What is Proposition 98? Guaranteed School Funding Explained

January 2025 | By California Budget & Policy Center

Watch to learn more

Proposition 98, passed in 1988, is a cornerstone of California school funding, guaranteeing minimum funding levels for K-12 education funding and community college funding. But how does it work? And what does it mean for public schools and the state budget?

In this explainer video, we break it all down, including the funding sources, calculations, and its impact on education funding in California. Learn how this law ensures a steady financial base for schools while adapting to the state’s fiscal conditions.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

The legislative process — also known as the policy bill process — provides a key pathway through the state Legislature for Californians who want to change state law.

Each year, members of the state Assembly and Senate collectively introduce thousands of bills that move, partially or all the way, through the legislative process. These bills propose changes to one or more of California’s nearly 30 state codes — changes that take effect only if a bill is passed by both houses and signed by the governor.

Proposals to amend the state Constitution also move through the legislative process. While Assembly and Senate constitutional amendments do not require the governor’s signature, they do need voter approval in order to take effect.

The legislative process operates according to rules outlined in the state Constitution, in state law, and in two-house agreements (“joint rules”) adopted by the Assembly and Senate at the outset of each two-year legislative session.

Written and unwritten rules that are unique to each house as well as to various committees within each house — and that can change from year to year — also shape the legislative process with opportunities for public involvement.

It is important to highlight that the state budget process provides a separate pathway through the Legislature for changing state law (through budget-related “trailer bills”). Compared to the legislative process, the state budget process has distinct rules, deadlines, and — in some cases — decision-makers. Advocates typically use both the state budget process and the legislative process to advance their policy goals. However, the remainder of this guide focuses exclusively on the legislative process.

Opportunities for Public Engagement in the Legislative Process

The public has many opportunities to engage with state policymakers during the legislative process. For example, members of the public can:

Suggest bill ideas to members of the Legislature.

Build/renew relationships with lawmakers and their staff in order to develop familiarity and trust — which is critical to securing bill authors and advancing legislation.

Meet with lawmakers and their staff as well as with members of the governor’s administration to make the case for legislation and address any concerns.

Write letters to committees and individual legislators sharing opinions about bills that have been introduced.

Attend legislative committee hearings to share opinions about bills during public comment periods.

Urge the governor to sign or veto legislation.

Policy Committees

Assembly and Senate policy committees consider the policy implications of a bill. Each house’s leadership assigns bills to policy committees based on subject matter and other factors. Bills may be reviewed by a single policy committee in each house or by multiple policy committees.

The state Senate has more than 20 standing policy committees, and the Assembly has over 30. Examples include the Assembly Education Committee and the Senate Revenue and Taxation Committee. Bills that are approved at this stage — potentially with amendments — go to the appropriations committee for further review.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

Appropriations committees estimate the cost of bills. If the cost meets or exceeds certain thresholds, the bill generally is placed on the committee’s suspense file, which is essentially a “holding pen” for bills that will receive additional scrutiny. The dollar thresholds are relatively low in both houses. In the Senate, the threshold ranges from $50,000 to $150,000, depending on which state fund the money would come from. The threshold in the Assembly is $150,000 regardless of the fund.

Twice per year, appropriations committees convene hearings where they rapidly announce the fate of the hundreds of bills on their suspense files. Bills voted off the suspense file — often with amendments — advance to the Assembly or Senate floor, while bills that are held “on suspense” in the appropriations committee are dead for the year.

Bills can be held on suspense for any number of reasons, including concerns about their cost. However, committee chairs typically do not publicly explain why some bills advance to the floor while others are held.

Floor Votes: Simple Majority or Supermajority

Once a bill clears the final committee in its “house of origin,” it is scheduled for a debate and vote on the house floor. Most bills require only a simple majority vote to advance off the floor — 41 votes in the 80-member Assembly and 21 votes in the 40-member Senate.

However, a two-thirds (supermajority) vote of each house is required if the bill:

Would create a new tax or increase an existing tax.

Contains an “urgency” clause that allows it to take effect immediately rather than on January 1 (the typical date).

Proposes to amend the state Constitution — a change that ultimately must be approved by a majority of voters in a statewide election.

Rinse and Repeat: Process Moves to the Second House

If a bill passes the first house, it moves to the second house, where it repeats the process — policy committee(s), appropriations committee, floor vote. Bills are typically amended again at this stage. If approved with amendments, the bill goes back to the first house for a “concurrence” vote. Bills passed on concurrence go to the governor for final consideration.

Learn the Lingo

Understanding budget-related terms is essential for navigating the state budget and legislative process and effectively engaging with decision-makers to advocate for just policy solutions for Californians.

Thumbs Up or Thumbs Down: Approved Bills Go to the Governor

Once a bill receives final legislative approval it goes to the governor, who can:

Sign the bill into law.

Allow the bill to become law without a signature.

Veto — reject — the bill. The Legislature can override a veto with a two-thirds vote of each house. However, veto overrides are extremely rare.

