Even before the COVID-19 pandemic, unaffordable housing costs represented one of California’s most pressing challenges – and the job losses triggered by stay-home orders necessary to address the public health emergency threaten to exacerbate this long-standing crisis. Housing affordability is a problem throughout the state when housing costs are compared to incomes, and the Californians who are most affected by the affordability crisis are renters, households with the lowest incomes, people of color, and immigrants. Many of these same Californians are also especially hard hit by the economic effects of the COVID-19 public health crisis. Policy solutions that particularly address the needs of these households represent a promising approach to tackling the state’s housing crisis strategically, with a focus on those most deeply affected. The current pandemic highlights the urgency for strategies to eliminate unjust disparities in who is burdened by unaffordable housing, including racial inequities in housing affordability.

Among the key findings based on the most recent data available from 2018:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

https://youtu.be/1bks1DvdSIs

Even before the COVID-19 pandemic, unaffordable housing costs represented one of California’s most pressing challenges – and the job losses triggered by stay-home orders necessary to address the public health emergency threaten to exacerbate this long-standing crisis. Housing affordability is a problem throughout the state when housing costs are compared to incomes, and the Californians who are most affected by the affordability crisis are renters, households with the lowest incomes, people of color, and immigrants.

This video is part of our Policy Perspectives Speaker Series.Thank you to our 2020 series sponsors: First 5 California, First 5 LA, and the Stupski Foundation, for making this programming possible.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

On a given night, more than 150,000 Californians are homeless. These individuals face significant risk of exposure to COVID-19 and serious barriers to following stay home orders to limit the spread of infection. Due to older ages and high rates of physical health conditions, they are also at high risk of severe complications or even death from the virus. Black Californians are greatly overrepresented among homeless individuals, making their health especially endangered by COVID-19. Policymakers should make sure the urgent housing and health needs of Californians who are homeless are met, to protect their health and the broader public health and to address racial health disparities exacerbated by this pandemic.

Nearly 3 in 4 Californians experiencing homelessness are unsheltered– living on the street, in cars, or in other places not meant for habitation. Lack of proper housing makes it impossible for these individuals to follow stay home orders or even practice basic hygiene, such as washing their hands.

Social distancing and self-quarantine are also a challenge for Californians staying in emergency shelters and transitional housing, due to shared sleeping, eating, bathroom, and living spaces.

The lack of housing and inability to consistently follow public health recommendations puts Californians who are homeless at greater risk of contracting COVID-19. This also hinders statewide efforts to stop the virus from spreading.

Older adults are at high risk of developing severe health complications from COVID-19. According to the US Centers for Disease Control and Prevention (CDC), adults age 50 and over have the highest rate of hospitalization due to COVID-19 — and those age 55 and older accounted for 92% of provisional COVID-19 deaths as of April 21, 2020.

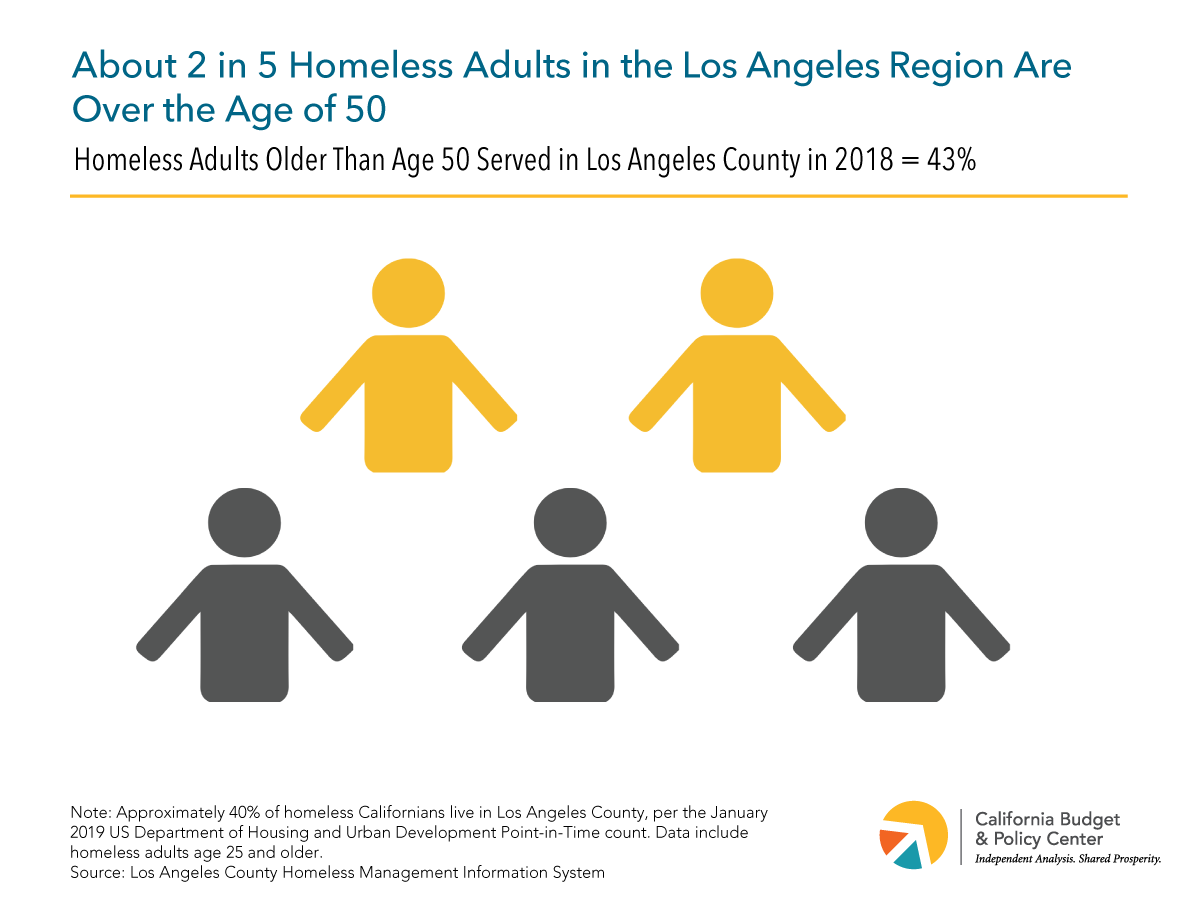

Even prior to the pandemic, the aging of the homeless population meant that older adults are now – and will continue to increasingly be – a large portion of Californians experiencing homelessness. In Los Angeles County, about 2 in 5 homeless adults are older than 50.

Further, homeless individuals demonstrate rates of illnesses and geriatric conditions on par with or higher than adults with stable housing who are 20 years older, increasing their risk of complications from COVID-19.

People with chronic health conditions also tend to have worse COVID-19 outcomes. A preliminary study by the CDC found that adults with COVID-19 who had at least one underlying health condition or risk factor were significantly more likely to require hospitalization or ICU admission, compared to those who did not.

