Dollars & Democracy: An Introduction to California’s State Budget Process is an introductory training slide deck that breaks down how California’s state budget works. Designed to be clear, engaging, and accessible, this slide deck explains the fundamentals of the state budget, the rules that shape the process, the key decision-makers involved, and the advocacy opportunities available at each stage of the budget cycle. This training is designed for advocates, community organizers, students, journalists, and anyone looking to better understand how California’s budget decisions are made.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

Cada año, el gobernador y la asamblea legislativa adoptan un presupuesto estatal que provee un marco y fondos para servicios y sistemas públicos esenciales: desde cuidado infantil y atención médica y transporte hasta universidades y escuelas de jardín de infantes al décimo primer grado.

Pero el presupuesto estatal no es solo dólares y centavos.

El presupuesto expresa nuestros valores así como nuestras prioridades para los californianos y como estado. En su mejor versión, el presupuesto debe reflejar nuestra labor colectiva para expandir las oportunidades económicas, promover el bienestar y mejorar las vidas de los californianos que no tiene la oportunidad de compartir la riqueza de nuestro estado y merecen tener dignidad y apoyo para vivir vidas prósperas.

Las elecciones del presupuesto estatal afectan a todos los californianos. Estas decisiones afectan la calidad de nuestras escuelas y nuestra atención médica, el costo de la educación terciaria, el acceso de las familias a cuidado infantil y vivienda asequibles, la disponibilidad de servicios y apoyo financiero para ayudar a los adultos mayores a envejecer sin tener que mudarse, y muchísimo más.

Como el presupuesto estatal afecta tantos servicios y nuestras vidas cotidianas, es esencial que los californianos entiendan el proceso de presupuesto anual y participen en él para asegurar que los líderes del estado tomen las decisiones estratégicas necesarias para permitir que todo californiano, sin importar su raza, sus antecedentes ni dónde se encuentre, prospere y pueda participar en la vida económica y social de nuestro estado.

Este informe ofrece información sobre el presupuesto estatal y su proceso con la meta de brindar a los californianos las herramientas que necesitan para interactuar eficazmente con los encargados de tomar decisiones y abogar por decisiones políticas justas y equitativas.

CONCLUSIONES CLAVE

Temas más importantes

El plan de gastos del estado no es solo dólares y centavos.

La creación del presupuesto les da a los californianos la oportunidad de expresar sus valores y prioridades como estado.

La Constitución estatal expone las normas del proceso presupuestario.

Entre otras cosas, estas normas permiten que los legisladores aprueben los gastos mediante un voto de mayoría simple, pero exige un voto de las dos terceras partes para aumentar los impuestos. Los votantes modifican el proceso presupuestario periódicamente aprobando enmiendas constitucionales.

El gobernador tiene una función de liderazgo en el proceso presupuestario.

Proponer un presupuesto estatal para el año fiscal siguiente le da al gobernador la primera palabra en las deliberaciones presupuestarias de cada año.

La revisión de mayo le da al gobernador otra oportunidad de establecer el plan presupuestario y político para el estado.

En general, el poder de veto le otorga la última palabra al gobernador.

La asamblea legislativa revisa y modifica las propuestas del gobernador.

Los legisladores pueden modificar las propuestas del gobernador e impulsar sus propias iniciativas al elaborar su versión del presupuesto antes de negociar un acuerdo con el gobernador.

Las decisiones presupuestarias se toman durante todo el año.

El público tiene varias oportunidades de expresar sus opiniones en el proceso presupuestario.

Esto incluye escribir cartas de apoyo o protesta, atestiguar en audiencias legislativas y reunirse con funcionarios del gobierno de gobernador, así como legisladores y miembros de su personal.

En pocas palabras, los californianos tienen amplias oportunidades de participar en el proceso presupuestario durante todo el año.

DATOS CLAVE SOBRE EL PRESUPUESTO ESTATAL DE CALIFORNIA

PRESUPUESTO ESTATAL = FONDOS ESTATALES + FONDOS

federales tres tipos de fondos estatales

Existen tres tipos de fondos estatales que conforman casi las dos terceras partes (64.8%) de presupuesto de $495.6 billones de California para 2025-26, el año fiscal que comenzó el 1 de julio de 2025. Específicamente:

Fondo general: El fondo general estatal cuenta con ingresos públicos que no están designados para un propósito específico. La mayor parte de los fondos para la educación, los servicios de salud y humanos y las prisiones del estado viene del fondo general.

Fondos especiales: Existen más de 500 fondos estatales especiales que administran impuestos, tasas y licencias designados para un propósito específico.

Fondos de bonos: Los fondos de bonos del estado registran la recepción y el desembolso de los recursos provenientes de bonos de obligación general (GO).

Los fondos federales constituyen el resto (35.2%) del presupuesto estatal de 2025-26.

LA MAYOR PARTE DE LOS INGRESOS PÚBLICOS DEL FONDO ESTATAL GENERAL Y ESPECIAL VIENE DE TRES FUENTES

los “tres grandes” impuestos de california

La mayor parte de los ingresos públicos vienen de los “tres grandes” impuestos de California. El total estimado de ingresos públicos del fondo general y el fondo especial combinados en 2025-26 es $296.7 billones, de los cuales casi el 73% ($215.8 billones) proviene de los tres grandes impuestos. Los tres grandes impuestos de California son:

Impuesto sobre los ingresos personales: Este es un impuesto sobre los ingresos de los residentes de California, así como sobre los ingresos de los no residentes provenientes de fuentes ubicadas en California. Es la mayor fuente de ingresos del estado de California.

Impuesto sobre las ventas y el uso: Este es un impuesto sobre la compra de bienes tangibles en California (el impuesto sobre las ventas) o sobre el uso en California de bienes tangibles que fueron adquiridos en otro lugar (el impuesto sobre el uso). Los servicios están excluidos del impuesto sobre las ventas y el uso, al igual que otros artículos exentos por ley, incluidos los alimentos y los medicamentos. El impuesto sobre las ventas y el uso es la segunda mayor fuente de ingresos públicos del estado de California.

Impuesto sobre las corporaciones: Este es un impuesto que se aplica a las corporaciones que hacen negocios en California o que obtienen ingresos provenientes de California, con la excepción de las compañías de seguros, que en su lugar pagan el impuesto sobre los seguros. El impuesto sobre las corporaciones es la tercera mayor fuente de ingresos públicos del estado de California.

Se estima que otros ingresos públicos del estado forman más de una cuarta parte (27.3 %) del total proyectado de ingresos del fondo general y de los fondos especiales en 2025-26. Estos otros ingresos públicos provienen de una amplia variedad de fuentes, incluidos impuestos, tarifas y multas.

EL PRESUPUESTO DEL ESTADO ES UN PRESUPUESTO LOCAL

Los dólares que se gastan a través del presupuesto estatal se destinan a personas, comunidades e instituciones en todo California. Según el presupuesto estatal aprobado para 2025-26:

Cuatro quintos de los gastos totales (80.6%) se destina en calidad de “asistencia local” a las escuelas públicas de jardín de infantes al décimo segundo grado, las escuelas terciarias comunitarias (Colleges), las familias inscritas en el programa CalWORKs y otros servicios y sistemas esenciales del estado que funcionan localmente.

Casi un quinto de los gastos totales (17.9%) se destina a 23 universidades estatales de California, más de 30 prisiones estatales y otros destinatarios de dólares para “operaciones estatales”.

Menos del 2 % del gasto total se destina a “gastos de capital”, que apoyan proyectos de infraestructura en todo California. (La asistencia local y los fondos de operaciones estatales también financian infraestructura).

LOS FONDOS DEL ESTADO FINANCIAN PRINCIPALMENTE LOS SERVICIOS DE SALUD Y HUMANOS O LA EDUCACIÓN

Según el presupuesto estatal aprobado para 2025-26:

Casi 3 de cada 4 dólares del fondo general y el fondo especial financian tres categorías de gastos: servicios de salud y humanos (42%), educación de jardín de infantes al décimo segundo grado (25.1%), y educación superior (7.2%).

Más del 5% de los dólares del fondo general y especial se destinan al sistema correccional, principalmente el sistema de prisiones estatales.

El saldo de estos dólares financian otros servicios esenciales (tales como el transporte y la protección medioambiental) e instituciones (tales como el sistema de tribunales estatales).

LOS FONDOS FEDERALES FINANCIAN PRINCIPALMENTE SERVICIOS DE SALUD Y HUMANOS

Según el presupuesto estatal aprobado para 2025-26:

Casi cuatro quintos de los dólares federales (78.3%) financian programas de servicios de salud y humanos.

El saldo de los dólares federales financia otros servicios esenciales, como el desarrollo de la fuerza laboral, la educación de jardín de infantes al décimo segundo grado, la educación superior y el transporte.