Bills passed by a simple majority vote typically take effect on January 1 of the next calendar year. Urgency statutes, tax increases, and certain other bills take effect as soon as they become law.

Committee agendas and other publications, floor session and committee schedules, the annual legislative calendar, and live and archived video streaming of legislative proceedings.

Kristina Bas Hamilton, Changemaker: An Insider’s Guide to Getting Sh*t Done at the California Capitol (October 2023).

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Watch to learn more about trailer bills in California

Trailer bills play a crucial role in California’s budget process by making the legal changes needed to implement policies in the Budget Act. This video explains how trailer bills work, their journey through budget committees, and the voting rules they must follow. You’ll explore how these bills impact vital areas like health, housing, and education to expand your knowledge of California’s legislative process.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

Every year, California’s 58 counties adopt local budgets that provide a framework and funding for critical public services and systems — from health care and safety net services to elections and the justice system.

But county budgets are about more than dollars and cents.

A county budget expresses our values and priorities as residents of that county and as Californians. At its best, a county budget should reflect our collective efforts to expand opportunities, promote well-being, and improve the lives of Californians who are denied the chance to share in our state’s wealth and who deserve the dignity and support to lead thriving lives.

Because county budgets touch so many services and our everyday lives, it is critical for Californians to understand and participate in the annual county budget process to ensure that county leaders are making the strategic choices needed to allow every Californian — from different races, backgrounds, and places — to thrive and share in our state’s economic and social life.

This guide sheds light on county budgets and the county budget process with the goal of giving Californians the tools they need to effectively engage local decision-makers and advocate for fair and just policy choices.

Key Takeaways

the bottom line

County budgets are about more than dollars and cents.

Crafting the annual spending plan provides an opportunity for county residents to express their values and priorities.

County and state budgets are inherently intertwined because counties are legal subdivisions of California and perform functions as agents of the state.

To a large degree, county budgets reflect funding and policy choices made by the governor and the Legislature as well as by federal policymakers.

However, county budgets also reflect local choices, as counties allocate their limited “discretionary” dollars to local priorities.

Counties’ ability to raise revenue to support local services is constrained.

For example, counties cannot increase the property tax rate to boost support for county-provided services.

Counties may increase other taxes to establish or improve local services, but only with voter approval.

Both state law and local practices shape the county budget process.

State law establishes minimum guidelines that counties must adhere to in developing their budgets.

Counties can — and often do — exceed these state guidelines in crafting their budgets and sharing them with the public.

The county budget process is cyclical, with decisions made throughout the year.

The public has various opportunities for input during the budget process.

This includes writing letters of support or opposition, testifying at budget hearings, and meeting with supervisors, the county manager, and other county officials.

In short, Californians have the opportunity to stay engaged and involved in their county’s budget process year-round.