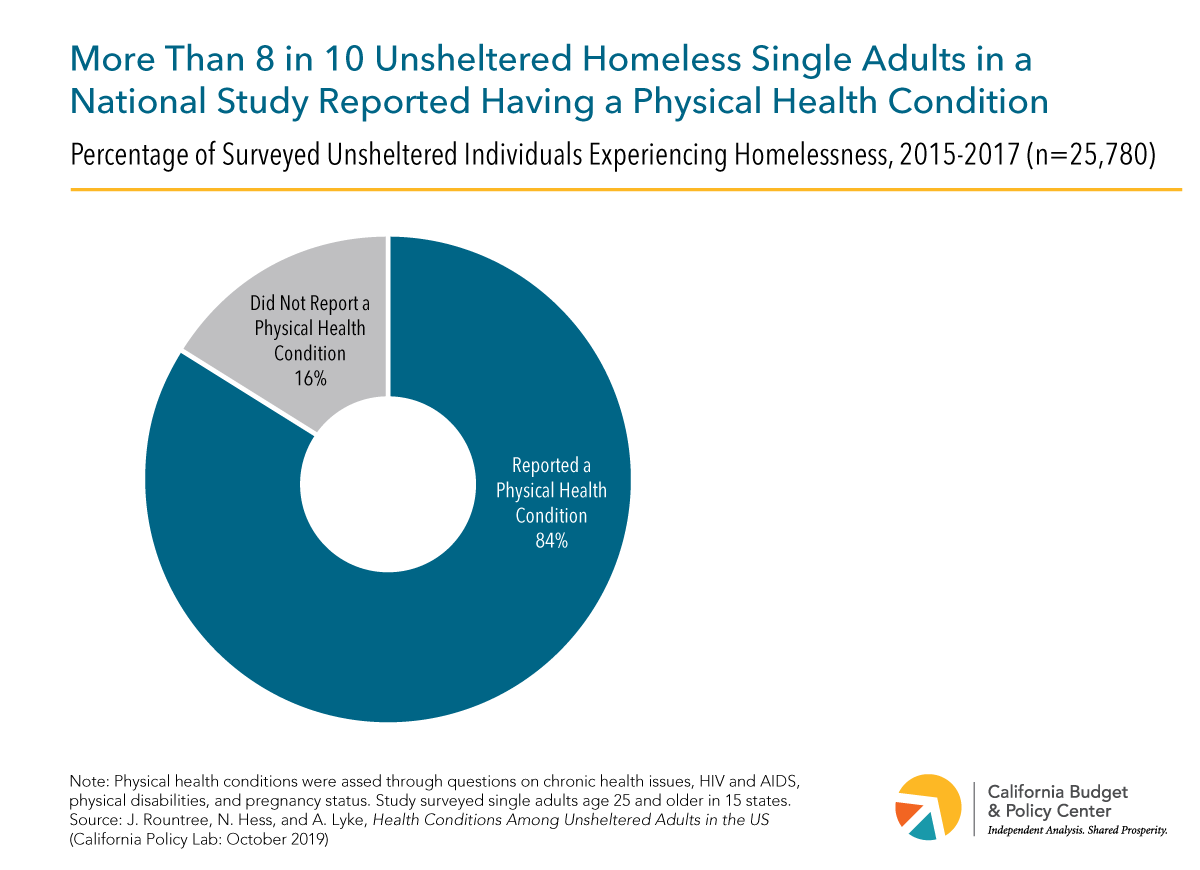

In addition, experiencing homelessness exacerbates existing health conditions and can lead to new ones, such as chronic illnesses and infectious and communicable diseases. In a national study of homeless single adults, more than 8 in 10 unsheltered individuals (84%) reported having at least one physical health condition.

Racial disparities linked to current and past discriminatory policies and practices are startlingly apparent in Black Californians’ overrepresentation both within the homeless population and among severe health outcomes and deaths related to COVID-19.

While Black Californians only comprise 6% of the state population, nearly 1 in 3 individuals experiencing homelessness are Black, and therefore face high risk of COVID-19 exposure and significant barriers to preventing and addressing infection.

Black Californians accounted for 12% of COVID-19 related deaths statewide as of April 19, 2020 — double their share of the state population. In Los Angeles County, where 1 in 11 residents (9%) are Black, they have accounted for 1 in 6 deaths (16%) due to COVID-19 as of April 18, 2020.

Federal and state policymakers have taken initial steps to address the needs of Californians experiencing homelessness during the COVID-19 crisis, such as providing support to house some individuals in hotels and allocating funds to local jurisdictions to address local homeless services needs. This support for individuals without a permanent home will be needed as long as the pandemic lasts. It is also critical to ensure that Californians at high risk of severe COVID-19 health outcomes – including older adults and individuals with chronic health conditions – do not fall into homelessness. Strong interventions are also important to avoid further exacerbating the disproportionate burdens of homelessness and COVID-19 among Black Californians. Given the high risk and devastating consequences for both individuals’ health and broader public health efforts, policymakers should prioritize the urgent COVID-19 health and housing needs of homeless Californians, while taking steps to address the state’s long-term homelessness challenges and racial health disparities.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Housing costs vary substantially throughout California, with the highest costs in coastal urban areas and the lowest costs in inland rural areas. But incomes also vary regionally, and areas with relatively lower housing costs also tend to have lower typical incomes. The result is that housing affordability is clearly a problem throughout the state when housing costs are compared to incomes. Across every region of California, from the high-cost San Francisco Bay Area and Los Angeles and South Coast to the lower-cost Central Valley and Far North, at least a third of households spent more than 30% of their incomes toward housing in 2018, and as many as 1 in 5 spent more than half of their incomes on housing costs.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Supplemental Security Income/State Supplementary Payment (SSI/SSP) grants are a critical source of income for well over 1 million California seniors and people with disabilities who have low incomes and need help paying for basic necessities, such as housing. Grants are funded with both federal (SSI) and state (SSP) dollars. The maximum monthly grant for an individual is about $944, which consists of an SSI grant of $783 and an SSP grant of $160.72.

To help close budget shortfalls during the Great Recession, the state made deep cuts to the SSP portion, reducing it from $233 per month in early 2009 to $156.40 per month by mid-2011. State policymakers increased the SSP grant by $4.32 per month starting in January 2017. However, no additional state grant increases have been provided since then, and the Governor’s proposed 2020-21 state budget assumes the SSP portion will remain frozen for another year.

Because state cuts largely remain in place, SSI/SSP recipients have less money to meet their basic needs, including housing. This is particularly concerning in light of California’s high housing costs. In all 58 California counties, the “Fair Market Rent” (FMR) for a studio apartment exceeds 50% of the maximum SSI/SSP grant for an individual. Moreover, the studio FMR exceeds the entire grant in 22 counties. People are at greater risk of becoming homeless when housing costs account for more than half of household income.

Senate Bill 13, as amended in the state Assembly on August 12, 2019, would help to facilitate the development of accessory dwelling units (ADUs) and provide amnesty for unpermitted ADUs to become compliant. SB 13 may have housing- and income-related health impacts on both homeowners and tenants. This review finds:

strong evidence that easing restrictions on the development of ADUs provides incentives for homeowners to build ADUs and, as a result, increases the supply of permanent housing.[1]

a fair amount of evidence that ADUs are affordable within the neighborhood where they are located, but may not be a viable housing option for lower-income residents in the absence of government incentives.[2]

a fair amount of evidence that rent from ADUs provides homeowners with additional income to maintain their properties, sustain their mortgages, and increase disposable income.[3] There is a fair amount of evidence that seniors (age 65+) do not own or live in ADUs at higher rates than other age groups;[4] instead, there is a concentration of ownership among middle-aged adults.[5]

a fair amount of evidence that infill development in higher-income areas could increase the social and economic diversity of neighborhoods, providing more residents with access to better services.[6]

a fair amount of evidence that an amnesty program for unpermitted ADUs encourages landlords to bring units into compliance with permitting requirements, but it is not well researched if this results in health- and safety-related improvements in units with unhealthy or unsafe conditions.[7] The impact of an amnesty policy on rents is not well researched.

