The California Legislature conducts most of its business during regular two-year sessions that begin in early December of even-numbered years. For example, the 2025-26 regular session started on December 2, 2024, and will end on November 30, 2026. These two-year sessions are formally known as “biennial sessions.”

From time to time, the governor convenes an extra — or special — session of the Legislature to address extraordinary situations. This Q&A answers key questions about special sessions, including how they work, how many have been convened, and how members of the public can follow the action.

What is a special session in California?

California governors have the authority to “cause the Legislature to assemble” on “extraordinary occasions.” These extraordinary sessions are commonly known as special sessions. To convene a special session, governors issue a proclamation, such as this one issued by Governor Newsom in 2024.

Why do governors call special sessions?

Governors periodically call special sessions to draw attention to issues that they view as urgent and encourage legislators to advance policy solutions to address those issues.

Over the years, governors have called special sessions to address a number of topics, including state budget deficits, spikes in gasoline prices, natural disasters, and workers’ compensation reform.

When can the governor call a special session?

The governor may call a special session at any point. This includes when the Legislature is already meeting as well as when legislators are on “recess” — such as during the autumn break between the first and second years of the regular two-year session.

What topics may be addressed during a special session?

The Legislature may only address the topics specified in the governor’s proclamation convening the special session. In other words, the Legislature must limit its actions to the purpose outlined by the governor. However, legislators may pay for expenses and address “other incidental matters” related to the special session.

Can governors revise the topics to be addressed in a special session after the special session has started?

Yes. Governors may amend the proclamation calling the special session, even after the special session has begun. This practice “has never been challenged” and is an accepted part of the legislative process.

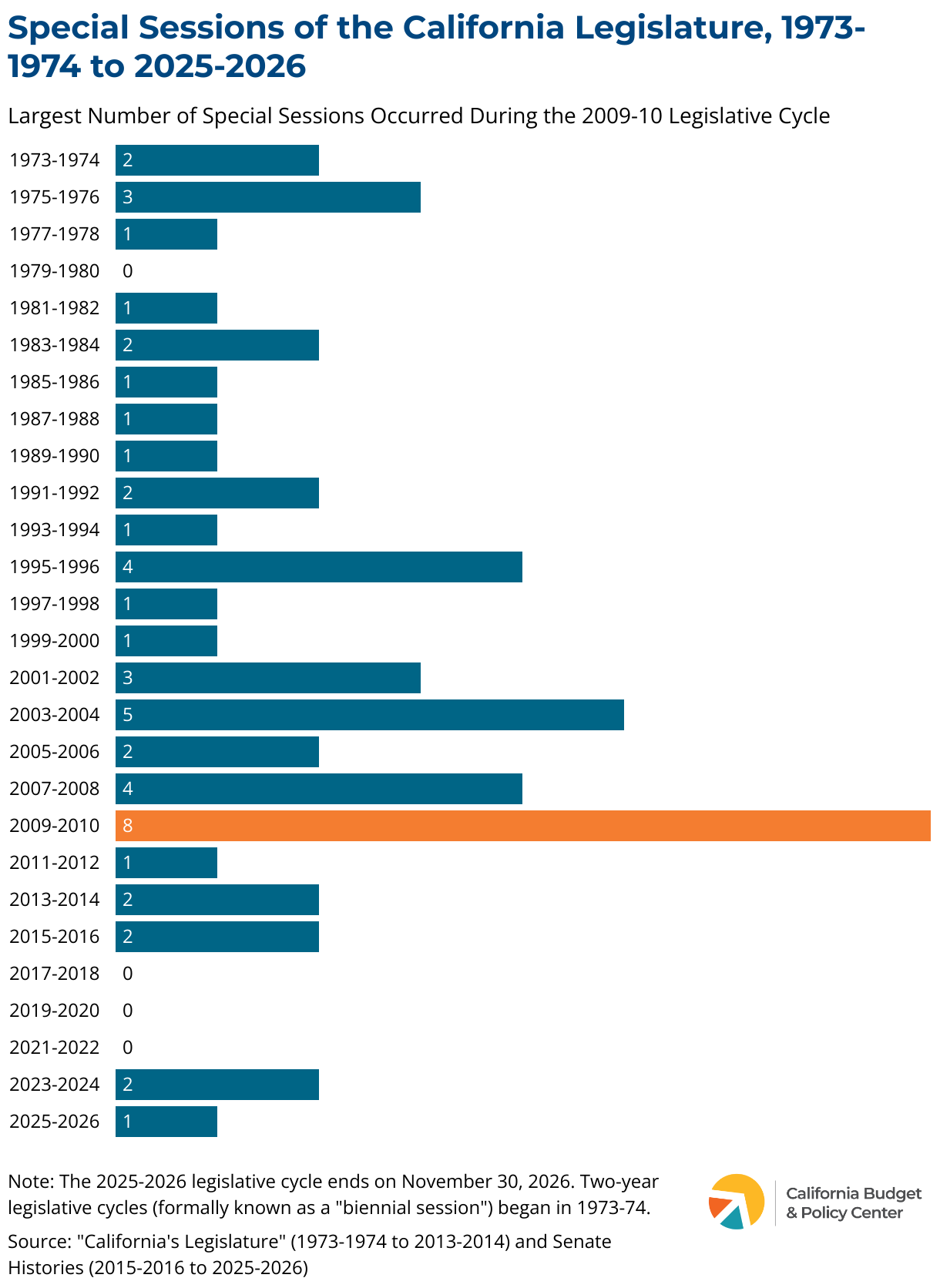

Can there be more than one special session during each two-year legislative cycle?

Yes. There have been multiple special sessions during half of the last 26 legislative cycles. For example, during the 2009-10 biennial session, Governor Arnold Schwarzenegger called eight special sessions as state leaders addressed the state budget impacts of the Great Recession. In contrast, Governor Newsom convened only two special sessions during the 2023-24 legislative cycle.

Can two or more special sessions run concurrently?

Is the Legislature required to consider or pass legislation in a special session?

No. As an independent branch of state government, the Legislature does not have to take up or pass any legislation during a special session.

How are special session bills identified?

Special session bills include an “X” to indicate that the legislation was introduced during an extraordinary (special) session. For example, during the first special session of a legislative cycle, the initial bill introduced in the Assembly may be identified as “ABX1 1,” with the “X1” in the middle denoting the First Extraordinary Session and the “1” at the end indicating the bill number. Similarly, the initial Assembly bill introduced during the Second Extraordinary Session may be identified as “ABX2 1,” etc.

Sometimes a simpler notation is used, with an “x” still denoting a special session — for example, “SB 1x” (Senate Bill 1 of the First Extraordinary Session), SB 1xx (Senate Bill 1 of the Second Extraordinary Session), etc.

When does legislation passed during a special session take effect?

However, certain bills — whether passed in a special session or the regular two-year session — always take effect as soon as the governor signs them. These are bills that:

Contain an urgency clause stating the bill takes effect immediately.

Provide for tax levies, which either increase or reduce state taxes.

Provide appropriations for the “usual current expenses” of the state.

Call an election.

Does the 72-hour bill-in-print rule apply to special session bills?

Yes. Any bill, including a bill introduced during a special session, must be distributed to legislators and published on the Internet, in its final form, at least 72 hours before being passed by the Legislature.

How long does the governor have to act on a special session bill passed by the Legislature?

The governor has 12 days to sign or veto a special session bill after the Legislature presents it. (The same rule generally applies to bills passed during the regular two-year session.) The bill automatically becomes law if the governor does not act on it within the required period.

If the governor vetoes a bill after the Legislature adjourns the special session, the bill and the veto message are returned to the Secretary of State instead of the house where the bill was introduced.

How can the public watch special session proceedings?

The Legislature may convene committee hearings during a special session and may also debate/vote on legislation on the floor of each house. As with regular sessions, the public can attend these proceedings in person or watch them online through the Assembly and Senate websites.

When does a special session end?

Although governors start special sessions, they do not have the power to end them. Only the Legislature has that authority. Specifically, a special session ends when the Assembly and Senate adopt a concurrent resolution to adjourn it. (This resolution is separate from any legislation that may have been passed as part of the special session.)

Otherwise, if legislators have not adjourned a special session, it automatically ends at midnight on November 30 of the even-numbered year when the regular two-year session ends.

Every year, California’s 58 counties — under state oversight — deliver essential public services that support Californians’ well-being, keep communities healthy and safe, and protect vulnerable populations, including children, older adults, and people with disabilities. These programs are funded with a broad range of revenues, including federal dollars, local county taxes, and funding provided by the state.

Counties’ responsibility for these services grew substantially beginning in the 1990s. The state restructured — or “realigned” — the state-county relationship in 1991 and again in 2011 by increasing counties’ fiscal and programmatic obligations for a number of services, while also providing counties with dedicated, ongoing revenues to help support their new costs.

These state-to-county “realignments” encompass vital programs that:

aim to protect vulnerable children and adults,

address health inequities,

support people facing mental health and/or substance use challenges,

keep people from cycling through carceral systems, and

improve Californians’ quality of life, particularly residents with low incomes.

Yet, while counties receive billions of dollars each year to deliver these critical public services, the concept of realignment is not well understood. Moreover, the framework and funding structures that underpin realignment are complex and can be challenging to grasp.

This report cuts through the complexity by explaining what realignment is, how it is structured, and key ways in which it has changed over time. This report does not describe every detail of these complex funding structures. It also does not evaluate realignment or assess how realigned services have been implemented. Instead, it provides a high-level overview that explains the basics, outlines the 1991 and 2011 realignment frameworks, and describes how realignment has evolved in recent decades.

Part 1: Realignment — The Basics

What Is Realignment?

California’s state government and the state’s 58 counties have long shared responsibility for financing and delivering a broad array of services, including public health, mental health care, and support for families with children with low incomes.

However, state and county roles are not static. Instead, they vary across programs and have shifted over time as state policymakers have redefined the state-county relationship. These periodic shifts in responsibility between the state and counties for the financing and implementation of public services are known as “realignment.”

Types of Realignment

The transfer of fiscal and programmatic responsibility for public services between the state and counties typically happens in one of two ways:

Realignment can modify how the state and counties share the cost of public services.

Historically, the state and counties have shared the cost of many public programs operated by counties. Often, these services are also supported with federal funding, in which case the state and counties split the nonfederal share of costs (although not usually 50/50).

Realignment can modify these state/county “cost-sharing ratios” so that one level of government pays more of the cost of a service and the other pays less. For example, counties’ share of costs for a program could be increased from 30% to 60%, with the state’s share reduced from 70% to 40%.

Realignment can transfer the full cost of a program to one level of government or the other.

Historically, the most common transfer scenario has been for state policymakers to eliminate General Fund support for a program that counties already operate and shift 100% of the cost of the program to counties.

The state may also require counties to take on new responsibility for a program or function that is operated at the state level, shifting 100% of the cost from the state General Fund to counties.