California’s Counties: The Basics

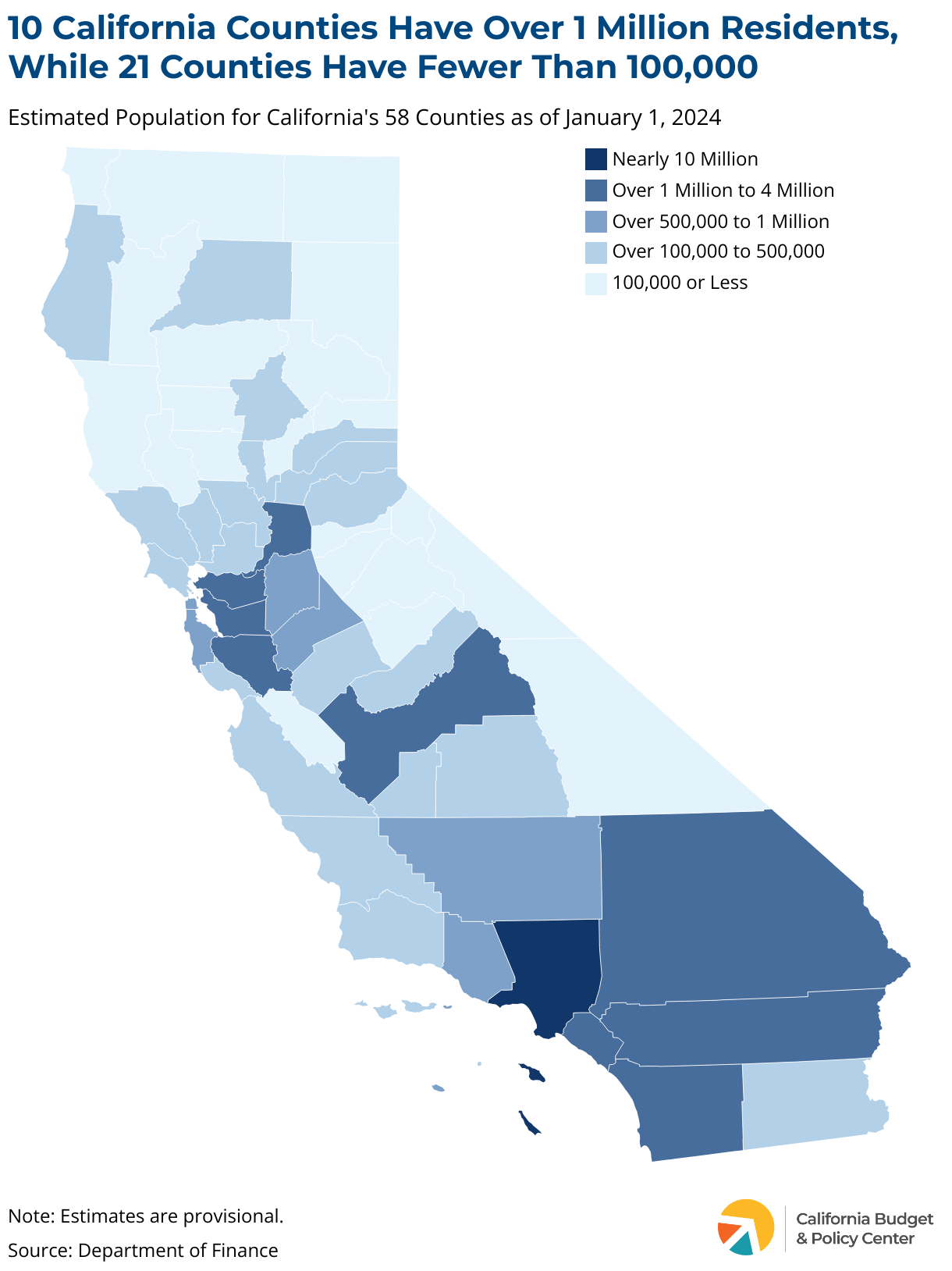

California Has 58 Counties That Vary Widely In Population and Size

California’s counties range widely in population.

10 counties have more than 1 million residents, and 21 counties have fewer than 100,000 residents.

Los Angeles County has the largest population of any county in the state (9.8 million).

Alpine County has the smallest population (less than 1,200).

California’s counties also differ considerably in size.

San Bernardino is California’s largest county (20,057 square miles).

San Francisco — which has the state’s only consolidated city and county government — is the smallest county (47 square miles).

California's Counties Are Legal Subdivisions of the State

California’s Constitution requires the state to be divided into counties. Counties’ powers are provided by the state Constitution or by the Legislature.

The Legislature may take back any authority or functions that it delegates to the counties.

There are 44 general-law counties and 14 charter counties.

Unlike general-law counties, charter counties have a limited degree of independent authority over certain rules that pertain to county officers. However, charter counties lack any extra authority with respect to budgets, revenue increases, and local regulations.

Counties Have Multiple Roles in Delivering Public Services

Counties operate health and human services programs as agents of the state.

These include foster care; child welfare services; Medi-Cal (health care for low-income residents); public health; behavioral health (mental health services and substance use disorder treatment); the CalWORKs welfare-to-work program; and others.

Counties carry out a broad range of countywide functions.

These include overseeing elections and operating — along with cities and the courts — the local justice system.

Counties provide some municipal-type services in unincorporated areas.

These include policing, fire protection, libraries, planning, and road repair.

Other Types of Local Agencies Also Deliver Public Services

Counties provide public services alongside other agencies that operate at the local level. A wide array of local services are delivered by:

More than 2,000 independent special districts, which provide specialized services such as fire protection, water, or parks.

More than 900 K-12 school districts, which are responsible for thousands of public schools.

More than 480 cities, which provide policing, fire protection, and other municipal services.

More than 70 community college districts, which oversee 113 community colleges.

Counties Are Governed By an Elected Board of Supervisors

The Board of Supervisors consists of five members in all but one county.

The City and County of San Francisco has an 11-member Board and an independently elected mayor.

Because counties do not have an elected chief executive (except for San Francisco), the Board’s role encompasses both executive and legislative functions.

These functions include setting priorities, approving the budget, controlling county property, and passing local laws.

Boards also have a quasi-judicial role.

For example, Boards may settle claims and hear appeals of land-use and tax-related issues.

A Number of Other County Officers Also Are Elected

Along with an elected Board of Supervisors, the state Constitution requires counties to elect:

An assessor.

A district attorney.

A sheriff.

Although not required by the state Constitution, a few other key county offices are typically filled by election, rather than by Board appointment. These include:

The auditor-controller.

The county clerk.

The treasure-tax collector.

The County Manager Oversees the Daily Operations of the County Government

The top administrator in each county is appointed by the Board of Supervisors.

Counties have various titles for this position. This guide uses the generic term “county manager.”

San Francisco, with an independently elected mayor, does not have a county manager position.

The county manager:

Prepares the annual budget for the Board’s consideration.

Coordinates the activities of county departments.

Provides analyses and recommendations to the Board.

May hire and fire department heads, if authorized to do so.

May represent the Board in labor negotiations.

Key Facts About County Revenues and Spending

County Budgets Reflect State and Federal Policy Priorities and Local Policy Choices

To a large degree, county budgets reflect state and federal policy and funding priorities.