What Is the Goal of the Health Note?

Policy decisions made outside of the public health and health care sectors, such as in education, land use, or criminal justice, can affect health and well-being. HealthNotes are intended to provide objective, nonpartisan information to help legislators understand the connections between these sectors and health. Health Notes are not intended to make definitive or causal predictions.

The California Budget & Policy Center selected SB 13 as an illustrative example to demonstrate potential health impacts of proposed legislation. Developing ADUs to increase the supply of housing has been cited by housing advocates and housing policy researchers as a potentially important strategy in California.

What Are the Potential Health Impacts of SB 13?

There are many ways in which housing and where one lives may influence health. For instance, housing affordability, the conditions in neighborhoods and communities, and the physical conditions within homes all affect individual health outcomes.[8] SB 13 aims to facilitate the development of ADUs and encourage landlords with unpermitted ADUs to become compliant. In doing so, this bill could help to provide more affordable housing options for renters, provide additional income for homeowners who build ADUs, increase renters’ access to well-established resource areas — higher-income neighborhoods — and improve the physical conditions of unpermitted ADUs that become compliant.

Both renters and homeowners may benefit from the development of ADUs by helping to lower their cost of living. Given that ADUs are often seen as affordable housing options for renters, particularly in urban areas, increasing the supply of ADUs may allow renters to spend less on housing.[9],[10] Homeowners who build and rent ADUs could also benefit from additional income support. Research shows that families that experience difficulty paying their rent, mortgage, or utility bills are more likely to lack a sufficient food supply and are less likely to have a consistent source of medical care.[11] Difficulty paying rent or mortgage is also a marker of housing instability and may lead to food insecurity and homelessness.[12] Therefore, this bill could lead to a change in income-related health outcomes for renters and homeowners, including a decrease in chronic health conditions and mental health conditions such as stress and anxiety.

Furthermore, given that access to affordable housing is a problem that disproportionately affects low-income households, and that the majority of individuals with high housing cost burdens in California are people of color, the development of more affordable housing options could help to address health inequities based on race and ethnicity.[13]

Building more ADUs could help with housing affordability even if the ADUs themselves are not considered to be affordable units. The development of ADUs could lead to an increase in the supply of housing, which could potentially reduce the cost of housing in the overall market. More specifically, it could be expected to slow the rate of increase in the cost of housing compared to the increase expected without adding those units to the housing supply.

ADUs could be particularly beneficial for middle-aged and elderly homeowners by allowing them to more easily remain in their homes as they transition into fixed or reduced incomes towards the end of their lives. Research demonstrates that “aging in place” significantly reduces stress and improves mental health among seniors.[16] The income from renting out either an ADU or the main house could help older adults achieve the financial stability needed to age in place, thereby allowing them to stay near their established networks and decreasing the risk of isolation and depression.[17] ADUs could also be beneficial for seniors because they can be built with ADA accessibility standards to allow easy mobility throughout the home.

If ADUs are developed in well-established resource areas, they could improve opportunities for renters to be healthy. Research suggests that people living in lower-income areas rate their own health lower than those living in higher-income neighborhoods.[18] In addition, low-income neighborhoods contribute to higher rates of obesity and chronic disease due to many factors, including a higher density of fast food restaurants, decreased accessibility to fresh foods, and environments that are not conducive to physical activity.[19] Building ADUs in well-established resource areas could help to increase access to the amenities that are often found in these areas, such as higher-performing and better-funded schools, better police protection, and transit stations. Furthermore, ADUs could help to increase social equity — defined as ensuring that social services are delivered fairly and equitably to all social groups.[20] Social equity also reflects the notion that increasingly diverse populations are the foundation for a more creative and more tolerant society.[21]

By providing amnesty to owners of unpermitted ADUs, this bill may help to achieve a higher level of housing quality, which would promote good physical and mental health.[22] Research shows that poor conditions are associated with various negative health outcomes, such as injury, chronic disease, and poor mental health.[23] Features of poor housing conditions include a lack of air conditioning, inadequate plumbing, and/or exposure to hazards such as carbon monoxide, allergens, and lead in paint, pipes, and faucets.[24] People living in units with poor housing conditions may be more likely to be exposed to damaged appliances, exposed nails, or peeling paint, which could lead to illness or injury.[25] Waiving certain fees and penalties may help to provide a pathway for unpermitted ADUs to meet health and safety standards that would be less harmful to an occupant’s health.

Why Do These Findings Matter for California?

The high cost of housing and lack of affordable housing are among the primary drivers of California’s high poverty rate, ranked first among the 50 states under the Supplementary Poverty Measure.[26] The high costs disproportionately affect renters and households with low incomes.[27] More than half of renters are “cost burdened,” meaning they pay more than 30% of income toward housing.[28] Eight in 10 households with incomes below 200% of the federal poverty line were housing cost burdened in 2017.[29] Additionally, more than 2 in 3 Californians who struggle to afford housing are people of color.[30] High costs are in part driven by the shortage of rental housing.[31]

As the state continues to debate policy solutions to improve housing affordability, encouraging the development of ADUs may be an effective strategy to increase the supply of housing because it allows homeowners to increase the number of available units without requiring direct government investments in large development projects.[32] Compared to other forms of low-income and affordable housing, studies show that ADUs are relatively inexpensive to build. The Terner Center for Housing Innovation at UC Berkeley found that costs to build ADUs in the cities of Portland, Oregon, Seattle, and Vancouver were low because they did not include land costs and construction duration is short.[33]

Recent state legislation by Senators Wieckowski and Bloom in 2016 and 2017 helped to facilitate the development of ADUs by requiring cities to limit parking requirements, eliminate some utility connection fees, and streamline review and approval processes.[34] San Diego had 17 ADU applications in 2016, which increased to 64 in 2017. [35] Similarly, Oakland saw an increase in the number of applications received from 99 in 2016 to 247 in 2017.[36] Los Angeles had the largest increase, receiving 80 ADU applications in 2016 and 1,980 through November of 2017.[37] Still, remaining barriers prevent further proliferation. Burdensome development fees and building codes continue to inhibit the construction of ADUs.[38] For example, the Terner Center survey of Portland, Seattle, and Vancouver found that city permits and utility connections accounted for over 10% of construction costs.[39]

What Are the Potential Effects of SB 13 on the Supply of Permanent Housing?

