- Introduction

- Wealth Is Critical to Economic Security and Mobility, but Access Varies by Race and Ethnicity

- The Path to the Racial Wealth Gap

- Key Factors Contributing to the Growing Wealth Divide

- Key State Policies to Address the Racial Wealth Gap

- The Future of Wealth

- Appendix

View the PDF version of this report.

Introduction

In the years since the 2007 Great Recession, economic commentary has veered between hailing the subsequent recovery and sounding the alarm about rising inequality. Income inequality is often identified as a sign of both the country’s underlying economic troubles and public policies that disproportionately benefit the wealthy. An alternative indicator of the nation’s social and economic health pertains to wealth, specifically the growing wealth gap among people of different races and ethnicities.[1] This report illuminates the racial wealth gap, explores its underlying historical context, discusses some key factors driving the wealth gap, and lays out a set of public policies that could put California and the nation as a whole on a better path to building wealth for millions of families.

Wealth Is Critical to Economic Security and Mobility, but Access Varies by Race and Ethnicity

Building wealth is a crucial factor in promoting generational economic mobility and opportunity. Commonly measured in terms of net worth — the difference between gross assets and debt — wealth provides families with financial security. The greater a family’s net worth, the more resources they have to weather costly unexpected events, pay for higher education, take risks on a business, purchase a home, and invest in other wealth-generating assets. Moreover, wealth can be transferred to the next generation through financial gifts or inheritances.

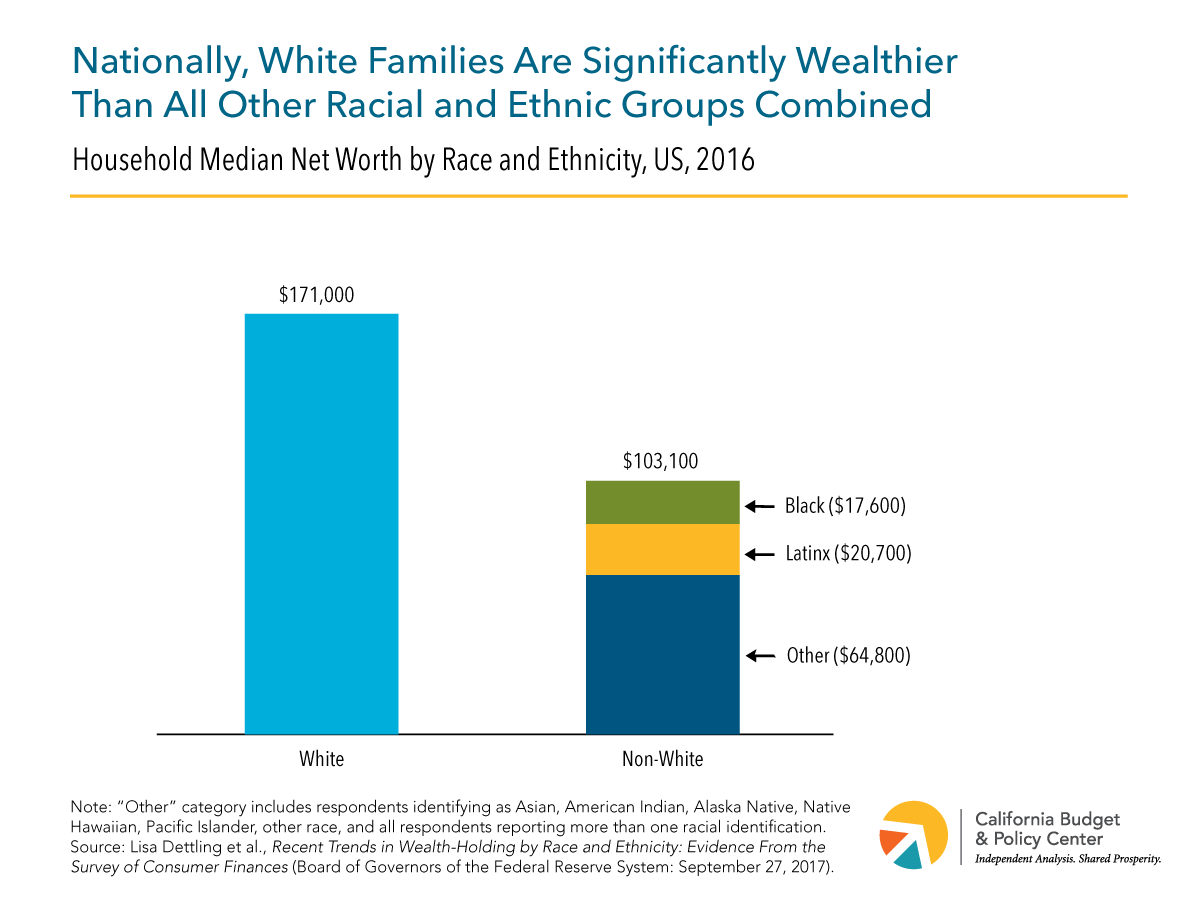

Income inequality has been extensively documented at both the state and national levels. Unfortunately, wealth inequality is even starker than income inequality. The top 1% of Americans took home 24% of all income, but they also had 39% of all wealth in 2016.[2] However, wealth is not only inequitably distributed across the income spectrum. It is also unfairly allocated among people of different races and ethnicities. For example, in 2016, the typical — or median — white family’s wealth nationally was $171,000 (Figure 1).[3] For black families, median wealth amounted to $17,600, or roughly 10% of that for white families. For Latinx families, median wealth was $20,700, or about 12% of that for white families. Put another way, the typical white household has $9.72 in wealth for every $1 that a typical black family has and $8.26 in wealth for every $1 that a typical Latinx family has.