However, the most far-reaching realignments were adopted in 1991 and 2011 when counties took on additional responsibility for a broad range of services. These realignments — 20 years apart — expanded counties’ fiscal and programmatic responsibilities in several policy areas.

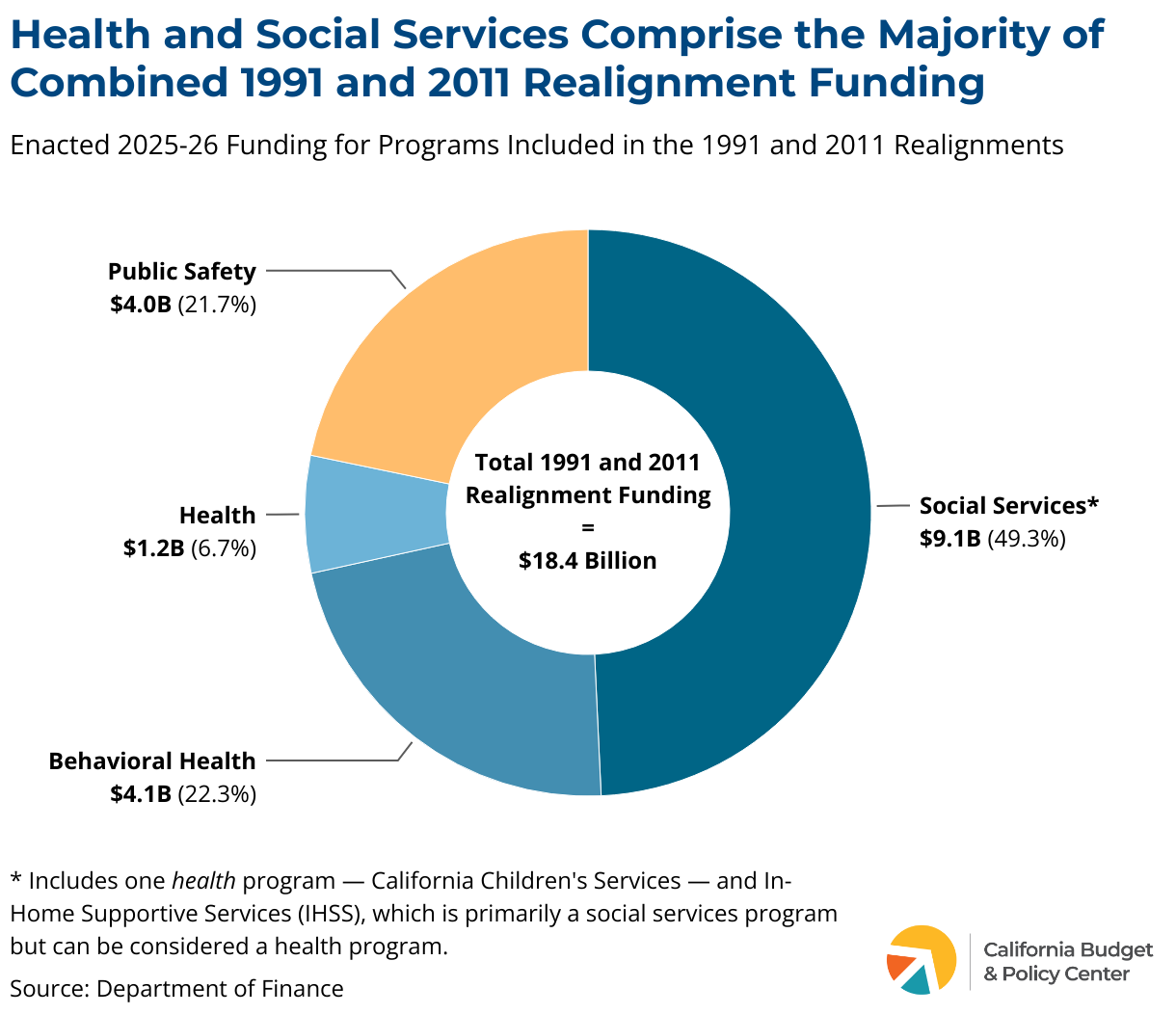

The 1991 and 2011 realignments encompass the following policy areas:

Social services for children, families, older adults, and people with disabilities

These include Child Welfare Services, Adult Protective Services, In-Home Supportive Services, and more.

Behavioral health services

These include community-based mental health services, substance use disorder treatment services, and more. Applying a different lens, these services include both 1) Medi-Cal specialty mental health and substance use disorder treatment services and 2) non-Medi-Cal services.

Health services

These include public health as well as health care for adults with low incomes who otherwise lack access to health coverage (this is known as indigent health care).

Public safety functions

These include — but are not limited to — trial court security, youth justice, and counties’ new role (as of 2011) in “community corrections” — managing, supervising, and rehabilitating adults convicted of certain low-level offenses.

See Part 2 and Part 3 for key facts about the 1991 and 2011 realignments, respectively, and the Appendix for a description of the programs included in each realignment.

Rationale for Realignment

The goals of realignment typically fall into three categories:

Realignment can help to address state budget deficits.

For example, Governor Pete Wilson and Governor Jerry Brown proposed major state-to-county realignments — in 1991 and 2011, respectively — in response to multibillion dollar state budget deficits.

Realigning responsibilities to the counties helped to address these shortfalls by shifting costs from the General Fund to the newly created realignment revenues that flowed directly to counties.

Realignment can help to improve funding stability.

Providing dedicated revenues to support realigned programs helps to insulate these programs from reductions when the state faces a budget shortfall.

For example, the health and mental health services included in the 1991 realignment were previously funded with state General Fund dollars. Due to state budget shortfalls, these programs were cut in previous budgets, according to the Department of Finance. Moreover, these health and mental health services “would have been subject to additional major reductions” in 1991 to help close the budget deficit if state policymakers had not adopted realignment that year.

Realignment can — but does not always — promote greater efficiency and effectiveness in service delivery.

A primary rationale for the 2011 realignment was that transferring funding and responsibilities to local governments would “allow governments at all levels to focus on becoming more efficient and effective,” helping to ensure that services are “delivered to the public for less money.” Similar claims were made for the 1991 realignment.

Two evaluations of the 1991 realignment — in 2001 and 2018 — found some evidence of progress in terms of efficiency and effectiveness. However, these evaluations also found that counties’ flexibility over these programs and their ability to control costs had diminished substantially since 1991 due to state law changes and other factors.

Funding to Support Realigned Services

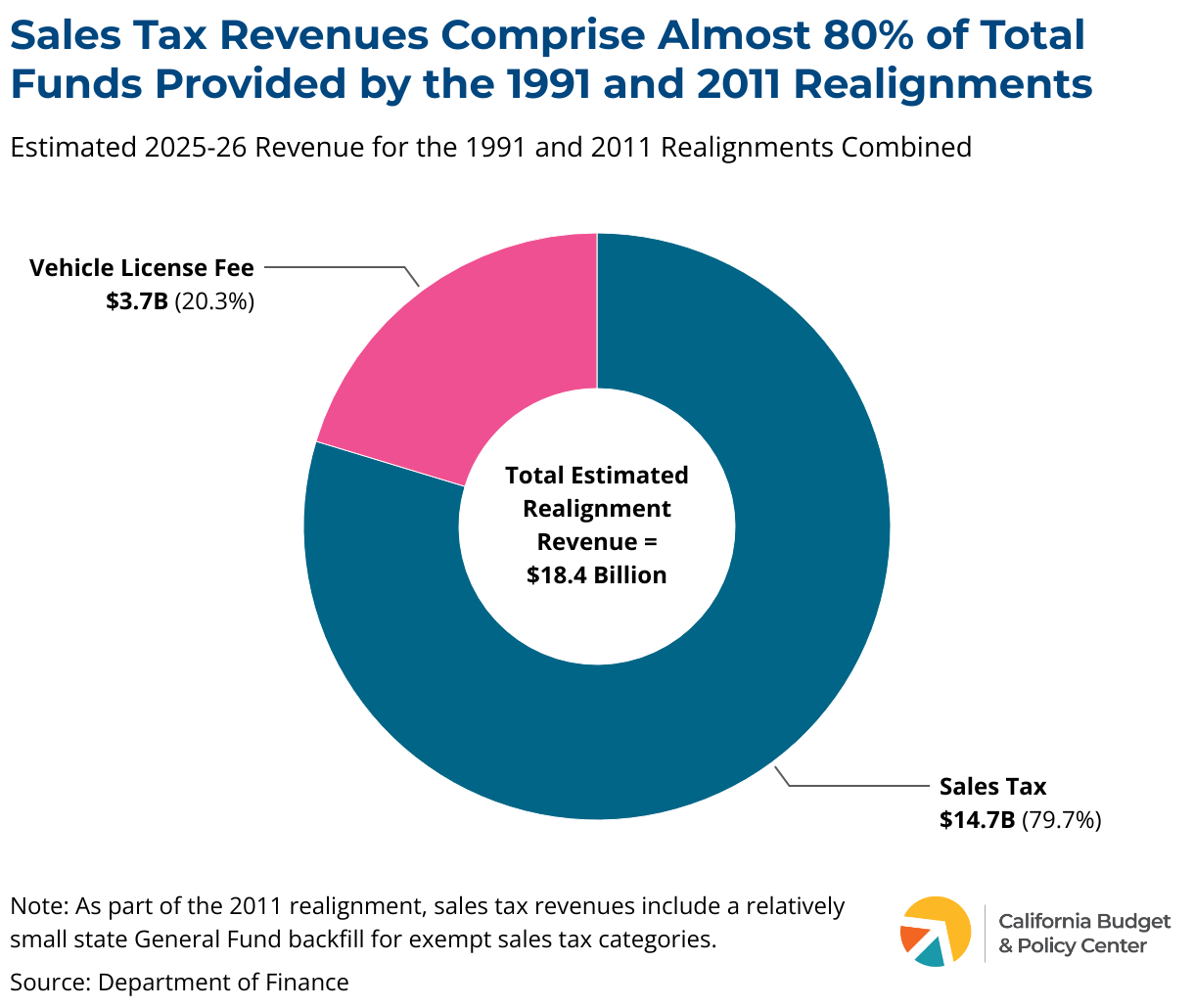

When state policymakers shift responsibilities to counties, they provide dedicated annual funding to help counties pay for their additional costs. Annual funding to support counties’ 1991 and 2011 realignment responsibilities comes from two sources — the sales tax and the Vehicle License Fee (VLF). Specifically:

To fund the 1991 realignment, state policymakers increased the state sales tax rate by one-half cent and raised the state’s VLF. Counties continue to receive these dedicated funds each year to support the programs that were realigned to them in 1991.

To fund the 2011 realignment, state policymakers redirected a portion of the state’s existing sales tax and VLF revenues to counties, without raising taxes. In other words, these dollars were carved out of existing state revenue streams. Counties continue to receive these dedicated funds each year to support the programs that were realigned to them in 2011.

What is the sales tax?

The sales tax — formally, the “sales and use tax” — is a tax on the purchase of tangible goods in California (the “sales tax”) or the use of tangible goods in California that were purchased elsewhere (the “use tax”).