There is strong evidence that easing restrictions on the development of ADUs provides incentives for homeowners to build ADUs and, as a result, increases the supply of permanent housing.[40]

Studies analyzing the effect of easing strict land-use regulations on the development of ADUs conclude that incentives are an effective policy tool to increase the supply of such units. In 2010, Portland, Oregon waived development fees covering sewer, water, and other infrastructure connections, reducing costs by $8,000 to $11,000 per unit.[41] In 2013, the city received almost 200 ADU applications, six times more than the yearly average from 2000-2009.[42]

A recent study found that localities in California with the least restrictive laws regulating ADUs were 67% more likely to receive frequent applications than localities with restrictive laws.[43] This study found that localities without off-street parking requirements were much more likely to receive monthly applications.[44] Another study analyzing single family lots within half a mile of five Bay Area Rapid Transit (BART) stations in the cities of Berkeley, El Cerrito, and Oakland estimated that 2,149 potential ADUs could be constructed if cities had less stringent lot-size, parking, and setback requirements than under the zoning laws at the time.[45]

The Terner Center survey of Portland, Seattle, and Vancouver found that 60% of ADUs were used for permanent housing, compared to 12% for short term rentals.[46] Results from another study in Oregon showed that about 82% of respondents used ADUs as someone’s permanent residence, which is similar to an analysis conducted in 2011 in the East Bay Area, where 85% of owners reported using ADUs as long-term housing.[47]

What Are the Potential Effects of SB 13 on the Supply of Affordable Housing?

There is a fair amount of evidence that ADUs are affordable within the neighborhood where they are located, but may not be a viable housing option for lower-income residents in the absence of government incentives.[48]

Some research finds that ADUs offer affordable rents, in part because of their smaller unit size, and that they often rent at below market rates. [49] The Terner Center study of Portland, Seattle, and Vancouver found that 58% of homeowners reported renting below market rate.[50] Similarly, a study in the East Bay Area concluded that average rents of ADUs were affordable to households earning at or below 62% of area median income. (Many ADUs included in this study were unpermitted, which may have decreased rents.[51]) In contrast, a study conducted in Portland, Oregon found that about 80% of ADUs were rented at market rate or sometimes even at a premium compared to apartments of similar size and location.[52]

Interwoven with the shortage in housing supply is the need to provide low-income housing to the state’s most financially strained residents. There is mixed evidence that permitted ADUs house low-income households, despite localities’ ability — since 2002 — to count ADUs as low-income housing for the Regional Housing Needs Assessment.[53]

Additional policies could guarantee that newly built ADUs have affordable rents. Research by Ramsey-Musolf finds that unless a local zoning code regulates an ADU’s maximum rent, occupancy income, and/or effective period, then the city or state will be unable to ensure that units are available to people with low income.[54] One strategy implemented in Los Angeles, through The Backyard Homes Project, provides owners with support through technical assistance and financing in return for agreeing to rent their ADUs to households using subsidized housing vouchers.[55] Another example is the city of Pasadena, which reduces permit fees from roughly $20,000 to $1,000 per unit if homeowners agree to a seven-year rent restriction.[56]

What Are the Potential Effects of SB 13 on Housing Stability for Homeowners and Seniors?

There is a fair amount of evidence that rent from ADUs provides homeowners with additional income to maintain their properties, sustain their mortgages, and increase disposable income.[57] There is a fair amount of evidence that seniors (age 65+) currently do not own or live in ADUs at higher rates than other age groups;[58] instead, there is a concentration of ownership among middle-aged adults.[59]

While more research is needed to better understand the social-economic breakdown of homeowners who are able to build ADUs, available information suggests that ADUs can provide additional income support. Research shows income received from rent is a major factor prompting homeowners to build ADUs. Building an ADU to have an extra source of income was the number one reason for initiating construction of an ADU, according to a recent Terner Center survey.[60] Furthermore, a study in Seattle found that 64% of respondents said they built ADUs for extra income, 53% to reduce house payments, and 47% to increase home value.[61]

It is often cited that ADUs can provide seniors with the ability to age in place, extend their independence, and allow caretakers to live in proximity. However, research over the past few decades has consistently shown that seniors do not own or live in ADUs at higher rates than other age groups.[62] Major barriers for seniors include the hardships entailed in construction, renting, and maintaining ADUs as well as reluctance to take on debt.[63],[64]

As the population of ADU owners ages, there may be a significant increase in the percentage of seniors who own ADUs and could benefit by living-closer to family, housing a caretaker, receiving additional income from rent, or downsizing. A survey in Oregon found that about 30% of ADU owners were 55 to 64 years old and nearly 23% were 45 to 54 years old. In contrast seniors (65+) accounted for 20% of homeowners in the areas surveyed.[65] Furthermore, opinion polls show that as many as 70% to 80% of Baby Boomers express a preference for aging in place.[66] Therefore, while seniors do not currently own or occupy ADUs at especially high rates, middle-aged adults do, and they could benefit from owning ADUs when they become seniors.

What Are the Potential Effects of SB 13 on Access to Neighborhood-Based Resources?

There is a fair amount of evidence that infill development in higher-income areas could increase the social and economic diversity of neighborhoods, providing more residents with access to better services.[67]

Research shows that when ADUs are located in higher-income areas and provide housing for middle- and low-income families, “place diversity” can increase.[68] “Place diversity” refers to the spatial diversity of people and functions.[69] It can increase social equity by mixing different social groups in one area, providing more people with access to key resources.[70] A recent study found that geographical disparities in life expectancy in US counties are large and increased from 1980 to 2014.[71] Furthermore, research shows that growing up in a neighborhood with concentrated poverty may decrease one’s well-being.[72]

Infill development — when new buildings are constructed in previously developed areas rather than on raw land — could provide more residents with access to better schools, safety, and other vital services that improve health and well-being, assuming that these new units are located in well-established resource areas.[73] In contrast, infill units in neighborhoods with high crime and low-performing schools would not provide access to crucial resources.

What Are the Potential Effects of SB 13 on Unpermitted ADUs?

There is a fair amount of evidence that an amnesty program for unpermitted ADUs encourages landlords to bring units into compliance with permitting requirements, but it is not well researched if this results in health- and safety-related improvements in units with unhealthy or unsafe conditions.[74] The impact of an amnesty policy on rents is not well researched.

Existing literature on ADUs notes that the majority of existing units are unpermitted.[75] A 2014 study estimated 25,000 unpermitted ADUs in Los Angeles alone.[76] Unpermitted ADUs may not have the proper living amenities and may not meet local health and safety standards, which could have health implications. One study in the East Bay Area found that ADUs were more likely to have substandard cooking facilities than other types of rental units, due largely to the number of unpermitted ADUs and construction carried out in an amateur manner.[77]

Research demonstrates that various amnesty programs throughout California have proven successful encouraging many homeowners to register unpermitted units.[78] For example, in just two years, 60 units were legalized in Marin County.[79]Their success was attributed to a limited grace period coupled with fee reduction and regulatory concessions.[80] However, it is unknown if ADU amnesty programs lead to improvements in the health and safety conditions of unpermitted units. Research is needed to determine how to most effectively structure an amnesty program to ensure that owners of unpermitted units in poor conditions may have a path to receive permits and also have incentives to improve the quality of their ADUs.

It is not well researched whether providing a pathway for unpermitted ADUs to become compliant changes rents for tenants. The informal manner in which many ADUs are built, managed, and supplied contributes to relatively lower rents.[81] As noted above, a 2011 study in the East Bay Area found that rents were affordable to someone earning at or below 62% of the area median income.[82] However, this same study found that upwards of 90% of ADUs in the city of Berkeley, one of three cities within the area researched, lacked building and zoning permits.[83] Further research is required to make conclusive claims regarding the effects widespread amnesty might have on rents.

Which Populations Are Most Likely to Be Affected by SB 13?