EL PRESUPUESTO ESTATAL FORMA PARTE DE UN PAQUETE DE PROYECTOS DE LEY

El presupuesto estatal nunca se presenta de manera aislada. En su lugar, avanza como parte de un paquete de legislación que por lo general incluye entre dos y tres docenas de proyectos de ley, y en ocasiones muchos más, en particular en los años en que existe un déficit presupuestario y los líderes estatales necesitan hacer múltiples cambios para equilibrar el presupuesto. En 2025, el gobernador Newsom firmó casi 50 proyectos de ley relacionados con el presupuesto.

cuatro tipos de proyectos de ley relacionados con el presupuesto

El paquete presupuestario incluye dos tipos de proyectos de ley presupuestarios con proyectos de ley asociados y otras leyes relacionadas con el presupuesto.

Ley de Presupuesto: El presupuesto estatal se conoce formalmente como la Ley de Presupuesto. La Ley de Presupuesto es el presupuesto inicial aprobado por la asamblea legislativa y firmada por el gobernador para convertirla en ley. En general, los proyectos de ley presupuestarios:

Otorgan autoridad para gastar dinero (“apropiaciones”) en una gama de servicios y sistemas públicos para un solo año.

Pasan por los comités presupuestarios de la asamblea legislativa según su propio calendario.

Proyecto de ley presupuestario junior: Este es el término informal que se utiliza para referirse a cualquier proyecto de ley presupuestario que modifica la Ley de Presupuesto, por ejemplo, aumentando o reduciendo los gastos autorizados. No existe un límite en la cantidad de proyectos de ley presupuestarios complementarios que pueden incluirse en un paquete presupuestario. Esto significa que las autoridades estatales pueden modificar la Ley de Presupuesto tantas veces como lo deseen mediante la aprobación de proyectos de ley presupuestarios adicionales.

Proyectos de ley remolque (trailer bills): El paquete presupuestario del estado también incluye proyectos de ley remolque. Los proyectos de ley remolque generalmente introducen cambios en la legislación estatal relacionados con la Ley de Presupuesto y, al igual que los proyectos de ley presupuestarios, avanzan a través de los comités presupuestarios de la asamblea legislativa. Además, los proyectos de ley remolque:

Deben contener al menos una asignación presupuestaria y estar incluidos en la Ley de Presupuesto, un requisito que los vincula directamente con el presupuesto estatal.

Están organizados por grandes áreas de política pública dentro del presupuesto. Por ejemplo, los cambios relacionados con la salud se incluirían en un proyecto de ley remolque para la “salud” y los cambios relacionados con la vivienda se incluirían en un proyecto de ley remolque para la “vivienda”, y así sucesivamente.

Otros proyectos de ley relacionados con el presupuesto: Se pueden incluir otros proyectos de ley en el paquete presupuestario de tanto en tanto. Estos son proyectos de ley que avanzan independientemente de la Ley de Presupuesto (y por lo tanto no son proyectos de ley remolque) pero igual se consideran parte del marco del presupuesto estatal. Esto puede incluir, por ejemplo, leyes para aumentar los impuestos o presentar enmiendas constitucionales a los votantes así como los proyectos de ley aprobados en una sesión especial de la asamblea legislativa. Estas otras leyes relacionadas con el presupuesto pueden avanzar ya sea a través de los comités de políticas de la asamblea legislativa como a través de los comités presupuestarios.

Comité presupuestario de la cámara de representantes y comité presupuestario y de revisión fiscal del senado

Revisan las propuestas presupuestarias del gobernador y elaboran la versión del presupuesto estatal de cada cámara. La mayor parte del trabajo de los comités presupuestario se hace a través de subcomités que se enfocan en áreas específicas de política pública.

Ley de Presupuesto

El proyecto de ley presupuestario inicial aprobado por la Legislatura y promulgado como ley por el gobernador, después de aplicar cualquier veto a partidas específicas. La Ley de Presupuesto puede identificarse por el año en el que entra en vigor («Ley de Presupuesto de 2026») o por el año fiscal al que corresponde («Ley de Presupuesto 2026-27»).

Proyecto de ley presupuestario junior

Es el término informal que se usa para describir todo proyecto de ley presupuestario que modifica la Ley de Presupuesto. Los proyectos de ley junior se pueden numerar en secuencia usando números romanos (por ejemplo, proyecto de ley junior I, proyecto de ley junior II, etc.).

Proyectos de ley relacionados con el presupuesto (“proyectos de ley remolque”)

En general hacen cambios a la ley estatal relacionada con la Ley de Presupuesto. Estos proyectos de ley se conocen formalmente como “proyectos de ley … relacionados con el proyecto de ley presupuestario”, pero se conocen más comúnmente como “proyectos de ley remolque (trailer)”. Los proyectos de ley remolque se indican en la Ley de Presupuesto y avanzan a través de los comités presupuestarios de la cámara de representantes y del senado. Los proyectos de ley remolque se organizan por área relacionada, como por ejemplo “salud”, “vivienda”, “educación superior” y “seguridad pública”.

De tanto en tanto, los proyectos de ley que avanzan independientemente de la Ley de Presupuesto, y por lo tanto no son proyectos de ley remolque, se pueden considerar parte del marco del presupuesto estatal general. Esto puede incluir, por ejemplo, leyes para aumentar los impuestos o presentar enmiendas constitucionales a los votantes.

Departamento de Finanzas (DOF)

Dirige el desarrollo de las propuestas presupuestarias del gobernador, prepara los documentos presupuestarios del gobernador, atestigua en nombre del gobernador en las audiencias legislativas presupuestarias, desarrolla los pronósticos económicos del gobernador y cumple con varias otras funciones. El director del DOF es el asesor fiscal en jefe del gobernador.

Resumen del presupuesto del gobernador

Presenta el panorama económico y de ingresos públicos del gobernador, destaca las principales iniciativas de política pública incluidas en el presupuesto propuesto por el gobernador y resume los gastos estatales propuestos. El resumen del presupuesto se publica el 10 de enero o antes.

Presupuesto propuesto del gobernador

Proporciona una descripción detallada de los gastos propuestos por el gobernador para el próximo año fiscal, los gastos estimados para el año fiscal en curso y los gastos reales del año fiscal anterior. El presupuesto propuesto se publica el 10 de enero o antes.

Oficina del analista legislativo (LAO)

Oficina independiente y no partidaria que hace investigaciones y análisis sobre asuntos del presupuesto estatal, analiza medidas electorales de alcance estatal y brinda asesoramiento fiscal y de política pública a la asamblea legislativa. La LAO es supervisada por el comité presupuestario legislativo conjunto, que es bipartito.

Veto de elementos específicos

La facultad del gobernador de reducir o eliminar elementos de apropiación específicos a pesar de aprobar porciones de un proyecto de ley. Esta facultad es aplicable a cualquier proyecto de ley que contenga una apropiación, incluso los proyectos de ley presupuestarios y los proyectos de ley relacionados con el presupuesto. La asamblea legislativa puede anular un veto con dos terceras partes del voto en casa cámara.

Revisión de mayo

Publicada a más tardar el 14 de mayo, la revisión de mayo actualiza el panorama económico y de ingresos públicos del gobernador; ajusta los gastos propuestos por el gobernador para reflejar estimaciones y supuestos revisados; revisa, complementa o retira las iniciativas de política pública incluidas en el presupuesto propuesto en enero; y detalla los ajustes a la garantía mínima de financiamiento establecida por la proposición 98 para la educación de jardín de infantes hasta el segundo año de la educación terciaria.

EL MARCO CONSTITUCIONAL

LA CONSTITUCIÓN ESTATAL EXPONE LAS NORMAS DEL PROCESO PRESUPUESTARIO

El gobernador y los legisladores crean el plan anual de gastos del estado conforme a normas delineadas en la Constitución del estado.

Los votantes de California cambian estas normas periódicamente cuando aprueban enmiendas constitucionales que aparecen en la boleta electoral.

Las propuestas de modificar la Constitución del estado se pueden incluir en la boleta electoral a través de una iniciativa de los ciudadanos o a través de la asamblea legislativa.

Una enmienda constitucional entra en efecto si es aprobada por una mayoría simple de los votantes.

TRES PLAZOS DE VENCIMIENTO CLAVES DEL PRESUPUESTO

DOS EN LA CONSTITUCIÓN DEL ESTADO (10 DE ENERO Y 15 DE JUNIO) UNA EN LA LEY ESTATAL (4 DE MAYO)

El gobernador debe proponer un presupuesto para el año fiscal venidero a más tardar el 10 de enero. El presupuesto debe estar balanceado: Los ingresos públicos estimados (según lo determine el gobernador) deben cubrir o superar los gastos propuestos por el gobernador.