Services are excluded from the sales and use tax, as are other items exempted by law, including groceries, menstrual hygiene products, and medications.

The sales and use tax is a regressive tax because households with lower incomes generally spend a larger share of their incomes on necessities than households with higher incomes, so a larger share of their income goes to sales taxes.

What is the vehicle license fee?

The VLF is an annual state fee that is based on the purchase price or value of a vehicle.

In 2011, state leaders shifted to counties part of the base 0.65% VLF rate in order to help fund counties’ increased responsibilities under the 2011 realignment.

The sales tax provides most of the revenue that counties receive to support their responsibilities under the 1991 and 2011 realignments. While sales tax revenues generally grow over time, they can decline from year to year, such as during recessions. When sales tax revenues fall, counties receive less realignment funding than they received the year before. When the economy improves, realignment revenues begin to grow again, providing counties with more resources to carry out their responsibilities.

However, under the 1991 realignment, the revenue shortfalls created during economic downturns are not filled. Even when revenues begin to grow again — providing additional funding for realigned programs — this growth comes on top of a permanently lowered funding base. This leaves counties with less revenue to carry out their 1991 realignment responsibilities over the long term. In contrast, under the 2011 realignment, counties’ funding base is restored when revenues begin to recover following a recession.

Moreover, counties are not reimbursed for their actual costs for realigned programs. Instead, counties receive dedicated revenue that is intended to cover their costs over time. However, this revenue often falls short of meeting the need for and growing cost of services, including counties’ health, public health, and behavioral health responsibilities under both realignments.

Realignment revenue comes closer to covering counties’ actual costs for social services programs, such as Child Welfare Services and In-Home Supportive Services. Under the 1991 realignment, these “entitlement” or “caseload” programs are first in line for sales tax revenue growth, with these growth revenues supporting counties’ rising costs for these services.

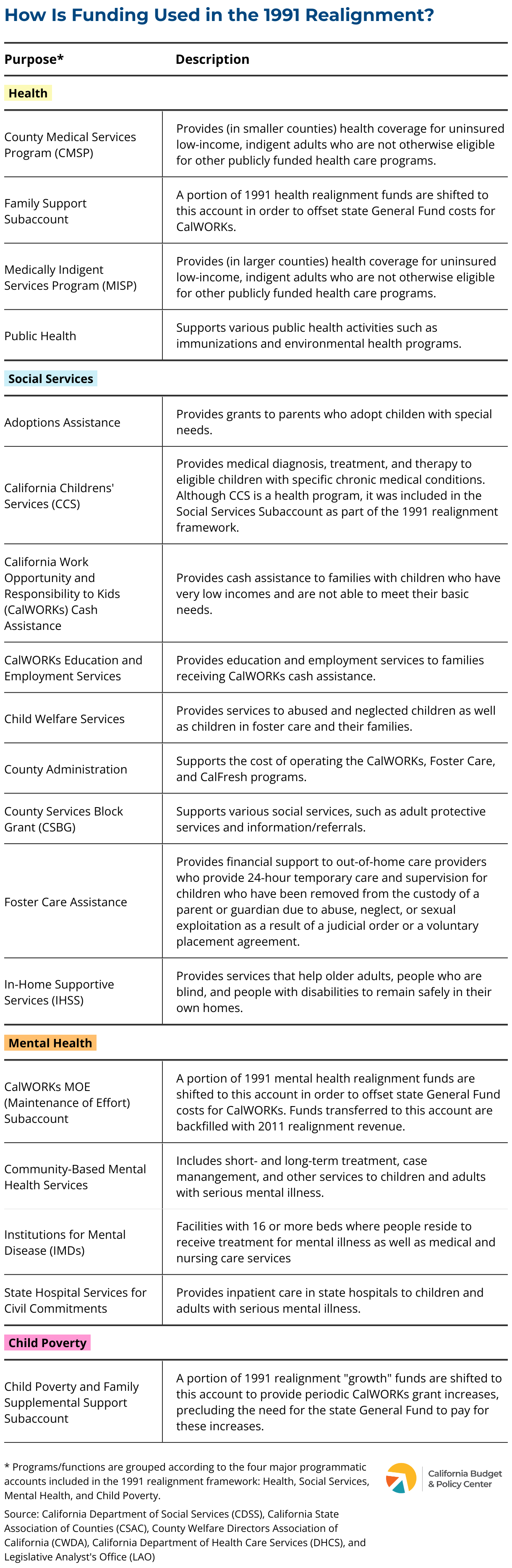

Part 2: Key Facts About the 1991 Realignment

What Did the 1991 Realignment Do?

In 1991, counties took on increased responsibility for a number of health, mental health, and social services programs. (See the Appendix for descriptions of these programs.) This “realignment” changed the state-county relationship in two major ways:

The state transferred responsibility for certain health and mental health programs to counties.

Specifically, counties took full responsibility for key health and mental health programs and also absorbed larger costs as the state eliminated General Fund support for those programs (although the state still maintained an oversight role).

The transferred services included community-based mental health, public health, and health care provided to uninsured adults with low incomes (commonly known as indigent health care).

The state generally increased counties’ share of the nonfederal costs for multiple social services programs as well as for one health program.

Prior to realignment, the state paid most or all of the nonfederal costs of major health and social services programs using General Fund dollars.

Realignment generally shifted more of these nonfederal costs to counties, which lowered the state’s share of costs, freeing up state General Fund dollars for other purposes.

Child Welfare Services and In-Home Supportive Services (IHSS) were among several social services programs for which counties’ share of cost increased under the 1991 realignment. (IHSS is generally considered a social services program but may be referred to as a health program.)

Counties also took on a larger share of the cost for California Children’s Services (CCS), a health program for children with certain diseases or health problems. (CCS was grouped with social services programs for the purpose of the 1991 realignment.)

In some cases, the state reduced counties’ share of cost — and increased the state’s share — to reflect counties’ relatively limited control over spending. The state began to pay a larger share of the cost for:

Cash assistance for low-income families with children, which was integrated into the new CalWORKs program in the mid-1990s.

County administration, which reflects counties’ operational costs for key social services programs.

How Is the 1991 Realignment Funded?