National data show that this wealth disparity is not simply explained by racial and ethnic differences in income. Though one might expect that those with greater income would also have greater wealth, the data indicate that this is not the case. In 2014, black households in the middle of the income distribution had $22,150 in median net wealth, far less than did whites in the second lowest 20% of the distribution ($61,070) and only somewhat greater than that of whites in the bottom quintile ($18,361).[4]

Data specific to the Los Angeles area highlights wealth inequality at the local level in California (Figure 2).[5] In 2014 in Los Angeles and Orange counties, US-born whites had a much higher median household net worth ($355,000) than did most non-whites, including Latinx households ($46,000) and US-born blacks ($4,000). At the same time, among non-white groups, Japanese ($592,000), Asian Indian ($460,000), and Chinese ($408,200) households had greater median net worth than whites. The variation among Asian groups may reflect differing socioeconomic histories and migration patterns, and it echoes findings of substantial wealth inequality among Asian American communities in the United States.[6] These racial and ethnic differences reveal how some groups are better positioned to make the kinds of critical investments in their futures that benefit their families and the broader community.

Weathering adverse events is more challenging for households that lack sufficient wealth. When families face financial setbacks such as job loss or unexpected expenses, liquid assets — which can be converted easily to cash, such as money in the bank — offer a needed financial cushion. Unfortunately, many black and Latinx families across the country do not have enough liquid wealth to absorb sudden shocks. Nationally, blacks in 2011 had only $25 in median liquid wealth, and Latinx residents had just $100.[7] In contrast, the typical white family had $3,000 in assets that they could quickly convert to cash if needed. In the Los Angeles area, the median value of liquid assets for white households in 2014 was $110,000, compared to $200 for US-born blacks, $0 and $7 for Mexican and non-Mexican Latinx households, respectively, $500 for Vietnamese, and $245,000 for Asian Indians.[8] Moreover, while the majority of American families own some wealth, too many have zero or negative net worth (indicating more debt than assets). This problem also varies by race and ethnicity, with far fewer white households nationally (9%) having no wealth in 2016 than did black (19%) or Latinx households (13%).[9]

Families with greater wealth are better positioned to be able to transfer resources to family or friends. In addition to having more wealth, whites generally are better able to rely on their social networks during hard times. In 2016, more than 7 in 10 white families expected that they could get $3,000 from friends or family during a financial emergency, with less than half of black and Latinx households reporting the same.[10]

These disparities are not a natural occurrence nor are they due to the individual failings of people of color. Rather, as the next section points out, there are structural problems deeply rooted in our nation’s long history of racism, which has infused every aspect of our economy and which our nation has failed to fully remedy.

The Path to the Racial Wealth Gap

Why Is There a Racial Wealth Divide?

The roots of the racial wealth divide can be found in racist policies and practices dating back to our nation’s early days. Under the institution of chattel slavery, enslaved Africans were valuable assets whose labor generated wealth for their white owners. After emancipation, blacks worked as landless tenant farmers and sharecroppers. They were also largely shut out of the Homestead Acts, through which the federal government gave approximately 246 million acres to homesteaders — land that was the original source of family wealth for about one-quarter of the US adult population by 2004.[11] Public land acquisition and private land ownership were often explicitly restricted by race. White expansion westward depended on the displacement of Native Americans from their territories and in many states — including California — land ownership was limited to citizens, precisely to discriminate against non-whites ineligible for citizenship.[12]

In the period following the Great Depression and World War II, US policy substantially restricted communities of color from benefiting from the wealth-building policies that helped grow the American middle class. Housing was a key area in which both public policy and private actions clearly advantaged whites. From 1934 to 1968, the Federal Housing Administration (FHA) financed mortgages to expand homeownership, but also deliberately created segregated white neighborhoods to keep out “incompatible racial element[s].”[13] Federal policies also harmed black neighborhoods by excluding many residents of these areas from eligibility for government-backed loans and mortgages and discouraging lending to people of color by designating their neighborhoods as bad credit risks. Nationally, due to the FHA’s underwriting practices, just 2% of government-backed mortgages during this period (1934 to 1968) went to homebuyers of color.[14] These practices helped whites build assets, reduced home values in non-white neighborhoods, and pushed would-be homebuyers of color into predatory land contracts that systematically stripped wealth from their communities.[15] While the Fair Housing Act of 1968 banned racial discrimination in housing rentals and sales, it initially carried no real federal enforcement mechanism for discrimination claims, light penalties for violators, and high burdens for victims of discrimination.[16] Additionally, due to political resistance to desegregation, the Department of Housing and Urban Development often avoided exercising or outright obstructed its legal mandate to affirmatively promote integration, thus entrenching these inequalities.[17] Today, housing discrimination remains a barrier for people of color, who are recommended and shown fewer housing units than are equally qualified whites.[18]

The Racial Wealth Gap Has Widened in Recent Decades

Due to a long history of discrimination, the racial wealth gap has been an ever-present feature of American economic life. Yet over the past several decades, this disparity has worsened. Although black and Latinx households saw their net worth rise incrementally, albeit fitfully, from 1983 to 2007, the net worth of white households was still steadily outpacing these gains.[19] Unfortunately, the Great Recession and the housing crisis reversed the gains made by black and Latinx families, rolling back a generation’s worth of progress.

The recession hit Americans hard; from 2007 to 2010, median net worth for all racial and ethnic groups dropped by about 30%.[20] However, for people of color, the pain did not end there. While white families’ net worth stabilized in the immediate aftermath of the downturn (2010 to 2013), black and Latinx families continued to see their wealth decline by an additional 20%.[21] Latinx and Asian American households were disproportionately hurt by the foreclosure crisis, as they were far more likely to live in one of the five states that were hardest hit, including California.[22] Though median net worth has since risen for all groups, the racial wealth divide has continued to increase. From 2013 to 2016, median net worth for Latinx and black families rose 30% to 50%, respectively, compared to an increase of 17% for white families.[23] Despite these gains, the white-black wealth gap still increased by 16% and the white-Latinx gap rose by 14% during the same period.