El gobernador debe publicar la revisión de mayo a más tardar el 14 de mayo. La asamblea legislativa debe aprobar un proyecto de ley presupuestario para el año fiscal siguiente a más tardar la medianoche del 15 de junio.

El proyecto de ley presupuestario debe estar balanceado: Los ingresos públicos estimados del fondo general (como se expone en el proyecto de ley presupuestario aprobado por la asamblea legislativa) debe cubrir o superar los gastos del fondo general.

PROPOSICIÓN 25: VOTO POR MAYORÍA SIMPLE PARA LOS PROYECTOS DE LEY PRESUPUESTARIOS Y LA MAYORÍA DE LOS PROYECTOS DE LEY REMOLQUE (TRAILER)

El paquete presupuestario, por lo general, puede aprobarse con un voto de mayoría simple en cada cámara de la asamblea legislativa.

La proposición 25 de 2010 permite a los legisladores aprobar, mediante un voto de mayoría simple, tanto los proyectos de ley presupuestarios como los proyectos de ley complementarios, los cuales pueden entrar en vigor tan pronto como el gobernador los firme.

Conforme a las normas de la proposición 25, los proyectos de ley remolque deben (1) incluirse en la lista de la Ley de Presupuesto y (2) contener una apropiación de cualquier monto.

Incluso con la proposición 25, algunos tipos de proyectos de ley remolque que se podrían incluir en el paquete presupuestario requerirán una supermayoría: generalmente dos tercios del voto de cada cámara. Esto incluye, por ejemplo, los proyectos de ley que aumentan los impuestos o enmiendan una ley estatal que fue aprobada por los votantes mediante una iniciativa en la boleta electoral. Sin embargo, la mayoría de los proyectos de ley remolque en el paquete presupuestario solo necesitarán un voto de mayoría simple para ser aprobados.

PROPOSICIÓN 25: SANCIONES POR ATRASO DEL PRESUPUESTO

Los legisladores enfrentan sanciones si no aprueban el proyecto de ley presupuestario a más tardar el 15 de junio.

La proposición 25 exige que los legisladores pierdan de forma permanente tanto su salario como el reembolso de gastos de viaje y manutención por cada día posterior al 15 de junio que se atrase la aprobación del proyecto de ley presupuestario y su envío al gobernador.

Estas sanciones no se aplican a los proyectos de ley relacionados con el presupuesto, los cuales no están obligados a aprobarse a más tardar el 15 de junio.

PROPOSICIÓN 26: VOTO POR SUPERMAYORÍA PARA LOS AUMENTOS DE IMPUESTOS

Todo aumento de impuestos requiere un voto de dos terceras partes de cada cámara de la asamblea legislativa.

Conforme a la Constitución del estado, “todo cambio en el estatuto estatal que causa que un contribuyente pague impuestos más altos” requiere un voto de las dos terceras partes de cada cámara.

Esta norma fue impuesta por la proposición 26 de 2010. Esta medida expandió la definición de un aumento de impuestos y por lo tanto el alcance del requisito del voto de las dos terceras partes, que fue impuesto originalmente por la proposición 13 de 1978.

Antes de la proposición 26, solo los proyectos de ley que cambiaban los impuestos estatales “para el propósito de aumentar los ingresos públicos” requerían un voto de las dos terceras partes. Los proyectos de ley que aumentaban algunos impuestos pero reducían otros por una cantidad equivalente o mayor podían aprobarse mediante una mayoría simple de votos en cada cámara.

PROPOSICIÓN 26: SE CLASIFICAN MÁS CARGOS COMO IMPUESTOS

La proposición 26 de 2010 también expandió la definición de impuesto para incluir algunas tarifas.

Antes de la proposición 26, los legisladores podían crear o aumentar las tarifas mediante un voto de mayoría simple. Estas tarifas aprobadas por mayoría incluían tarifas regulatorias destinadas a abordar problemas de salud, ambientales u otros causados por diversos productos como el alcohol, el petróleo o los materiales peligrosos.

La proposición 26 reclasificó las tarifas regulatorias y algunas otras como impuestos. Por esta razón, ahora se requiere un voto de las dos terceras partes de cada cámara de la asamblea legislativa para muchos cargos que antes se consideraban tarifas y podían aprobarse por voto de mayoría simple.

REQUISITOS ADICIONALES DE VOTO POR SUPERMAYORÍA

La Constitución estatal requiere un voto de dos terceras partes de cada cámara de la asamblea legislativa para:

Apropiar dinero para el fondo general, excepto para las apropiaciones que son para las escuelas públicas o que se incluyen en proyectos de ley presupuestarios o proyectos de ley remolque (trailer).

Aprobar proyectos de ley que entran en vigencia de inmediato (estatutos urgentes), excepto los proyectos de ley presupuestarios y los proyectos de ley remolque (trailer).

Someter enmiendas constitucionales o medidas de bonos de obligación general a la consideración de los votantes.

Anular el veto del gobernador a un proyecto de ley o a un elemento de gasto específico.

PROPOSICIÓN 54: UN PROYECTO DE LEY SE DEBE PUBLICAR DURANTE POR LO MENOS 72 HORAS ANTES DE QUE LA ASAMBLEA LEGISLATIVA PUEDA ACTUAR EN RELACIÓN A ÉL

La proposición 54 de 2016 requiere que los proyectos de ley se distribuyan a los legisladores y se publiquen en internet, en su formato final, al menos 72 horas antes de ser aprobados por la asamblea legislativa.

Esta norma es aplicable a todos los proyectos de ley, incluso el proyecto de ley presupuestario y otras leyes incluidas en el paquete presupuestario.

Este período de revisión obligatorio se puede eximir para un proyecto de ley si:

El gobernador declara una emergencia en respuesta a un desastre o un peligro extremo, y

Las dos terceras partes de los legisladores en la cámara de representantes que consideran el proyecto de ley votan por renunciar al período de revisión.

PROPOSICIÓN 98: UNA GARANTÍA DE FONDOS PARA LAS ESCUELAS DE JARDÍN DE INFANTES AL DÉCIMO SEGUNDO GRADO Y LAS ESCUELAS TERCIARIAS COMUNITARIAS

La proposición 98 de 1988 garantiza un nivel anual mínimo de fondos para la educación de jardín infantes hasta el segundo año de educación terciaria.

El monto garantizado se calcula cada año en base a una de tres pruebas que se aplican conforme a condiciones fiscales y económicas. Dos de estas pruebas incluyen ajustes por cambios en la asistencia a las escuelas primarias y secundarias en todo el estado. Los fondos de la proposición 98 provienen del fondo general y de los ingresos públicos generados por impuestos locales sobre la propiedad.

La asamblea legislativa puede suspender la garantía por un solo año mediante un voto de las dos terceras partes de cada cámara y proporcionar menos fondos. Después de una suspensión, el estado debe aumentar los fondos de la proposición 98 con el paso del tiempo al nivel que hubiera alcanzado si no se hubiera implementado la suspensión.

Aunque la asamblea legislativa puede proveer más fondos de los que requiere la proposición 98, en general, la garantía a servido como un nivel de fondos máximo.

PROPOSICIÓN 2: AHORROS PARA UN DÍA DE LLUVIA, PAGO DE DEUDAS

La proposición 2 de 2014 revisó las reglas que se aplican a la cuenta de estabilización presupuestaria (BSA, por sus siglas en inglés), el fondo constitucional de “emergencia” del estado, y también estableció un nuevo requisito para reducir la deuda presupuestaria del estado.

El estado está obligado a reservar cada año el 1.5% de los ingresos del fondo general, además de dólares adicionales en los años en que los ingresos tributarios provenientes de las ganancias de capital son particularmente elevados.

Hasta 2029-30, la mitad de estos ingresos se deposita en la BSA y la otra mitad debe utilizarse para reducir la deuda presupuestaria del estado, que incluye pasivos no financiados de pensiones. A partir de 2030-31, la totalidad de la transferencia anual se depositará en la BSA.

Los responsables de formular políticas públicas del estado pueden suspender o reducir el depósito en la BSA y retirar fondos de la reserva, pero únicamente en circunstancias limitadas que califiquen como una “emergencia presupuestaria”.

PROPOSICIÓN 2: UNA RESERVA PRESUPUESTARIA PARA LA EDUCACIÓN DE JARDÍN DE INFANTES HASTA EL SEGUNDO AÑO DE EDUCACIÓN TERCIARIA

La proposición 2 de 2014 también creó una reserva para el presupuesto del estado para las escuelas de jardín de infantes al décimo segundo grado llamada la cuenta de estabilización del sistema de escuelas públicas (Public School System Stabilization Account) (PSSSA).

Los depósitos provienen de los ingresos públicos de los impuestos sobre las ganancias de capital cuando esos ingresos son particularmente elevados.

