Summer Financial Aid: A Tool for Boosting Low-Income Students’ Graduation Rates

July 2019 | By Amy Rose

Ensuring college students graduate from California’s public universities in a timely manner is necessary for the state to satisfy student demand for higher education and to meet the state’s workforce needs. As previously discussed in our analyses, the high cost of college attendance and overcrowded degree programs make it difficult for many low-income students to graduate on time. One way students can graduate more quickly is to enroll in summer courses. However, many low-income students miss out on summer enrollment because of insufficient financial aid. Providing low-income students with financial aid during the summer can help ensure timely graduation, which means less student loan debt, greater earning potential, and more room for the next cohort of students to start college. The 2019-20 budget includes summer-term financial aid to help some low-income students cross the graduation stage in a timely manner, but leaves others without support.

Limited Summer Financial Aid Keeps Low-Income Students Away

Students attending the state’s public four-year universities, California State University (CSU) and University of California (UC), pay for college through a combination of family contributions, earnings from work, and federal, state, and institutional aid. Many low-income students receive state and federal need-based financial aid to help pay for tuition and living expenses.

At the federal level, Pell Grants provide financial aid to low-income students to help afford the cost of college such as food and housing. The maximum Pell Grant award for 2019-20 is $6,195. In 2017, Congress reinstated the Year-Round Pell Grant, which allows students to receive a Pell Grant during the summer without drawing from their lifetime eligibility.

In California, Cal Grants are the foundation of the state’s financial aid for college students. In 2019-20 the maximum Cal Grant tuition award at CSU is $5,742 and $12,570 at UC. While Pell Grants are available for summer coursework, Cal Grants have limitations. If students take more courses during the summer it draws from their total lifetime financial aid eligibility. This means that students who wish to attend summer courses must: 1) do so without the support of Cal Grants or 2) cut into their lifetime award eligibility — leaving them without aid later in their academic careers.

As a recent Budget Center report highlighted, for students experiencing unmet basic needs, lack of financial support is a barrier to success, so receiving financial aid in the summer might allow students to continue their studies year-round and could shorten the time it takes for students to earn a degree. While a growing number of students are graduating from high school and more are attending college, completion rates at CSU and UC are low. At CSU, only 26% of students graduate in four years and 69% do so in six years. At UC, 61% of students graduate in four years and 85% graduate in six years.

For low-income students, the time it takes to earn a bachelor’s degree is often much longer because of a variety of factors, including limited availability of financial aid and other expenses of affording college. At CSU, the four- and six-year graduation rate for low-income students is 18.5% and 56.2%, respectively. Among this population, outcomes vary significantly by race and ethnicity. Black students and Latino and Hispanic students graduate at about half of the rate as their White counterparts (13.7% and 15.6%, respectively, compared to 29.3%). The CSU is working to improve graduation rates and eliminate achievement gaps through their Graduation Initiative 2025. While graduation rates are higher at UC than CSU, racial disparities still exist. Four-year graduation rates for White UC students is 70% compared to 50% for Black UC students. These racial disparities in graduation rates mimic disparities in socioeconomic status, health outcomes, and health care for people of color and reflect a legacy of discriminatory policies and practices that cut people of color off from opportunity.

Summer Financial Aid Can Help Boost Graduation Rates and Ease Capacity Limits

Summer financial aid can help more students graduate on time and ease the capacity limitations at CSU and UC.

Every year thousands of students who are qualified for admittance to the CSU and UC do not attend these colleges due to capacity limitations. These students either delay entering college, attend a private nonprofit or for-profit (often at much higher costs), or skip college completely, which disproportionately impacts low-income students who may not have the financial resources to attend a private university or who may take on staggering amounts of debt to cover the higher costs. Turning away qualified students is also counterproductive to the state’s efforts to increase the number of bachelor degrees awarded at CSU and UC in order to meet future workforce demands. To meet these needs, the CSU and UC should increase enrollment and improve graduation rates.

Limited capacity at CSU and UC also affects current students, many whom struggle to get the courses they need due to “impacted” campuses, which occurs when the number of qualified applicants is greater than the number of available spaces in a major. When programs are impacted students must wait for classes to become available, delaying their time to graduation. The sooner students graduate the sooner they can enter the workforce and free up space at a campus for another student.

California lawmakers have followed the lead of the federal Pell Grant’s extension to summer by funding some summer financial aid in the 2019-20 state budget. The budget allocates $6 million to CSU and $4 million to UC to provide summer-term financial aid to eligible students, including undocumented students. While this is a step in the right direction, the spending plan leaves behind students attending California community colleges and the state’s private institutions. Additionally, the budget notes that this funding will be suspended in two years unless General Fund revenues are higher than expected in the coming years.

Ensuring all students have access to quality public higher education is a long-standing priority of state leaders. The 2019-20 state budget builds on recent institutional efforts to help students more quickly earn a bachelor’s degree at UC and CSU. Now it’s time for the state to support these efforts by extending financial aid to summer at all of California’s colleges.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

The Trump Administration has quietly announced a proposal to change the way the federal poverty line is updated each year for inflation. This proposal is far more than a minor technical change affecting government statistics — it would cut low-income Californians’ access to health care, basic nutrition, and other essential needs. These consequences arise because the federal poverty line forms the basis of criteria that determine whether individuals are eligible to access many vital public supports that are funded (at least in part) by federal dollars — like public health insurance through Medi-Cal, food assistance through CalFresh, and home energy assistance through the Low Income Home Energy Assistance Program (LIHEAP). As a result, changing the method for updating the poverty line as proposed would threaten low-income Californians’ ability to meet their most basic needs.

The Trump Administration’s under-the-radar proposal, included in a notice requesting public comments issued by the Office of Management and Budget (OMB), puts forward the idea of updating the Census Bureau’s official poverty thresholds, or poverty line, using an alternative measure of inflation in place of the inflation measure currently used to update the thresholds each year (the Consumer Price Index for All Urban Consumers, or CPI-U). Two alternative inflation measures specifically mentioned as options are the chained Consumer Price Index (the chained CPI, or C-CPI-U) or the Personal Consumption Expenditures Price Index (PCE Price Index). Using either of these alternative inflation measures would make the poverty thresholds increase more slowly over time. There are several reasons that this proposed change would actually make the federal poverty line less accurate rather than more accurate as a measure of basic economic security. What is more, the Trump Administration is explicitly not requesting input to understand how this change would affect people’s access to vital public supports that help address families’ and individuals’ most basic needs.

Slowing Down the Annual Increase in the Poverty Line Would Make It Less Accurate, Not More Accurate, Especially in California

Switching to a slower-rising inflation measure to update the federal poverty line each year would make the official poverty thresholds less accurate as a measure of a minimum adequate level of economic security. The federal poverty line is already far lower than the basic cost to support a family, particularly in California, where the cost of living is high in many regions. According to the Budget Center’s Making Ends Meet analysis, the statewide average cost of a basic family budget for a working single parent with two children — including housing and utilities, food, child care, health care, transportation, taxes, and miscellaneous other basic necessities — totals nearly $66,000 (in 2017 dollars), while the 2017 official poverty threshold for the same family was only $19,749. In the most expensive parts of the state the cost of basic needs is much higher — as much as $103,423 for this same family in San Francisco County, or more than five times the federal poverty line. Even in Fresno County, a county with relatively low costs, the basic family budget for a single parent with two children is more than $50,000, or two and a half times the poverty line. Slowing down the rate by which the poverty thresholds are updated each year would only make this disconnect worse.

The slower-rising chained CPI and PCE Price Index are also unlikely to be more accurate ways to measure inflation specifically for low-income households, or to update a poverty threshold, which represents a minimum level of resources to meet basic needs. The largest basic needs expense in a household budget is typically housing, and housing costs in California in recent years have increased much faster than even the standard CPI-U inflation measure currently used to update the federal poverty line. While the CPI-U rose by 21.6% from 2006 to 2017, median household rent in California rose by 41.6%, or nearly twice as fast. Research has shown that costs for the overall bundle of goodstypically purchased by low-income households have risen faster than costs for the goods typically purchased by higher-income households. Also, the reason that the chained CPI increases more slowly than the standard CPI-U inflation measure used currently to update the poverty line is because the chained CPI assumes that consumers will trade more expensive items for similar less expensive items as prices change (e.g., they will buy chicken instead of beef if the price of beef rises). The PCE Price Index makes the same assumption. However, housing and child care are typically the two largest expenses in the basic family budgets for working families, and both are items where it is unlikely that families can easily switch to a similar, lower-cost alternative if they face an increase in price.

The Trump Administration has framed considering alternative inflation measures as an important technical question for accurate calculation of the federal poverty line, but research on ways to improve the measurement of poverty has not identified slowing down the annual inflation update as a key strategy. An expert panel of the National Academy of Sciences examined many technical aspects of the official federal poverty measure in 1995 and issued recommendations for improving the government measure of poverty, resulting in the creation of the Supplemental Poverty Measure (SPM). The SPM poverty line is higher than the official poverty line for most people, particularly in California. For example, the SPM poverty threshold for a family of two adults and two children who rent their home in the Los Angeles metropolitan area was $34,308 in 2017, while the official federal poverty threshold for the same family was only $24,858. The SPM incorporates many other improvements to measuring poverty. (See the Budget Center poverty explainer webinar for more details on the SPM.) If the objective is to improve poverty measurement, it would make more sense to consider all of these types of improvements rather than focusing on just one item, the choice of inflation measure. This is particularly true because switching to one of the proposed alternative inflation measures alone would cause the poverty thresholds to shrink over time, when research provides more support for increasing the thresholds.

Changing the Way the Poverty Thresholds Are Updated Could Reduce Low-Income Californians’ Access to Vital Public Supports

This proposal would have serious, concrete consequences in the lives of low-income individuals and families. That is because the federal poverty thresholds are the basis for the federal poverty guidelines that are used to determine eligibility, benefits, and funding levels for a wide variety of public supports and federal grants that help families and individuals meet their basic needs. Millions of Californians with low incomes are enrolled in Medi-Cal (known as Medicaid at the federal level) for public health insurance, for example, and millions of Californians access CalFresh food assistance (known as the Supplemental Nutrition Assistance Program, or SNAP, at the federal level) to meet their basic need for food. To be eligible to access these public supports, a family’s or individual’s income must be less than the federal poverty guideline or a multiple of it. Slowing down the annual increase in the poverty guidelines would result in fewer Californians eligible to access these critical public supports over time, with a small impact at first but a large impact over the long term.