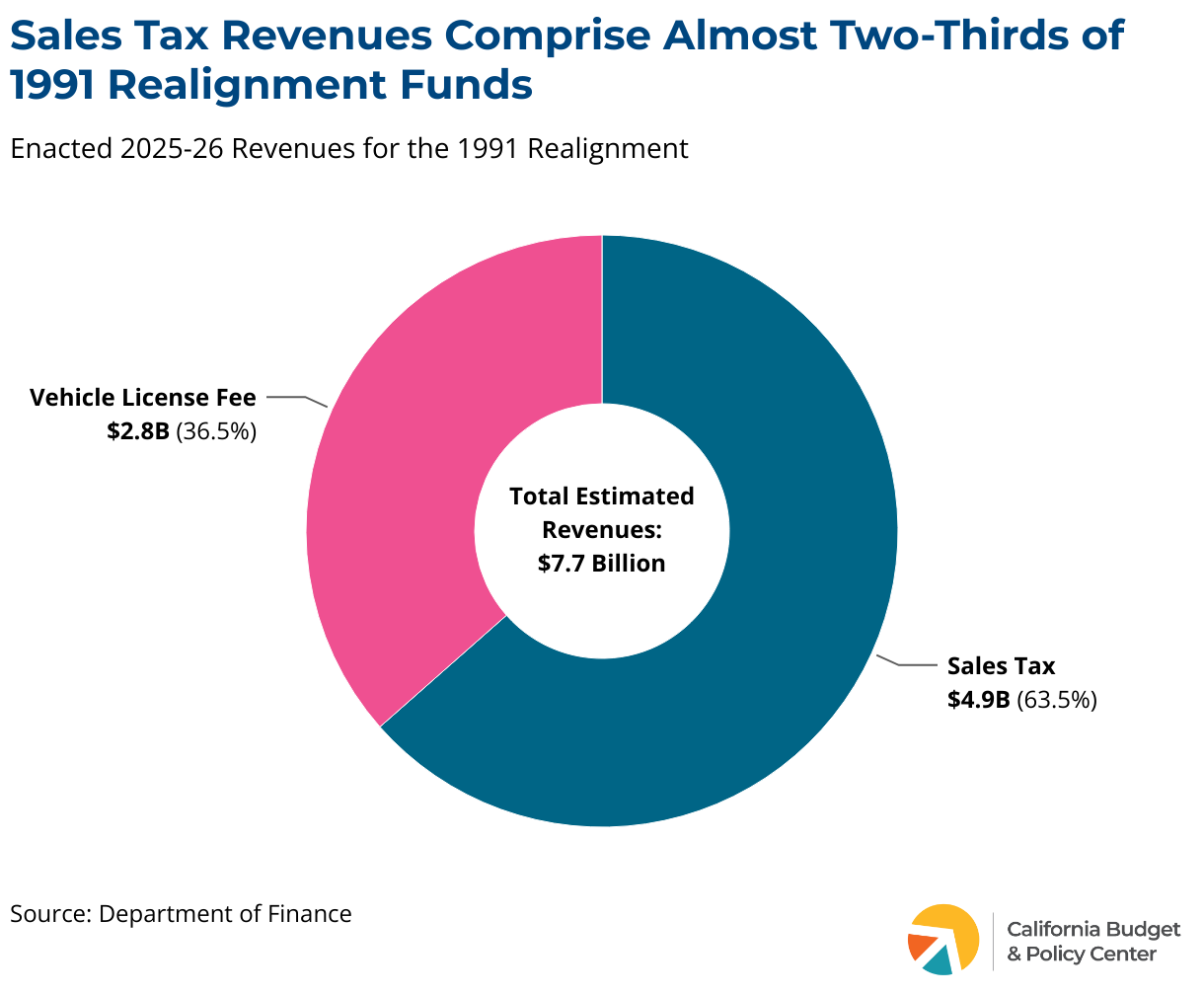

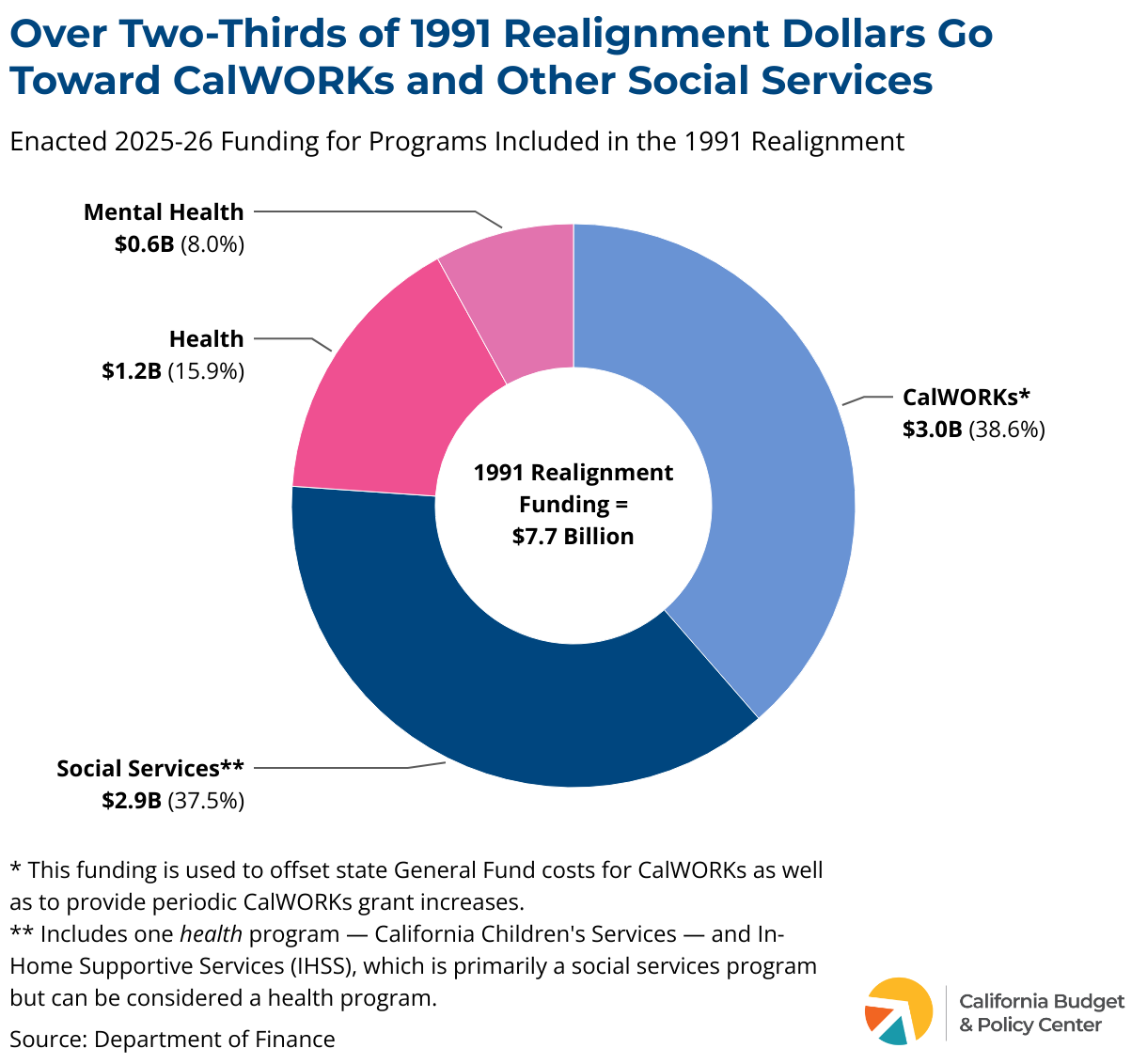

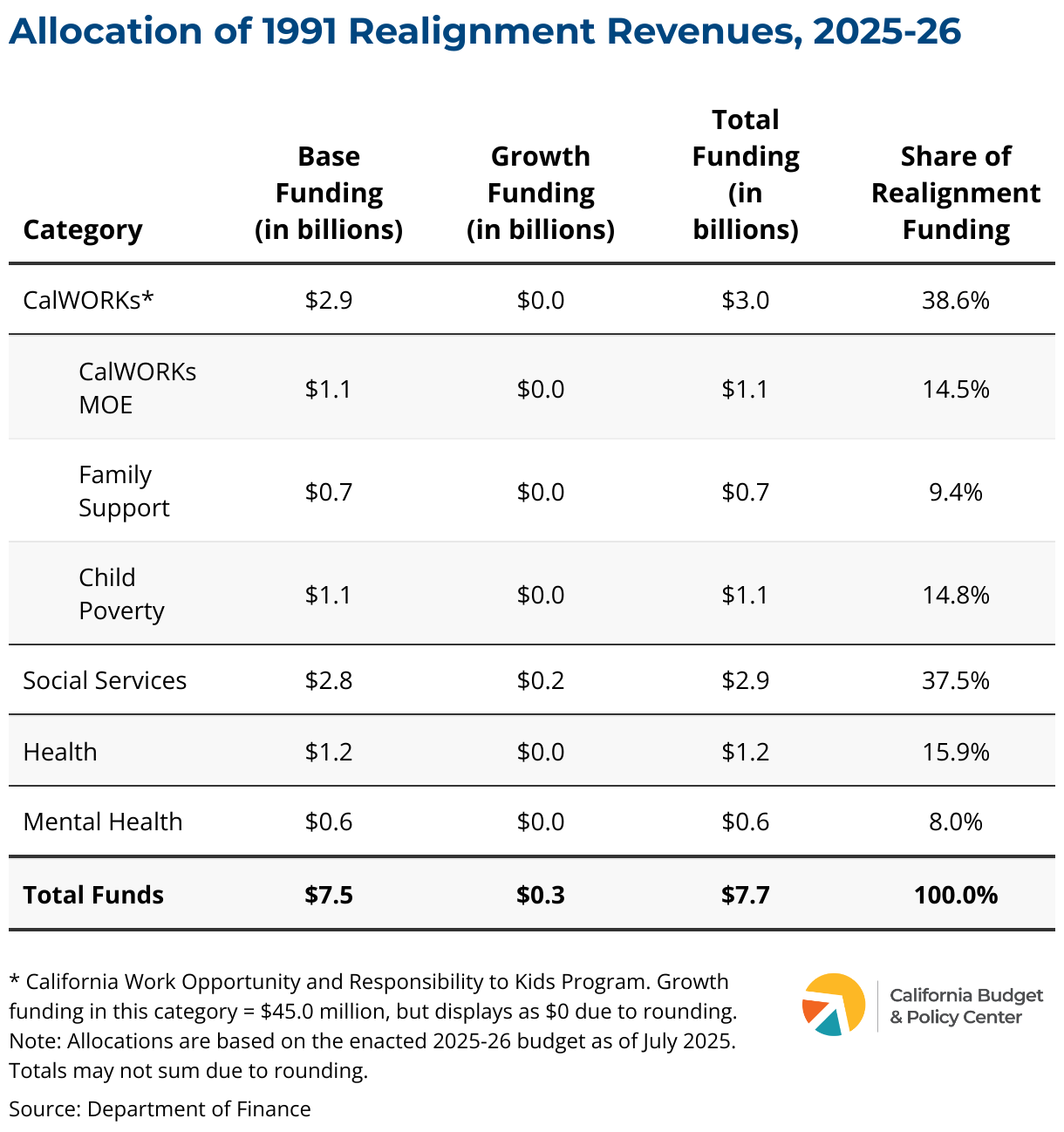

In order to support the programs included in the 1991 realignment, the state Legislature increased taxes and dedicated the revenues to the realigned programs. In 2025-26, these taxes are estimated to raise $7.7 billion. Specifically:

The Legislature raised the state sales tax rate by one-half cent and increased the state’s Vehicle License Fee (VLF), allocating all of the revenue to counties to support the realigned programs.

The half-cent sales tax rate provides almost two-thirds of annual 1991 realignment revenues, totaling an estimated $4.9 billion in 2025-26.

The VLF increase generates about one-third of annual realignment revenues, totaling an estimated $2.8 billion in 2025-26.

What is the sales tax?

The sales tax — formally, the “sales and use tax” — is a tax on the purchase of tangible goods in California (the “sales tax”) or the use of tangible goods in California that were purchased elsewhere (the “use tax”).

Services are excluded from the sales and use tax, as are other items exempted by law, including groceries, menstrual hygiene products, and medications.

The sales and use tax is a regressive tax because households with lower incomes generally spend a larger share of their incomes on necessities than households with higher incomes, so a larger share of their income goes to sales taxes.

What is the vehicle license fee?

The VLF is an annual state fee that is based on the purchase price or value of a vehicle.

In 2011, state leaders shifted to counties part of the base 0.65% VLF rate in order to help fund counties’ increased responsibilities under the 2011 realignment.

How Is the 1991 Realignment Structured?

The 1991 realignment revenues flow through a series of accounts that grew increasingly complex as the Legislature modified the original framework in the decades after the 1991 realignment took effect. (See Part 4 for details on this point.)

Revenue

Annual revenues generated by the higher sales tax rate and the VLF increase first flow into “base funding” accounts.

Realignment “base” revenue is allocated through the Sales Tax Account or the Vehicle License Fee Account, with these funds supporting the various services included in the 1991 realignment.

Realignment revenues sometimes fail to reach the base level of funding, such as when sales tax revenues decline during a recession. When this happens, counties’ funding base is reduced for a fiscal year to match the (lower) available revenues. In other words, counties receive less realignment funding than they received the year before.

Under this scenario, funding for the realigned programs increases only when realignment revenues grow again in future years. However, counties’ realignment base is permanently lowered — that is, the revenue that counties lose during tough budget years when revenues fall short is not made up in future years.

What is realignment “Base” revenue?

“Base” revenue for a fiscal year = the amount of realignment revenue allocated to counties in the prior fiscal year. In other words, the total amount of realignment revenue that counties receive in one year becomes the base level of funding for the next fiscal year.

If available, annual revenues generated by the higher sales tax rate and the VLF increase next flow into “growth funding” accounts.

Growth revenue — if available — is allocated through the Sales Tax Growth Account or the Vehicle License Fee Growth Account, with these funds supporting 1991 realignment services based on a complex set of funding priorities.

Sales tax growth revenues go first to social services programs, including but not limited to Child Welfare Services and In-Home Supportive Services. (Social services are called “caseload” programs in the 1991 realignment framework).

Any remaining sales tax growth revenues go to the health and mental health accounts as well as to support certain increases to CalWORKs grants. As discussed in Part 4, the state began using sales tax growth revenues to fund periodic CalWORKs grant increases in 2013.

Vehicle License Fee Growth Account

VLF growth revenues go first to the County Medical Services Program to support counties’ role in providing health care to low-income, uninsured adults (known as indigent health care).

Any remaining VLF growth revenues go to health and mental health programs as well as to support certain increases to CalWORKs grants. As discussed in Part 4, the state began using VLF growth revenues to fund periodic CalWORKs grant increases in 2013.

what is realignment “growth” revenue?

“Growth” revenue = the amount of realignment revenue left over (if any) after the base level of revenue for a fiscal year has been reached.

In other words, sales tax and VLF revenue that exceeds the base level of funding for a fiscal year flows to counties on top of their base allocations.

Allocations: Big Picture

Originally, revenue raised by the 1991 realignment solely supported the realigned health, mental health, and social services programs. However, in the early 2010s, state leaders redirected a portion of 1991 realignment revenue to offset some state costs for CalWORKs. To implement these shifts, state leaders added three CalWORKs-focused accounts to the 1991 realignment framework. (See Part 4 for details.)

With the addition of these new CalWORKs accounts, 1991 realignment revenue — which is estimated to total $7.7 billion in 2025-26 — is divided among four spending categories:

CalWORKs,

Social Services,

Health, and

Mental Health.