Sin embargo, se deben cumplir varias condiciones antes de poder transferir estos dólares a la PSSSA. Por ejemplo, las transferencias solo pueden ocurrir en los así llamados años “prueba 1” conforme a la proposición 98, que han sido relativamente infrecuentes.

PROPOSICIÓN 55: FONDOS NUEVOS POTENCIALES PARA MEDI-CAL GRACIAS A UN IMPUESTO A LOS CALIFORNIANOS MÁS PUDIENTES

La proposición 55 de 2016 extiende hasta finales de 2030 los aumentos en la tasa de impuestos sobre la renta personales para los californianos con ingresos muy elevados y establece una fórmula para impulsar los fondos para Medi-Cal, que proporciona servicios de atención médica a los californianos con ingresos bajos.

A partir de 2018-19, los ingresos públicos del fondo general, incluso los obtenidos por la proposición 55, deben usarse primero para financiar (1) la garantía anual de la proposición 98 para las escuelas de jardín de infantes a décimo segundo grado y las escuelas terciarias comunitarias, y (2) el costo de otros servicios que fueron autorizados a partir del 1 de enero de 2016, ajustado según los cambios poblacionales, los mandatos federales y otros factores.

Si queda algún ingreso público de la proposición 55 después de cumplir con estos gastos obligatorios, Medi-Cal recibirá el 50% de este exceso, hasta un máximo de $2 billones en cualquier año fiscal.

La proposición 55 aún no ha generado fondos adicionales para Medi-Cal.

PROPOSICIÓN 4: LÍMITE DE APROPIACIONES ESTATALES (STATE APPROPRIATIONS LIMIT) (SAL): UN LÍMITE PARA LOS GASTOS

Las apropiaciones están sujetas a un límite establecido por la proposición 4 de 1979, según modificada por iniciativas posteriores. Este límite de gastos se suele denominar el límite Gann.

El SAL limita la cantidad de ganancias por impuestos estatales que se puede apropiar cada año. Este límite se ajusta anualmente según los cambios de población y los ingresos personales por persona.

Algunas apropiaciones de las ganancias impositivas no se cuentan para calcular el límite, como los gastos de servicio de las deudas y los gastos necesarios para cumplir con mandatos judiciales o federales.

Los ingresos públicos que superan el SAL durante un plazo de dos años se dividen por igual entre gastos de la proposición 98 y reembolsos a los contribuyentes. El estado superó por última vez el SAL en 2020-21 (pero no lo hizo el año anterior).

MANDATOS ESTATALES: HAY QUE PAGARLOS O SUSPENDERLOS

El estado está obligado a pagar los mandatos que impone a los gobiernos locales o suspenderlos.

La proposición 4 de 1979 exige que el estado reembolse a los gobiernos locales los costos relacionados con un programa nuevo o un nivel más elevado de servicio exigido por el estado.

La proposición 1A de 2004 expandió la definición de un mandato para incluir la transferencia de responsabilidad financiera del gobierno estatal a los gobiernos locales.

La proposición 1A también requiere que el estado suspenda un mandato todo año en el que los costos de los gobiernos locales no se reembolsen por completo.

¿QUÉ HACEN EL GOBERNADOR Y LA ASAMBLEA LEGISLATIVA?

El gobernador:

Aprueba, modifica o rechaza las propuestas de gastos preparadas por los departamentos y agencias estatales mediante un proceso interno coordinado por el Departamento de Finanzas.

Propone cada enero un plan de gastos para el estado, que se presenta ante la asamblea legislativa como el proyecto de ley presupuestario.

Actualiza y revisa el presupuesto propuesto cada mayo (la «Revisión de mayo»).

Firma o veta los proyectos de ley incluidos en el paquete presupuestario.

Puede vetar la totalidad o una parte de las apropiaciones individuales (partidas presupuestarias), pero no puede aumentar ninguna apropiación por encima del nivel aprobado por la asamblea legislativa.

La asamblea legislativa:

Aprueba, modifica o rechaza las propuestas del gobernador.

Puede agregar gastos nuevos o hacer otros cambios que modifican sustancialmente las propuestas del gobernador.

Necesita una voto de mayoría simple de cada cámara para aprobar los proyectos de ley presupuestarios y la mayor parte de los proyectos de ley remolque (trailer).

Necesita un voto de las dos terceras partes para aprobar ciertos otros proyectos de ley que pueden formar parte del paquete presupuestario, como por ejemplo los proyectos de ley que aumentan los impuestos o proponen enmiendas constitucionales.

Necesita un voto de las dos terceras partes de cada cámara para anular el veto del gobernador de un proyecto de ley o apropiación.

¿QUÉ PASA Y CUÁNDO?

CRONOGRAMA DEL PRESUPUESTO ESTATAL

El proceso del presupuesto estatal es cíclico. Se toman decisiones durante todo el año.

Los departamentos y agencias estatales elaboran presupuestos base para mantener los niveles de servicio existentes en el próximo año fiscal y pueden preparar «propuestas de cambio presupuestario» destinadas a modificar esos niveles de servicio. El Departamento de Finanzas (DOF) revisa estos documentos.

Los departamentos y agencias estatales elaboran presupuestos base para mantener los niveles de servicio existentes en el próximo año fiscal y pueden preparar «propuestas de cambio presupuestario» destinadas a modificar esos niveles de servicio. El Departamento de Finanzas (DOF) revisa estos documentos.

De manera independiente del gobernador, los líderes legislativos elaboran sus prioridades presupuestarias para el próximo año fiscal.

En noviembre, la oficina del analista legislativo (LAO) publica su panorama fiscal, que ofrece la evaluación de la LAO sobre los ingresos públicos, los gastos y la situación general del presupuesto del estado a lo largo de varios años fiscales.

A más tardar el 10 de enero

El gobernador publica el presupuesto propuesto para el año fiscal venidero que comienza el 1 de julio.

Enero a mediados de mayo

Unos pocos días después de la publicación del presupuesto propuesto: La oficina del analista legislativo (LAO) publica su panorama general y su evaluación de las propuestas del gobernador y posteriormente divulga una proyección actualizada de los ingresos.

Finales de enero: El comité presupuestario de la cámara de representantes y el comité presupuestario y de revisión fiscal del senado celebran audiencias generales sobre el presupuesto propuesto por el gobernador.

Finales de febrero hasta principios de mayo: Los subcomités presupuestarios de cada cámara celebran decenas de audiencias para revisar en profundidad las propuestas del gobernador.

A más tardar el 14 de mayo

El gobernador publica un presupuesto modificado (la «revisión de mayo») para el próximo año fiscal, que comienza el 1 de julio.

Mediados de mayo a principios de junio

Pocos días después de la revisión de mayo: La oficina del analista legislativo (LAO) publica su panorama general y su evaluación de la revisión de mayo y posteriormente divulga una proyección actualizada de los ingresos y una perspectiva presupuestaria de varios años.

La semana siguiente a la revisión de mayo: Los subcomités presupuestarios de la cámara de representantes y del senado se reúnen para revisar las propuestas del gobernador incluidas en la revisión de mayo.

Aproximadamente 10 días después de la revisión de mayo: La cámara de representantes y el senado publican resúmenes, denominados «informes de subcomité», de sus versiones del paquete presupuestario.

Aproximadamente dos semanas después de la revisión de mayo: Los líderes de la cámara de representantes y del senado llegan a un acuerdo sobre una versión legislativa unificada del paquete presupuestario y publican resúmenes del acuerdo. Durante muchos años, los líderes legislativos convocaron un comité de conferencia compuesto por demócratas y republicanos para resolver las diferencias entre los planes de gastos de ambas cámaras. Sin embargo, no se ha convocado un comité de conferencia desde 2019.

En esta etapa es posible alcanzar un acuerdo completo con el gobernador, aunque es poco frecuente. No obstante, el paquete presupuestario de la asamblea legislativa reflejará muchos puntos de coincidencia con el gobernador, basados en negociaciones continuas y discretas entre el gobernador y los líderes legislativos.

Un poco más de dos semanas después de la revisión de mayo: La legislatura comienza a redactar el proyecto de ley presupuestario inicial, también conocido como la Ley de Presupuesto. La finalización de la Ley de Presupuesto para las votaciones de todos los miembros de la legislatura puede tardar aproximadamente una docena de días.

A más tardar el 15 de junio

La asamblea legislativa aprueba la Ley de Presupuesto antes del 15 de junio, la fecha límite constitucional, y la envía al gobernador.

Si las dos cámaras han programado votos formales de toda la asamblea legislativa para el 15 de junio, la Ley de Presupuesto se debe publicar en el sitioweb de información legislativa de California a más tardar el 12 de junio para cumplir con el requisito de notificación previa de 72 horas.