The Public Can Submit Comments on This Proposal Now

The public has until Friday, June 21 to submit comments to the Office of Management and Budget via an online submission form on this proposed change to how the poverty line is updated each year for inflation. Individuals and organizations are encouraged to share the implications of the proposal for their households or those they serve, keeping comments substantive and unique, with at least 70% of the content different from other submitted comments. The Trump Administration explicitly did not request public comments on how the proposed change to the poverty thresholds would affect the federal poverty guidelines and eligibility for vital public supports. However, organizations can draw attention to the importance of this cascading effect of the proposal by describing what questions the federal government should take the time to research, and what additional input the government should solicit and consider, before deciding whether to move forward with the change.

The poverty line is more than a measure, and ensuring that low-income Californians have access to vital public supports such as health care and food assistance, and that those benefits are not diminished over time under the guise of a technical change, should be a priority for all Californians.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

College can be stressful for students, especially during this time of the year as students are completing final examinations and graduating. Considering the challenging academic workload, it is normal for students to feel worried, anxious, restless, or sad from time to time. If these feelings or other mental health symptoms persist and start to interfere with daily living and academic performance, it may be indicative of a mental health issue. Without treatment for mental health issues, college students are more likely to drop out, abuse substances, and even commit suicide.

Years of rising demand in mental health services among California college students have contributed to longer wait times and growing pressure to improve access to these services. California higher education leaders and policymakers are taking steps to reduce the gap between students’ need for mental health services and their use of these services.

In light of Mental Health Awareness Month, and as budget deliberations are underway in the state legislature, this piece describes mental health trends and examines current state proposals to maintain, improve, and/or expand access to mental health supports in college campuses across California.

Mental Health Trends in California Colleges

The 2018 National College Health Assessment reports that in the past year, 63% of college students surveyed felt overwhelming anxiety, 42% felt so depressed that it was difficult to function, 62% felt very lonely, and 12% seriously considered suicide. Researchers at UC Berkeley found that nationally, the percentage of students who reported being diagnosed or treated for anxiety disorder in the past year doubled from 2008 to 2016 from 10% to 20%.

Students in California’s public colleges report similar experiences. At the California State University (CSU), students reported an increase in hopelessness, loneliness, sadness, depression, anxiety, and suicidal thoughts in the past two years and 16% of students received some psychological counseling or treatment on campuses last year. At the University of California (UC), the percentage of students seeking mental health services in the past 10 years rose 78%, nearly three times higher than enrollment growth during the same period. While the demand for mental health services has increased significantly, it may actually understate the need, as many students may choose not to seek support due to the stigma attached to counseling.

At California Community Colleges (CCC), students experience similar rates of psychological distress as UC and CSU students — uncomfortable feelings or emotions that affect daily living — according to a recent study. However, students from CCC reported higher rates of impaired academic performance due to mental health issues than students at CSU and UC campuses. CCC students were half as likely to receive referrals for counseling or mental health services by a faculty member and were also less likely to receive services on campuses than their UC and CSU counterparts.

Availability of Mental Health Services and Resources for College Students Varies Across the State

The UC, CSU, and CCC have long recognized the need to provide mental health resources on campus, but have differed in their responses to meet increasing demand due to budget constraints and other factors. For that reason, students’ access to mental health services varies depending on the sector and campus.

At the UC, each campus has a Student Counseling Center that provides direct services, outreach and prevention services, and campus consultation services. In response to the increasing demand for mental health services at these centers, the UC Board of Regents approved a 5% annual increase in the Student Services Fee (SSF) for five consecutive years (2014 – 2019), with half of revenues earmarked for Student Mental Health. In 2018-19, the UC received $4.8 million in State General Fund in lieu of another SSF increase. As a result of this funding, UC was able to hire 70 Full Time Equivalent (FTE) counseling providers, reduce the average wait times for intakes from 12-18 days to 9-11 days, increase the use of case managers and launch integrated care efforts, and more.

The CSU campuses also provide myriad services to support students, focusing on efforts around education outreach, training, and acute crisis care. All campuses provide baseline mental health services: counseling, suicide and violence prevention, emergency crisis interventions, outreach, consultation, and referral resources.

Several CSU campuses have attempted to address the increased demand for mental health in a variety of innovative ways. Some campuses offer wellness workshops, a series of emotional well-being workshops led by counselors. At CSU Fresno, the Let’s Talk Program has allowed counselors to meet with students anonymously for 20-minute sessions in locations around campus, during which the counselor assesses the student’s need. Campuses have also invested in peer mentoring programs, which have “increased academic and social integration” as well as “improved student outcomes for all students, particularly those from historically underserved communities,” according to the CSU Office of the Chancellor.

CSU is also working to strengthen community partnerships in order to increase mental health services. Earlier this year, the Office of the Chancellor hosted a systemwide convening to connect campuses with their local county behavioral health offices. The goal of this convening was to develop partnerships that will bring additional mental health services to CSU students.

Compared to the UC and CSU systems, mental health services at the CCC appear to be less consistent, partly because community colleges typically do not offer their own health insurance plans. Currently, 90 of the 115 community colleges offer mental health services, with students averaging one to three counseling sessions per semester. Establishing health services is optional for community college districts, and districts that provide health services cannot charge a student health fee that exceeds $21 per semester, which means student health services are typically more scarce on campuses with relatively small student populations.

In 2011, CCC implemented the California Community Colleges Student Mental Health Program (CCC SMHP), a statewide effort focusing on prevention and early intervention. The CCC SMHP promotes faculty and staff training, peer counseling, and suicide prevention. According to a recent CCC SMHP report, nearly 168,000 students, faculty, and community members have been reached through prevention and early intervention trainings.

Barriers to Accessing Mental Health Support

One of the greatest challenges on California college campuses is that mental health funding has not kept pace with demand. This disinvestment in crucial services results in understaffed counseling offices, long wait times, and inadequate facilities — all of which negatively affect students seeking help.

The International Association of Counseling Services advisesthere to be one professional for every 1,000 to 1,500 students — an effort pushed for by legislators and vetoed by Governor Brown in 2018. Recent reports suggest that staffing ratios at the UC and CSU are close to that ratio (about 1,100 students per counselor at UC and 2,000 students per counselor at CSU); however, ratios at the CCC exceed more than 7,000 students per counselor. While the rates of both perceived and personal stigma have decreased in recent years, it is particularly salient for black students, Latinx students, and others who may already suffer from discrimination. Ensuring diversity among counseling staff may help with stigmatization and is a priority advocated for by students.

Before students can receive counseling, many must wait up to a few weeks for an available appointment. Additionally, many campuses have inadequate counseling infrastructure, with appointments taking place in non-discrete locations.

Current Budget and Policy Proposals to Improve Access to Mental Health Services

Improving access to mental health services for college students is a widely shared goal among policymakers, students, and institutional leaders. Several budget and policy proposals have been introduced this year from the legislature, Governor, and educational institutions.

In the legislature, AB1689 (McCarty) would create the College Mental Health Services Program, a matching grant program to enhance the provision of mental health services at CSU, UC, and CCC. Additionally, the Assembly’s budget provides $2 million ongoing and $3 million one-time of Proposition 63 state administration fund to support student mental health services at UC and CSU, and $10 million ongoing and $12 million one-time Proposition 63 state administration fund for the community colleges. The Senate’s budget allocates $550 million for “Mental Health Partnerships” between local behavioral health departments and K-12 schools, county offices of education, and public colleges within a county region.

For the UC, Governor Newsom’s proposed 2019-20 budget includes $5.3 million ongoing General Fund to improve mental health programs on campuses, which UC proposes using to hire more counselors and stabilize funding for existing counselors. Ultimately, UC notes that this funding would help to improve capacity for direct services, further enhance provider diversity, and bolster targeted prevention efforts for vulnerable students. In 2018-19, UC received $4.8 million in State General Funds to support expanding mental health services. This year, UC asked to make this funding permanent and ongoing and warned that without it, there is a potential for counseling staff layoffs, worsening accessibility, longer wait times, and decreased provider diversity.

For the CCC, there are no funds included in the Governor’s budget for the mental health needs of students. However, last year the legislature approved $10 million dollars of one-time funding in the 2018-19 state budget for California Community Colleges to support mental health services and training.

Mental Health Services Are Critical to Student Success

Given the increased rate of mental health issues among college students, California colleges must work to improve access to mental health services and treatment. Increased mental health funding should be directed to prevention and early intervention as well as direct services for students, considering that the demand for these services already exceeds the availability at many campuses across the state. Adequately funding these services can help mitigate the negative toll that mental health conditions can take and help students succeed academically.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Executive Summary

On May 9, Governor Gavin Newsom released the May Revision to his proposed 2019-20 state budget that continues to call for a series of bold investments in creating economic security and opportunities for Californians, while also fostering the state’s fiscal health.

The Governor forecasts revenues that are $3.2 billion higher (over a three-year “budget window” from 2017-18 to 2019-20) than projected in January, driven largely by continued economic growth.

The Governor’s proposal includes a mix of one-time and ongoing investments vital to low- and middle-income California’s economic prosperity, including: a significant expansion of the state’s Earned Income Tax Credit (EITC), investment in early childhood development, extending paid family leave, continuing to expand health coverage, increasing investment in K-12 and state higher education systems, and working toward greater access to mental health services. The Governor’s revised budget also provides additional support for housing and homelessness supports, recognizing that the high cost of housing continues to burden and destabilize many Californians. These proposals, individually and in combination, would significantly improve the health and well-being of millions of Californians, most notably low- and middle-income people of color, immigrants, and women and children.

The May Revision also continues to bolster the state’s fiscal resilience by building up reserves and paying down state debts and liabilities. While the Governor’s revised budget continues to call for a variety of program expansions, the May Revision sunsets some of those investments within a few years.

These proposals — a combination of one-time and ongoing investments, building up reserves, and paying down debts — represent a mostly balanced approach to managing the state’s fiscal health. But, there are opportunities to further enhance the state’s fiscal health and extend support to more Californians in need. By seeking an extension of California’s tax on health insurance plans — also known as MCOs — the state could move even closer to universal health coverage. The state also has room to further improve the economic and social well-being for all Californians, including older adults and people with disabilities, working immigrants who file their taxes and who are left out of the EITC expansion, and families with young children who are struggling to find affordable child care.

