of federal cuts to health care, food assistance, and other basic needs programs.

One option for state leaders is to modify the state’s flat corporate tax rate to apply higher tax rates to corporations with higher profit levels, similar to California’s progressive tax system for personal income taxes. State leaders could either establish a single surtax on profits above a certain threshold or transition to a graduated tax rate with several brackets.

As state leaders look to blunt the harm of the federal budget on Californians with low incomes and the state’s finances, it’s clear that California’s corporate tax structure is in need of repair. While large, profitable corporations benefit from new federal tax breaks, California policymakers must ensure these businesses pay their fair share in state taxes. There is no one-size-fits-all solution: different options can all complement each other. For example, limiting corporate tax credit usage and ending the “water’s edge” loophole will make it harder for profitable corporations to avoid their tax liability from an increase in their corporate tax rate.

MORE IN THIS SERIES

To learn more about the water’s edge election, net operating losses, tax credits, corporate tax rates, and options for common-sense reform, see the other fact sheets in this series:

Corporate Profits are Highly Concentrated, Yet Corporations are Taxed at the Same Rate Regardless of Profit Level

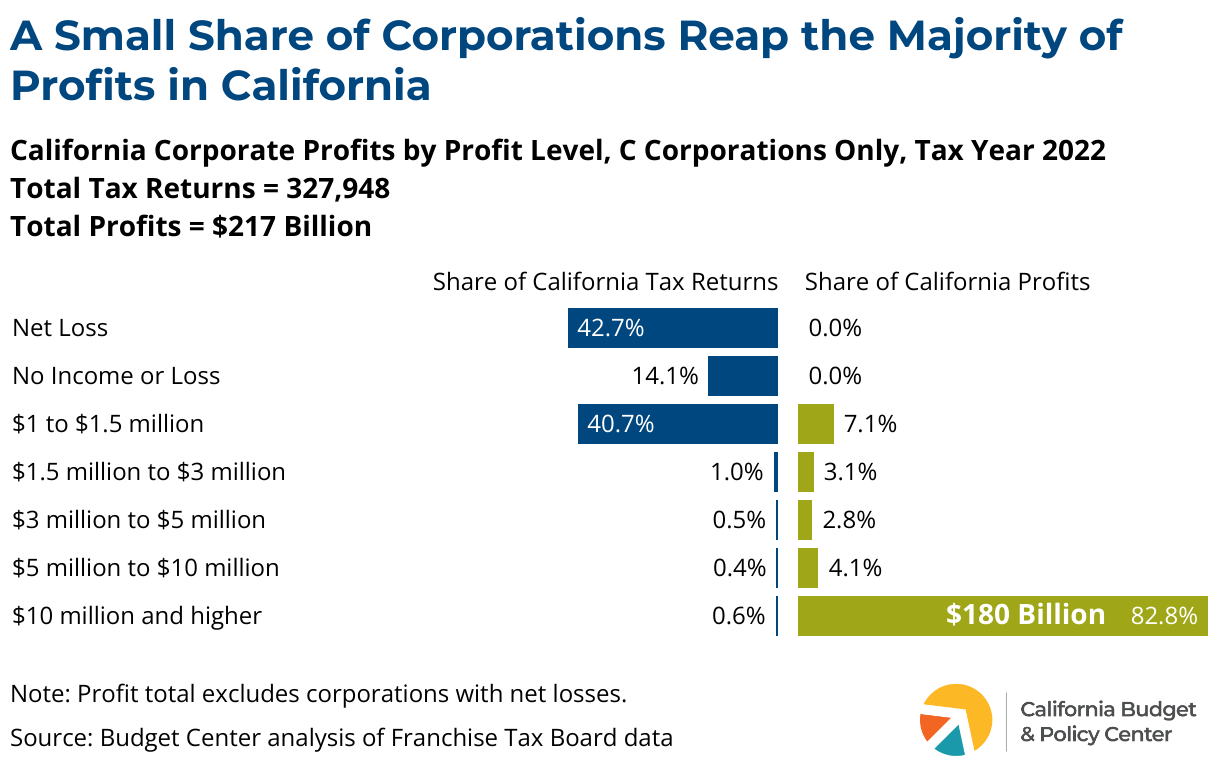

Unlike the state’s personal income tax system, which is a graduated tax structure with higher rates applied to higher levels of income, the state’s corporate tax system applies the same tax rate regardless of profit level. But the lion’s share of profits is earned by a small number of large corporations. In 2022, “C corporations” with at least $10 million in California profits received more than four-fifths of the total profits in the state — $180 billion in the aggregate — while making up less than 1% of tax returns for all C corporations (see box describing types of corporations).

Types of Corporations and their California Tax Rates

There are two main types of corporations for tax law purposes: C corporations and S corporations, so named for the sections in the federal tax code governing them.

C corporations

C corporations are taxed on their profits at the business level. Their owners are subject to personal income tax when they receive corporate distributions as dividends and when they sell shares of corporate stock. Large corporations that trade their shares on public stock exchanges are organized as C corporations. In California, C corporations are subject to an 8.84% tax rate regardless of profit level.

S corporations

S corporations are not subject to federal tax at the business level, but their profits (or losses) are passed through to the individual shareholders, who pay federal and state taxes on their shares of business income through the personal income tax, whether or not that income is distributed to them as payments. S corporations have a limited number of shareholders and their stock is not traded on public stock exchanges. In California, S corporations are also subject to a 1.5% tax at the business level.

Other California Business Types and Their Taxes

In addition to the regular state rates, there is an additional 2% tax on banks and other financial institutions — both C corporations and S corporations — because these corporations are exempt from certain local taxes.