Research suggests ADUs are composed of smaller households and younger adults compared to the primary residence. Also, ADUs may have important implications for middle age adults, seniors, and communities of color.

The Terner Center study found that ADU households in Portland, Seattle, and Vancouver generally are small: 57% of ADUs consisted of one person and 36% consisted of two people.[84] A study in Oregon found similar results: 64.2% of households included one person and 34.3% two people.[85] It also found that nearly 60% of occupants were female.[86]

Various studies have found that ADU tenants are younger than residents of the primary unit and that most do not have children. A study conducted in the Bay Area found that adults in ADUs were, on average, 11 years younger than those residing in the main residence.[87] It also found an average of 0.18 children per ADU household compared to 0.37 in households in the primary residence.[88] Other studies suggest that ADUs can be an affordable housing option for students near college campuses.[89]

In addition, ADUs can help middle-aged and elderly homeowners who build and rent ADUs. Although seniors currently do not disproportionally utilize ADUs more than other age groups, ADUs may become a source of income for them in the long run. ADUs could provide seniors with the ability to live in multi-generational homes near their children, house caretakers, or downsize to live in a smaller unit while renting the primary residence for extra income.

Facilitating the development and legalization of ADUs could have important implications for communities of color. The majority of individuals in California facing high housing cost burdens are people of color, so if SB 13 led to an increase in the housing supply — particularly in the supply of affordable housing, with resulting effects on health as described above — people of color might especially benefit.[90] At the community level, one study found the most restrictive ADU laws are in communities of color with lower household incomes, greater declines in income during 2010s, and lower median home values.[91] More research is needed to understand why these communities have chosen to enact more restrictive ADU laws in order to understand the benefits and tradeoffs that these communities could experience if SB 13 becomes law.

How Large Might the Impact Be?

The history of zoning in the United States and California has led to urban sprawl and strict limitations on density, which makes ADUs a potential solution to increase the supply of housing in desirable neighborhoods. ADUs allow for infill development of housing in single-family-home neighborhoods. Census data from 2000 show that 56% of overall housing stock in California is composed of single-family detached units.[92] The concentration of single-family-home neighborhoods is even higher in some cities. For example, 94% of residential land in San Jose is zoned for detached single-family homes.[93] After state policymakers eased ADU regulations in 2016, applications in San Jose increased from 45 in 2016 to 166 in 2017.[94] Many other cities, including Los Angeles, Oakland, and San Francisco, also saw significant growth in the number of applications. Oakland received 99 ADU applications in 2016, and 247 in 2017.[95] Therefore, ADUs are a potential strategy to boost the supply of housing in areas that offer few opportunities for large scale multi-family and apartment developments.[96]

Bill Information

Bill number: SB 13

Bill topic: Accessory Dwelling Units (ADUs)

Primary Sponsor: Senator Bob Wieckowski

The bill aims to facilitate the construction of ADUs in single-family and multi-family areas. Key components of the bill prohibit a local agency from:

Requiring the replacement of parking spaces if a garage, carport, or covered parking is demolished to construct an ADU.

Imposing parking standards on ADUs located within a traversable distance of one-half mile of public transit.

Establishing a minimum square footage.

Establishing a maximum square footage that is either less than 850 square feet, or 1,000 square feet for ADUs with more than one bedroom.

Requiring owner occupancy for either the primary residence or the ADU until January 1, 2025.

Imposing any impact fees upon the development of an ADU that is less than 750 square feet. For larger ADUs, the bill would require any impact fees to be proportional to the square footage of the primary dwelling unit.

SB 13 requires a local agency to consider an application within 60 days, instead of the current 120-day review window. In addition, the bill encourages owners of unpermitted ADUs – those built before January 1, 2020 – to register their units and come into compliance with local building standards. Specifically, a local agency, upon request of an owner, would be required to delay enforcement of a local building standard for five years.

Methodology

Once the bill was selected, the research team hypothesized the bill’s likely impacts, including health outcomes. The bill components were mapped into steps on a pathway of impacts. Research questions and a list of keywords to search were developed. They reached consensus on the final conceptual model, research questions, contextual background questions, keywords, and keyword combinations. Internal and external subject matter experts reviewed a draft of the note. A copy of the conceptual model is available upon request.

Our research questions related to the bill components examined:

To what extent do ADUs affect the supply of housing?

To what extent do ADUs affect the supply of affordable housing?

To what extent do ADUs affect the supply of housing in areas zoned for single-family/multi-family dwelling use?

To what extent do ADUs affect access to well-established neighborhoods with services and transportation?

To what extent do ADUs affect access to safe and quality neighborhoods?

To what extent does rent from ADUs supplement homeowner income to pay for mortgages?

To what extent does rent from ADUs help seniors supplement income?

To what extent do ADUs help seniors retire in place?

To what extent do ADUs affect household disposable income?

To what extent do ADUs affect housing instability?

To what extent do ADUs provide long-term housing?

To what extent do ADUs house families compared to individuals?

To what extent do ADUs provide quality housing?

To what extent do ADUs affect homelessness?

To what extent does legislation incentivize the construction of ADUs?

To what extent does amnesty of unpermitted ADUs lead owners to register and become fully compliant?

The research team then conducted an expedited literature review using a systematic approach to minimize bias and answer each of the identified research questions.[97] They limited the search to systematic reviews and meta-analyses of studies first, since they provide analyses of multiple studies or address multiple research questions. If no appropriate systematic reviews or meta-analyses were found for a specific question, we searched for nonsystematic research reviews, original articles, and research reports from US agencies and nonpartisan organizations. The search was limited to electronically available sources published between January 2014 and January 2019. Research cited by these sources was also explored, some of which were outside these dates.

The research team searched PubMed and EBSCO databases along with the following leading journals to explore each research question: The American Journal of Public Health, Social Science and Medicine, Health Affairs, Social Science Research, Journal of Urban Economics, Housing Policy Debate, Housing Studies, and Journal of Housing and Community Development. For all searches, the research team used the following key terms: Accessory Dwelling Units, supply of housing, affordable housing, proximity to services, quality housing, healthy housing, transportation, disposable income, rent, rent burden, housing stability, mortgages, seniors, aging, low-income families, green housing, and secondary income.

The research team also searched the websites of leading relevant policy organizations, including the Terner Center at UC Berkeley, the Lincoln Institute of Land Policy, the US Department of Housing and Urban Development, the Brookings Institute, and the Urban Institute.

After following the above protocol, the research team screened 95 abstracts. They reviewed and identified 36 peer-reviewed and grey literature sources for full-text review, excluding 18 titles. The remaining 18 sources were included in the Health Note. In addition, the research team identified other peer-reviewed sources through the original articles and identified additional resources with relevant research outside of the peer-reviewed literature. A final sample of 26 resources was used to create the Health Note.

Of the studies included, the strength of the evidence was qualitatively described and categorized as: not well researched, mixed evidence, a fair amount of evidence, strong evidence, or very strong evidence. The evidence categories were adapted from a similar approach from another state.

Very strong evidence: The literature review yielded robust evidence supporting a causal relationship with few if any contradictory findings. The evidence indicates that the scientific community largely accepts the existence of the relationship.

Strong evidence: The literature review yielded a large body of evidence on the association, but the body of evidence contained some contradictory findings or studies that did not incorporate the most robust study designs or execution or had a higher than average risk of bias; or some combination of those factors.