Download full report (PDF) or use the links below to browse individual sections of this report:

May Revision Reflects Short-Term Improvements in the Revenue Outlook, but Slowing Growth in the Long Term

The Governor’s revised budget assumes that General Fund revenues for the three-year budget window, spanning 2017-18 to 2019-20, will be $3.2 billion higher than projected in January, before accounting for transfers. After accounting for transfers, including deposits into the state’s rainy day fund and loan repayments, General Fund revenues are expected to be $1.9 billion higher than in the January forecast. However, these improvements are expected to be temporary, and the revised forecast reflects increasing risks and slower economic and revenue growth beyond the budget window.

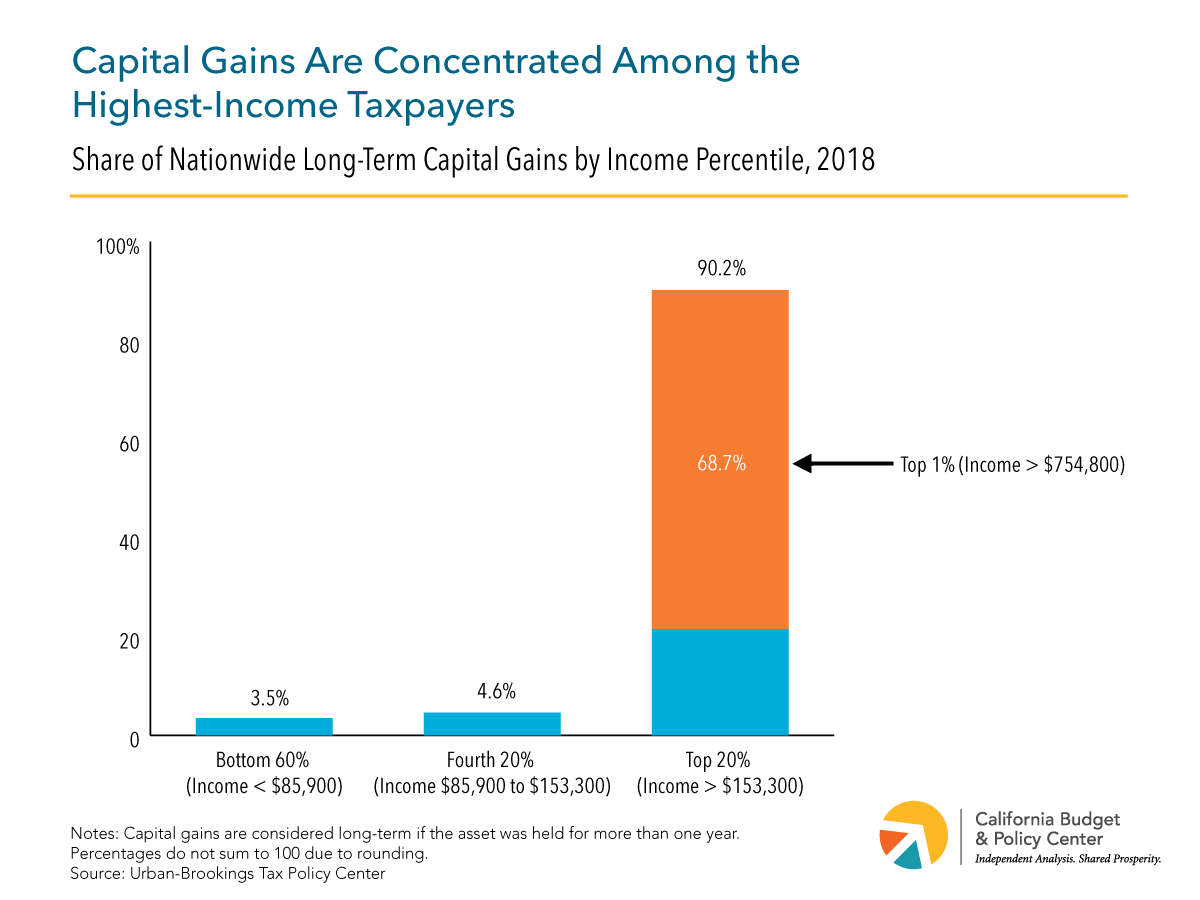

The improved short-term outlook is driven by higher Personal Income Tax (PIT) and Corporation Tax (CT) receipts, while Sales and Use Tax (SUT) projections have been revised downward. PIT revenues for 2017-18 to 2019-20 are expected to be nearly $1.9 billion higher than projected in January, primarily reflecting upward revisions in capital gains realizations due to an improved stock market forecast. Capital gains realizations are now expected to return to a normal level by 2022 — one year later than was forecast in the January budget proposal. The revised budget notes that new tax return data for 2017 shows that the income distribution was less skewed toward higher-income taxpayers than previously assumed, which offsets some of the expected revenue increases.

Expected CT revenues have been revised upward by over $1.7 billion, but this is largely due to the shifting of income from 2017 to 2018 and one-time payments associated with the 2017 federal tax law. The projection for SUT revenues was adjusted downward by $360 million, reflecting lower than expected growth in capital investments, lower cannabis sales, and higher utilization of the sales tax exemption for manufacturing equipment. Slightly offsetting these decreases is a modest increase in the expected revenue boost resulting from the US Supreme Court ruling in Wayfair v. South Dakota and the state’s recently enacted AB 147, which expand the state’s ability to require out-of-state retailers and marketplace facilitators to collect use tax.