Si la asamblea legislativa programa votos de toda la asamblea para una fecha anterior al 15 de junio, la Ley de Presupuesto debe imprimirse antes del 12 de junio para cumplir con la norma de las 72 horas, por ejemplo a más tardar el 10 de junio para hacer la votación con todos los miembros el 13 de junio.

No es obligatorio que los proyectos de ley remolque (trailer), que también forman parte del paquete presupuestario estatal, se aprueben a más tardar el 15 de junio, y raramente lo son. En general, los proyectos de ley remolque (trailer) hacen cambios legales necesarios para implementar las políticas públicas que aparecen en la Ley de Presupuesto.

Segunda mitad de junio

El gobernador y los líderes legislativos continúan negociando con el fin de alcanzar un acuerdo tripartito sobre el paquete presupuestario para el próximo año fiscal.

Una vez que se alcanza un acuerdo, se dan a conocer el resto de los proyectos de ley que conforman el paquete presupuestario, los cuales incluyen múltiples proyectos de ley remolque (trailer) junto con un «proyecto de ley presupuestario junior». Este proyecto de ley presupuestario junior modifica la Ley de Presupuesto aprobada por la asamblea legislativa para reflejar los cambios exigidos por el acuerdo alcanzado con el gobernador.

La cámara de representantes y el senado publican resúmenes del paquete presupuestario del modo acordado con el gobernador.

La asamblea legislativa aprueba el proyecto de ley presupuestario junior y los proyectos de ley remolque (trailer).

Todos los proyectos de ley deben ser firmados dentro de los 12 días de su presentación al gobernador. Sin embargo, si el duodécimo día es un sábado, domingo o feriado, el plazo se extiende hasta el siguiente día que no sea sábado, domingo o feriado.

El gobernador puede reducir o eliminar cualquier elemento de apropiación en cualquier proyecto de ley (el “veto de elementos específicos”).

Los departamentos y agencias del estado se enfocan en el siguiente presupuesto estatal comenzando a preparar el presupuesto propuesto del gobernador para publicarlo a más tardar el 10 de enero. Este proceso que dura meses puede comenzar antes en junio y continúa todo el verano y durante el otoño.

Julio y después

El nuevo año fiscal comienza el 1 de julio.

El gobernador firma los proyectos de ley remolque (trailer) restantes que no se firmaron en junio.

El Departamento de Finanzas publica un resumen del paquete presupuestario de junio firmado y convertido en ley por el gobernador. Este resumen puede publicarse antes del final de junio.

La asamblea legislativa entra en un receso de un mes en verano comenzando alrededor del 3 de julio en los años electorales y a mediados de julio en los años no electorales.

La asamblea legislativa vuelve a reunirse en agosto para las semanas de sesión finales, que concluye en agosto en los años con elecciones y en septiembre en los años que no hay elecciones.

En agosto, los líderes del estado típicamente impulsan cambios en el paquete presupuestario estatal adoptados en junio, incluso por lo menos un proyecto de ley presupuestario junior junto con proyectos de ley remolque adicionales. Estos cambios incluyen ajustes técnicos del presupuesto, como la corrección de errores en la Ley de Presupuesto, así como revisiones sustantivas, a menudo de gran alcance, en materia de gastos y políticas públicas.

La cámara de representantes y el senado publican resúmenes de las revisiones presupuestarias conforme al acuerdo alcanzado con el gobernador.

El comité presupuestario en pleno de cada cámara celebra una sola audiencia sobre las revisiones presupuestarias antes de enviar el paquete las cámaras plenas de la cámara de representantes y del senado para las votaciones finales.

El gobernador firma las revisiones presupuestarias y las convierte en ley en septiembre, o a veces en octubre en los años no electorales, posiblemente con ciertos elementos vetados.

Oficina del analista legislativo: Análisis presupuestarios y de políticas públicas, recomendaciones y datos presupuestarios históricos.

Asesor legislativo: Proyectos de ley y análisis de proyectos de ley, un servicio gratuito de seguimiento de proyectos de ley, los códigos estatales y la Constitución del estado.

Asamblea y senado estatal: Programas y otras publicaciones de los comités, cronogramas de sesiones de la asamblea legislativa y de los comités, el calendario legislativo anual y vídeo en vivo y de archivo de los procedimientos legislativos.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

The most common way for Californians to shape state funding decisions and policy priorities is through the state budget process and the legislative (or policy bill) process.

The deadlines for the state budget process are established in California’s Constitution or in state law and rarely change.

In contrast, most of the deadlines for thelegislative process are jointly set by the leadership of the state Senate and Assembly. These deadlines are adjusted annually to reflect the amount of time the Legislature has to complete its business. Specifically:

In non-election (odd-numbered) years, the deadline for the Legislature to pass bills is typically set in September — on a date determined jointly by the Assembly and Senate.

In election (even-numbered) years, the Legislature generally must pass bills by August 31 — a deadline established in the state Constitution. There are a few exceptions to this deadline. For example, after August 31 the Legislature may pass bills calling for elections, bills that would increase or reduce state taxes, and bills that would take effect immediately (“urgency statutes”).

The state budget process and legislative (policy bill) process differ in multiple ways. For example, the legislative process has many more deadlines compared to the state budget process, reflecting the long and linear path that policy bills take through both houses. The legislative process also has more steps and “hoops” to jump through in order to advance legislation to the governor’s desk.

However, there is a key similarity between these two processes. Much of the Legislature’s work on policy bills as well as on the state budget is organized through committees:

In the legislative process, Assembly and Senate policy committees consider the policy implications of a bill, while appropriations committees estimate the cost of policy bills. At each stage of the process, committees can either pass and send policy bills to the floor of each house or hold the bills in committee (where they die).

In the state budget process, Assembly and Senate budget committees and their subcommittees review the governor’s budget proposals, develop each house’s version of the state budget, and pass the budget-related bills that reflect each year’s state budget agreement with the governor.

Committee hearings are open to the public and typically include opportunities for public comment. Members of the public can attend committee hearings in person or watch them online through the Assembly and Senate websites.

The dates in the table below reflect deadlines established in state law and the state Constitution as well as the joint rules set by the Assembly and Senate for 2026.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

What’s the difference between income and wealth? Taxes for individuals and corporations in California? Tax credits and deductions? Understanding these key terms is critical to navigating the state budget and its intersection with California’s tax and revenue system to generate ongoing resources and provide quality education, affordable health care, child care, housing, and other services for communities.

Generally, a tax filer’s total income before deductions. However, some types of income are not included in AGI; for example, income from Social Security and unemployment benefits is not included in California AGI. Additionally, certain “above-the-line” deductions can reduce AGI. Because federal and California law differ in these exclusions and deductions, a tax filer’s federal AGI may not match their California AGI.

Alternative Minimum Tax (AMT)

Certain tax filers must use an alternative calculation of tax liability if they benefit from certain tax expenditures and the tax that they would owe under the alternative method exceeds what they would owe under the regular method. The purpose of the AMT is to ensure that tax filers that take advantage of tax expenditures pay a minimum amount of tax on that preferentially treated income. The California AMT applies to both individual and corporate tax filers, and the federal AMT only applies to individual filers.

Asset

Property owned by an individual or business that is expected to provide a future economic benefit. Examples include financial assets such as stocks and bonds as well as physical assets such as real estate, vehicles, and business equipment.

Capital Gain

Generally, the difference between the value of an asset when sold and when it was originally purchased. California and the federal government generally do not tax the increase in the value of an asset until it is sold; this is sometimes referred to as a capital gain being “realized.” In contrast, an “unrealized capital gain” refers to the increase in value of an asset that has not yet been sold. In California, capital gains are taxed at the same rate as income from employment, whereas at the federal level, they are subject to lower tax rates than employment income.

Corporation Tax

A tax imposed on corporations that do business in or derive income from California — with the exception of insurance companies, which instead pay the insurance tax. This tax is California’s third-largest revenue source. California only taxes the share of a corporation’s net income — revenues less deductions — that is earned in California. This is generally determined by the share of the corporation’s total sales that are attributable to California using a formula known as “single sales factor apportionment.” The corporation tax includes:

The corporation franchise tax, a tax of 8.84% of a corporation’s California net income or an $800 minimum franchise tax, whichever is higher;

The corporation income tax, which is nearly identical to the corporation franchise tax but applied to very few corporations; and

The bank tax, which is an additional 2% rate (for a total of 10.84%) for banks and other financial institutions. These institutions pay the additional rate in place of personal property taxes and all other local business taxes paid by other corporations.

Deduction

A reduction in taxable income (or a reduction in Adjusted Gross Income, in some cases) for certain expenses. Deductions cannot reduce taxable income below zero. Many deductions are available only to tax filers who claim itemized deductions. Because the value of a deduction is based on a tax filer’s tax bracket, and higher-income households are subject to higher income-tax rates, they receive larger savings for each dollar deducted than do lower-income households, which are subject to a lower tax rate.