Exacerbating the racial wealth divide is the nation’s current wealth-building incentive structure. The federal government subsidizes savings and investment through certain tax benefits — including tax credits, deductions, exclusions, and preferential rates — which do not show up on the federal government’s balance sheet but still count as public spending.[24] These subsidies perpetuate inequality by favoring those who are already wealthy, with the top 20% of earners receiving most of the benefits.[25] With the exception of tax credits, these tax breaks are more likely to benefit white households, which disproportionately belong to the top 20%.

Just as wealth is distributed unevenly, so are practices that strip wealth from communities. In the years leading up to the foreclosure crisis, predatory lenders made subprime mortgage loans — which have higher interest rates, fees, and penalties — irrespective of borrowers’ ability to repay. People of color, especially women, were particularly targeted by subprime lenders for bad mortgages even when they qualified for better loans, with black, Latinx, and Asian Pacific Islander women more likely to receive subprime mortgages than whites.[26] When the mortgage market crashed, these households lost substantial wealth. Payday lenders, which offer short-term, high-cost loans with excessive interest rates that borrowers must repay quickly, present another obstacle to wealth-building for communities of color.[27] Lenders tend to be concentrated in neighborhoods of color, and 60% of borrowers are women, particularly Latinx and black women.[28] These borrowers are often living paycheck to paycheck and use these loans to cover basic needs. They can become trapped by debt, taking out new loans with increasing fees to pay the previous loan. As a result of this “loan churn,” only 14% of borrowers can repay their loans within the short-term window and half of all loans are extended over 10 times.[29] In California, 83% of the total payday loan transactions in 2016 were for subsequent transactions by the same borrower and 79% of these subsequent loans were made within a week of the previous loan, the majority on the same day.[30]

Key Factors Contributing to the Growing Wealth Divide

Many factors are driving the growth of the racial wealth gap. This section examines three key causes: housing, unemployment and the labor market, and higher education.[31]

Unequal Access to Homeownership and Affordable Housing

Throughout the US as well as in California, housing has become unaffordable for many families, whether they own or rent their homes. In 2015, more than 4 in 10 California households had unaffordable housing costs, meaning these costs exceeded 30% of household income.[32] More than 1 in 5 households statewide faced severe housing cost burdens, spending more than half of their income on housing. This affordability crisis predominantly affects Californians of color. Among all of the state’s renters paying more than 30% of their income toward rent, more than two-thirds (68%) were people of color and nearly half (46%) were Latinx.[33]

For those who own their homes, a house is often a family’s greatest investment, and it represents the largest single segment of their wealth portfolio. Among all homeowners, housing comprised about 30% to 40% of their assets in 2016.[34] Historically less able to access homeownership, black and Latinx Americans have lower homeownership rates than whites. Nationally, more than 7 in 10 white households (73%) own their homes, compared to less than half of Latinx and black households.[35] In California, where homeownership rates are lower than the national average, more than 6 in 10 whites (63%) own their homes, while only one-third of blacks and about 4 in 10 Latinx Californians (42%) are homeowners (Figure 3).[36] In Los Angeles and Orange counties specifically, over two-thirds of whites were homeowners in 2014, which was significantly greater than the homeownership rate for most other racial and ethnic groups.[37]

Racial disparities in housing wealth account for a substantial share of the wealth divide. According to one study, the number of years a household owned their home explained 27% of the growth in the racial wealth gap between blacks and whites from 1984 to 2009.[38] Whites are more likely to receive family assistance in making a down payment on a home and generate housing wealth years earlier than black and Latinx families. Even among homeowners, a substantial racial wealth gap exists: black and Latinx homeowners still see lower returns to homeownership. In 2016, net housing wealth among homeowners was $215,800 for white families, compared to only $94,400 for blacks and $129,800 for Latinx families.[39] Greater access to assistance from family means that white buyers are more likely to be able to make a down payment earlier in their lives as well as to make more sizable down payments, which leads to lower interest rates and lending costs.[40] Additionally, because of the legacy of residential segregation, blacks tend to own homes in majority black neighborhoods, and these homes do not appreciate at the same rate as those in largely white neighborhoods.[41]

Given these deep disparities, some researchers argue that in order to help people of color build housing wealth on par with whites, increasing both homeownership rates and returns is key.[42] If black and Latinx families owned their homes at the same rates as whites, the wealth gap would decrease by 31% and 28%, respectively.[43] Separately, equalizing returns to homeownership would reduce the black-white wealth gap by 16% and the Latinx-white gap by 41%.

Higher Unemployment and Unequal Access to Well-Paying Jobs With Benefits

Earned income and employer-provided benefits are an important source of economic security for many American households. Taken together, unemployment and household income explain almost 30% of the growth in the white-black wealth gap.[44]

Across all levels of education, the unemployment rate for blacks is higher than for whites.[45] Equal rates of employment would not be enough to eliminate the racial wealth divide, as white families with an unemployed head of household possess five times the wealth of black families headed by a person who works full-time.[46] Clearly, people of color remain at a disadvantage in the labor market even when they are employed. Furthermore, black and Latinx workers are less likely to hold higher-paying jobs that offer key benefits like retirement plans, health coverage, or paid leave, all of which are important for wealth-building.[47] This insecurity may affect women of color to an even greater extent. They face a “larger wage gap, greater job segregation, higher rates of unemployment, and primary caregiving responsibility” than do white women.[48] Latinx and black women are less likely than white women to have employers who offer retirement plans, and women in general are more likely than men to work part-time or low-wage jobs that restrict access to wealth-building benefits.[49]

The Heavier Burden of Higher Education Costs

Having at least a college degree is increasingly tied to greater economic security. Workers with a college degree have higher lifetime earnings than those with only a high school diploma and are more likely to be stably employed in a job with benefits.[50] Californians with a bachelor’s degree can expect more than double the average annual earnings of those with only a high school diploma.[51] Increasing access to higher education is also beneficial for the state. Some research suggests that the lifetime return to the state per graduate with a bachelor’s degree is over $200,000.[52] However, state investments in public higher education lag far below pre-recession levels.[53] Over the years, spending cuts have shifted the cost of higher education from the state to students and their families through increased tuition and fees.