CalWORKs Allocation

Nearly 40% of realignment funding — an estimated $3.0 billion in 2025-26 — is used to achieve state savings by offsetting the state’s cost for CalWORKs.

These funds flow into three accounts created in the early 2010s: the CalWORKs MOE [Maintenance of Effort] Subaccount, the Family Support Subaccount, and the Child Poverty and Family Supplemental Support Subaccount. (See Part 4 for details.)

Using 1991 realignment dollars to offset a portion of the state’s General Fund cost for CalWORKs frees up state dollars for other purposes and reduces pressure on the state budget.

Social Services Allocation

More than one-third of realignment funding — an estimated $2.9 billion in 2025-26 — supports multiple social services programs as well as one health program.

These funds flow into the Social Services Subaccount, supporting programs like Child Welfare Services, Foster Care, and In-Home Supportive Services. (IHSS is generally considered a social services program but may be referred to as a health program.)

These revenues also support California Children’s Services (CCS), which assists children with certain diseases or health problems and is the only health program included in the Social Services Subaccount.

All of the programs in the Social Services Subaccount are known as “caseload” programs in the 1991 realignment framework.

Health Allocation

About 16% of realignment funding — an estimated $1.2 billion in 2025-26 — supports counties’ role in delivering health services.

The Health Subaccount includes funding for public health activities as well as for indigent health care (care provided to low-income, uninsured adults).

Counties’ role in indigent health care diminished substantially starting in 2014 when California adopted the Medi-Cal eligibility expansion as allowed by the Affordable Care Act. With this expansion, millions of uninsured adults who previously accessed health care through county programs became newly eligible for Medi-Cal. With fewer adults turning to counties for health care, the state redirected some indigent health care dollars away from counties, as described in Part 4.

Mental Health Allocation

Less than 10% of realignment funding — an estimated $618 million in 2025-26 — supports counties’ role in delivering mental health services.

The Mental Health Subaccount includes funding for community-based mental health services, state hospital services for civil commitments, and Institutions for Mental Disease (IMDs) — facilities with 16 or more beds where people reside to receive treatment for mental illness as well as medical and nursing care services.

Looking at it through a different lens, these services include both 1) Medi-Cal specialty mental health services and 2) non-Medi-Cal services.

What Else Changed with Realignment in 1991?

In addition to establishing dedicated revenue streams and allocation formulas, the 1991 realignment legislation included other significant elements. Specifically:

Counties may transfer a limited amount of their annual revenue from one realignment account to another.

Counties are allowed to transfer funds among the Health, Mental Health, and Social Services subaccounts.

Specifically, up to 10% of one account’s annual allocation may be shifted to the other two subaccounts.

In addition, under certain circumstances, counties may transfer:

An additional 10% of funds from the Health account to the Social Services subaccount.

An additional 10% of funds from the Social Services subaccount to the Health or Mental Health subaccounts.

Realignment legislation included “poison pill” provisions — one of which remains in effect today.

When the realignment legislation was advancing, state leaders were uncertain whether any of its provisions would be challenged through a lawsuit or a “mandate” claim filed by a county seeking reimbursement from the state.

As a result, state leaders added several “poison pills” to the legislation that were intended to nullify key components of realignment if a challenge was successful.

Some of the hurdles created by these poison pills were ultimately overcome — specifically, provisions that would have rolled back the half-cent sales tax increase or the Vehicle License Fee increase, either of which would have reduced the revenue available to support the realigned programs.

However, one of the poison pills remains active: If any county makes a mandate claim that results in state costs of more than $1 million, the 1991 realignment would come to an end.

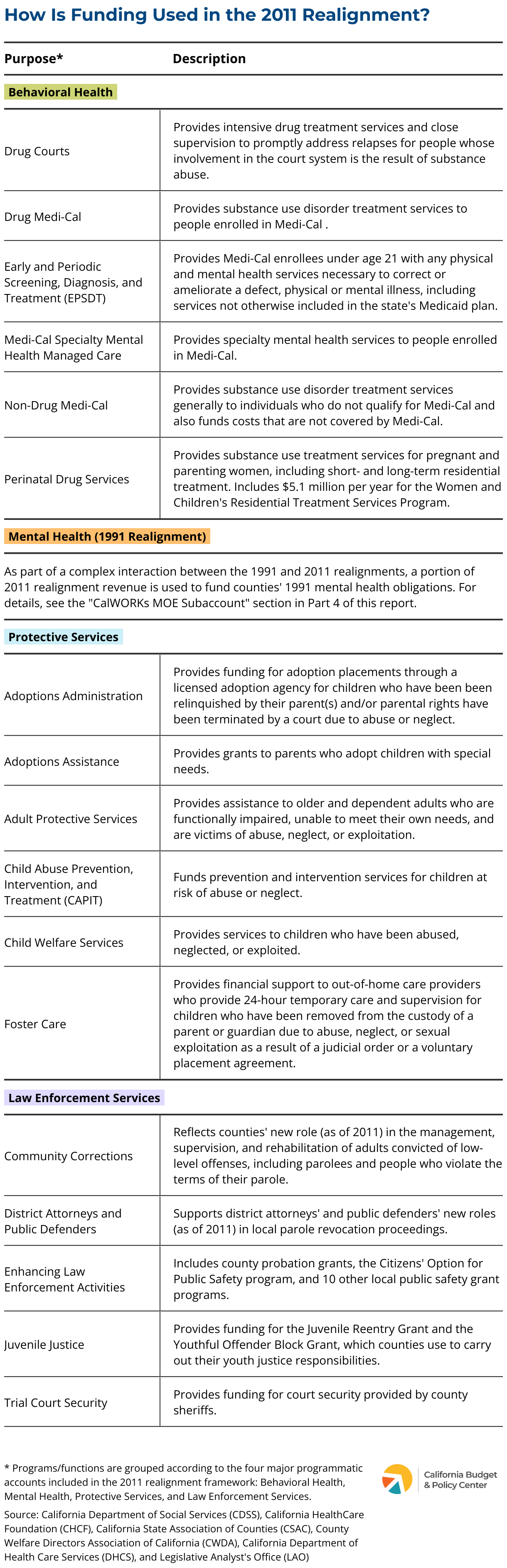

Part 3: Key Facts About the 2011 Realignment

What Did the 2011 Realignment Do?

In 2011, the Legislature built on the 1991 realignment by further increasing counties’ responsibility for several health and social services programs while also realigning certain public safety functions. (See the Appendix for descriptions of these programs.) This new realignment in 2011 revised the state-county relationship in two key ways:

Counties became fully responsible for funding — supported with realignment revenue — certain behavioral health, social services, and public safety programs that they were already administering.

Prior to 2011, counties, the state, and the federal government shared the cost of operating the child welfare system and key behavioral health services. With the 2011 realignment, the state stopped using its own General Fund dollars to help pay for the nonfederal costs of these programs. Instead, counties started paying 100% of the nonfederal costs using realignment funds to help pay for those costs. This change applied to:

Nearly the entire child welfare system, including Child Welfare Services, Foster Care, Adoptions Administration, Adoption Assistance, and Child Abuse Prevention, Intervention, and Treatment.

Major behavioral health programs, including Drug Medi-Cal services, Medi-Cal Specialty Mental Health Managed Care, and the Early and Periodic Screening, Diagnosis, and Treatment (EPSDT) program.

The state also eliminated General Fund support for several other programs that counties were administering in 2011. Instead, counties began to use the revenue provided by the 2011 realignment to fund these programs. This change applied to:

The Adult Protective Services program.

Key substance use treatment programs, such as drug courts and the Women and Children’s Residential Treatment Services Program.

Certain local public safety programs and functions, including trial court security, counties’ youth justice responsibilities, and local grants focused on law enforcement and county probation.

Counties took on new responsibility — supported with realignment revenue — for certain public safety functions that previously had been carried out by the state.

In order to help reduce overcrowding in state prisons, the 2011 realignment included a new role for counties in managing, supervising, and rehabilitating adults convicted of certain low-level offenses — a change commonly called “community corrections.” Previously, people convicted of low-level offenses served their sentences in state prison and were supervised by state parole agents upon their release.

The Legislature also created new roles for county district attorneys and public defenders in parole revocation hearings. These proceedings determine whether people who violate the terms and conditions of their local supervision should be punished with county jail time.

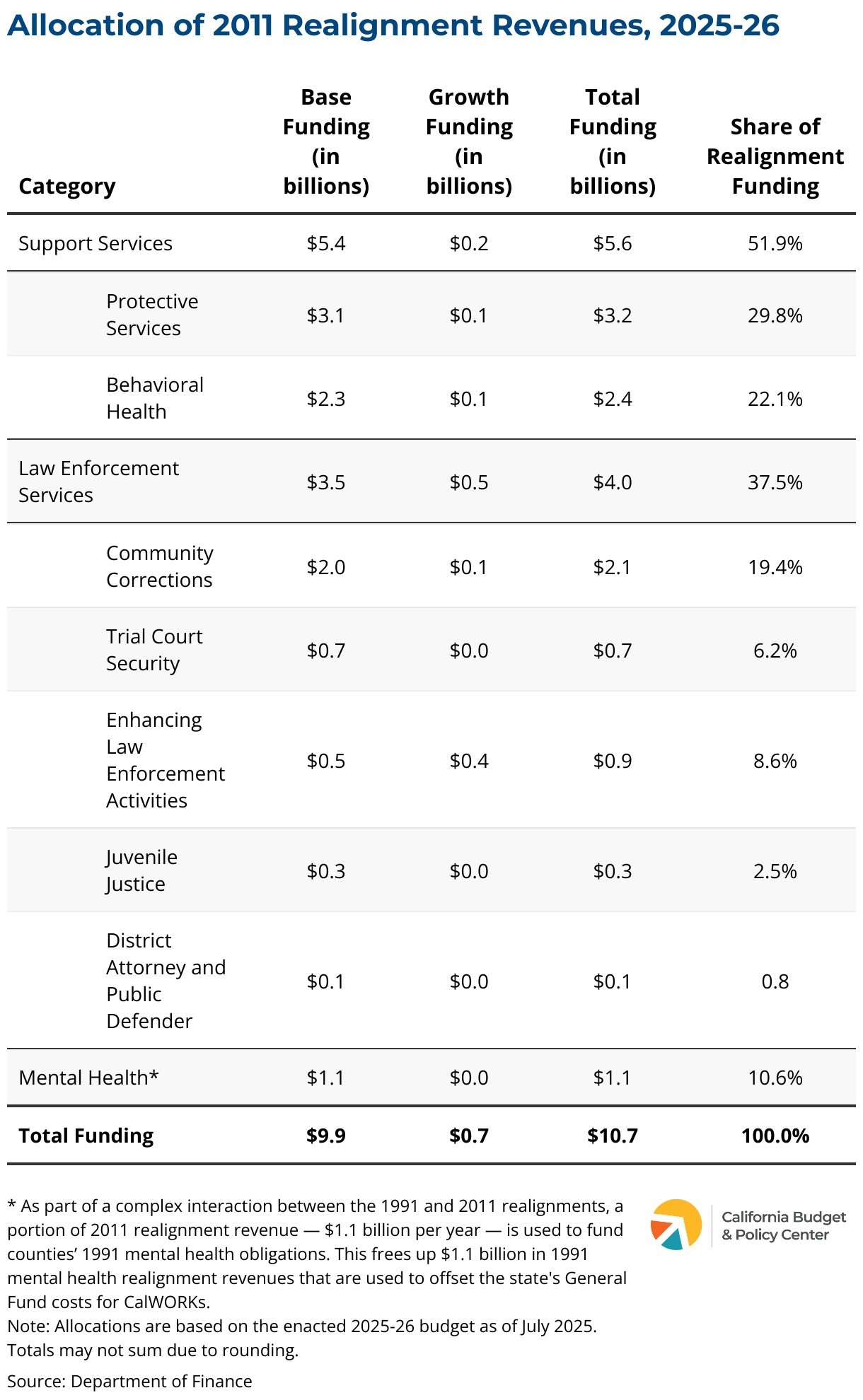

How Is the 2011 Realignment Funded?