Dividends

A distribution of a corporation’s profits to its shareholders. Like capital gains, dividends are taxed as ordinary income in California but are subject to lower rates by the federal government.

Earned Income Tax Credit (EITC)

Arefundable tax credit that boosts the incomes of workers with low wages, and that is provided in both federal and California tax law. The credit increases as earnings rise up to a maximum point, after which the credit phases out. California’s Earned Income Tax Credit (CalEITC) is modeled on the federal EITC, but structured differently. California also provides an additional credit for CalEITC-eligible families with children under age 6, the Young Child Tax Credit.

Effective Tax Rate

The percentage of the tax base that is actually paid in tax after taking into account applicable credits, exemptions, deductions, and other tax preferences. Due to these preferences — as well as the graduated rate structure for the personal income tax — the effective tax rate is lower than the statutory or marginal tax rate.

Estate Tax

A tax imposed on someone’s estate, meaning the value of their assets upon their death. In contrast to an inheritance tax, an estate tax is paid by the estate prior to distribution to heirs and other beneficiaries. Currently, the federal government imposes an estate tax on high-valued estates, but California does not impose an estate tax. California voters approved Proposition 6 in 1982, which repealed the state’s existing inheritance tax and prohibited the enactment of future taxes on estates, inheritances, or any transfer occurring upon death. Thus, any proposed estate tax would need to be approved by California voters.

Excise Tax

A tax on the sale of a specific good, such as alcohol, tobacco, or gasoline.

Exclusion

A provision that allows certain types of income to be ignored in tax calculations. For example, California does not require tax filers to include income from Social Security or unemployment benefits in their total income for tax purposes.

Exemption

This can have different meanings in different contexts.

At the federal level, tax filers were able to claim “personal exemptions,” essentially a deduction of a flat dollar amount per tax filer and dependent, prior to 2018. However, the 2017 “Tax Cuts and Jobs Act” suspended personal exemptions through 2025.

California offers “exemption credits,” which are nonrefundable tax credits of a set dollar amount for each tax filer and dependent, with higher amounts for blind individuals, seniors, and dependents.

California law includes many sales tax exemptions, where certain types of items are not subject to the sales tax. The largest of these sales tax exemptions are for food products, prescription medications, and utilities.

Some organizations, such as nonprofit, educational, and religious organizations, can have tax-exempt status, meaning they are generally not subject to corporation taxes.

Filing Status

The category a tax filer belongs to based on their marital status and family structure. One’s filing status affects the applicable income thresholds for each tax bracket, the amount of the standard deduction, and the qualification criteria for some tax expenditures. There are five filing status at both the state and federal levels:

Single

Married filing jointly (also applies to Registered Domestic Partnerships in California)

Married (or Registered Domestic Partnership) filing separately

Head of household

Qualifying widow(er)

Graduated Income Tax

An income tax structure in which the tax rate increases with income, with the first x dollars subject to a low rate, the next y dollars subject to a higher rate, and so on. California has a graduated income tax structure, with rates ranging from 1% to 12.3% — before the application of a 1% surtax on income above $1 million to fund mental health services. This structure, along with tax preferences such as exemptions, deductions, and credits, reduces tax filers’ effective tax rate below their marginal tax rate.

Horizontal Equity

Along with vertical equity, one of the two principles of tax equity. Horizontal equity isthe concept that tax filers with similar economic circumstances should be taxed similarly. For example, under Proposition 13 of 1978, California’s local property tax is based on the inflation-adjusted purchase price of the property rather than its current market value, meaning two tax filers owning properties with the same market value may owe significantly different amounts of tax based on when they purchased the property. This Prop. 13 policy violates the principle of horizontal equity.

Income

Money received over a certain period by an individual, family, or household, such as money from employment, investments, business ownership, and other sources. Income is not equivalent to wealth.

A tax on the value of inherited wealth received by an heir, in contrast to an estate tax, which is applied directly to the decedent’s estate before assets are distributed to beneficiaries. California voters approved Proposition 6 in 1982, which repealed the state’s existing inheritance tax and prohibited the enactment of future taxes on estates, inheritances, or any transfer occurring upon death. Thus, any proposal to reinstate an inheritance tax would need to be approved by California voters.

Insurance Tax

A tax on the premiums received by insurance companies. This tax is paid by insurance companies in lieu of the corporation tax.

Investment Income

Income received from investmenting in assets, including capital gains, dividends, and interest payments.

Itemized Deduction

A deduction for specific types of expenses. Major itemized deductions allowed under California’s tax law include those for mortgage interest, local property taxes, charitable contributions, an employee’s business-related and miscellaneous expenses, and large medical expenses. At both the federal and state levels, tax filers choose between taking a flat standard deduction or itemizing their deductions. Itemizing deductions generally benefits higher-income tax filers most, since they are more likely to have high-value homes — and therefore large expenses for mortgage interest and property taxes — and more likely to donate large sums to charity. However, California law does reduce the amount of itemized deductions allowed for tax filers with federal Adjusted Gross Income above specified thresholds (roughly $200,000 for single filers, $300,000 for heads of household, and $400,000 for joint filers).

Limited Liability Company (LLC)

A type of business that blends corporate and partnership structures and can elect to be taxed as a partnership or as a corporation. LLCs are also required under California law to pay an annual tax of $800 as well as a tiered fee based on income.

Marginal Tax Rate

The rate at which one’s highest increment of income is taxed. Due to California’s graduated income taxstructure, a tax filer’s marginal tax rate is higher than their effective tax rate. For example, under California’s 2021 personal income tax brackets, a single tax filer with a taxable income of $150,000 had a top marginal rate of 9.3%, but they only paid this rate on income above $61,214. The first $9,325 of their income was subject to a 1% rate, then income between $9,325 and $22,107 was subject to a 2% rate, and so on. Due to this tiered rate structure, this tax filer’s effective tax rate would be well below 9.3%.

Nonrefundable Tax Credit

A tax credit that cannot exceed a tax filer’s tax liability, or in other words, cannot reduce tax liability below zero. For example, if a tax filer has a tax liability of $1,500 and would otherwise qualify for a tax credit of $2,000, the credit would be capped at $1,500. This means that tax filers with low incomes who have little to no personal income tax liability often do not fully benefit from these credits. California’s Renter’s Credit and Child and Dependent Care Credit are nonrefundable.

Partnership

A type of pass-through business where the business’ income (or loss) is passed through to its partners. There are two common types of partnerships: limited partnerships, which are required to pay an annual entity-level tax of $800 in California; and general partnerships, which are not required to pay an entity-level tax.

Pass-Through Business

A type of business entity which is not subject to the regular federal or state taxes on corporations, and instead passes income (or losses) through to its owners, who report it on their personal income tax returns. Depending on the type of pass-through business, the entity may also be required to pay an annual tax or fee in California. Pass-through entities include S corporations, partnerships, limited liability companies, and sole proprietorships.

Personal Income Tax

A tax on the income of California residents as well as the income of nonresidents derived from California sources. The tax applies to income from employment, investments, pass-through businesses, and retirement plans. California’s personal income tax has a graduated rate structure that includes nine tax brackets, with rates ranging from 1% on the lowest share of income up to 12.3%. California also levies a 1% surtax on all income above $1 million to fund mental health services. Due to its graduated structure and other features, California’s personal income tax is a progressive tax. The personal income tax is California’s largest source of revenues.

Progressive Tax

A tax which takes up a higher share of income for higher-income households than for lower-income households. California’s personal income tax is a progressive tax.

Property Tax

A tax on real property (land and buildings) and certain types of personal property, including aircraft, watercraft, and business equipment and fixtures. Property taxes remain within the county where they are collected and are allocated among the county government, cities, K-12 schools and community colleges, and special districts based on formulas outlined in state law. While the property tax is a local revenue source, it is governed by provisions put into the state Constitution by Proposition 13 of 1978 and subsequent ballot measures. Under Prop. 13, the general property tax rate is capped at 1% of the assessed value of the property, which for real property is limited to its purchase price plus an annual inflation adjustment not exceeding 2%.

Proportional Tax

Also called a “flat” tax, a tax which takes up the same percentage of income for all households.

Refundable Tax Credit

A tax credit which can reduce a tax filer’s tax liability below zero and provide the difference as a refund. For example, if a tax filer has a tax liability of $1,500 and is eligible for a $2,000 credit, the credit will zero out their tax liability and provide a $500 refund. Because low-income families often have little to no tax liability, a tax credit will only fully benefit these families if it is refundable. The federal Earned Income Tax Credit and California’s Earned Income Tax Credit (CalEITC) and Young Child Tax Credit are refundable.