Yet not all families can support their children’s education equally. In 2013, whites were more than twice as likely as blacks to receive financial help from their parents for higher education.[54] This disparity in financial support is not due to a difference in parents’ supportiveness of their children’s postsecondary education. Indeed, research indicates that black parents are more likely to spend a larger share of their resources on their children’s education.[55] Those black parents who support their children financially have less wealth and income than white parents who provide no financial support. However, in general, black families simply have less wealth to leverage toward the cost of an education.

Families may consider financial aid, but that assistance is not always available or sufficient. In California, low- and middle-income students turn to Cal Grants, which are the foundation of California’s financial aid program.[56] Only 16% and 25% of very low-income black and Latinx students in California, respectively, receive a Cal Grant award.[57] The vast majority of black and Latinx students who do receive state financial aid get the Cal Grant B access award, which is intended to help low-income students pay for basic expenses yet has not kept pace with the state’s rising housing costs.[58] The federal Pell Grant has also eroded in value, failing to keep up with rising costs of college attendance.[59]

Disproportionately burdened by rising tuition and fees, facing insufficient financial aid, and less able to rely on family resources, low-income students as well as students of color are more likely to face economic barriers to completing their degrees. These students often have to employ a range of coping strategies that impede their academic progress, including enrolling part-time, dropping courses, skipping semesters, or taking a job to cover expenses.[60] They also are more likely to take on debt to finance their education. Among all households, black families are more burdened by student debt than are white families. Over half (54%) of all black households headed by those ages 25 to 40 have student debt, compared to 39% of their white counterparts.[61] For Latinx households, just over 1 in 5 (21%) have student debt, likely due to lower rates of college attendance and attainment. Black borrowers also tend to owe more than white borrowers and both black and Latinx borrowers are more likely to take out riskier private loans.[62] This debt burden can be an obstacle to attaining a degree, as black and Latinx student borrowers are more likely to drop out.[63] As a result, they lack access to the relative labor market stability and asset-building opportunities that come with a college degree.