A fair amount of evidence: The literature review yielded several studies supporting the association, but a large body of evidence was not established; or the review yielded a large body of evidence but findings were inconsistent with only a slightly larger percent of the studies supporting the association; or the research did not incorporate the most robust study designs or execution or had a higher than average risk of bias.

Mixed evidence: The literature review yielded several studies with contradictory findings regarding the association.

Not well researched: The literature review yielded few if any studies or yielded studies that were poorly designed or executed or had high risk of bias.

Additional Information

This Health Note was produced using a methodology and approach developed by the Health Impact Project at The Pew Charitable Trusts, and is part of a pilot program in several jurisdictions to test the use of Health Notes to inform policymaking at state and local levels. This Health Note is supported by a grant from the Health Impact Project. The views expressed are those of the authors and do not necessarily reflect the views of the Health Impact Project or The Pew Charitable Trusts.

Dr. Sherice Janaye Nelson is a professor at St. Mary’s College of California and researches the effects of the Black Diaspora with emphasis in the United States. Her study of Black Americans encompasses the economic and political behaviors and the effect of those behaviors in a modern-day democracy. Dr. Nelson served as our external subject matter expert. Sara Kimberlin, Senior Policy Analyst at the Budget Center, served as internal subject matter expert and guided the development of the Health Note.

Aureo Mesquita, Adriana Ramos-Yamamoto, and Monica Davalos prepared this Health Note. The Budget Center was established in 1995 to provide Californians with a source of timely, objective, and accessible expertise on state fiscal and economic policy issues. The Budget Center engages in independent fiscal and policy analysis and public education with the goal of improving public policies affecting the economic and social well-being of low- and middle-income Californians. General operating support for the Budget Center is provided by foundation grants, subscriptions, and individual contributions.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Introduction

Unaffordable housing costs are one of California’s most pressing challenges. The high cost of housing is one of the primary drivers of California’s high poverty rate — ranked first among the 50 states — under the Supplemental Poverty Measure, which accounts for differences in the local cost of living.[1] The lack of affordable housing increases economic insecurity among California families and also creates challenges for California employers striving to retain and recruit workers. Housing affordability is a problem throughout the state when housing costs are compared to incomes, and the Californians who are most affected by the housing affordability crisis are renters and households with the lowest incomes. Policy solutions that particularly target these households represent a promising approach to tackling the state’s housing crisis strategically, with a focus on those most deeply affected.

Renters Are Especially Likely to Have Unaffordable Housing Costs, While Homeowners Without Mortgages Are Least Affected

Determining whether housing is affordable requires considering both housing costs and household incomes. For renters, housing costs include monthly rent payments, plus the cost of utilities if not included in the rent. Housing costs for homeowners include monthly mortgage principal and interest payments, plus property tax, property insurance, utilities, and condo or mobile home fees (if applicable). To understand California’s housing affordability challenges, it is important to consider these housing costs relative to incomes. If high housing costs are matched by high incomes, then expensive housing may be affordable to many households. At the same time, even relatively low housing costs may be unaffordable if local incomes are also low.

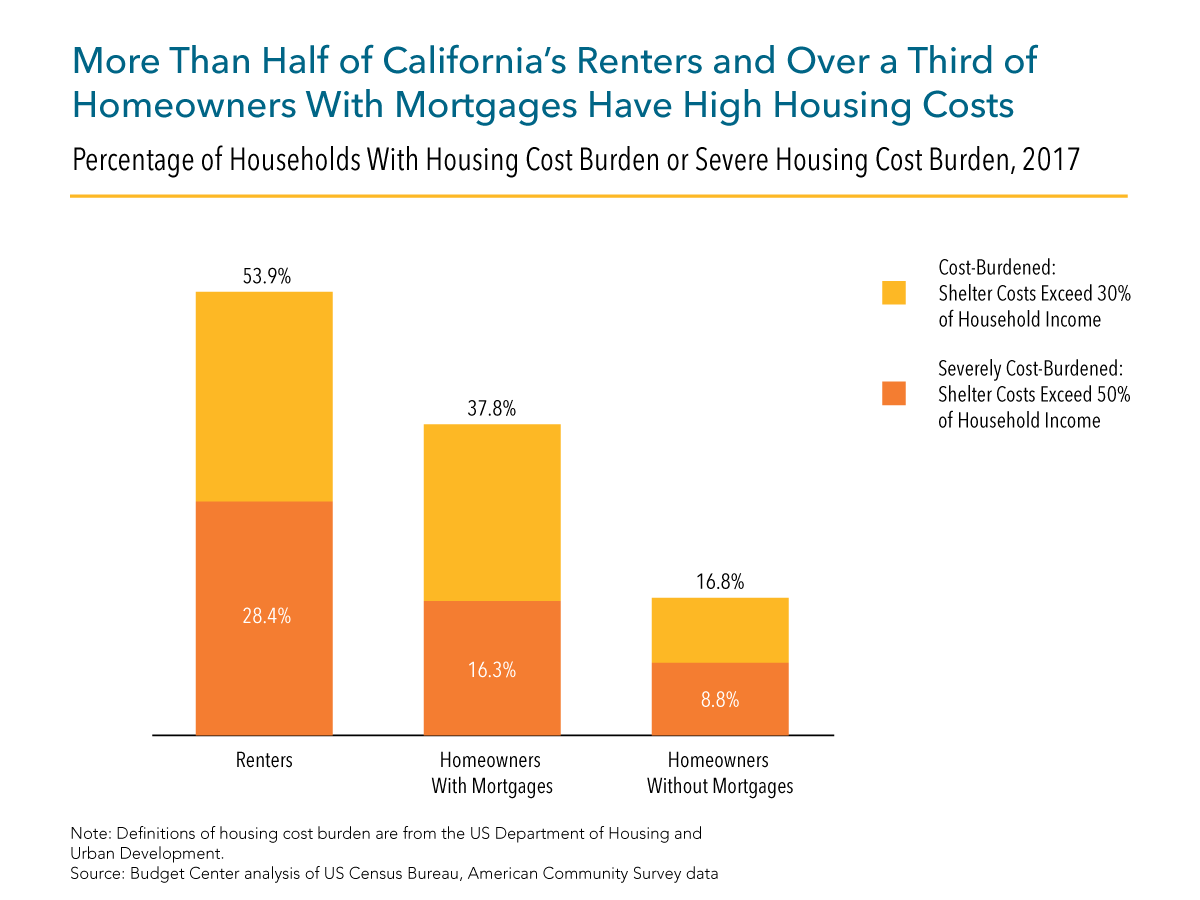

For housing costs to be considered affordable, a household’s total housing costs should not exceed 30 percent of household income, according to the US Department of Housing and Urban Development. Households paying more than 30% of income toward housing are considered housing “cost-burdened,” and those with housing costs that exceed half of their income are considered “severely cost-burdened.” By these standards, more than 4 in 10 households statewide had unaffordable housing costs in 2017. Furthermore, 1 in 5 households across California faced severe housing cost burdens, spending more than half of their income toward housing expenses.

California’s renters are substantially more likely to struggle with housing affordability than homeowners in California. More than half of renter households paid over 30% of income toward housing in 2017, and more than a quarter were severely cost-burdened, paying more than half of household income toward housing costs. California homeowners generally struggle less to afford their housing, though more than a third of homeowners with mortgages were housing cost-burdened in 2017. Owners without mortgages are least likely to face high housing burdens in California. Besides not having the monthly expense of a mortgage, many of these homeowners have been in their homes for decades and therefore benefit from relatively low property taxes due to Proposition 13’s limitation on property tax increases.