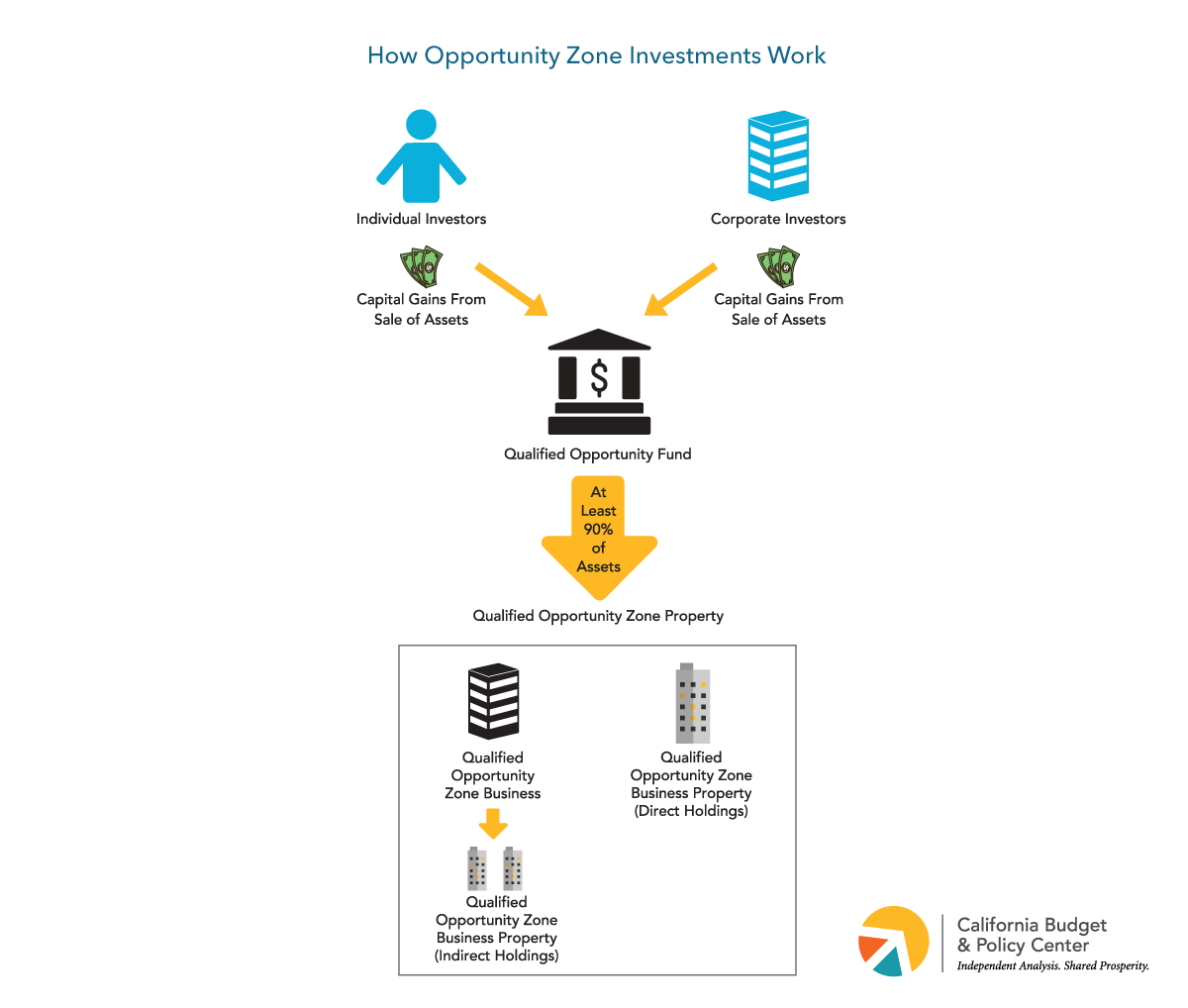

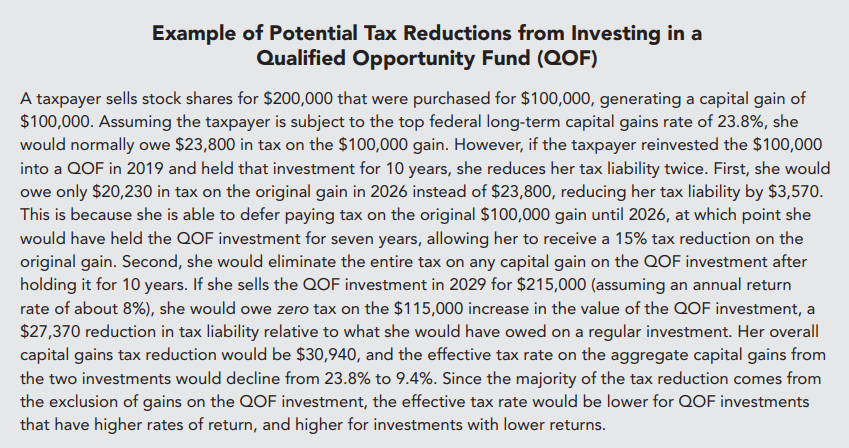

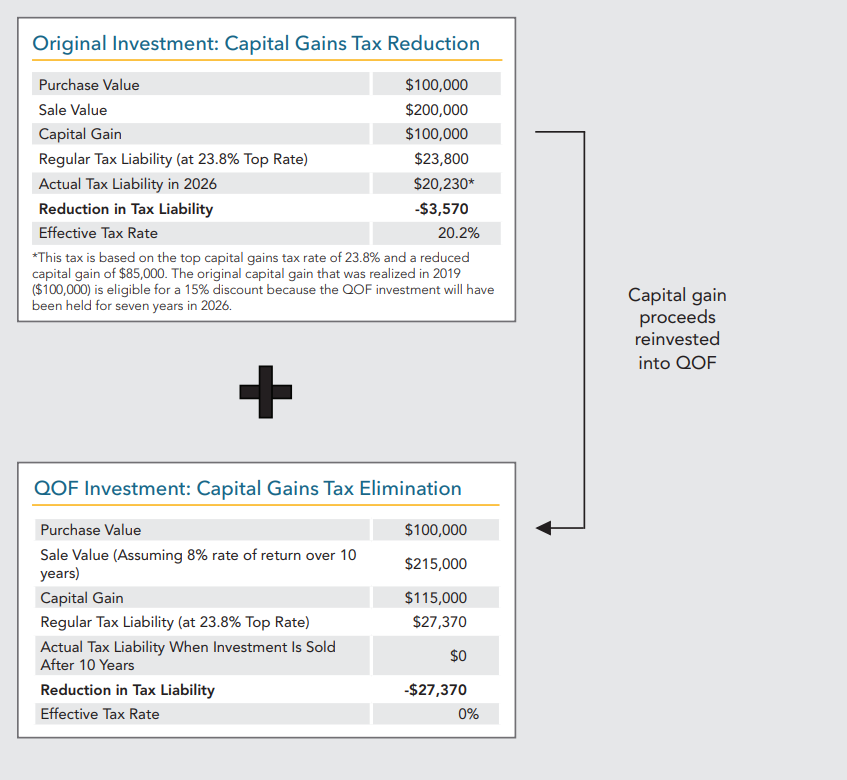

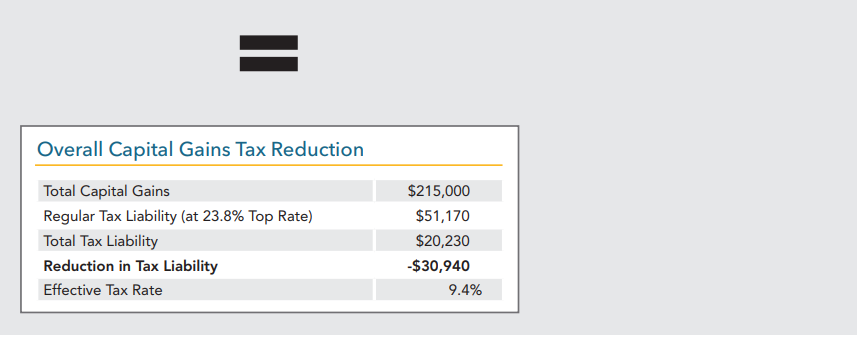

The May Revision includes some policy proposals that, while well-intended, would reduce available revenues. As in the January budget proposal, the revised budget includes a proposal to adopt (or “conform to”) certain provisions of the 2017 federal tax law, some of which would decrease state revenues. One of these items would allow for deferred and reduced capital gains taxes for individuals and corporations that make investments in economically-distressed census tracts designated as Opportunity Zones. The Governor proposes to limit these tax incentives to investments in affordable housing and green technology within the state. Additionally, the tax conformity package includes a provision that would allow small businesses more flexibility in the accounting methods used for tax purposes.

The May Revision also contains a new proposal to exempt diapers and menstrual products from sales taxes for two years, beginning in January 2020. This would result in decreased General Fund revenues of $17.5 million in 2019-20 and $35 million in the following year. Additionally, since a portion of sales tax revenues are allocated to local governments, cities and counties would see revenue reductions. The total state and local revenue losses due to these exemptions is projected to be $38 million in 2019-20 and $76 million in 2020-21.

Revised Budget Proposal Continues to Build Up Reserves to Bolster State’s Fiscal Resilience

California voters approved Proposition 2 in November 2014, amending the California Constitution to revise the rules for the state’s Budget Stabilization Account (BSA), commonly referred to as the rainy day fund. Prop. 2 requires an annual set-aside equal to 1.5% of estimated General Fund revenues. An additional set-aside is required when capital gains revenues in a given year exceed 8% of General Fund tax revenues. For 15 years ─ from 2015-16 to 2029-30 ─ half of these funds must be deposited into the rainy day fund and the other half is to be used to reduce certain state liabilities (also known as “budgetary debt”). Prop. 2 also established a new state budget reserve for K-12 schools and community colleges called the Public School System Stabilization Account (PSSSA). The PSSSA requires that, when certain conditions are met, the state deposit a portion of General Fund revenues into the new reserve as part of California’s Proposition 98 funding guarantee (See Prop. 98 section).

The Governor’s May Revision includes a total transfer of $2.2 billion to the BSA for 2019-20, which will bring the reserve’s balance to $16.5 billion by the end of the fiscal year. Prop. 2 requires that when the BSA balance has reached its constitutional maximum of 10% of General Fund tax revenues, any additional dollars that would otherwise go into the BSA must be spent on infrastructure, including spending on deferred maintenance. However, while the BSA has already reached this maximum (total proposed General Fund Expenditures for 2019-20 are $147 billion), the Governor’s budget assumes that constitutionally required deposits will continue to be made because the account’s current balance was achieved in part through supplemental payments in prior years. This assumption is based on an opinion by the Legislative Counsel, but could be subject to a legal challenge.

The revised budget also includes a deposit of $389.3 million into the PSSSA, the first time such a deposit would be made into this reserve.

Additionally, the 2018-19 budget agreement created the Safety Net Reserve Fund, which holds funds that can be used to maintain benefits and services for CalWORKs and Medi-Cal participants in the event of an economic downturn. The May Revision maintains a proposed $700 million deposit into the Safety Net Reserve, bringing the fund’s balance to $900 million.

Each year, the state also deposits additional funds into a “Special Fund for Economic Uncertainties” (SFEU). The Governor’s proposed budget assumes an SFEU balance of $1.6 billion.

Taking into account the BSA, PSSSA, Safety Net Reserve, and SFEU, the Governor’s proposal would build state reserves to a total of $19.4 billion in 2019-20.

The Governor’s revised proposal continues to prioritize paying down state and local unfunded pension liabilities and paying off outstanding budgetary debt incurred during the Great Recession and its aftermath.

The May Revision continues to include required and supplemental contributions to two state-run retirement systems: the California Public Employees’ Retirement System (CalPERS) and the California State Teachers’ Retirement System (CalSTRS). CalPERS and CalSTRS, like many retirement systems, are not funded at levels that will keep up with future benefits, resulting in the state needing to make higher annual contributions in order to pay down unfunded liabilities.

Beyond statutorily required contributions, the Governor’s revised budget maintains the January proposal to provide a $3 billion supplemental pension payment to CalPERS that would be made in the current fiscal year (2018-19).

In the case of CalSTRS, the budget proposal continues to devote an additional $1.1 billion toward the state’s share of CalSTRS unfunded liabilities. The $1.1 billion comes from Prop. 2 funds (see Reserves section) that are required to be set aside for reducing state liabilities.

In addition, the Governor’s revised budget includes a one-time $3.2 billion non-Proposition 98 payment to CalSTRS to reduce the employers’ (local educational agencies and community colleges) share of unfunded liabilities in response to prior changes in contribution levels and pressures confronting employers. This is slightly higher than the $3 billion proposed in January for this purpose. In 2014, the state enacted AB 1469, increasing the share of CalSTRS costs borne by all parties (the state, employers, and teachers), but particularly increasing the contribution rate of employers. Confronting a series of other pressures, including enrollment decline and increases in the costs of local services, some local educational agencies are in danger of not being able to meet their financial obligations. Overall, the proposed supplemental payment would free up local dollars for investment in education, allow employers to pay down retirement obligations, or close budget deficits.

As with the January proposal, the revised budget would pay off all remaining outstanding budgetary debts and deferrals incurred during the Great Recession.

May Revision Further Expands the California Earned Income Tax Credit

The California Earned Income Tax Credit is a refundable state tax credit that boosts the incomes of low-earning workers and their families, helping them to afford necessities, such as utilities or food. The May Revision proposes to further expand the credit beyond the plan included in the Governor’s January budget and also to rename the credit the “California EITC, a cost-of-living refund.” Specifically, the revised budget would double a component of the California EITC that the Governor proposed creating in January. This component, the “young child tax credit,” would provide an additional $1,000 — up from $500 proposed in January — for each tax filer who is eligible for the California EITC and has at least one qualifying child under age 6. This revised proposal would increase the maximum California EITC for families with at least one qualifying child under age 6 from:

• Nearly $2,900 currently to nearly $3,900 if the family has a total of 3 or more qualifying children;

• From more than $2,500 to more than $3,500 if the family has two qualifying children; and

• From more than $1,500 to more than $2,500 if the family has one qualifying child.

As proposed in January, the young child tax credit would “phase-out” (decline) for families with annual earnings over $28,000. The credit would fully phase out for families with annual earnings of $30,000.

The Administration estimates that the Governor’s revised California EITC expansion plan will reduce state personal income tax (PIT) revenue by $190 million more than in January, increasing the cost of the proposed expansion from $600 million to $790 million. As a result, the total cost of the California EITC is estimated to be about $1.2 billion under the revised proposal, up from $1 billion under the January proposal.

The May Revision maintains the Governor’s January proposal to offset the cost of the expanded California EITC by conforming to several federal tax law provisions — mainly affecting business income – that would, on net, increase state revenue. However, the May Revision increases the number of provisions to which the Governor is proposing that California conform, according to Administration officials. One notable addition is the proposal to conform to federal law that generally prohibits corporations and other taxpayers to carry back a net operating loss (NOL). (A NOL occurs when a taxpayer’s total tax deductions exceed total income for the tax year. NOLs can be claimed by both corporate and individual taxpayers, but are usually related to losses from operating a business.) The Administration projects that, collectively, its conformity package will increase state revenue by $1.7 billion in 2019-20 and by roughly $1.4 billion per year thereafter. Because this package would raise revenue by increasing state taxes — primarily on corporations and other businesses — it would require a two-thirds vote of each house of the Legislature.