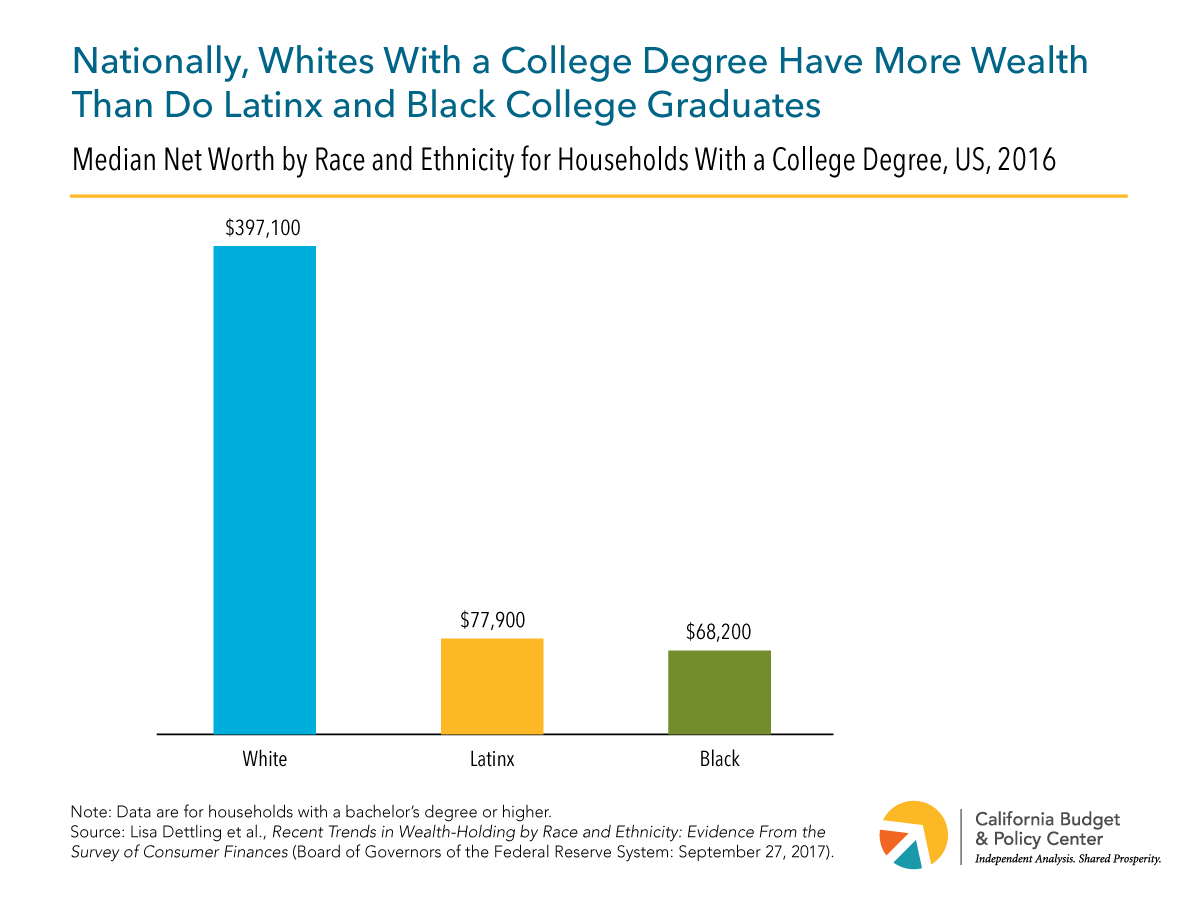

Yet while higher education is associated with greater earning potential, boosting the number of black and Latinx students who attain a degree in and of itself will not eliminate the wealth divide. In part due to debt payments, higher risk of default, and disparate experiences in the labor market, black and Latinx graduates do not see returns to their education that are equal to those of their white peers. At every level of educational attainment, black and Latinx families have less median wealth than their white peers. Not only do white college graduates hold more than five times the wealth of black and Latinx graduates, but even whites without a degree are wealthier (Figures 4 and 5).[64] Nor does the disparity disappear for those who received parental financial support for a degree, which is associated with degree completion but does little to reduce racial gaps in income or net worth.[65] In short, attaining a degree does not necessarily protect graduates of color from debt burdens or the discriminatory policies and practices that contribute to the racial wealth gap over the course of a lifetime.

Key State Policies to Address the Racial Wealth Gap

The research on wealth overwhelmingly concludes that individual achievement is not sufficient to overcome growing racial and ethnic wealth inequalities. Given the important role of public policy in fostering both an American middle class and the racial wealth divide, closing the wealth gap will require a new approach to public policy at both the state and national levels. This section suggests some state-level policy changes that could increase wealth for communities of color and decrease the disparity between whites and other groups.

The Need for Action: Four Key Policies to Build Wealth

1. Create a state-level estate tax

An estate tax is levied on large accumulations of wealth that are transferred from the estate of people who have died to their beneficiaries.[66] Ideally, the US would have a robust estate tax that would reduce wealth accumulation, with the proceeds invested in wealth-building strategies designed to level the playing field for all Americans. However, the federal estate tax has been weakened dramatically since the late 1990s to the point that nearly all estates are exempt from this tax.[67] Most recently, the Tax Cuts and Jobs Act of 2017 raised the exemption from the federal estate tax to more than $10 million per person.[68] This change will further concentrate wealth among families that are already highly advantaged. California should create its own estate tax, joining 18 other states and the District of Columbia that tax inherited wealth.[69] With such a tax, California could both reduce wealth disparities and use the resulting revenues — potentially in the billions per year — to fund wealth-building policies or other public investments that would benefit the vast majority of Californians.[70]

2. Support homeownership for low-income Californians

To ease the burdensome housing costs and help Californians build wealth, state policymakers can further help low-income Californians become homeowners, which could benefit Californians of color. One option is to invest in shared equity programs, which offer subsidies to lower the initial costs of a home for new buyers.[71] When homeowners sell their home, a portion of the proceeds is reinvested in the program, allowing future low-income buyers to afford a home and keeping the program sustainable. California could significantly invest in affordable homeownership by providing funding for shared equity housing for those otherwise priced out of the housing market and tie funds to long-term affordability requirements. Local governments and nonprofits could be responsible for monitoring units and resales, and offering support to homeowners.

To help fund this investment, California should consider eliminating the state mortgage interest tax deduction. The deduction allows households to reduce their taxable incomes by the value of qualified mortgage interest expenses paid on up to $1 million in debt and primarily benefits wealthy homeowners.[72] This tax break exacerbates racial and ethnic disparities, with white families not only more likely to own homes, but also to have more valuable homes.[73] Eliminating the deduction would both make California’s tax code more equitable and yield substantial revenue for shared equity programs.[74]

3. Create debt-free public higher education for low- and middle-income households

California policymakers should take steps to substantially deepen the state’s investment in higher education, with a particular focus on subsidizing the full cost of attendance for low- and middle-income households. Targeting students with lower incomes would reduce the racial wealth divide by eliminating borrowing for many students of color, thus removing one barrier to completion and increasing the return on a college degree by allowing students to avoid wealth-stripping student debt.[75] To this end, policymakers should increase the supply of competitive Cal Grants and raise the value of the Cal Grant B access award for living expenses.

4. Boost investments in children through Children’s Savings Accounts (CSAs).

CSAs are savings accounts for children that have the potential to reduce generational inequities in wealth-building. Seeded with an initial deposit from the state that would accrue interest throughout childhood, a CSA could be automatically opened for each child at birth (with greater endowments for children from less wealthy families) or applied only to children from low-wealth households. Contributions from family and friends could receive a public match, the size of which could increase for families with less wealth. Once the child reaches adulthood, the savings could be used for higher education, homeownership, or other investments throughout their lifetime. Such a program could substantially reduce the racial wealth gap and increase asset security.[76]

The Future of Wealth

The rise of a strong American middle class did not happen accidentally. It required a healthy economy supported by large and intentional public investments. These actions were largely structured to benefit whites to the exclusion of communities of color, and that decision bears serious moral and economic consequences for our future well-being. Nationally, whites are projected to become a racial minority by 2045.[77] In California, people of color already constitute the majority of the state’s population, and their share is projected to rise to more than two-thirds (68%) by 2045.[78] As a result, the economic welfare of people of color will increasingly determine the welfare of our state and of the larger society. Californians and all Americans need to decide which future we want. One option is to continue down our current path, disproportionately concentrating wealth and opportunity with a handful of whites, while locking out people of color. A better option is to improve public policies at the state and federal levels in order to ensure equitable investments in all of our people and create a strong and inclusive economy.