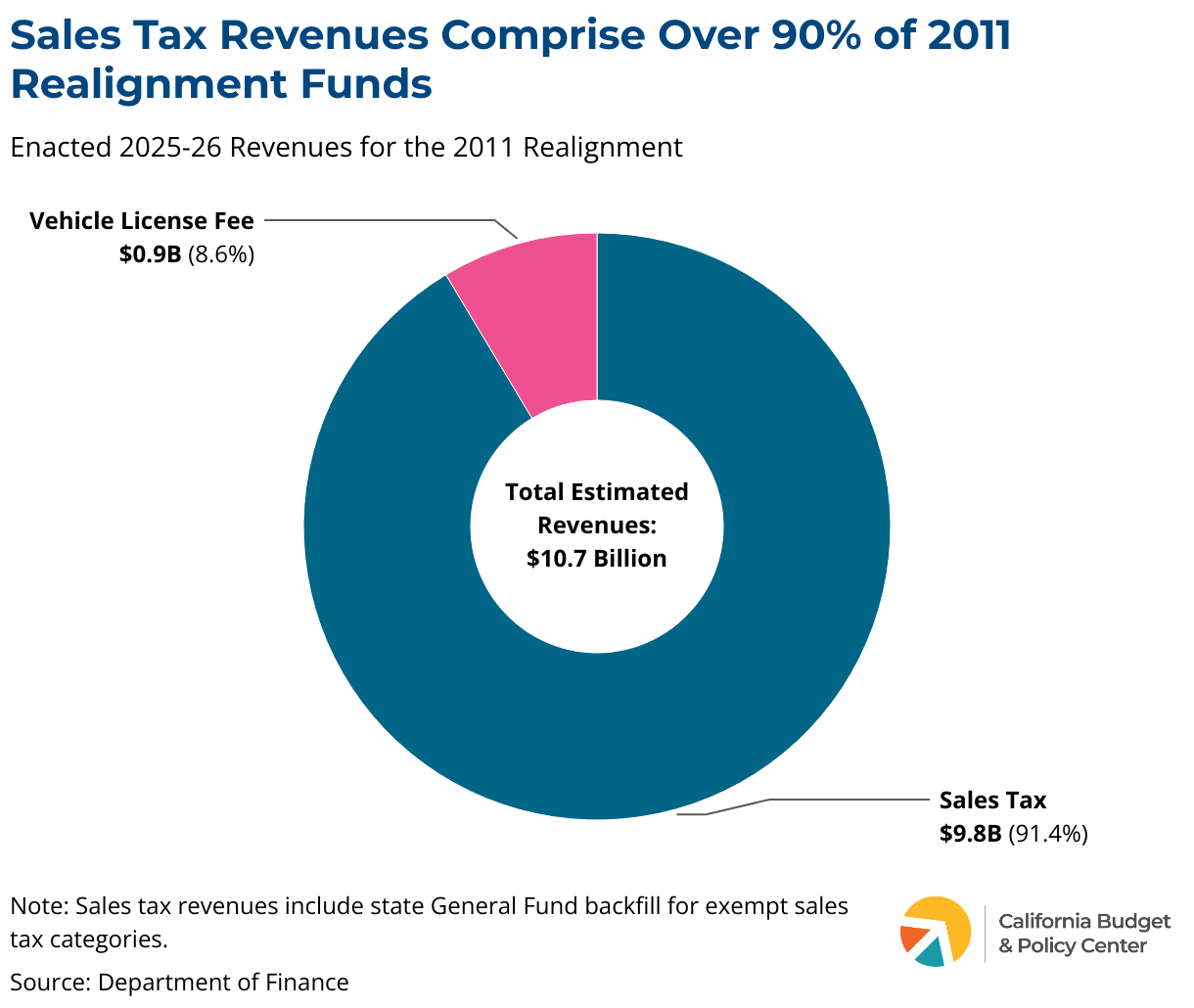

To fund the 2011 realignment, state leaders carved out portions of two existing revenue streams and dedicated those revenues to counties. These revenues are estimated to total $10.7 billion in 2025-26.

The Legislature redirected to counties a portion of state sales taxes as well as a portion of Vehicle License Fee (VLF) revenue in order to fund the realigned programs.

The Legislature shifted revenues equal to 1.0625 cents of the state sales tax rate to counties. In other words, slightly more than 1 cent of the sales tax rate on each $1 in taxable purchases bypasses the state treasury and goes directly to counties. In 2025-26, these diverted sales tax dollars are estimated to total $9.8 billion — more than 90% of all revenues that counties receive through the 2011 realignment.

In addition, the state uses General Fund dollars to backfill for certain exempt sales tax categories. This provides a relatively small amount of additional revenue to support counties’ 2011 realignment responsibilities. This General Fund backfill is estimated to total $44.2 million in 2025-26.

The Legislature also redirected a portion of VLF revenues to counties. In 2025-26, the VLF revenues shifted to counties are estimated to total $919.3 million — about 9% of all revenues that counties receive through the 2011 realignment.

What is the sales tax?

The sales tax — formally, the “sales and use tax” — is a tax on the purchase of tangible goods in California (the “sales tax”) or the use of tangible goods in California that were purchased elsewhere (the “use tax”).

Services are excluded from the sales and use tax, as are other items exempted by law, including groceries, menstrual hygiene products, and medications.

The sales and use tax is a regressive tax because households with lower incomes generally spend a larger share of their incomes on necessities than households with higher incomes, so a larger share of their income goes to sales taxes.

What is the vehicle license fee?

The VLF is an annual state fee that is based on the purchase price or value of a vehicle.

In 2011, state leaders shifted to counties part of the base 0.65% VLF rate in order to help fund counties’ increased responsibilities under the 2011 realignment.

How Is the 2011 Realignment Structured?

The 2011 realignment revenues move through a complicated set of accounts that the Legislature last modified in 2012, the year after this realignment was adopted.

Revenue

The state sales tax and Vehicle License Fee (VLF) revenues that fund the 2011 realignment flow into an account called the “Local Revenue Fund 2011” until this fund reaches its “base” level for a fiscal year.

These base funds support counties’ role in providing the services included in the 2011 realignment.

Realignment revenues sometimes fail to reach the base level of funding, such as when sales tax revenues decline during a recession. When this happens, counties receive less funding, but the gap is tracked and the base is gradually restored when revenues begin to grow again.

In other words, under the 2011 realignment, counties’ base funding is temporarily lowered when revenues decline. In contrast, when 1991 realignment revenues fail to reach the base level, counties’ base funding is permanently lowered because there is no requirement for base restoration in the 1991 realignment.

What is realignment “Base” revenue?

“Base” revenue for a fiscal year = the amount of realignment revenue allocated to counties in the prior fiscal year. In other words, the total amount of realignment revenue that counties receive in one year becomes the base level of funding for the next fiscal year.

Any sales tax and VLF revenue that exceeds the base funding level for a fiscal year becomes “growth” revenue.

Growth revenue — if available — is allocated to the programs included in the 2011 realignment based on complex rules that set funding priorities.

For example, if sales tax revenue grows year-over-year, about two-thirds of that growth is divided among the behavioral health and social services programs, while the remaining one-third of those growth dollars go to the public safety programs.

what is realignment “growth” revenue?

“Growth” revenue = the amount of realignment revenue left over (if any) after the base level of revenue for a fiscal year has been reached.

In other words, sales tax and VLF revenue that exceeds the base level of funding for a fiscal year flows to counties on top of their base allocations.