Regressive Tax

A tax that takes up a larger share of income for lower-income households than for higher-income households. Examples include the sales and use tax and excise taxes.

S Corporation

Formally known as a “Subchapter S corporation,” a type of corporation that is taxed as a pass-through business and has no more than 100 shareholders. State law also requires S Corporations to pay the higher of a $800 minimum franchise tax or 1.5% of its California income.

Sales and Use Tax

A tax on the purchase of tangible goods in California (the sales tax) or on the use of tangible goods in California that were purchased elsewhere (the use tax). The sales and use tax is California’s second-largest revenue source. Services are excluded from the sales and use tax, as are other items exempted by law, including groceries and medications. The sales and use tax is a regressive tax, because lower-income households generally must spend a larger share of their incomes on necessities than higher-income households, so a larger share of their income goes to sales taxes.

A type of pass-through business owned by an individual, or couple, who reports the business’ income on their personal income tax return rather than being subject to corporation taxes.

Standard Deduction

A deduction that tax filers can claim on federal and California tax returns instead of claiming itemized deductions. A standard deduction is a set amount that only varies by filing status. For 2021, the California standard deduction was $4,803 for single filers and married couples filing separately, and $9,606 for married couples filing jointly, heads of household, and qualifying widow(er). These amounts are adjusted annually for inflation.

State and Local Tax (SALT) Deduction

A federal itemized deduction for state and local taxes paid, including property taxes and either income or sales taxes. The federal tax changes of 2017 (the “Tax Cuts and Jobs Act”) limited the deduction any tax filer can take to $10,000 (through 2025). California allows a similar deduction for property taxes and certain other state, local, and foreign taxes, but does not limit the amount of the deduction.

Surtax

An additional tax levied on top of the regular tax structure. For example, California voters approved Proposition 63 in 2004, which created a 1% surtax on taxable income over $1 million to fund mental health services. This is in addition to the tax owed according to the state’s regular personal income tax structure with a top rate of 12.3%, making the combined top tax rate 13.3%.

Tax Avoidance

Legal methods of reducing tax liability (in contrast to tax evasion).

Tax Base

The universe of income, assets, sales, or other economic activity subject to tax. Tax expenditures narrow the tax base, whereas eliminating or limiting tax expenditures broadens the tax base.

Tax Brackets

Ranges of taxable income that are subject to a given tax rate. The brackets vary by filing status; in California’s personal income tax system, the income thresholds for each bracket for couples filing taxes jointly are two times the thresholds for single filers. Additionally, the thresholds are higher for Californians who file as heads of household than for single filers.

Tax Conformity

This term refers to alignment between California’s tax law and the federal tax code. California’s tax law contains many references to federal tax law, but unlike many other states, California does not automatically adopt, or “conform to,” changes to the federal tax code. Instead, the Legislature must take action to incorporate federal tax changes — in part or in whole — into state law. At the time this glossary was published, references in California’s tax law to the federal Internal Revenue Code generally pointed to the federal code as it read on January 1, 2015. However, state policymakers have incorporated into state law selected federal tax changes that occurred after that date.

Tax Credit

A dollar-for-dollar reduction in tax liability for individual or corporate tax filers. Tax credits can be refundable or nonrefundable.

Tax Evasion

Illegal methods of avoiding or reducing taxes, such as deliberate non-payment or underpayment.

Tax Expenditure

Refers to exceptions to “normal tax law” that reduce the revenue governments would otherwise collect. These exceptions include, but are not limited to, exemptions, deductions, exclusions, tax credits, deferrals, elections, and preferential tax rates. Tax expenditures can be commonly referred to as tax breaks, tax loopholes, or tax preferences.

Tax Liability

The amount of tax owed. Tax credits can reduce tax liability; nonrefundable tax credits cannot reduce tax liability below zero, but refundable tax credits can.

Tax Rate Schedule

A table indicating the tax rates that apply to each interval of taxable income. California’s personal income tax has three tax rate schedules, which tax filers with taxable income above $100,000 must use to determine their tax liability: “Schedule X” applies to single filers and married/Registered Domestic Partnership couples filing separately; “Schedule Y” applies to married/Registered Domestic Partnership couples filing jointly and qualifying widow(er)s; and “Schedule Z” applies to head of household filers. Filers with taxable income of $100,000 or less consult a tax table to determine their state personal income tax liability instead of using the tax rate schedule.

Tax Table

A table that California tax filers with taxable incomes of $100,000 or less use to look up the amount of their state income tax liability. In contrast to California’s tax rate schedules — which include precise tax liability calculations — the tax table assigns one rounded tax amount to filers of a given filing status with taxable incomes within intervals of approximately $100.

Taxable Income

The result of subtracting a tax filer’s standard deduction or itemized deductions from their Adjusted Gross Income. A filer’s tax liability is determined by applying the applicable tax rates to their taxable income.

Vertical Equity

Along with horizontal equity, one of the two types of equity considered when evaluating tax policies. While horizontal equity is concerned with tax filers with similar economic circumstances, vertical equity is concerned with the distribution of taxes across the tax filers of different income levels. Progressive taxes are considered to be vertically equitable because they make up a largest share of income for the highest-income tax filers, who have the greatest ability to pay.

Wealth

The value of the resources that an individual, family, or household owns. Wealth is often measured by net worth, which is the sum of the value of all assets minus all liabilities, or debts, like money owed on loans.

Every year, California’s governor and Legislature adopt a state budget that provides a framework and funding for critical public services and systems — from child care and health care to housing and transportation to colleges and K-12 schools.

But the state budget is about more than dollars and cents. The budget expresses our values as well as our priorities for Californians and as a state. At its best, the budget should reflect our collective efforts to expand economic opportunities, promote well-being, and improve the lives of Californians who are denied the chance to share in our state’s wealth and who deserve the dignity and support to lead thriving lives.

State budget choices have an impact on all Californians. These decisions affect the quality of our schools and health care, the cost of a college education, families’ access to affordable child care and housing, the availability of services and financial support to help older adults age in place, and so much more.

Because the state budget touches so many services and our everyday lives, it is critical for Californians to understand and participate in the annual budget process to ensure that state leaders are making the strategic choices needed to allow every Californian — from different races, backgrounds, and places — to thrive and share in our state’s economic and social life.

This report sheds light on the state budget and the budget process with the goal of giving Californians the tools they need to effectively engage decision makers and advocate for fair and just policy choices.

Key Takeaways

The Bottom Line

The state spending plan is about more than dollars and cents.

Crafting the budget provides an opportunity for Californians to express our values and priorities as a state.

The state Constitution establishes the rules of the budget process.

Among other things, these rules allow lawmakers to approve spending with a simple majority vote, but require a two-thirds vote to increase taxes. Voters periodically revise the budget process by approving constitutional amendments.

The governor has the lead role in the budget process.

Proposing a state budget for the upcoming fiscal year gives the governor the first word in each year’s budget deliberations.

The May Revision gives the governor another opportunity to set the budget and policy agenda for the state.

Veto power generally gives the governor the last word.

The Legislature reviews and revises the governor’s proposals.

Lawmakers can alter the governor’s proposals and advance their own initiatives as they craft their version of the budget prior to negotiating an agreement with the governor.

Budget decisions are made throughout the year.

The public has various opportunities for input during the budget process.

This includes writing letters of support or opposition, testifying at legislative hearings, and meeting with officials from the governor’s administration as well as with legislators and members of their staff.

In short, Californians have ample opportunity to stay engaged and involved in the budget process year-round.

Key Facts About California’s State Budget

The State Budget = State Funds + Federal Funds

Three Kinds of State Funds

Three kinds of state funds account for almost two-thirds (64.8%) of California’s $495.6 billion budget for 2025-26, the fiscal year that began on July 1, 2025. Specifically:

General Fund — The state General Fund accounts for revenues that are not designated for a specific purpose. Most state support for education, health and human services, and state prisons comes from the General Fund.

Special Funds — Over 500 state special funds account for taxes, fees, and licenses that are designated for a specific purpose.

Bond Funds — State bond funds account for the receipt and disbursement of general obligation (GO) bond proceeds.

Federal funds comprise the rest (35.2%) of the state’s 2025-26 budget.

Most State General Fund and Special Fund Revenue Comes From Three Sources

California’s “big three” taxes

Most state revenue comes from California’s “Big Three” taxes. In 2025-26, General Fund and special fund revenue combined is estimated to total $296.7 billion, with almost 73% ($215.8 billion) expected to come from the Big Three. California’s Big Three taxes are the:

Personal income tax — This is a tax on the income of California residents as well as the income of nonresidents derived from California sources. It is California’s largest source of revenue.

Sales & use tax — This is a tax on the purchase of tangible goods in California (the sales tax) or on the use of tangible goods in California that were purchased elsewhere (the use tax). Services are excluded from the sales and use tax, as are other items exempted by law, including groceries and medications. The sales and use tax is California’s second-largest source of revenue.