Appendix

Measuring Wealth

Researchers primarily use three surveys to explore the distribution of wealth in the US: the US Census Bureau’s Survey of Income and Program Participation (SIPP), the Federal Reserve Board’s Survey of Consumer Finances (SCF), and the Panel Study of Income Dynamics (PSID) conducted by University of Michigan faculty. While all three of these surveys allow for comparisons by race and ethnicity, these categories tend to be limited. For example, due to sample size constraints, Asians, Native Americans, Pacific Islanders, and those who report more than one race are grouped into a single “Other” category, as in the SCF.[79] Wealth-related data by race and ethnicity is available for certain localities — including the Los Angeles area — from The National Asset Scorecard and Communities of Color survey (NASCC).[80] Due to these data limitations, The Racial Wealth Gap: What We Can Do About a Long-Standing Obstacle to Shared Prosperity focuses on the national differences in wealth between white, black, and Latinx households and reports local data when available.

Endnotes

[1] In this report, the term “racial wealth gap” is used to refer to an economic problem that affects various races and ethnicities.

[2] Jesse Bricker, et al., Changes in US Family Finances From 2013 to 2016: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 2017), p. 10.

[3] Though these gaps decrease when accounting for other demographic and economic factors associated with wealth, sizable disparities remain. See Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[4] William Darity Jr., et al., What We Get Wrong About Closing the Racial Wealth Gap (Samuel DuBois Cook Center on Social Equity and Insight Center for Community Economic Development: April 2018), p. 9.

[5] Data are from the 2014 National Asset Scorecard and Communities of Color survey and are for Los Angeles and Orange counties. The authors do not account for nativity status, with the exception of distinguishing between US-born blacks and African blacks. Median net worth for African blacks was $72,000. See Melany De La Cruz-Viesca, et al., The Color of Wealth in Los Angeles (Duke University, The New School, the University of California, Los Angeles, and the Insight Center for Community Economic Development: March 2016), p. 40.

[6] Christian E. Weller and Jeffrey Thompson, Wealth Inequality Among Asian Americans Greater Than Among Whites (Center for American Progress: December 20, 2016).

[7] This analysis excludes retirement savings. Including retirement savings, black and Latinx Americans had $200 and $340 in median liquid wealth, respectively, while whites had $23,000. See Rebecca Tippett, et al., Beyond Broke: Why Closing the Racial Wealth Gap Is a Priority for National Economic Security (Center for Global Policy Solutions and Duke Research Network on Racial and Ethnic Inequality at the Social Science Research Institute: May 2014), p. 2.

[8] Data are from the 2014 National Asset Scorecard and Communities of Color survey and are for Los Angeles and Orange counties. The authors do not account for nativity status, with the exception of distinguishing between US-born blacks and African blacks. See Melany De La Cruz-Viesca, et al., The Color of Wealth in Los Angeles (Duke University, The New School, the University of California, Los Angeles, and the Insight Center for Community Economic Development: March 2016), p. 38.

[9] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[10] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[11] Thomas M. Shapiro, The Hidden Cost of Being African American: How Wealth Perpetuates Inequality (New York: Oxford University Press, 2004), p. 190.

[12] Office of the Historian, United States Department of State, Indian Treaties and the Removal Act of 1830; Gregory P. Downs and Kate Masur, The Era of Reconstruction: 1861-1900 (National Park Service, US Department of the Interior: 2017), p. 70; and Masao Suzuki, “Important or Impotent? Taking Another Look at the 1920 California Alien Land Law,” The Journal of Economic History 64 (2004), pp. 125-130.

[13] Richard Rothstein, The Racial Achievement Gap, Segregated Schools, and Segregated Neighborhoods: A Constitutional Insult (Economic Policy Institute: November 12, 2014).

[14] Dedrick Asante-Muhammad, et al., The Road to Zero Wealth: How the Racial Wealth Divide Is Hollowing Out America’s Middle Class (Institute for Policy Studies and Prosperity Now: September 2017), p. 15.

[15] Jeremiah Battle, Jr., et al., Toxic Transactions: How Land Installment Contracts Once Again Threaten Communities of Color (National Consumer Law Center: July 2016), pp. 3-4.

[16] Under the 1968 Fair Housing Act, the Department of Housing and Urban Development (HUD) had to investigate complaints of discrimination within 30 days. If HUD pursued the claim, it could only seek voluntary settlements with noncompliant parties or advise complainants to file private lawsuits, for which penalties were capped at $1,000. In 1988, Congress updated the Act to provide administrative enforcement of the law, extend HUD’s investigation time to 100 days, and increase the maximum civil penalties, which currently range from $20,111 for a first offense to $100,554 for those with a history of offenses. See Douglas S. Massey, “The Legacy of the 1968 Fair Housing Act” Sociological Forum 30 (2015), pp. 571-588; Administrative Conference of the United States, Enforcement Procedures Under the Fair Housing Act (June 18, 1992); and 82 Federal Register 24523 (2017).

[17] Douglas S. Massey, “The Legacy of the 1968 Fair Housing Act” Sociological Forum 30 (2015), pp. 571-588; Nikole Hannah-Jones, “Living Apart: How the Government Betrayed a Landmark Civil Rights Law,” ProPublica (June 25, 2015).

[18] US Department of Housing and Urban Development, Housing Discrimination Against Racial and Ethnic Minorities 2012: Executive Summary, (June 2013), p. 1.

[19] This analysis excludes durable goods. Dedrick Asante-Muhammad, et al., The Road to Zero Wealth: How the Racial Wealth Divide Is Hollowing Out America’s Middle Class (Institute for Policy Studies and Prosperity Now: September 2017), p. 8.

[20] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[21] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[22] Rebecca Tippett, et al., Beyond Broke: Why Closing the Racial Wealth Gap Is a Priority for National Economic Security (Center for Global Policy Solutions and Duke Research Network on Racial and Ethnic Inequality at the Social Science Research Institute: May 2014), p. 4.

[23] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[24] Refundable tax credits are the exception, as they are recorded in the federal budget. See Lewis Brown Jr. and Heather McCulloch, Building an Equitable Tax Code: A Primer for Advocates (PolicyLink: 2014), p. 3.