As agents of the state, counties provide an array of services that are supported with state and federal dollars and governed by state and federal rules.

This means that a large share of any county budget will reflect priorities that are set in Sacramento and in Washington, DC.

County budgets also reflect the policy and funding priorities of local residents and policymakers.

Counties can use a portion of their locally generated revenues to fund key local services and improvements.

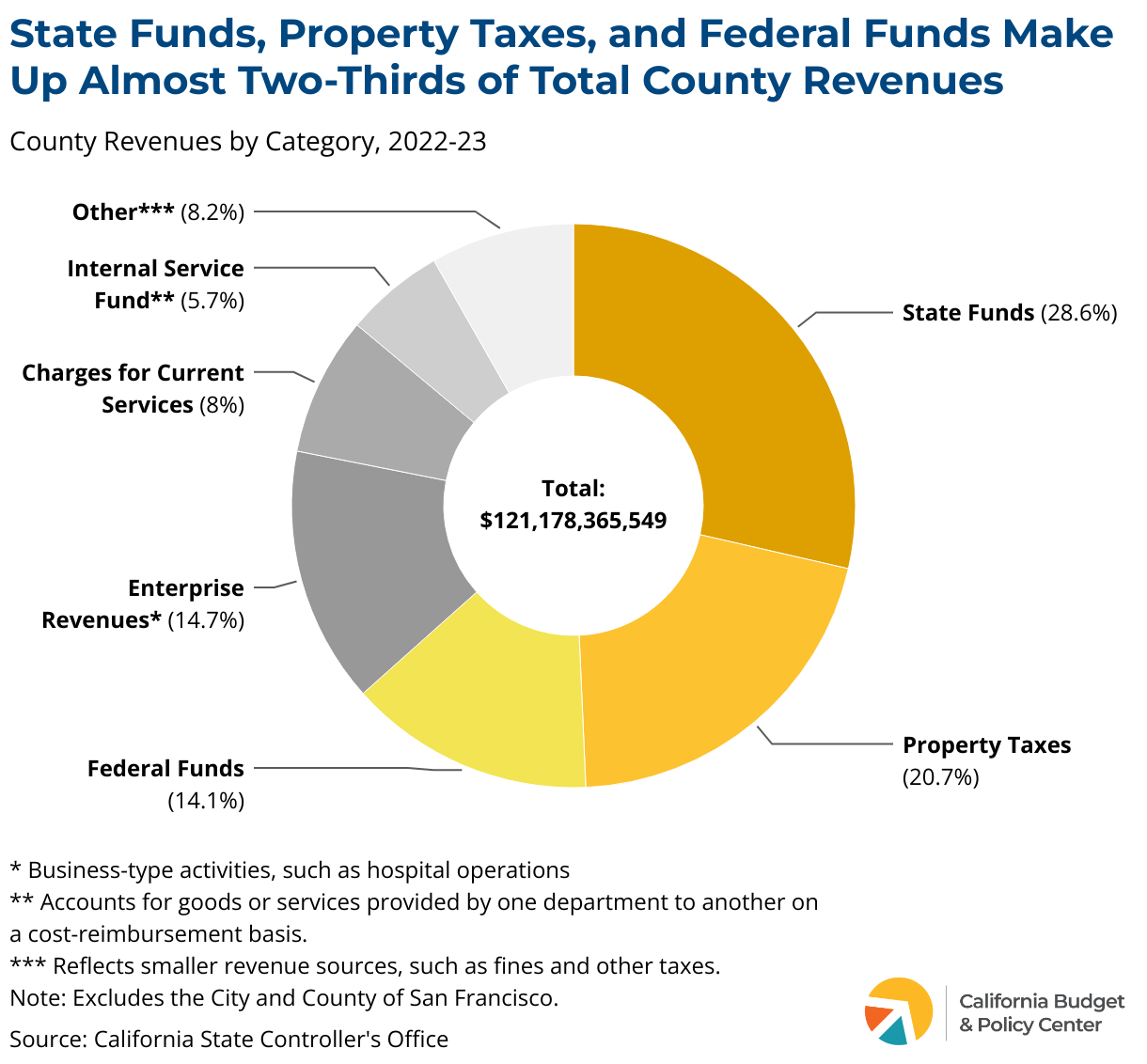

County Revenues = State Funds + Federal Funds + Local Funds

County revenues consist of state and federal dollars along with locally generated funds.

State and federal revenues pay for health and human services, roads, transit, and other services.

Local revenues, particularly property tax dollars, are important because they are mostly “discretionary” and can be spent on various local priorities.

In 2022-23, almost two-thirds of county revenues statewide came from the state government, the federal government, and local property taxes.