The May Revision also proposes to provide $18.7 million in 2019-20 for the Franchise Tax Board (FTB) to develop and administer a program that would give tax filers who qualify for the California EITC the option to receive a portion of their credit as advance monthly payments. Budget documents state that this program “is targeted to begin in 2021,” contingent upon determination by the Department of Finance that this program will not affect tax filers’ eligibility for any state or federal income-based supports. This contingency is in response to concerns that have been raised by the Legislative Analyst’s Office and others that providing periodic, advanced payments of the California EITC could reduce the amount of support families receive from other sources. According to Administration officials, tax filers who expect to qualify for a California EITC of more than $1,200 would be eligible to receive half of their expected credit in advance monthly payments. This would allow participants in the program to receive advance payments of at least $50 per month.

Budget documents do not provide any additional details about the Governor’s January proposal to provide $5 million one-time General Fund to nonprofits, community-based organizations, or governmental entities that provide increased awareness of the California EITC and free tax preparation services.

The Governor’s May Revision also does not extend the California EITC to low-earning immigrants and their children who are currently ineligible due to a rule requiring tax filers and all of the children they claim to have Social Security Numbers (SSNs) valid for work in order to qualify for the credit. Hundreds of thousands of additional low-income working families would become eligible for the California EITC — at relatively little cost — if California permitted tax filers to claim the credit using a federally assigned Individual Taxpayer Identification Number (ITIN) or any federally assigned SSN.

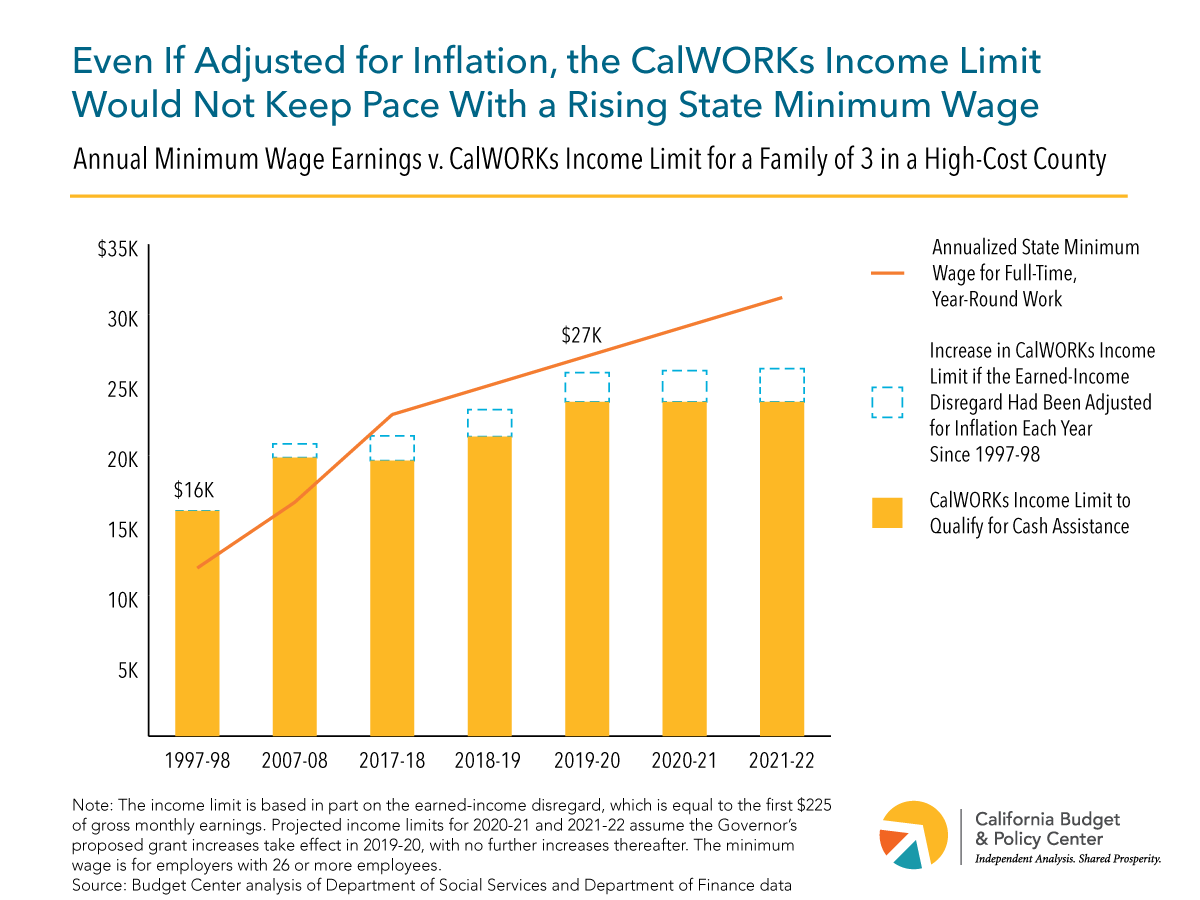

Governor Maintains Proposal to Raise CalWORKs Grants to the Deep Poverty Threshold for Some Families

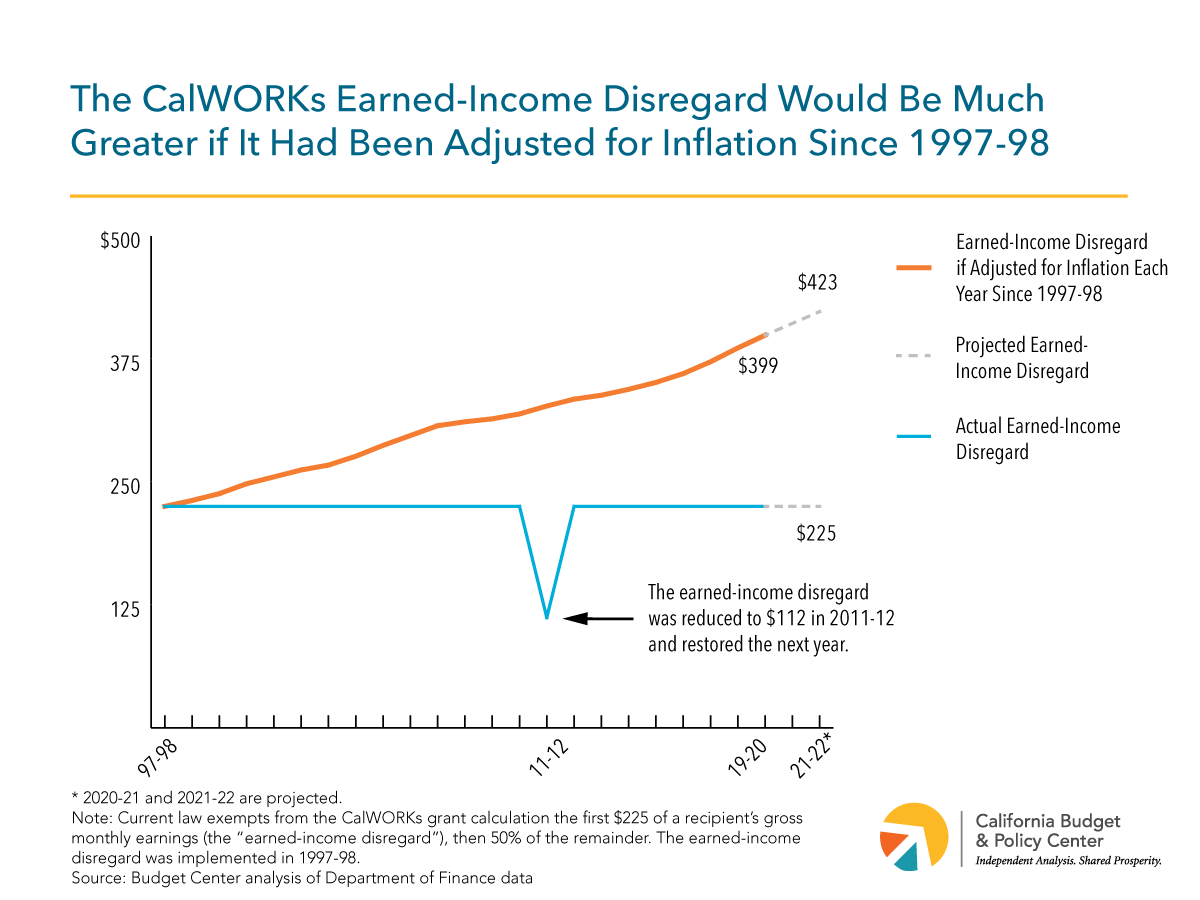

The California Work Opportunity and Responsibility to Kids (CalWORKs) program provides modest cash assistance for over 775,000 low-income children while helping parents overcome barriers to employment and find jobs. Monthly grants are adjusted according to the size of the CalWORKs assistance unit (AU), which is the number of people in the household who are eligible for CalWORKs. According to the Legislative Analyst’s Office, at least one family member is ineligible for cash assistance in about 55% of CalWORKs cases. In these cases, the AU size is smaller than the family size. A family member may be ineligible if they have exceeded the 48-month time limit, have not met work requirements, or due to their immigration status.

The annualized maximum CalWORKs grant for a family of three has been well below the deep poverty threshold (50% of the federal poverty line) for over a decade. To better serve CalWORKs families, the state took the first of three proposed steps in the 2018-19 budget package to raise the maximum grant to the deep poverty threshold. The first step was an across-the-board 10% increase that began April 1, 2019. The proposed second and third steps (subject to annual appropriations in 2019-20 and 2020-21) would seek to close the gap between the new maximum grants and the deep poverty threshold for all CalWORKs families.

In January, Governor Newsom presented a different plan to raise CalWORKs grants. He proposed allocating $347.6 million General Fund in 2019-20 for an additional 13.1% grant increase for all assistance units, effective October 1, 2019. This increase would immediately raise the maximum grant to 50% of the federal poverty line for a three-person AU where the AU size equals the family size. However, the proposed increase would still leave children in a one-person AU (which represent over a quarter of all CalWORKs cases) at 43% of the federal poverty line. Additionally, because the Administration’s proposed budget does not provide funding for ineligible family members, children in all AUs sharing resources with ineligible members (about 55% of all CalWORKs cases) would still live in deep poverty.

May Revision Extends the Duration of California’s Paid Family Leave Program

Paid family leave has the potential to benefit both children and parents, boosting health and well-being, while also providing savings for both businesses and the state. California leads the nation in paid family leave policy, but the state and the nation lag other wealthy countries in terms of the length of leave and the level of benefits. The California Paid Family Leave (PFL) program is funded entirely by workers’ contributions to the state’s Disability Insurance Program. These contributions are housed in a special fund that provides 60% to 70% of a worker’s weekly earnings based on income when a worker takes family leave. Caregivers can currently take up to six weeks of paid time off to care for a family member or bond with a newborn or adopted child. Birth mothers are generally allowed another six weeks to recover from the birth, for a total of 12 weeks.