[25] Lewis Brown Jr. and Heather McCulloch, Building an Equitable Tax Code: A Primer for Advocates (PolicyLink: 2014), p. 7.

[26] Heather McCulloch, Closing the Women’s Wealth Gap: What It Is, Why It Matters, and What Can Be Done About It (Closing the Women’s Wealth Gap Initiative: updated January 2017), p. 9; Suparna Bhaskaran, Pinklining: How Wall Street’s Predatory Products Pillage Women’s Wealth, Opportunities, and Futures (June 2016), p. 16.

[27] Scott Graves and Alissa Anderson, Payday Loans: Taking the Pay Out of Payday (California Budget & Policy Center: September 2008), p. 7.

[28] Suparna Bhaskaran, Pinklining: How Wall Street’s Predatory Products Pillage Women’s Wealth, Opportunities, and Futures (June 2016), p. 18-19.

[29] Suparna Bhaskaran, Pinklining: How Wall Street’s Predatory Products Pillage Women’s Wealth, Opportunities, and Futures (June 2016), p. 17.

[30] California Department of Business Oversight, Summary Report: California Deferred Deposit Transaction Law—Annual Report and Industry Survey (May 31, 2017), p. 8.

[31] In a 2013 analysis, these areas explained 61% of the ongoing racial wealth divide between whites and blacks. See Thomas Shapiro, Tatjana Meschede, and Sam Osoro, The Roots of the Widening Racial Wealth Gap: Explaining the Black-White Economic Divide (Institute on Assets and Social Policy: February 2013), pp. 2-3.

[32] Sara Kimberlin, Californians in All Parts of the State Pay More Than They Can Afford for Housing (California Budget & Policy Center: September 2017).

[33] Sara Kimberlin, Californians in All Parts of the State Pay More Than They Can Afford for Housing (California Budget & Policy Center: September 2017).

[34] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[35] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[36] California Budget & Policy Center analysis of US Census Bureau, American Community Survey data. Data are for household heads age 18 and older in 2016.

[37] Melany De La Cruz-Viesca, et al., The Color of Wealth in Los Angeles (Duke University, The New School, the University of California, Los Angeles, and the Insight Center for Community Economic Development: March 2016), p. 33.

[38] Thomas Shapiro, Tatjana Meschede, and Sam Osoro, The Roots of the Widening Racial Wealth Gap: Explaining the Black-White Economic Divide (Institute on Assets and Social Policy: February 2013), p. 2.

[39] Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[40] Thomas Shapiro, Tatjana Meschede, and Sam Osoro, The Roots of the Widening Racial Wealth Gap: Explaining the Black-White Economic Divide (Institute on Assets and Social Policy: February 2013), p. 3.

[41] Thomas Shapiro, Tatjana Meschede, and Sam Osoro, The Roots of the Widening Racial Wealth Gap: Explaining the Black-White Economic Divide (Institute on Assets and Social Policy: February 2013), p. 3.

[42] Laura Sullivan, et al., The Racial Wealth Gap: Why Policy Matters (Institute for Assets and Social Policy and Demos: 2015), p. 1.

[43] If black families owned their homes at the same rate as whites, the median black household’s wealth would increase by over $32,000 (451%). For Latinx families, equalizing homeownership rates would increase the median household wealth by over $29,000 (350%). Laura Sullivan, et al., The Racial Wealth Gap: Why Policy Matters (Institute for Assets and Social Policy and Demos: 2015), pp. 11-13.

[44] Thomas Shapiro, Tatjana Meschede, and Sam Osoro, The Roots of the Widening Racial Wealth Gap: Explaining the Black-White Economic Divide (Institute on Assets and Social Policy: February 2013), pp. 2-3.

[45] William Darity Jr., et al., What We Get Wrong About Closing the Racial Wealth Gap (Samuel DuBois Cook Center on Social Equity and Insight Center for Community Economic Development: April 2018), p. 7.

[46] William Darity Jr., et al., What We Get Wrong About Closing the Racial Wealth Gap (Samuel DuBois Cook Center on Social Equity and Insight Center for Community Economic Development: April 2018), p. 8.

[47] Laura Sullivan, et al., The Racial Wealth Gap: Why Policy Matters (Institute for Assets and Social Policy and Demos: 2015), p. 25.

[48] Heather McCulloch, Closing the Women’s Wealth Gap: What It Is, Why It Matters, and What Can Be Done About It (Closing the Women’s Wealth Gap Initiative: updated January 2017), p. 7.

[49] The data refers specifically to defined contribution plans. See Heather McCulloch, Closing the Women’s Wealth Gap: What It Is, Why It Matters, and What Can Be Done About It (Closing the Women’s Wealth Gap Initiative: updated January 2017), p. 12.

[50] Tatjana Meschede, et al., “‘Family Achievements’? How a College Degree Accumulates Wealth for Whites and Not for Blacks,” Federal Reserve Bank of St. Louis Review 99 (2017), p. 123.

[51] Hans Johnson, Testimony: The Need for College Graduates in California’s Future Economy (The Public Policy Institute of California: November 1, 2017).

[52] Jon Stiles, Michael Hout, and Henry Brady, California’s Economic Payoff: Investing in College Access and Completion (The Campaign for College Opportunity: April 2012), p.13.

[53] Amy Rose, State Spending Per Student at CSU and UC Remains Well Below Pre-Recession Levels, Despite Recent Increases (California Budget & Policy Center: March 2018).

[54] Yunju Nam, et al., Bootstraps Are for Black Kids: Race, Wealth, and the Impact of Intergenerational Transfers on Adult Outcomes (Insight Center for Community Economic Development: September 2015), p. 8.