Corporation tax — This is a tax imposed on corporations that do business in or derive income from California, with the exception of insurance companies, which instead pay the insurance tax. The corporation tax is California’s third-largest source of revenue.

Other state revenue is estimated to make up more than one-quarter (27.3%) of total projected General Fund and special fund revenue in 2025-26. This other revenue comes from a broad range of sources, including taxes, fees, and fines.

The State Budget is a Local Budget

Dollars spent through the state budget go to individuals, communities, and institutions across California. Under the enacted 2025-26 state budget:

Four-fifths of total spending (80.6%) flows as “local assistance” to K-12 public schools, community colleges, families enrolled in the CalWORKs program, and other essential state services and systems that are operated locally.

Nearly one-fifth of total spending (17.9%) goes to 23 California State University campuses, 10 University of California campuses, over 30 state prisons, and other recipients of “state operations” dollars.

Less than 2% of total spending flows as “capital outlay” dollars, supporting infrastructure projects across California. (Local assistance and state operations dollars also fund infrastructure.)

State Funds Primarily Support Health and Human Services or Education

Under the enacted 2025-26 state budget:

Almost 3 in 4 General Fund and special fund dollars support three categories of spending: health and human services (42%), K-12 education (25.1%), and higher education (7.2%).

More than 5% of General Fund and special fund dollars go to corrections, primarily the state prison system.

The balance of these dollars supports other essential services (such as transportation and environmental protection) and institutions (such as the state’s court system).

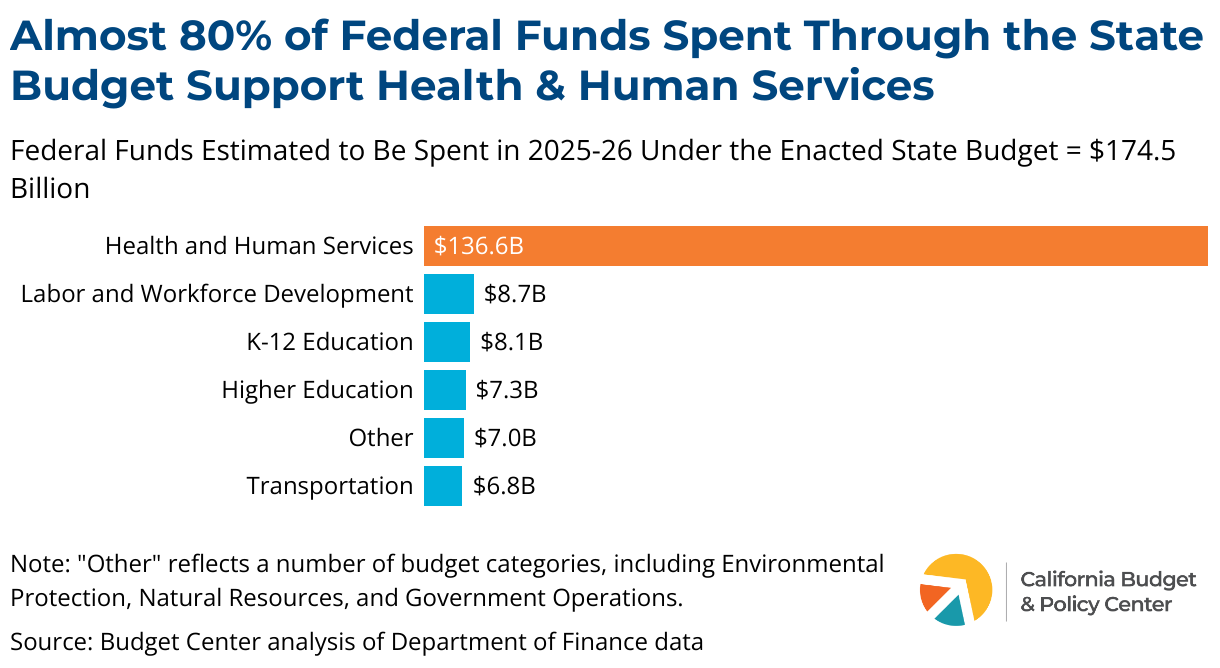

Federal Funds Primarily Support Health and Human Services

Under the enacted 2025-26 state budget:

Nearly four-fifths of federal dollars (78.3%) support health and human services programs.

The balance of federal dollars supports other essential services, including labor and workforce development, K-12 education, higher education, and transportation.

The State Budget is Part of a Package of Bills

The state budget never stands alone. Instead, it moves as part of a package of legislation that typically includes two to three dozen bills, and sometimes many more — particularly in years when there is a budget shortfall and state leaders need to make multiple changes to balance the budget. In 2025, Governor Newsom signed nearly 50 budget-related bills.

four kinds of budget-related bills

The budget package consists of two types of budget bills along with trailer bills and other budget-related legislation.

Budget Act — The state budget is formally known as the Budget Act. The Budget Act is the initial budget bill passed by the Legislature and signed into law by the governor. In general, budget bills:

Provide authority to spend money (“appropriations”) across an array of public services and systems for a single year.

Move through the Legislature’s budget committees on their own timeline.

Budget Bill Juniors — This is the informal term for any budget bill that amends the Budget Act, such as by increasing or reducing authorized expenditures. There is no limit on the number of Budget Bill Juniors that may be included in a budget package. This means state leaders can revise the Budget Act as many times as they wish by passing additional budget bills.

Trailer bills — The state budget package also includes trailer bills. Trailer bills generally make changes to state law related to the Budget Act and, like budget bills, move through the Legislature’s budget committees. In addition, trailer bills:

Must contain at least one appropriation and be listed in the Budget Act — a requirement that directly links trailer bills to the state budget.

Are organized by major policy areas in the budget. For example, health-related changes would be included in a “health” trailer bill, housing-related changes would be included in a “housing” trailer bill, etc.

Other budget-related bills — Other bills may be included in the budget package from time to time. These are bills that move independently of the Budget Act (and therefore are not trailer bills) but are still considered part of the state budget framework. This could include, for example, legislation to increase taxes or to place constitutional amendments before the voters as well as bills passed in a special session of the Legislature. This other budget-related legislation can move either through the Legislature’s policy committees or through budget committees.

Assembly Budget Committee and Senate Budget & Fiscal Review Committee

Review the governor’s budget proposals and develop each house’s version of the state budget. Most budget committee work is done through subcommittees that focus on specific policy areas.

Budget Act

The initial budget bill passed by the Legislature and signed into law by the governor, after any line-item vetoes. The Budget Act can be referred to by the year in which it becomes law (“Budget Act of 2026”) or by the fiscal year to which it applies (“2026-27 Budget Act”).

Budget Bill Jr.

The informal term to describe any budget bill that amends the Budget Act. Budget Bill Jrs. may be numbered sequentially using Roman numerals (e.g., Budget Bill Jr. I, Budget Bill Jr. II, etc.).

Budget-Related Bills (“Trailer Bills”)

Generally make changes to state law related to the Budget Act. These bills are formally known as “bills … related to the budget bill,” but are more commonly called “trailer bills.” Trailer bills are listed in the Budget Act and move through the Assembly and Senate budget committees. Trailer bills are organized by issue area, such as “health,” “housing,” “higher education,” and “public safety.”

From time to time, bills that move independently of the Budget Act — and therefore are not trailer bills — may be considered part of the overall state budget framework. This could include, for example, legislation to increase taxes or to place constitutional amendments before the voters.

Department of Finance (DOF)

Leads the development of the governor’s budget proposals, prepares the governor’s budget documents, testifies on behalf of the governor at legislative budget hearings, develops the governor’s economic forecasts, and performs several other functions. The DOF’s director is the governor’s chief fiscal adviser.

Governor’s Budget Summary

Provides the governor’s economic and revenue outlook, highlights major policy initiatives in the governor’s proposed budget, and summarizes proposed state expenditures. The budget summary is released on or before January 10.

Governor’s Proposed Budget

Provides a detailed overview of the governor’s proposed expenditures for the upcoming fiscal year, estimated expenditures for the current fiscal year, and actual expenditures for the prior fiscal year. The proposed budget is released on or before January 10.

Legislative Analyst’s Office (LAO)

An independent, nonpartisan office that conducts research and analysis on state budget issues, analyzes statewide ballot measures, and provides fiscal and policy advice to the Legislature. The LAO is overseen by the Legislature’s bipartisan Joint Legislative Budget Committee.

Line-Item Veto

The governor’s power to reduce or eliminate specific items of appropriation while approving other portions of a bill. This power applies to any bill that contains an appropriation, including budget bills and budget-related bills. The Legislature may override a line-item veto with a two-thirds vote of each house.

May Revision