County Budgets Support a Broad Range of Public Services and Systems

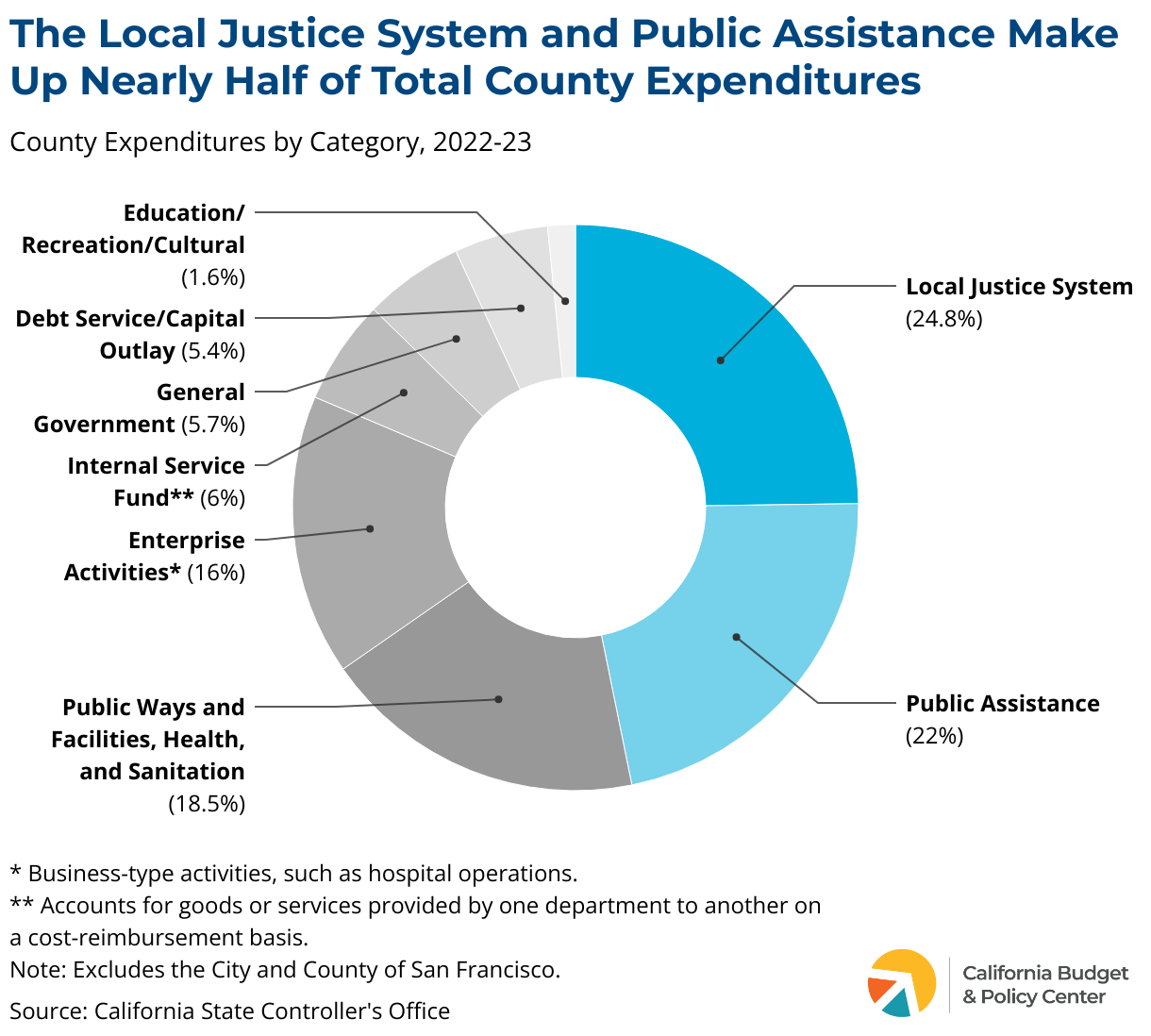

In 2022-23, nearly half of all county spending across the state funded the local justice system or public assistance.

The local justice system includes the district attorney, adult and youth detention, policing provided by the sheriff’s department, and probation.

Public assistance includes spending on cash aid for Californians with low incomes, including families with children in the CalWORKs welfare-to-work program.

Large shares of county spending in 2022-23 also supported either 1) public ways and facilities, health, and sanitation (18.5%) or 2) enterprise activities (16%), which include airports, hospitals, and golf courses.

The State Rules That Determine Counties' Revenue-Raising Authority

State Rules Establish Counties' Authority to Raise Revenue

Counties can levy a number of taxes and other charges to fund public services and systems.

The rules that allow counties to create, increase, or extend various charges are found in state law — as determined by the Legislature — as well as in the state Constitution.

Statewide ballot measures approved by voters since the late 1970s have constrained counties’ ability to raise revenues.

These measures are Proposition 13 (1978), Prop. 62 (1986), Prop. 218 (1996), and Prop. 26 (2010).

Counties Can Increase the Property Tax Rate Solely to Pay for Voter-Approved Debt

Prop. 13 (1978) limits the countywide property tax rate to 1% of a property’s assessed value.

Each county collects revenues raised by this 1% rate and allocates them to the county government, cities, and other local jurisdictions based on complex formulas.

Revenues from the 1% rate may be used for any purpose.

Local jurisdictions may increase the 1% rate to pay for voter-approved debt, but not to increase revenues for services or general operating expenses.