Low-Income Households Are Particularly Affected by Unaffordable Housing

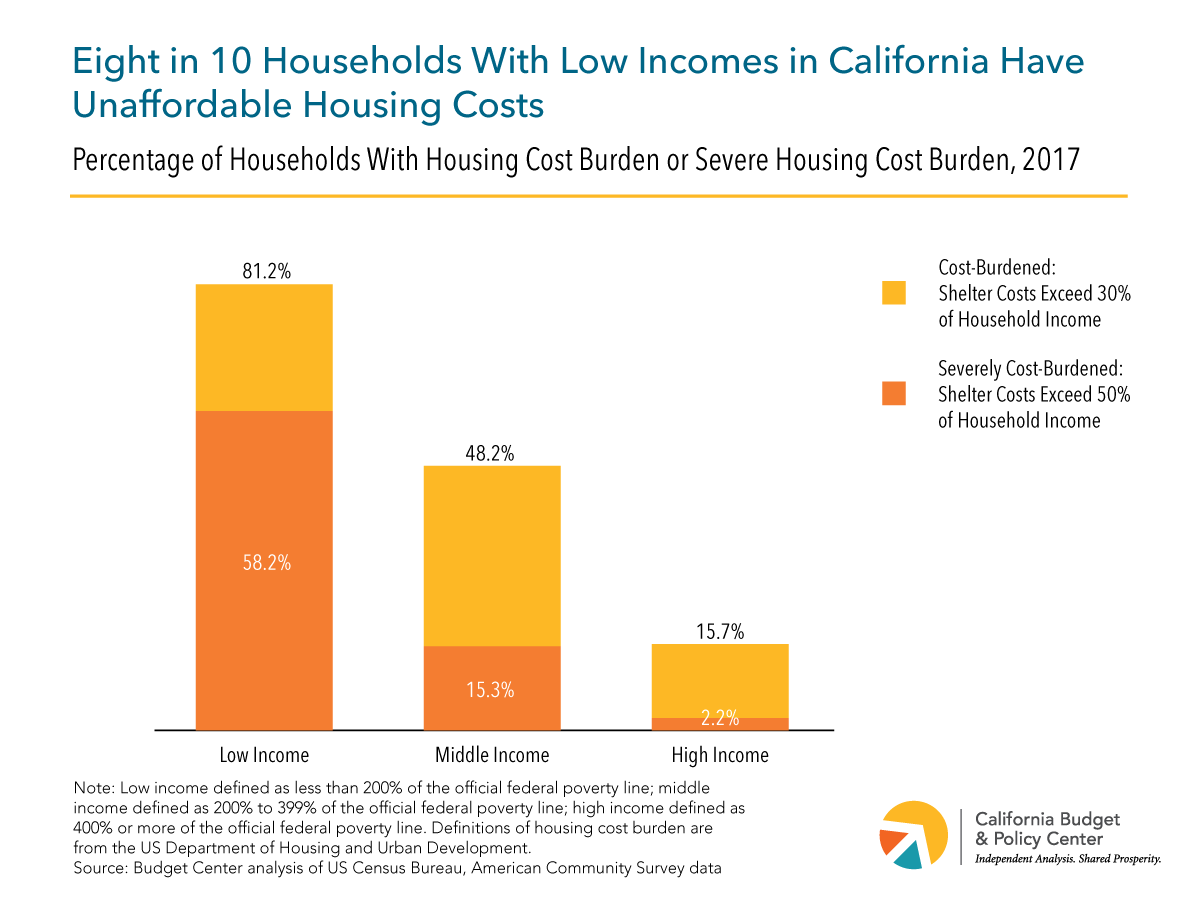

Households with the lowest incomes are by far the most likely to have housing costs that are unaffordable. Eight in 10 households with low incomes (those with incomes of less than 200% of the federal poverty line) were housing cost-burdened in 2017, and more than half of these households spent more than half their income on housing. At the same time, only about 16% of high-income households (with incomes of 400% or more of the federal poverty line) were housing cost-burdened in 2017, and less than 3% were severely cost-burdened.

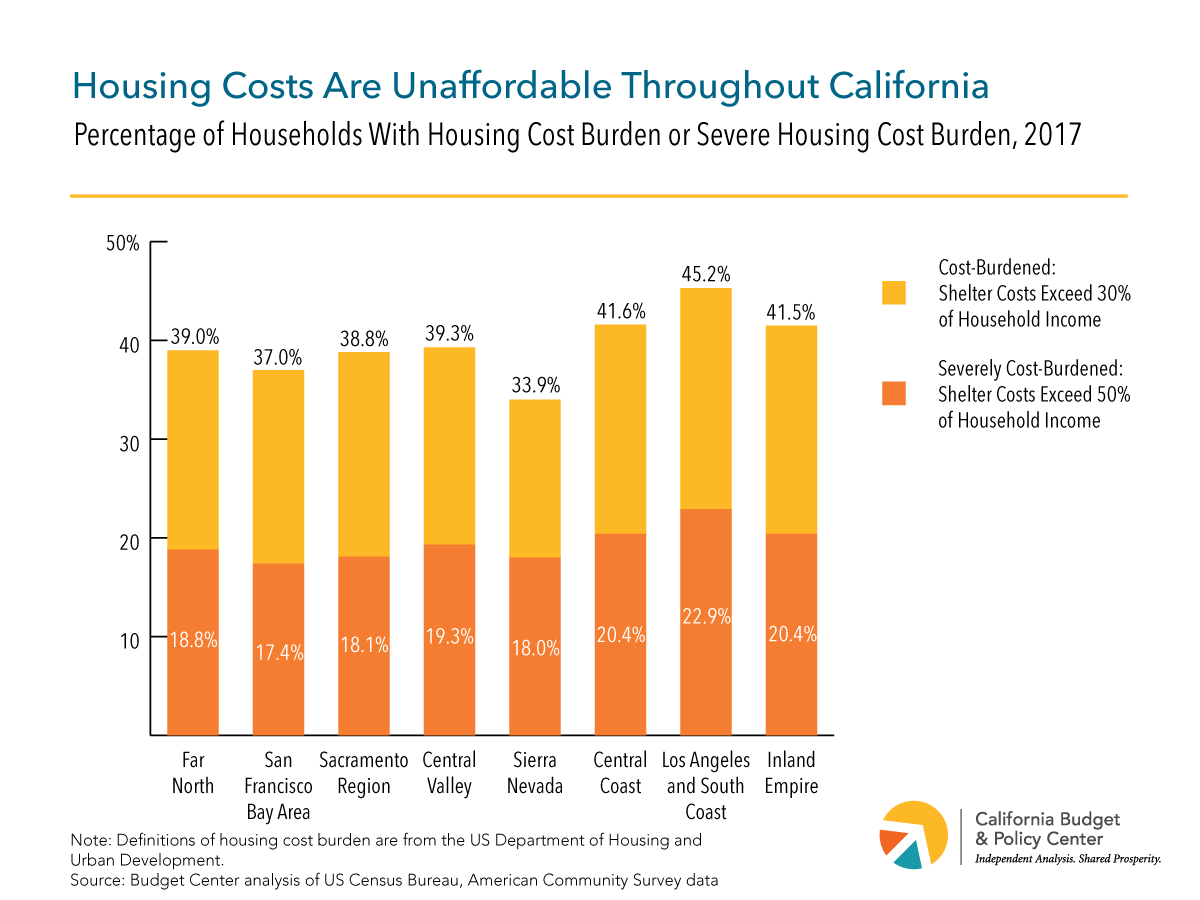

Housing Affordability Is a Problem in All Regions of California, and Many of Those Affected Are People of Color