Some businesses — including most small businesses — are not structured as corporations and pay no business-level taxes. Like S corporations, the individual owners of these businesses pay taxes on their business income (and are thus known as “pass-through” businesses). However, these businesses are not subject to an income tax at the business level and are not included in state corporate tax data.

These businesses can be organized as sole proprietorships (for example, a typical “mom-and-pop shop”), partnerships (for example, many law firms, medical practices, and other professional service firms), or limited liability companies (LLCs). Some of these business types are subject to the state’s $800 minimum tax, and LLCs are subject to a capped, tiered fee based on income level.

Learn more about California’s taxation of various business types from the Franchise Tax Board.

Policymakers Can Require Greater Tax Contributions from Top-Earning Corporations

In contrast to California’s flat corporate tax system, thirteen other states already have graduated corporate tax systems with multiple rates based on profit levels. Notably, in recent years, New York and New Jersey lawmakers have approved or extended surtaxes (additional taxes beyond regular tax rates) on the most profitable corporations in those states. New York applies a tax rate to corporations with state profits of more than $5 million that is 0.75% higher than the regular corporate tax rate. In comparison, New Jersey applies a 2.5% surtax on the state profits of corporations with profits above $10 million in the state.

Some California policymakers proposed a two-rate corporate tax system in 2023; this proposal would have increased the 8.84% C corporation tax rate to 10.99% on California taxable income above $1.5 million and decreased the rate to 6.63% on taxable income up to $1.5 million. The tax rate for S corporations would have been reduced from 1.5% to 1.125% on taxable income up to $1.5 million. At the time, it was estimated that a total of around 2,500 corporations would have seen a tax increase and that the increased rate would have raised around $6 billion annually, falling to around $4 billion annually after accounting for the revenue losses from the proposed lower rate on lower income levels.

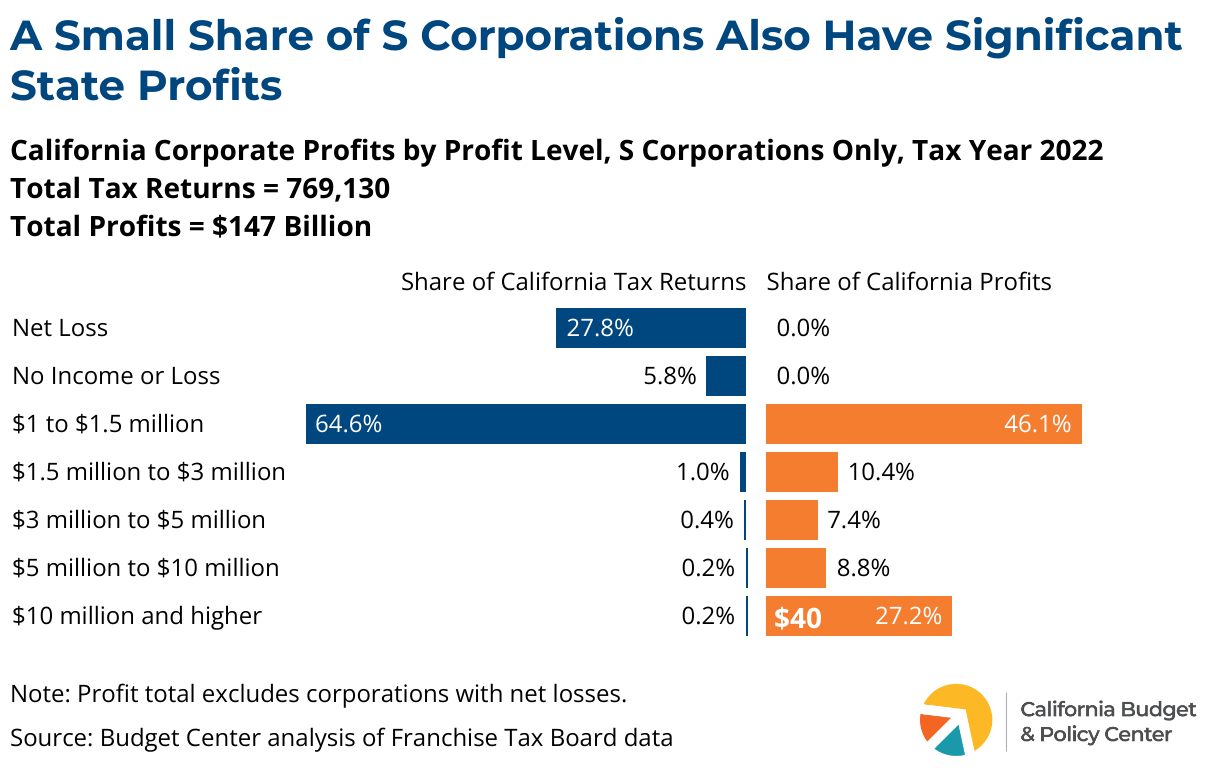

While the 2023 proposal excluded S corporations from a rate increase — and while S corporation profits are less concentrated among the largest corporations than C corporation profits — there are large and profitable S corporations as well. In 2022, there were more than 13,000 S corporations with California profits of at least $1.5 million, representing just 1.8% of S corporations and receiving more than half of S corporation profits in the state. Policymakers could raise additional revenue by applying a higher rate on very profitable S corporations as well.

Finally, if policymakers pursue corporate tax rate changes, it is also critical to pair this with other corporate tax changes to reduce the ability of corporations to avoid the tax increase, which can significantly reduce the revenue potential of increases to the tax rate alone. Namely, policymakers should also address corporations’ use of offshore tax havens by eliminating the water’s edge loophole and put reasonable annual limits on business tax credits and deductions. These actions will help ensure corporations contribute a fair share of their profits in California taxes to support the state services that allow companies, their workers, and their consumers to thrive.