Most voter-approved debt rates are used to repay bonds issued for local infrastructure projects.

At the county level, bonds must be approved by a two-thirds vote of both the Board of Supervisors and the voters.

Counties Can Raise Other Taxes, But Only With Voter Approval

In contrast to counties’ limited authority over property taxes, counties may levy a broad range of other taxes to support local services. These include taxes on:

Retail sales.

Short-term lodgings.

Businesses.

Property transfers.

Parcels of property.

However, county proposals to increase taxes generally must be approved by local voters. These voter-approval requirements vary depending on whether the proposal is a “general” tax or a “special” tax.

Must be placed on the local ballot and approved by a simple majority of voters.

Special taxes

Include both parcel taxes and taxes dedicated to specific purposes.

Must be placed on the local ballot and approved by at least two-thirds of voters.

Counties Also Can Levy Charges That Are Not Defined as "Taxes"

In addition to taxes, counties can establish, increase, or extend other charges to support local services. These are:

Charges for services or benefits that are granted exclusively to the payer, provided that such charges do not exceed the county’s reasonable costs.

Charges to offset reasonable regulatory costs.

Charges for the use of government property.

Charges related to property development.

Certain property assessments and property-related fees.

Fines and penalties

The state Constitution, as amended by Prop. 26 (2010), specifically excludes these charges from the definition of a “tax.”

Charges that are not defined as “taxes” can be created, increased, or extended by a simple majority vote of the Board of Supervisors. A countywide vote is not required.

However, Prop. 218 (1996) does require the Board of Supervisors to consult property owners regarding two types of charges.

Property assessments, which pay for specific services or improvements, must be approved by at least half of the ballots cast by affected property owners, with ballots weighted according to each owner’s assessment liability.

Property-related fees — except for water, sewer, and garbage pick-up fees — must be approved by 1) a majority of affected property owners or 2) at least two-thirds of all voters who live in the area.

The County Budget Process: State Rules and Local Practices

State Law Shapes the County Budget Process

Counties develop and adopt their annual budgets according to rules outlined in state law.

Rules pertaining specifically to county budgets are found in the County Budget Act (Government Code, Sections 29000 to 29144).

The Ralph M. Brown Act (Government Code, Sections 54950 to 54963) includes additional rules that county officials must follow when discussing official county business.

State law delineates:

The process by which county budgets must be developed and shared with the public and the information that must be included in these budgets.

Local Practices Also Shape the County Budget Process

Counties have some discretion in how they craft their annual spending plans.

For example, the Board of Supervisors may hold more public hearings than state law requires and/or convene informal public budget workshops. Some counties also begin developing their budgets earlier than others do.

Counties have some leeway in how they structure their budgets and share them with the public.

County budgets may include more information and provide a higher level of detail than the state requires.

Counties may make their spending plans and other budget-related materials widely accessible to the public in multiple formats, including online.

Three Versions of Annual County Budget

At all stages, the county budget must be balanced (funding sources must equal financing uses).

The Recommended Budget is the county manager's proposed spending for the next fiscal year, as submitted to the Board of Supervisors.

The Adopted Budget is the budget as formally adopted by the Board by October 2 or — at county option — by June 30.

The Final Budget is the adopted budget adjusted to reflect all revisions made by the Board during the fiscal year.

Counties Must Adopt Their Budgets Using One of Two Models

State law provides two models for adopting the annual county budget.

One model — called the “two-step” model in this guide — requires the Board of Supervisors to first approve an interim budget by June 30 and then formally adopt the budget by October 2.

The other model — called the “one-step”model in this guide — allows the Board to formally adopt the budget by June 30 of each year, with no need to first approve an interim budget. This alternative process was created by Senate Bill 1315 (Bates, Chapter 56, Statutes of 2016).

Each county decides which model to follow in adopting its annual budget.

Two-Step Model (Step 1): Board Approves the Recommended Budget By June 30

The Board of Supervisors must approve — on an interim basis — the Recommended Budget, including any revisions that it deems necessary, on or before June 30.

The Board must consider the Recommended Budget, as proposed by the county manager, during a duly noticed public hearing.

The Recommended Budget must be made available for public review prior to the public hearing.

At this stage, the Recommended Budget is essentially a preliminary spending plan, which authorizes budget allocations for the new fiscal year (beginning on July 1) until the Board formally adopts the budget.

Two-Step Model (Step 2): Board Adopts the County Budget by October 2

The Board of Supervisors must formally adopt the county budget on or before October 2.

On or before September 8, the Board must publish a notice stating 1) that the Recommended Budget is available for public review and 2) when a public hearing will be held to consider it. At this stage, the budget reflects the preliminary version approved by the Board along with any changes proposed by the county manager.

The public hearing must begin at least 10 days after the Recommended Budget is made available to the public.

The Board must adopt a balanced budget, including any additional revisions that it deems advisable after the public hearing has concluded, but no later than October 2.