Housing costs vary substantially throughout California, with the highest costs in coastal urban areas and the lowest costs in inland rural areas. But incomes also vary regionally, and areas with relatively lower housing costs also tend to have lower typical incomes. The result is that housing affordability is clearly a problem throughout the state when housing costs are compared to incomes. Across every region of California, from the high-cost San Francisco Bay Area and Los Angeles and South Coast to the lower-cost Central Valley and Far North, at least a third of households spent more than 30% of their incomes toward housing in 2017, and more than 1 in 6 spent more than half of their incomes on housing costs.

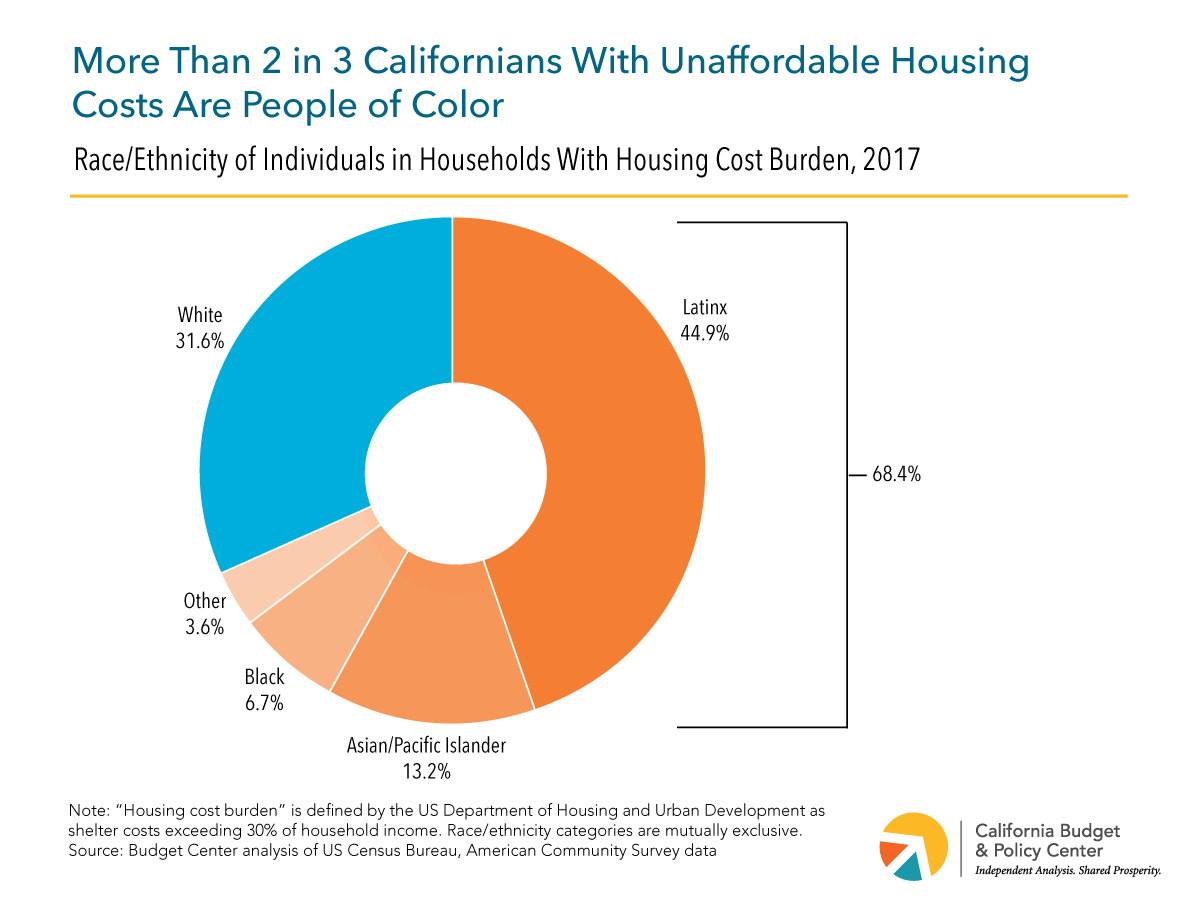

Throughout the state, many of the individuals affected by unaffordable housing costs are people of color. Among all Californians living in households paying more than 30% of income toward housing costs in 2017, more than two-thirds were people of color, and about 45% were Latinx.

High Housing Cost Burdens Call for Policies Designed to Help Those Who Are Most Affected

What problems arise when households struggle to afford housing? Unaffordable housing costs can force families to spend less on other basic necessities like health care or food, to cut costs by seeking lower-quality child care, and to under-invest in important long-term assets like education or retirement savings. Unaffordable housing costs can also force families and individuals to accept substandard housing or live in neighborhoods that lack basic safety and offer limited opportunities. In the most serious cases, unaffordable housing can push households into homelessness. All of these consequences can have cascading effects on health and can shape both short-term well-being and long-term outcomes for affected individuals.[2]

Given the challenges of housing affordability across all regions of California — especially for renters, households with the lowest incomes, and people of color — strategies to increase affordability are urgently needed, particularly for the most-affected Californians. Housing affordability policy solutions can focus on protection of affordability for current residents, preservation of existing affordable housing, and production of more housing, particularly homes targeted to the households that struggle most to find and retain affordable housing, including renters and those with the lowest incomes. Specific policy solutions that can make a difference include tenant protections against excessive rent increases, funding to support affordable housing construction and preservation, and policies that increase local incentives and local accountability for accommodating more housing development, particularly for housing affordable to low-income households. Moreover, policies outside of the housing arena that help families make ends meet — by reducing costs for child care, food, health care, or other necessities, or by supplementing incomes — represent another important approach to helping Californians who are struggling to afford the cost of housing.

As state leaders craft budget and policy proposals, it is important to acknowledge that a mix of policies is needed to address California’s housing affordability challenges and that doing so is particularly important for California’s renters, low-income households, and people of color.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

The Center on Budget and Policy Priorities’ annual conference, Impact 2018: Building Momentum for Equity and Opportunity, brought together members of the State Priorities Partnership (SPP), a network of independent, nonprofit research and policy organizations representing more than 40 states, and others interested in state policy. Executive Director Chris Hoene presented to the SPP Leadership Institute on the results of a strategic planning retreat he attended earlier this year and also introduced the conference’s closing plenary speaker, Professor Manuel Pastor of USC. Also, Steven Bliss, Director of Strategic Communications, presented “Using Digital Tools to Expand Reach and Engagement” for the workshop “Digital Advocacy 101.”

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

This website uses cookies to analyze site traffic and to allow users to complete forms on the site. The California Budget & Policy Center does not share, trade, sell, or otherwise disclose personal information. By using our website you agree to our Privacy Policy.