In January, the Governor expressed a commitment to expand the PFL program to six months in future years. The May Revision takes the first step towards this goal by extending the duration of the PFL program from six weeks to eight weeks, effective July 1, 2020. In order to ensure that the special fund that pays PFL claims can provide additional benefits, the state would reduce the minimum reserve balance to a lower level, which the Administration states will be adequate. Finally, the May Revision affirms the plan to convene a PFL task force in the near future in order to provide recommendations on how to expand the program. The task force recommendations would be due in November and could be included in the 2020-21 budget.

May Revision Maintains Funding for Child Care “Infrastructure” While Expanding Access to Care for Older Children

Subsidized child care allows parents with low and moderate incomes to find jobs and remain employed, but the high cost of care across California often forces parents to make difficult choices about who cares for their child while they go to work. Due to a lack of state and federal funding, in 2017 just 1 in 9 children eligible for subsidized child care and development programs in California were enrolled in a program that could accommodate families for more than a couple hours per day and throughout the entire year.

The Governor’s May Revision maintains provisions included in the January proposal to invest $490 million General Fund in child care “infrastructure,” split equally between a facilities grant program and a workforce development program, as well as $10 million General Fund for a comprehensive plan to increase access to the subsidized child care and development system. The May Revision expands upon the January proposal by proposing new investments that would increase access to subsidized child care for certain children. Specifically, the Administration:

Provides $80.5 million from the Cannabis Tax Fund to add spaces for school-age children. After certain administrative, regulatory, and research activities have been funded, remaining resources in the Cannabis Tax fund are to be directed to a number of programs and services, including youth-related drug education, prevention, and treatment. The Governor proposes using $80.5 million from the estimated $198.8 million available in the Cannabis Tax Fund to increase access to subsidized child care for income-eligible families with school-age kids to “keep these children occupied and engaged in a safe environment, thus discouraging potential use of cannabis.” In a phone call with the Administration, it was noted that this level of funding would serve about 8,700 children.

Provides $40.7 million General Fund to implement a 12-month eligibility period for certain CalWORKs families. Currently, upon initial determination of eligibility, most families participating in the state’s subsidized child care and development system establish a 12-month period of eligibility. However, CalWORKs Stage 1 child care, which is available to families newly enrolling in the welfare-to-work program, do not have this same benefit. The May Revision would extend 12-month eligibility to families participating in CalWORKs Stage 1 child care, which is intended to stabilize childcare for these welfare-to-work families. The ongoing cost is estimated to increase to $54.2 million General Fund in future years.

Provides $12.8 million in federal funds for a pilot emergency child care program. The May Revision creates a pilot program that would provide subsidized child care for families in crisis that are currently waiting for subsidized care in the Alternative Payment Program. The Speaker of the Assembly’s Blue Ribbon Commission on Early Childhood Education proposed a similar program in their recent comprehensive report.

The Administration has made it clear that they intend to invest in the state’s subsidized child care and development system. The May Revision reinforces this intention by maintaining funding for child care infrastructure and a comprehensive plan to increase access to the system, while also providing additional slots for certain children. Yet, the May Revision does not provide more low- and moderate-income families with young children with access to subsidized child care, despite years-long waiting lists and a high level of unmet need.

Governor Maintains Investment in Child Savings Accounts for Kindergarteners

A Child Savings Account (CSA) is an account established for children as early as birth that builds assets over time. CSAs are generally seeded with an initial deposit from a government agency or another sponsoring organization, then built with contributions from family, friends, or the child. Once the child reaches adulthood, the savings are typically used for higher education, though they can also support homeownership or other asset-building investments.

The May Revision maintains a one-time investment of $50 million General Fund for Child Savings Account pilot programs and identifies the California Student Aid Commission, with consultation from First 5 California, as the administrator of the pilot programs.

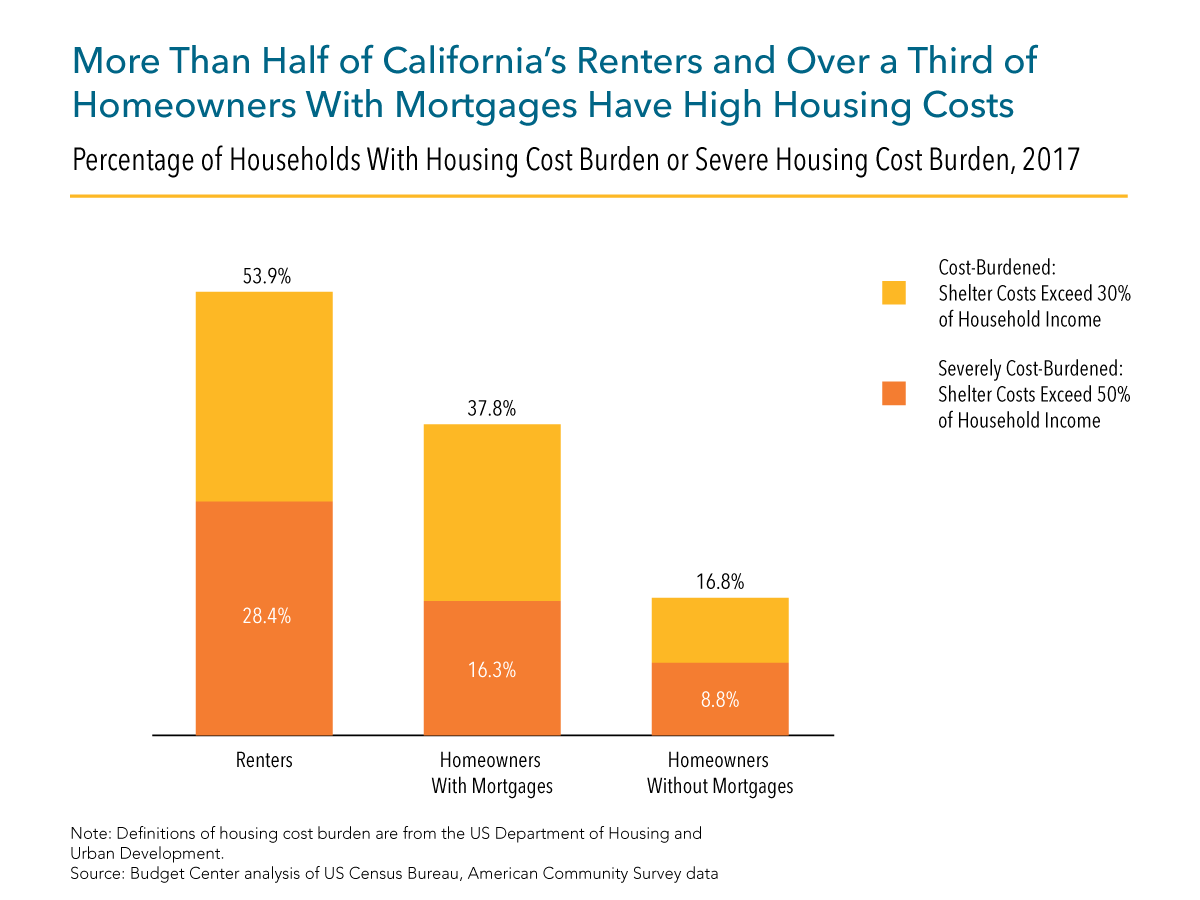

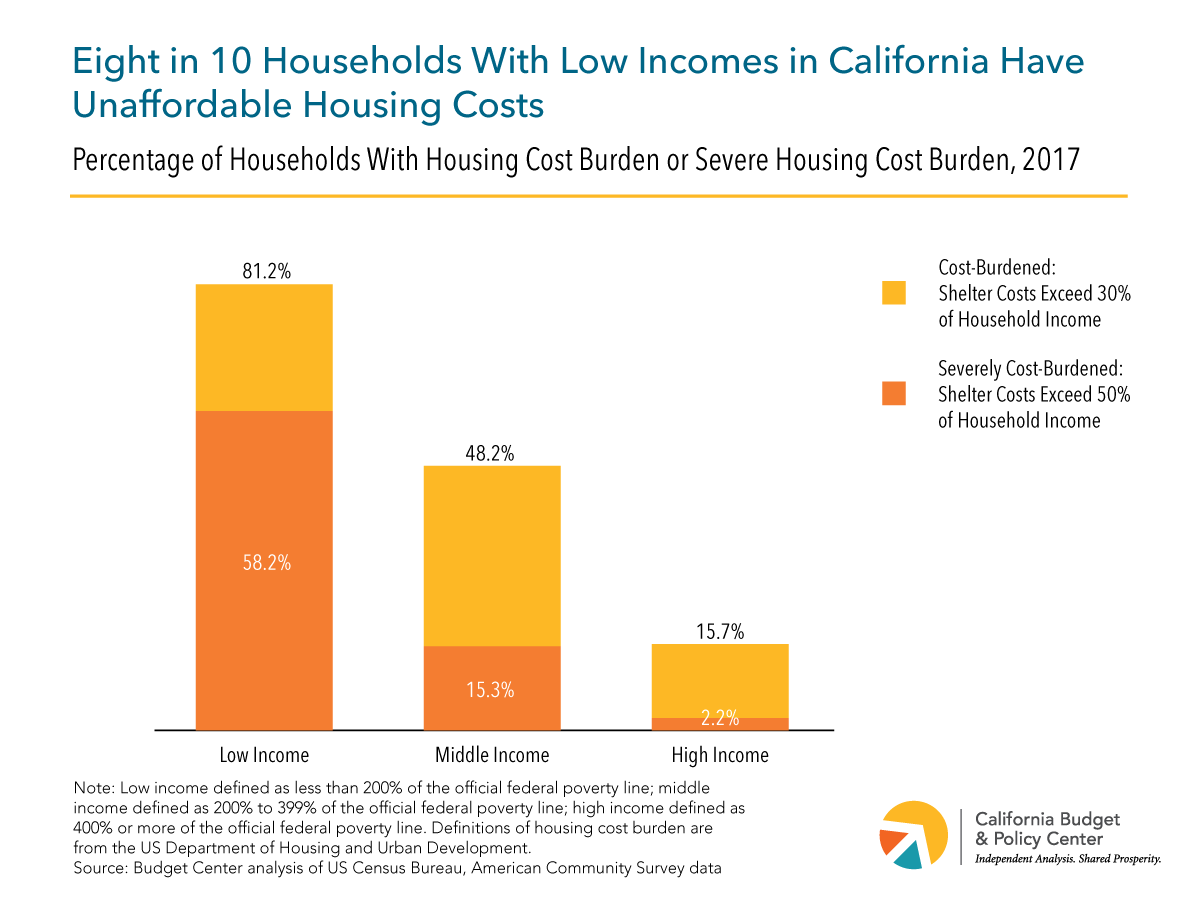

May Revision Maintains Housing Production Expenditures, Adds Funds for Legal Aid for Renters

More than half of California renter households pay more than 30% of their income toward rent. The state’s lowest-income households are most likely to struggle with housing affordability, and high housing costs are a key driver of California’s high poverty rate. The Governor’s May Revision generally maintains the state investment in housing production proposed in January, with some modification of funding allocation and some minor increases in spending.