One-Step Model: Board Adopts the County Budget by June 30

The Board of Supervisors must formally adopt the county budget on or before June 30, with no need to initially approve the Recommended Budget on a preliminary basis.

On or before May 30, the Board must publish a notice stating that 1) the Recommended Budget (as proposed by the county manager) is available for public review and 2) when a public hearing will be held to consider it.

The public hearing must begin at least 10 days after the Recommended Budget is formally released to the public, but no later than June 20.

The Board must adopt a balanced budget, including any revisions that it deems advisable, after the public hearing has concluded, but no later than June 30.

County Budget Actions Require a Simple Majority Vote or a Supermajority Vote

State law allows the Board of Supervisors to make certain budget decisions by majority vote.

These include approving the Recommended Budget and/or the Adopted Budget as well as eliminating or reducing appropriations.

However, a four-fifths supermajority vote of the Board is required for a number of budget actions, including to:

Appropriate unanticipated revenues.

Appropriate revenues to address an emergency.

Transfer revenues between funds or from a contingency fund after the budget has been formally adopted.

Increase the general reserve at any point during the fiscal year.

The Timeline of the County Budget Process

The County Budget Process is Cyclical and Interacts With the State Budget Process

County budgets are developed, revised, and monitored throughout the year.

Because counties perform functions required by the state and receive significant state funding, county budgets are shaped by state budget choices.

County officials must take into account decisions made as part of the state’s annual budget process. Federal policy and funding decisions also affect county budgets.

The budget process varies somewhat across counties.

For example, counties can hold more public hearings than required, and some counties start developing their budgets earlier than others do.

Appendix

How to Find Your County's Budget

Counties generally make their budget documents available on the internet.

Online budget materials are typically located in a “budget and finance” section of the county’s website or the county manager’s webpage.

Perhaps the fastest way to find a county’s budget is by using an internet search engine and entering a phrase like “Kern County budget.”

In addition, counties make their budget documents available in county buildings and local libraries.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

California’s Budget Reserves

California’s Constitution and state law govern when funds may be withdrawn from the state’s budget reserves, the amount that can be withdrawn, and how funds may be used.

Established in the state Constitution: Budget Stabilization Account, Public School System Stabilization Account

Established in state law: Safety Net Reserve, Special Fund for Economic Uncertainties, Projected Surplus Temporary Holding Account

Budget Stabilization Account (BSA) (aka Rainy Day Fund)

Public School System Stabilization Account (PSSSA)

Safety Net Reserve

Special Fund for Economic Uncertainties (SFEU)

Projected Surplus Temporary Holding Account

Is the state required to make an annual deposit?

Yes

No However, a deposit is required under a restricted set of circumstances.1For example, these circumstances include requirements that deposits only occur when capital gains tax revenues exceed a specific level of total General Fund proceeds of taxes and when growth in the state’s minimum funding guarantee for K-12 schools and community colleges is relatively strong.

No

No

No

Can a required deposit be reduced or suspended — and by who?

Yes A required deposit can be reduced or suspended if the governor declares a budget emergency and the Legislature approves the reduction or suspension by a majority vote.

Yes A required deposit can be reduced or suspended if the governor declares a budget emergency and the Legislature approves the reduction or suspension by a majority vote.

Not applicable

Not applicable

Not applicable

When can funds be withdrawn?

Funds may be withdrawn if the governor declares a budget emergency and the Legislature passes a bill, by majority vote, to withdraw funds.2These withdrawal rules apply to funds that are deposited into the BSA as required by Proposition 2 of 2014. State policymakers may also deposit funds into the BSA on top of Prop. 2 requirements, creating a “discretionary” balance within the reserve. The Legislative Analyst’s Office suggests that the Legislature can withdraw a discretionary balance at any time without a declaration of a budget emergency by the governor. Separate from this issue, funds must be withdrawn from the BSA — without the need for a declaration of a budget emergency — when updated revenue estimates indicate that a prior-year deposit was greater than required.

Funds may be withdrawn if the governor declares a budget emergency and the Legislature passes a bill, by majority vote, to withdraw funds.3Funds must be withdrawn from the PSSSA — without the need for a declaration of a budget emergency — when the state’s minimum funding guarantee for K-12 schools and community colleges is less than the prior year’s funding level, adjusted for changes in student attendance and the cost of living, or when updated revenue estimates indicate that a prior-year deposit was greater than required.

The Legislature may withdraw the funds at any time by majority vote.

The Legislature may withdraw the funds at any time by majority vote.4Additionally, the Department of Finance may withdraw funds from the SFEU without legislative approval to cover the cost of state disaster response efforts upon an emergency proclamation by the governor.

The Legislature may withdraw the funds by majority vote at any time up to one year after they are deposited. After one year, any unappropriated funds must be transferred back to the General Fund.

Is there a limit on the amount of funds that can be withdrawn?

Yes The amount that can be withdrawn is limited to the lower of 1) the amount needed to address the budget emergency or 2) half of the funds in the BSA, unless funds had been withdrawn in the previous fiscal year, in which case all of the funds remaining in the BSA may be withdrawn.