Allocations: Big Picture

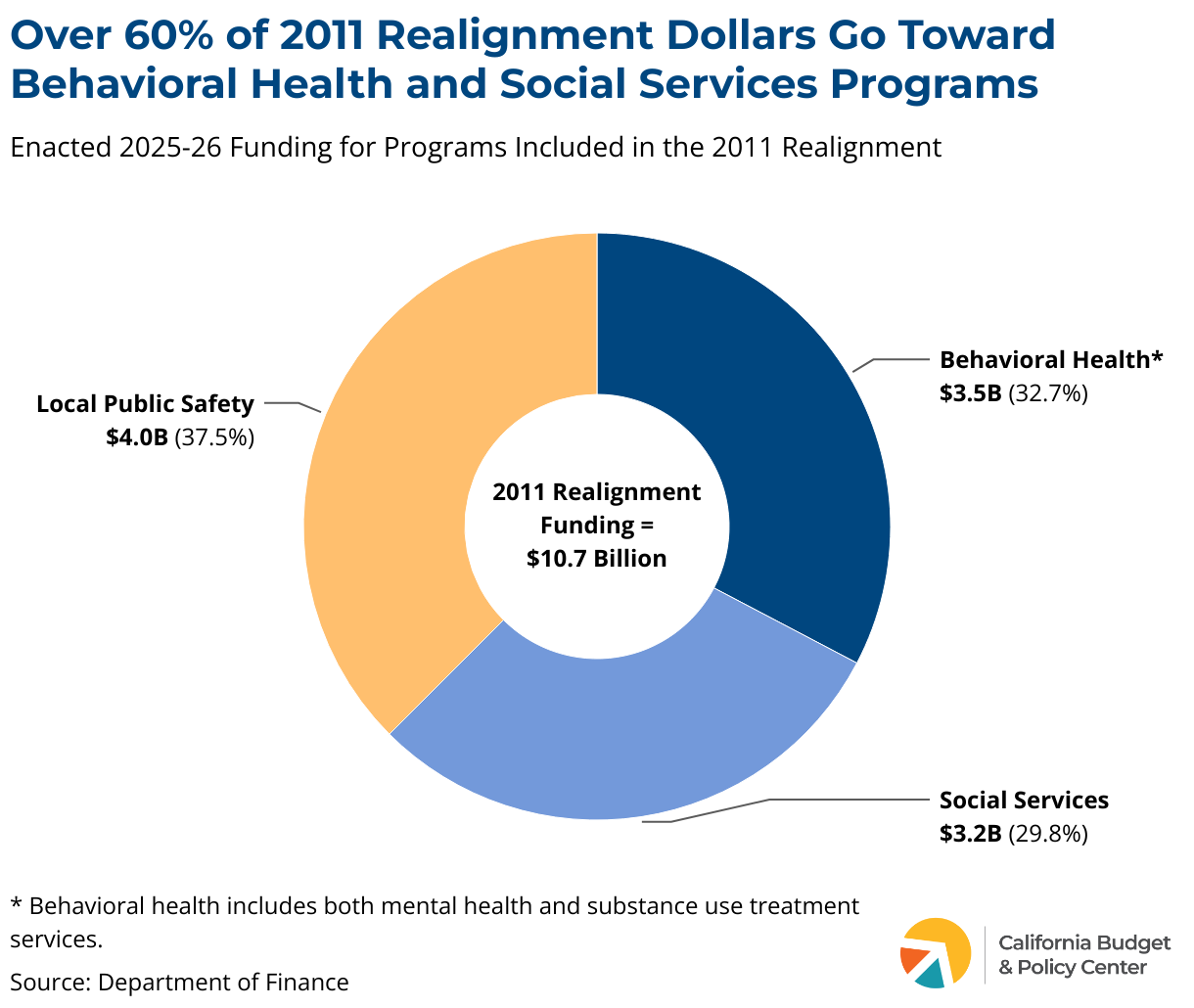

More than 60% of revenues provided through the 2011 realignment — an estimated $6.7 billion in 2025-26 — support counties’ role in delivering behavioral health and social services. The remaining funds — an estimated $4.0 billion — go to public safety programs that were realigned to counties in 2011.

Behavioral Health Allocation

Nearly one-third of 2011 realignment funding — an estimated $3.5 billion in 2025-26 — supports behavioral health services. This includes funding for both 1) the mental health and substance use disorder treatment services that counties took increased responsibility for starting in 2011 and 2) the mental health services that were shifted to counties as part of the earlier realignment in 1991.

$2.4 billion of these funds flow into the Behavioral Health Subaccount, which was created as part of the 2011 realignment.

This subaccount supports both 1) Medi-Cal specialty mental health and substance use disorder treatment services and 2) non-Medi-Cal services, including:

Early and Periodic Screening, Diagnosis, and Treatment (EPSDT) services for children and youth,

Medi-Cal Specialty Mental Health Managed Care (MHMC), and

Substance use treatment services, including perinatal drug services and drug courts.

In 2011, counties were already administering these programs. The primary impact of the 2011 realignment was to increase counties’ costs — and eliminate the state’s costs — for these programs, with the new realignment revenue intended to help counties meet their larger financial obligations.

For example, since 2011 counties have been fully responsible for the nonfederal share of costs for EPSDT and MHMC.

The remaining $1.1 billion of these 2011 realignment funds flow into the Mental Health Subaccount, which was created as part of the 1991 realignment.

These funds — which are capped at $1.1 billion per year — support the mental health responsibilities that counties took on in 1991 as part of the first major state-to-county realignment.

In other words, counties’ 1991 mental health responsibilities are largely funded with revenues provided by the 2011 realignment rather than with 1991 realignment dollars — a fund switch that benefited the state’s General Fund. See Part 4 for details about this switch.

Social Services Allocation

Around 30% of 2011 realignment funding — an estimated $3.2 billion in 2025-26 — supports counties’ role in providing social services for children, youth, and older and dependent adults.

These funds flow into the Protective Services Subaccount, supporting Child Welfare Services, Foster Care, Adoption Assistance, and related programs for children and youth as well as Adult Protective Services.

In 2011, counties were already administering these programs, most of which were also included in the 1991 realignment. The primary impact of the 2011 realignment was to increase counties’ costs — and eliminate the state’s costs — for these programs, with the new realignment revenue intended to help counties meet their larger financial obligations.

For example, since 2011 counties have been fully responsible for the nonfederal share of costs for the child welfare system.

Public Safety Allocation

Over one-third of 2011 realignment funding — an estimated $4.0 billion in 2025-26 — supports public safety programs.

These funds flow into the Law Enforcement Services Account and primarily support counties’ role in “community corrections” — the management, supervision, and rehabilitation of people convicted of certain low-level offenses who, prior to 2011, served their sentences in state prison and were supervised by state parole agents upon release.

What Else Changed with Realignment in 2011?

In addition to establishing dedicated revenue streams and allocation formulas, the 2011 realignment legislation included other significant elements. Specifically:

Counties may transfer a limited amount of revenue between the Behavioral Health and Protective Services subaccounts, both of which are part of the Support Services Account.

Specifically, counties may shift — in either direction — an amount of funding that does not exceed 10% of the funds in the smaller account, based on the prior fiscal year’s funding level. (Certain counties are not subject to the 10% cap.)

Any transfer applies only for the fiscal year in which it is made, meaning that transfers do not create a permanent funding shift.

Counties are not allowed to transfer funds between the Support Services Account and the Law Enforcement Services Account.

This means that funding for behavioral health programs and social services cannot be used for law enforcement purposes (or vice versa) — even on a temporary basis.

The 2011 realignment includes constitutional protections approved by California voters.

In 2012, California voters strengthened the 2011 realignment by approving Proposition 30, which enshrined significant protections for the state and counties in the state Constitution. Specifically, Prop. 30:

Constitutionally protects the state revenue that was shifted to counties to fund their responsibilities under the 2011 realignment. This means the state cannot reduce or eliminate these revenues without voter approval.

Requires the state to provide counties with alternative funding if current realignment revenues are eliminated.

Allows counties to disregard state policy changes that increase realignment program costs if the state does not provide funding to offset those costs.

Requires the state to pay at least half of any 2011 realignment program cost increases that stem from federal court or administrative decisions or federal law or regulations.

Constrains the state’s ability to submit federal plans or waivers that would increase counties’ costs for realigned programs.

Protects the state from mandate claims related to the 2011 realignment.

Part 4: How State Leaders Reshaped Realignment to Benefit the State Budget

In the early 2010s, as California struggled to emerge from the Great Recession, state leaders made three major changes to the 1991 realignment framework to reduce cost pressures on the state’s General Fund. Notably, one of these changes involved shifting funds between the 1991 and 2011 realignments.

Taken together, these changes today provide a roughly $3 billion annual benefit to the state budget. These adjustments to the 1991 realignment funding structure — and the new accounts that were created to implement them — are described below.

CalWORKS MOE Subaccount

In 2011, state leaders approved a complex funding shift between county-run mental health programs and CalWORKs, creating over $1 billion in annual state General Fund savings.

In 2011, as state leaders were developing California’s second major state-to-county realignment, they decided to use a portion of the revenue from this new realignment — capped at $1.1 billion per year — to pay for counties’ mental health obligations, which were shifted to counties as part of the first major realignment in 1991.

This fund shift freed up $1.1 billion of 1991 realignment revenue that otherwise would have remained in the Mental Health Subaccount and supported counties’ mental health responsibilities. In other words, counties no longer needed those 1991 realignment dollars for mental health because those funds were replaced with revenue from the 2011 realignment.

These freed-up revenues were redirected to a CalWORKs MOE Subaccount that was added to the 1991 realignment framework (MOE = “maintenance of effort”). These dollars replaced, or offset, the state’s cost for CalWORKs grants, resulting in ongoing annual state General Fund savings of $1.1 billion.

Because this policy change implemented a funding shift rather than a funding cut, there was no detrimental impact on county-run mental health programs or on the CalWORKs program.

Family Support Subaccount

In 2013, state leaders shifted some 1991 realignment revenue from county-run indigent health care programs to CalWORKs, generating hundreds of millions of dollars in ongoing state General Fund savings.

Prior to 2014, Californians with low incomes who were ineligible for Medi-Cal (Medicaid) received care through county indigent health care programs, which were part of the 1991 realignment and funded with realignment revenues.

With the passage of the federal Affordable Care Act (ACA) in 2010, states were allowed to expand — starting in 2014 — their Medicaid programs to millions of adults who previously were excluded due to Medicaid’s stringent rules. California implemented this expansion in 2014. This change shifted primary responsibility for providing health care to these adults — along with the cost — from counties to the state and federal governments.

Given counties’ diminished role — and the state’s significantly expanded role — in indigent health care, state leaders created a complex set of formulas to capture county savings. In other words, a portion of counties’ 1991 realignment revenue for indigent health care was shifted to the state. These changes were included in Assembly Bill 85 (Committee on Budget, Statutes of 2013), as modified by Senate Bill 98 (Chapter 358, Statutes of 2013).

These redirected 1991 realignment revenues:

Are deposited into the Family Support Subaccount, which was added to the 1991 realignment framework by AB 85.

Replace, or offset, the state’s cost for CalWORKs grants and county administration of the program, resulting in annual state General Fund savings.

The amount of 1991 health realignment funds redirected to the state varies from year to year. This fund shift is estimated to exceed $700 million in 2025-26.

Child Poverty and Family Supplemental Support Subaccount

In 2013, state leaders redirected a portion of 1991 realignment “growth” revenue to support periodic increases to CalWORKs cash assistance for families, precluding the need for the state General Fund to pay for these increases.

In the early 2010s, the state adjusted counties’ share of cost for the In-Home Supportive Services (IHSS) program, which counties fund largely with revenues provided by the 1991 realignment.

With this adjustment, counties’ costs for IHSS grew more slowly than under the previous cost-sharing formula. As a result, counties needed less 1991 realignment revenue to cover their annual IHSS cost growth. Under the longstanding rules of the 1991 realignment, these freed-up revenues became available for other programs, such as public health and mental health services.

However, state leaders changed the rules for distributing certain 1991 realignment growth revenue (“general growth”) in order to provide periodic CalWORKs grant increases with these growth dollars. These changes were included in Assembly Bill 85 (Committee on Budget, Statutes of 2013), as modified by Senate Bill 98 (Chapter 358, Statutes of 2013).

As a result, in addition to supporting counties’ long-standing health and mental health obligations, a portion of “general growth” dollars were shifted into a Child Poverty and Family Supplemental Support Subaccount — often called the “Child Poverty” account — that was added to the 1991 realignment framework by AB 85 in 2013.

Child Poverty funds provide automatic CalWORKs grant increases if there is enough funding to support 1) the ongoing cost of prior grant increases and 2) the ongoing cost of a new grant increase. Funds in the Child Poverty account have grown from $0 in 2013-14 to an estimated $1.1 billion in 2025-26.

Using a portion of 1991 realignment revenue to fund periodic CalWORKs grant increases means that less money from the state’s General Fund is needed for this purpose, improving the state budget’s bottom line. Nonetheless, state leaders have continued to use General Fund dollars to provide some discretionary grant increases over the past decade. These discretionary increases — which are on top of the automatic increases provided with realignment funds — have aimed to reduce the number of CalWORKs families living in extreme poverty.