Several proposals relate to local housing production goals and accountability. Specifically, the May Revision:

Reallocates $500 million in local incentive funds for housing production. In January, the Administration proposed $750 million one-time General Fund to support local planning and incentives for housing production, including $500 million to be awarded for “general purposes” as local jurisdictions meet housing production milestones. The May Revision reallocates this $500 million to the Infill Infrastructure Grant Program administered by the Department of Housing and Community Development, which funds infrastructure needed to support development of higher-density and mixed-income housing in infill locations. For the $250 million proposed in the January budget for planning, the Administration also adds school districts and county offices of education to the jurisdictions eligible for support (e.g., for planning for teacher housing).

Maintains the Governor’s January proposal to link local transportation funding to housing production goals. Specifically, the Administration proposes that transportation funds available through Senate Bill 1, the Road Repair and Accountability Act of 2017 (the “gas tax”), be distributed to local jurisdictions “upon compliance with housing element law and zoning and entitling to meet updated housing goals.”

Retains the January plan to “revamp” the Regional Housing Needs Allocation (RHNA) process through which local housing production goals are set, but proposes maintaining the current RHNA process for the short-term. The Department of Housing and Community Development would work toward developing long-term housing production targets through a new RHNA process by 2022.

The Governor proposes no additional state tax expenditures in the May Revision for affordable housing production through the state Low Income Housing Tax Credit (LIHTC), maintaining the boost of $500 million proposed in January as well as the January budget’s increased commitment to supporting mixed-income housing with both tax credits and loans. To support preservation and rehabilitation of existing affordable housing units, the May Revision includes a new proposal to modify the existing LIHTC program to allow for “deeper subsidies for specified preservation projects,” but no increase in overall LIHTC expenditures for this purpose is proposed.

Additional proposals relate to use of excess state property and cap and trade proceeds. Building on the January proposal to make excess state property available for affordable and mixed-income housing demonstration projects, the May Revision adds $2.5 million one-time General Fund, as well as $780,000 ongoing and four staff positions, to enable the Department of Housing and Community Development to facilitate and monitor the use of state land for these housing projects. Funding from cap and trade auction proceeds is available to support housing production and other neighborhood projects through the Transformative Climate Communities program. The Governor’s January budget proposed $40 million for this program, and the May Revision allocates an additional $92 million one-time from higher-than-anticipated cap and trade revenues, bringing the total to $132 million.

As a new proposal, the May Revision proposes allocating $20 million one-time to support legal aid for renters to resolve landlord-tenant disputes. Funds would be distributed as grants to nonprofit legal aid organizations through the Judicial Branch’s Equal Access Fund.

May Revision Proposes Some Additional Funding to Address Homelessness

California has nearly 25% of the nation’s population of homeless individuals, with an estimated 134,000 homeless residents as of January 2017. In the May Revision, the Administration continues to highlight homelessness as a key challenge facing California. The revised budget includes increases in funding for some specific proposals that address the needs of individuals who are homeless or at risk of homelessness:

The January proposal’s allocation of $500 million in one-time General Fund dollars for local jurisdictions to support homeless emergency aid would be increased by $150 million, for a new total of $650 million. The January proposal divided these funds between $300 million for activities directly related to shelter or navigation center development and $200 million as incentive funds available “for general purposes,” but the May Revision does not make this distinction. The May Revision also specifies how these funds would be allocated among jurisdictions, with $275 million for the state’s 13 most populous cities, $275 million for counties, and $100 million for Continuums of Care. Eligible uses for the funds would also be expanded to include hotel/motel conversions, permanent supportive housing, rapid re-housing, and jobs programs.

A $20 million one-time augmentation from the Mental Health Services Fund is proposed for counties that do not currently operate Whole Person Care Pilot Programs, adding to the $100 million for Whole Person Care Pilots included in the January budget. The increase in funding in the May Revision would allow these additional counties to coordinate health, behavioral health, and social services, including housing, for targeted individuals, with priority for individuals with mental illness who are homeless or at risk of homelessness (see also the Mental Health section).

To support college students who are homeless or housing insecure, the May Revision proposes $10 million in new ongoing General Fund for the state’s public four-year universities ($6.5 million for the California State University and $3.5 million for the University of California). This proposal builds on the $30 million dedicated to addressing student food and housing insecurity in the January budget (see also the CSU and UC section).

The Administration notes that with these additions, overall state funding to address homelessness will total $1 billion more than the amount dedicated to homelessness in the current state budget. This $1 billion increase includes all funding for housing and mental health services for homeless individuals proposed in Governor Newsom’s January budget, the new funding described above, and additional spending proposed in the May Revision to address staffing shortfalls in the public mental health system and to provide legal aid for renters.

The May Revision also proposes that after the closure of the state’s Fairview Developmental Center in Orange County (expected by the end of 2019), the state repurpose the site by leasing a building or buildings to a local jurisdiction to provide permanent supportive housing for individuals who are homeless or at risk of homelessness.

May Revision Makes Modest Adjustments to Immigration Proposals

California has the largest share of immigrant residents of any state, and half of all California workers are immigrants or children of immigrants. Given the prominence of immigrants in California’s population and the state’s economy, recent and ongoing federal actions that limit immigration, aggressively enforce immigration laws, and seek to exclude immigrant communities have significant negative implications for California. The May Revision creates two new pilot programs but otherwise maintains the proposals included in the January budget with minor adjustments. Specifically, the updated spending plan:

Creates two pilot projects to support unaccompanied minors and Temporary Protected Status beneficiaries. The January budget proposal allocated $10 million out of the $58 million total for immigrant legal services to the Department of Social Services to unaccompanied undocumented minors and Temporary Protected Status beneficiaries. The Governor proposes to use up to $5 million of these funds for two pilot projects. The first pilot project would provide “mental health evaluations related to legal defense” and the second pilot project would develop a family reunification navigator to connect undocumented minors and their families with services in the community.

Maintains expansion of eligibility for comprehensive Medi-Cal coverage to undocumented young adults ages 19 through 25. This proposal remains unchanged from January but reflects a decrease in state funding as a result of a later start date and revised estimates of the number of people eligible. The revised budget delays the implementation date to January 1, 2020, six months later than the initial proposed start date. The May Revision estimates that 90,000 undocumented young adults would enroll in full-scope Medi-Cal coverage during the first year, a decrease from the Governor’s 138,000 projection in January.

Provides a modest increase in funding for legal services for undocumented immigrant students and their families at the UC beginning in 2022-23. The May Revision increased funding for legal services at the UC to $1.7 million, a modest increase from $1.3 million initially allocated in the Governor’s January budget proposal. The Administration noted in January that the 2018-19 budget allocated sufficient funding to sustain legal services through 2021-22.

The Governor remains adamant that the State “be a part of a multi-lateral solution” to address immigration issues nationally and in California. Still, the revised budget proposal omits key priorities advocates and legislators have pushed for in the recent months. Proposals not included in the May Revision include extending the CalEITC to immigrant workers who file taxes with an Individual Taxpayer Identification Number (ITIN) and expanding full scope Medi-Cal coverage to immigrants 26 years and older. While California continues to make strides to provide support and create safe communities for immigrants, ensuring that all Californians are protected and can access economic opportunity requires enacting policies that extend vital state supports to immigrants and their families.

May Revision Maintains Proposals to Improve Health Insurance Affordability and Move Toward Universal Coverage

Building on the federal Affordable Care Act (ACA), California has substantially expanded access to health coverage in recent years. For example, more than 13 million Californians with modest incomes receive free or low-cost health care through Medi-Cal (California’s Medicaid program) — several million more than before the ACA took effect. Another 1.2 million Californians with incomes up to 400% of the federal poverty line — $48,560 for an individual in 2019 — receive federal premium subsidies to reduce the cost of coverage purchased through Covered California, our state’s health insurance marketplace. Despite these gains, around 3 million Californians remain uninsured, health care costs continue to rise, and many people face both high monthly premiums and excessive out-of-pocket costs — such as copays and deductibles — when they use health care services.

The May Revision maintains, with some changes, key proposals that the Governor introduced in January to help move California toward universal health coverage. Specifically, the revised budget:

Maintains the Governor’s proposal to create state subsidies to reduce the cost of health insurance purchased on the individual market. The Governor’s original proposal allowed Californians with incomes between 250% and 600% of the federal poverty line to receive these new subsidies. The May Revision would extend these subsidies to Californians with incomes between 200% and 250% of the poverty line as well. Overall, these new state subsidies would cost an estimated $295 million in 2019-20, rising to $380 million by 2021-22, and would be paid for with revenues from a new state penalty on residents who do not obtain comprehensive health coverage (see next bullet). The May Revision assumes that about three-quarters of subsidy expenditures would benefit Californians with incomes between 400% and 600% of the poverty line, with an average subsidy of around $100 per month. Subsidies would average around $10 per month for residents with incomes between 200% and 400% of the poverty line. (Californians in this income range would continue to be eligible for federal ACA subsidies if they purchase health insurance through Covered California.) Finally, the May Revision assumes the subsidies would take effect on January 1, 2020, and expire in three years.

Continues to assume the state will impose a new requirement for Californians to carry health insurance or pay a penalty. The ACA included an “individual mandate” to encourage young and healthy people to buy health insurance. The goal was to create healthier “risk pools” and keep premiums lower than they otherwise would be if only older and sicker people signed up for coverage. With limited exceptions, people who failed to comply with this requirement had to pay a penalty to the federal government. However, Congress and President Trump eliminated the individual mandate penalty effective January 1, 2019. The Governor proposes to establish an individual mandate at the state level, which would require Californians to obtain comprehensive health care coverage or pay a penalty. The May Revision assumes this penalty would take effect on January 1, 2020, and would raise an estimated $317 million in 2020-21, rising to $353 million in 2022-23. As described above, these revenues would be used to fund the proposed state subsidies.