No5However, in any year when funds must be withdrawn from the PSSSA because the state’s minimum funding guarantee for K-12 schools and community colleges is less than the prior year’s funding level — adjusted for changes in student attendance and the cost of living — the required withdrawal is limited to the amount of that shortfall.

No

No

No

How can the funds be used by the state?

Funds may be used for any purpose.

Funds must be used to support K-12 schools and community colleges.

Funds are intended to maintain existing CalWORKs and Medi-Cal benefits and services during an economic downturn, but may be used for any purpose if the Legislature so chooses.

Funds may be used for any purpose.

Funds may be used for any purpose.

Note: A ”budget emergency” that’s declared by the governor is defined as either: 1) the existence of ”conditions of disaster or of extreme peril to the safety of persons and property within the State, or parts thereof” as defined in Article XIII B, Section 3(c)(2) of the state Constitution; or 2) a determination by the governor that there are insufficient resources to maintain General Fund expenditures at the highest level of spending in the three most recent fiscal years, adjusted for state population growth and the change in the cost of living. Article XIII B, Section 3(c)(2), defines “conditions of disaster or of extreme peril” as being “caused by such conditions as attack or probable or imminent attack by an enemy of the United States, fire, flood, drought, storm, civil disorder, earthquake, or volcanic eruption.”

Sources: California Constitution, California Government Code, and California Welfare and Institutions Code

For example, these circumstances include requirements that deposits only occur when capital gains tax revenues exceed a specific level of total General Fund proceeds of taxes and when growth in the state’s minimum funding guarantee for K-12 schools and community colleges is relatively strong.

2

These withdrawal rules apply to funds that are deposited into the BSA as required by Proposition 2 of 2014. State policymakers may also deposit funds into the BSA on top of Prop. 2 requirements, creating a “discretionary” balance within the reserve. The Legislative Analyst’s Office suggests that the Legislature can withdraw a discretionary balance at any time without a declaration of a budget emergency by the governor. Separate from this issue, funds must be withdrawn from the BSA — without the need for a declaration of a budget emergency — when updated revenue estimates indicate that a prior-year deposit was greater than required.

3

Funds must be withdrawn from the PSSSA — without the need for a declaration of a budget emergency — when the state’s minimum funding guarantee for K-12 schools and community colleges is less than the prior year’s funding level, adjusted for changes in student attendance and the cost of living, or when updated revenue estimates indicate that a prior-year deposit was greater than required.

4

Additionally, the Department of Finance may withdraw funds from the SFEU without legislative approval to cover the cost of state disaster response efforts upon an emergency proclamation by the governor.

5

However, in any year when funds must be withdrawn from the PSSSA because the state’s minimum funding guarantee for K-12 schools and community colleges is less than the prior year’s funding level — adjusted for changes in student attendance and the cost of living — the required withdrawal is limited to the amount of that shortfall.

You may also be interested in the following resources:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

The California budget process moves quickly after the governor releases the “May Revision” in mid-May. This revised budget proposal opens a crucial window for public engagement, but the tight timeline can make advocating for your priorities challenging.

Here’s a breakdown of the key stages:

May Revision: The governor releases an updated budget proposal on or before May 14. This is your chance to weigh in with, and express, your budget priorities to policymakers.

Budget Negotiations: Policymakers engage in intense negotiations to reconcile the governor’s budget plan with legislative priorities throughout May and June.

Legislative Budget Plan: Roughly 10 to 14 days after the May Revision (timing depends on when the revised budget is released), the Assembly and Senate release their own budget plans. Roughly 2 to 3 weeks after the May Revision, legislative leaders agree on a unified legislative budget plan. This plan forms the basis for the Budget Act. A deal with the governor at this stage is possible but not very likely.

Constitutional Deadline: The Legislature passes the Budget Act by June 15 — the constitutional deadline — and sends it to the governor, even as negotiations continue between legislative leaders and the governor on the full budget package.

Budget Deal Announcement: The “Big 3” — the governor, Assembly Speaker, and Senate President pro Tempore — typically announce a final budget deal by late June.

Budget Package Approval: In late June, all budget-related legislation (including trailer bills) is unveiled, voted on by both houses of the Legislature, and signed by the governor, potentially with line-item vetoes.

The June package isn’t the end of the story. In August, state leaders often revisit the budget, potentially adding to the size and scope of the original budget package enacted earlier in the summer.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

The California budget process moves quickly after the governor releases the “May Revision” in mid-May. This revised budget proposal opens a crucial window for public engagement, but the tight timeline can make advocating for your priorities challenging. Here’s a breakdown of the key stages: The June package isn’t the end of the story. In August, … Continued

This website uses cookies to analyze site traffic and to allow users to complete forms on the site. The California Budget & Policy Center does not share, trade, sell, or otherwise disclose personal information. By using our website you agree to our Privacy Policy.

California Budget & Policy Center

Secure Your Early Bird Ticket!

Join us in Sacramento on April 22, 2026 for engaging sessions, workshops, and networking opportunities with fellow changemakers, inspiring speakers, and much more.