Appendix

1991 Realignment Details: Funding and Programs

This table displays estimated funding for each 1991 realignment account as of the enacted 2025-26 state budget (signed into law in June 2025):

This table describes the programs and functions included in the 1991 realignment:

2011 Realignment Details: Funding and Programs

This table displays estimated funding for each 2011 realignment account as of the enacted 2025-26 state budget (signed into law in June 2025):

This table describes the programs and functions included in the 2011 realignment:

The amount of realignment revenue that counties receive in one fiscal year becomes the base level of funding for the next fiscal year. Therefore, counties’ base allocation for a fiscal year equals the amount of revenue allocated in the prior fiscal year, with growth revenue (if any) provided on top of the base.

Base Restoration

When 2011 realignment revenues fall short of meeting the base level of funding for all subaccounts, this shortfall is tracked and repaid in later fiscal years when revenues are higher. The 1991 realignment does not include a base restoration provision.

Growth Allocation

The amount of realignment revenue left over (if any) after the base allocation for a fiscal year has been reached. Sales tax and VLF revenue that exceeds the base level of funding for a fiscal year flows to counties on top of their base allocations.

Maintenance-of-Effort (MOE)

A requirement for one level of government to maintain a set level of spending for a program in order to receive additional funding for that program from another level of government.

Poison Pill

Legislation that was intended to nullify key components of the 1991 realignment if any county filed a successful challenge. Only one poison pill provision is still in effect today: If any county makes a mandate claim that results in state costs of more than $1 million, the 1991 realignment would come to an end.

Realignment

Periodic shifts in responsibility between the state and counties for the financing and implementation of public services.

Sales Tax

A tax on the purchase of tangible goods in California (the “sales tax”) or the use of tangible goods in California that were purchased elsewhere (the “use tax”).

Subaccount

Accounts to which dedicated revenues are transferred to fund a program or groups of programs. Includes, for example, the Social Services Subaccount (1991 realignment) and the Behavioral Health Subaccount (2011 realignment).

Unmet Need

Occurs when revenue growth for a fiscal year is less than the increase in costs for social services programs included in the 1991 realignment. As revenues increase in later years, additional funds are provided to social services programs through the Caseload Subaccount to make up the difference — which reduces the revenue growth available to support other programs funded through the 1991 realignment.

Vehicle License Fee

An annual state fee that is based on the purchase price or value of a vehicle.

guide to the county budget process

Check out our Guide to the County Budget Process — a resource designed to help Californians understand how county budgets work and how you can engage with local leaders to advocate for fair and just policy choices.

Supported by California Health Care Foundation (CHCF), which works to ensure that people have access to the care they need, when they need it, at a price they can afford. Visit www.chcf.org to learn more.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Watch to learn more

Ever wondered where California gets the money to fund schools, healthcare, and public services? This quick explainer breaks down the key components of the state budget — from the General Fund to federal dollars — and shows how these funds work together to power the state’s economy and serve its communities.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Watch to learn more

California’s state budget affects every Californian, but where do those dollars go? In this short explainer video, we break down how California’s budget is funded and where the money goes, from health care and education to public infrastructure, safety net programs, and environmental protection.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Each year, California’s 58 counties develop their budgets, which are influenced by state-mandated responsibilities as well as funding decisions made by the governor and Legislature. However, these budgets also reflect the unique priorities and needs of residents and county leaders, balancing state requirements with community-driven goals

This infographic illustrates the key steps in the county budget process, how it interacts with the state budget process, as well as the respective roles of the Board of Supervisors and the County Manager.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

California’s Constitution establishes several statewide offices that oversee the functions, policies, and programs of state government. While the Governor is the most prominent and powerful statewide official, several other constitutional officers have significant authority and responsibilities that affect the day-to-day lives of Californians, including the Attorney General, the Controller, and the Insurance Commissioner. In addition, the Constitution establishes the Board of Equalization, the only elected tax board in the United States.

Elections for all of these executive branch offices are held every four years, during non-presidential election years. Term limits apply: Individuals may only be elected to two four-year terms for any office. However, a person may hold a position for more than eight years if they are appointed to fill a vacancy and then elected to two four-year terms.

This glossary identifies current constitutional officeholders in the executive branch and highlights the roles and responsibilities of each office.

Acts as representative for the People of California in civil and criminal matters that come before trial, appellate, and supreme courts in California and at the federal level.

Ensures that laws are enforced fairly and impartially.

Coordinates statewide law enforcement efforts, assists local and federal law enforcement agencies, and provides legal counsel to state officers as well as to state departments, boards, and commissions.

Elected in 2018, reelected to final four-year term in 2022.

Statewide (Ex Officio):Malia M. Cohen, California State Controller

Elected to a four-year term in 2022.

Role in a nutshell:

Oversees California’s property tax system, the Alcoholic Beverage Tax, and the Insurance Tax.

Key duties:

Oversees and aids in the assessment practices of California’s 58 county assessors, promoting a uniform property tax system across the state.

Directly assesses certain public utilities and properties — such as property used by telephone companies or by gas and electric companies — and allocates the assessed values among the counties where the properties are located.

Holds hearings and decides on taxpayer appeals related to the tax programs that the Board constitutionally oversees.

Manages the Private Railroad Car Tax — the only property tax administered and collected by the state.

Responsible for tracking and protecting California’s public funds.

Key duties:

Audits state expenditures, monitors the fiscal condition of state and local governments, and administers payroll systems for state government and California State University employees.

Safeguards lost and forgotten property turned over to the state — such as bank accounts and insurance benefits — until claimed by the rightful owners.

Chairs the Franchise Tax Board and sits on numerous boards and commissions, including the California Public Employees’ Retirement System (CalPERS) and the California State Teachers’ Retirement System (CalSTRS).

Serves as one of five members of the California State Board of Equalization in an “ex officio” capacity.

Elected in 2018, reelected to final four-year term in 2022.

Role in a nutshell:

Oversees the executive branch — except for independent entities like the University of California Board of Regents as well as offices and departments overseen by other constitutional officers.

Key duties:

Executes the laws of the state.

Fills numerous positions throughout the executive branch as well as judicial vacancies and newly created judgeships.

Submits a proposed state budget by January 10 of each year and a revised budget by May 14 of each year.

Reviews bills passed by the Legislature and may 1) sign or veto any bill and 2) reduce or eliminate any item of appropriation.

Serves as commander-in-chief of the state militia and as California’s official communicator to other states and to the federal government.

Elected in 2018, reelected to final four-year term in 2022.

Role in a nutshell:

Governor-in-waiting — automatically becomes governor if a vacancy occurs.

Key duties:

Serves as acting governor when the governor leaves California.

Serves as president of the state Senate and casts tie-breaking votes.

Serves on several boards and commissions, including the boards that oversee the California Community Colleges, the California State University, and the University of California.

Appointed by Gov. Gavin Newsom to fill a vacancy in December 2020.

Elected to a full four-year term in 2022.

Role in a nutshell:

California’s chief elections officer.

Key duties:

Administers election laws, including testing voting equipment, publishing a voter information guide, compiling election returns, and certifying election results.

Maintains key databases, including of registered voters and lobbyists, campaign contributions, domestic partners, advance health care directives, and local, state, and federal elected officials.

Keeps the complete record of the official acts of the legislative and executive branches, including laws passed by the Legislature.

Provides several business-related services, including approving articles of incorporation for new California corporations and qualifying out-of-state and international corporations to do business in California.

Leads the operational aspects of the public school system, including teacher licensing.

Serves on numerous boards and commissions, including the University of California Board of Regents, the California State University Board of Trustees, and the California Commission on Teacher Credentialing.

Elected in 2018, reelected to final four-year term in 2022.

Role in a nutshell:

California’s banker, investor, and lead asset manager.

Key duties:

Safely invests tax dollars on behalf of the state and local governments through the Pooled Money Investment Account to manage the state’s cash flow and strengthen the financial security of local governments.

Sells state bonds, including voter-approved general obligation bonds.

Chairs or serves on several boards, commissions, and authorities, including state pension boards and the California Housing Finance Agency.

Chairs dozens of bond finance committees.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

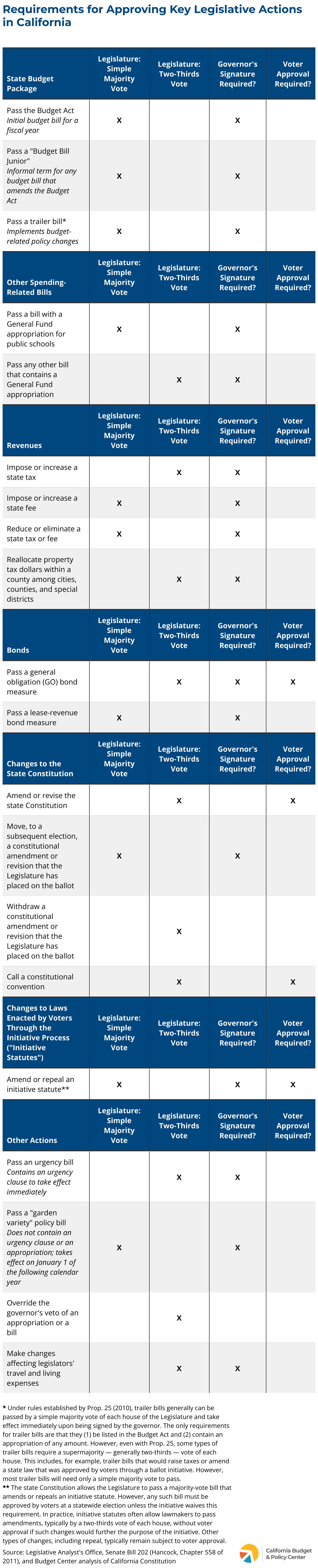

California’s Constitution establishes rules for a wide range of legislative actions, from passing the state budget to increasing taxes to placing constitutional amendments on the ballot.

Some actions need only a simple majority vote of each house of the Legislature — 41 votes in the 80-member Assembly and 21 votes in the 40-member state Senate.

Other actions require a two-thirds vote of each house of the Legislature — 54 votes in the Assembly and 27 votes in the Senate.

Most legislative actions require the governor’s signature, and some need voter approval.

This table summarizes the requirements for approving key legislative actions in California.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Watch to learn more

Explore the year-long process of creating and revising California’s state budget — a process that shapes policies impacting every Californian. This video simplifies each key step, from initial proposals by state agencies to the governor’s budget release, legislative reviews, and final negotiations.

Gain the insights you need to stay informed and empowered about California’s financial decisions.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

This website uses cookies to analyze site traffic and to allow users to complete forms on the site. The California Budget & Policy Center does not share, trade, sell, or otherwise disclose personal information. By using our website you agree to our Privacy Policy.

California Budget & Policy Center

Secure Your Early Bird Ticket!

Join us in Sacramento on April 22, 2026 for engaging sessions, workshops, and networking opportunities with fellow changemakers, inspiring speakers, and much more.