Maintains the Governor’s proposal to expand eligibility for comprehensive Medi-Cal coverage to undocumented young adults who otherwise meet the program’s requirements, but changes the implementation date. States are prohibited from using federal dollars to provide comprehensive, or “full-scope,” Medicaid coverage to undocumented immigrants. States, however, may use their own funds to provide such coverage. In 2016, California expanded full-scope Medi-Cal coverage to undocumented children and youth through age 18 who meet all other eligibility requirements, including income limits. In January, the Governor proposed to extend this policy to undocumented Californians ages 19 through 25, effective no sooner than July 1, 2019. At the time, it was estimated that 138,000 undocumented young adults would sign up for full-scope Medi-Cal under this policy. In contrast, the May Revision assumes that this change would take effect no sooner than January 1, 2020, with about 90,000 young adults signing up during the first year.

May Revision Allocates an Additional $263 Million in Proposition 56 Revenues to Support the Medi-Cal Program

Approved by California voters in 2016, Proposition 56 raised the state’s excise tax on cigarettes by $2 per pack and triggered an equivalent increase in the state excise tax on other tobacco products. These increases took effect on April 1, 2017. Prop. 56 requires most of the revenues raised by the measure to go to Medi-Cal, which provides health care services to more than 13 million Californians with low or moderate incomes.

In January, the Administration projected that Medi-Cal will receive around $1 billion in Prop. 56 revenues in 2019-20. The Governor proposed to use these funds to increase payments to doctors, dentists, and other providers as well as to support other services, including early developmental screenings for children, screenings for trauma for children and adults, and family planning services.

The May Revision indicates that Medi-Cal will receive an additional $263 million in Prop. 56 revenues “due to a one-time fund reallocation.” The revised budget allocates these funds to several purposes, including $120 million for a loan repayment program for doctors and dentists who commit to serve Medi-Cal beneficiaries and $60 million to train providers to conduct trauma screenings. In addition, the Governor proposes to use $11.3 million of these Prop. 56 funds to restore optician and optical lab services for adults enrolled in Medi-Cal, effective no sooner than January 1, 2020. This optional Medi-Cal benefit was cut during the Great Recession to help close a state budget shortfall. Finally, the May Revision assumes that “the package of Proposition 56 investments” will expire on December 31, 2021.

Revised Budget Increases Funding for Home Visiting and Black Infant Health Programs

A new home visiting initiative in the California Work Opportunity and Responsibility to Kids (CalWORKs) program was instituted in the 2018-19 budget and began on January 1, 2019. The program provides up to 24 months of evidence-based home visiting for CalWORKs parents who are either pregnant or parenting a child under age 2, with a priority for first-time parents. A total of $158.4 million in federal TANF and state General Fund dollars was set aside to fund home visiting through calendar year 2021, after which the initiative will be subject to annual appropriation. In January, Governor Newsom proposed allocating $78.9 million for the 2019-20 budget year. His revised budget includes an additional $10.7 million to reflect updated caseload projections for a total of $89.6 million in 2019-20. The home visiting program is expected to serve 18,500 CalWORKs cases.

The Governor’s January proposal also called for $30.5 million General Fund to the Department of Public Health to support the Black Infant Health program ($7.5 million) and to expand home visiting outside of CalWORKs ($23 million). The proposed $23 million represented the state’s first financial investment in home visiting for non-CalWORKs families. In the revised proposal, the Administration includes an additional $34.8 million in reimbursements from the Department of Health Care Services to support Medicaid-eligible activities. Of the $34.8 million, $12 million ($11.95 million unrounded) will support Black Infant Health and $22.9 million ($22.87 million unrounded) will support the California Home Visiting program. With these reimbursements, the total proposed investment to these programs is $65.3 million in 2019-20.

May Revision Builds on Investments in Mental Health Services

Mental health services in California are primarily provided by counties, with funding from the state and federal government. The mental health system confronts many challenges, such as rising homelessness (a substantial share of individuals who are homeless struggle with mental illness) and the need for crisis services. To help address these challenges, the revised budget includes additional funding and new proposals to improve mental health outcomes. Specifically, the May Revision:

Includes a one-time investment of $20 million Mental Health Services Fund over five years for counties that currently do not operate Whole Person Care Pilot Programs — which provide additional supportive housing services for people who are homeless or at risk of becoming homeless, with a focus on mental health. This is in addition to the $100 million one-time General Fund proposed in the Governor’s budget for counties that currently operate pilots.

Allocates $3.6 million Mental Health Services Fund annually for three years to the Department of Health Care Services to establish a Peer-Run Mental Health Crisis Line. This crisis line would be a resource for those “on the brink of a mental health crisis,” according to the Governor’s budget summary.

The Governor’s Revised Budget Includes Additional Funding for State Hospitals

The Governor’s revised budget proposes additional funding to the Department of State Hospitals (DSH), which manages the state mental health hospital system. Specifically, the May Revision:

Provides $5.7 million General Fund for DSH to contract for a 78-bed community step-down program to serve individuals with a mental illness — both “Mentally Disordered Offenders and Not Guilty by Reason of Insanity commitments” — who are preparing for conditional release from state hospitals within 18 to 24 months. This funding also includes increasing an existing contract by four beds for a total of 24 beds.

Provides $2.2 million General Fund for DSH to expand the use of telepsychiatry to treat patients remotely via video-conferencing.

May Revision Includes Additional Investments in the Health Care Workforce

In order to address increasing demand for health care providers, the Governor’s revised budget:

Maintains $50 million one-time General Fund to increase support for mental health workforce programs. This funding would be administered by the Office of Statewide Health Planning and Development.

Includes $38.7 million Proposition 56 funds to develop residency programs at hospitals throughout the state. These programs would be administered and operated by the University of California in partnership with Physicians for a Healthy California.(see Prop. 56 section)

Includes $33.3 million ongoing General Fund to the Song-Brown Health Care Workforce program, which provides grants to support primary care residency training programs in California.

Invests $100 million from the Mental Health Services Fund in the new Workforce Education and Training (WET) 5-year plan. The program aims to address the shortage of mental health practitioners in the public mental health system.

The May Revision Scales Back Early Learning Investments

State policymakers have taken steps in recent years to expand access to full-day early learning opportunities for preschool-age children. The Governor’s January budget proposal continued this trend by providing 30,000 full-day California State Preschool Program (CSPP) slots over a three-year period and investing $750 million one-time General Fund in grants for kindergarten facilities. The May Revision scales back on these proposals. Specifically, the Administration:

Provides $600 million one-time General Fund for grants for full-day kindergarten. The May Revision reduces the proposed one-time funding for the grant program by $150 million. The $600 million is to be used over a three-year period, but grants administered during the first two years would be restricted to schools that will be transitioning from part-day to full-day kindergarten programs. The state is also proposing to increase the state share of the grant from 50% to 75% for programs moving to a full day to incentivize participation.

Provides $31.4 million General Fund to increase the number of full-day slots in the CSPP. This is down from the proposed $124.9 million included in the January proposal — a difference of $93.5 million. The January proposal signaled the intent to continue expanding the CSPP over the next two fiscal years, but in the May Revision the Governor notes that additional spaces for children will be subject to available revenues in future years, given lower projected revenues.

The May Revision maintains other CSPP provisions included in the January proposal, such as shifting a share of CSPP funding to the General Fund to free up funding for non-profit providers, and eliminating the parental work or school requirement for the full-day CSPP. The May Revision also maintains $10 million one-time General Fund for a comprehensive plan to increase access to the subsidized child care and development system, including the CSPP.

Increased Revenues Boost the Minimum Funding Level for Schools and Community Colleges, May Revision Includes First-Ever K-14 Education Rainy Day Fund Deposit

Approved by voters in 1988, Proposition 98 constitutionally guarantees a minimum level of funding for K-12 schools, community colleges, and the state preschool program. Changes in state General Fund revenues tend to affect the Proposition 98 guarantee, and the May Revision’s estimates of 2018-19 and 2019-20 revenues are up compared to those made in January’s budget proposal. As a result, the May Revision assumes a 2019-20 Prop. 98 funding level of $81.1 billion, $389.3 million above the level assumed in the Governor’s proposed budget. The May Revision also assumes Prop. 98 funding levels of $78.1 billion in 2018-19 and $75.6 billion in 2017-18, up $278.8 million and $78.4 million, respectively, from the levels assumed in January. The revised spending plan reflects a 2017-18 Prop. 98 funding level that is approximately $117 million above that year’s minimum funding guarantee.

The revised budget projects that a deposit of $389.3 million into the Public School System Stabilization Account (PSSSA) will be required in 2019-20, which would reflect the entire increase in 2019-20 Prop. 98 funding above the level assumed in the January budget proposal. The deposit to the PSSSA would be the first made into this state budget reserve for K-12 schools and community colleges. The PSSSA was established by Proposition 2, a ballot measure voters approved in November 2014 that amended the state constitution. In a fiscal year immediately after the balance of the PSSSA is equal to or greater than 3% of the total share of the Prop. 98 minimum funding guarantee allocated to K-12 school districts, current law limits the amount that local school districts may keep in their budget reserves. However, because the $389.3 million deposit to the PSSSA in 2019-20 would be significantly below the 3% threshold (approximately $2.1 billion), limits on school district reserves would not be required in 2020-21.

The May Revision also maintains a January budget proposal that would change how the final funding level guaranteed under Prop. 98 is certified, a process established by the 2018-19 budget agreement. The overall effect of the Governor’s January proposal would shift the risk associated with the uncertainty in the annual Prop. 98 guarantee from K-12 school and community college districts to the state.

The largest share of Prop. 98 funding goes to California’s school districts, charter schools, and county offices of education (COEs), which provide instruction to approximately 6.2 million students in grades kindergarten through 12. The May Revision proposes to increase support for special education services and to further reduce school districts’ spending obligations for retirement costs. Specifically, the May Revision:

Increases funding by $119.2 million to support special education services, for a total of $696.2 million in ongoing funding. The Governor’s January budget proposed $577 million to provide grants to school districts with large shares of students with disabilities and other disadvantaged students — English learners, students from low-income families, and foster youth — to supplement services for students in special education programs and for preventative services. The May Revision references concerns about coordination between local general education and special education programs, but does not provide information about how the proposed increase in funding would be used.

Provides $44.8 million in one-time funding to support classroom educators. The revised budget proposes to use this funding to provide training and resources to build capacity around a variety of subjects including social emotional learning and computer science.