[55] Tatjana Meschede, et al., “’Family Achievements?’ How a College Degree Accumulates Wealth for Whites and Not for Blacks,” Federal Reserve Bank of St. Louis Review 99 (2017), p. 124.

[56] There are three types of Cal Grant awards: Cal Grant A is used for tuition and fees; Cal Grant B provides an allowance for living costs known as an “access award” (in addition to tuition and fee assistance after the first year); and Cal Grant C is for students who attend occupational or career colleges. See California Student Aid Commission, What Is a Cal Grant Award?

[57] Data are from 2008. See The Campaign for College Opportunity, The State of Higher Education in California: Latinos (April 2015), p. 18 and The Campaign for College Opportunity, The State of Higher Education in California: Blacks (May 2015), p. 29.

[58] The Campaign for College Opportunity, The State of Higher Education in California: Latinos (April 2015), p.19; The Campaign for College Opportunity, The State of Higher Education in California: Blacks (May 2015), p. 29; and Amy Rose, Barriers to Higher Education Attainment: Students’ Unmet Basic Needs (California Budget & Policy Center: May 2018).

[59] Spiros Protopsaltis and Sharon Parrott, Pell Grants — a Key Tool for Expanding College Access and Economic Opportunity — Need Strengthening, Not Cuts (Center on Budget and Policy Priorities: July 27, 2017).

[60] Amy Rose, Barriers to Higher Education Attainment: Students’ Unmet Basic Needs (California Budget & Policy Center: May 2018).

[61] Mark Huelsman, et al., Less Debt, More Equity: Lowering Student Debt While Closing the Black-White Wealth Gap (Demos and Institute on Assets and Social Policy: 2015), pp. 16-17.

[62] Latinx students tend to borrow smaller amounts than both blacks and whites at public institutions but may borrow greater amounts at private for-profit institutions. See Mark Huelsman, The Debt Divide: The Racial and Class Bias Behind the “New Normal” of Student Borrowing (Demos: May 19, 2015), pp. 7-8.

[63] Mark Huelsman, The Debt Divide: The Racial and Class Bias Behind the “New Normal” of Student Borrowing (Demos: May 19, 2015), pp. 14-16.

[64] For a white household whose head does not have a bachelor’s degree, median net worth is $98,100. For a black household whose head does have a college degree, median net worth is $68,200. For Latinx households, the equivalent figure is $77,900. See Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[65] Yunju Nam, et al., Bootstraps Are for Black Kids: Race, Wealth, and the Impact of Intergenerational Transfers on Adult Outcomes (The Insight Center for Community Economic Development: September 2015), p. 12.

[66] Jonathan Kaplan, Repeal of the Estate Tax Would Reduce Federal Resources While Key Public Services Are on the Chopping Block (California Budget & Policy Center: October 26, 2017).

[67] Even before the passage of the Tax Cuts and Jobs Act of 2017, which further scaled back the national estate tax, only 2 out of every 1,000 estates were subject to the tax. Jonathan Kaplan, Repeal of the Estate Tax Would Reduce Federal Resources While Key Public Services Are on the Chopping Block (California Budget & Policy Center: October 26, 2017).

[68] Steven Bliss and Chris Hoene, Final GOP Tax Plan Is a Big Gift to the Wealthy, but Would Harm Most Households and Our Economy (California Budget & Policy Center: December 18, 2017).

[69] In order to establish a state estate tax, the Legislature would have to ask voters to repeal or amend Proposition 6 of 1982, which prohibits the state from imposing an estate, inheritance, or wealth tax. See California Budget & Policy Center, Principles and Policy: A Guide to California’s Tax System (April 2013), p. 21. For more information about state estate taxes, see Elizabeth McNichol, State Estate Taxes: A Key Tool for Broad Prosperity (Center on Budget and Policy Priorities: May 11, 2016).

[70] For estimates on the amount of revenue an estate tax could raise, see Elizabeth McNichol, State Estate Taxes: A Key Tool for Broad Prosperity (Center on Budget and Policy Priorities: May 11, 2016) and Legislative Analyst’s Office, A.G. File No. 2017-038 (November 30, 2017).

[71] Brett Theodos, et al., Affordable Homeownership: An Evaluation of Shared Equity Programs (Urban Institute: March 2017), p. 1.

[72] William Chen, Spending Through California’s Tax Code (California Budget & Policy Center: August 2016).

[73] In 2016, the average net housing wealth in the US was $215,800 for white homeowners versus $94,400 for black homeowners and $129,800 for Latinx homeowners. See Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[74] The Department of Finance estimates that California will lose $4 billion in revenue due to the mortgage interest deduction in state fiscal year 2018-19. See California Department of Finance, Tax Expenditure Report: 2018-19, p. 5.

[75] Mark Huelsman, et al., Less Debt, More Equity: Lowering Student Debt While Closing the Black-White Wealth Gap (Demos and Institute on Assets and Social Policy: 2015), pp. 18-20.

[76] Laura Sullivan,, et al., Equitable Investments in the Next Generation: Designing Policies to Close the Racial Wealth Gap (Institute on Assets and Social Policy and CFED: 2016), pp. 9-11.

[77] William H. Frey, The US Will Become “Minority White” in 2045, Census Projects (The Brookings Institution: Updated September 10, 2018).

[78] California Budget & Policy Center analysis of Department of Finance data.

[79] This report uses the terms “Asian” and “Asian American” depending on the cited source. For more on the SCF’s racial and ethnic categories, see Lisa Dettling, et al., Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence From the Survey of Consumer Finances (Board of Governors of the Federal Reserve System: September 27, 2017).

[80] Melany De La Cruz-Viesca, et al., The Color of Wealth in Los Angeles (Duke University, The New School, the University of California, Los Angeles, and the Insight Center for Community Economic Development: March 2016), pp. 19-20.