Established as part of the 2015-16 state budget package, the California Earned Income Tax Credit (CalEITC) is a refundable state credit that helps people who earn little from their jobs to pay for basic necessities. An updated research summary from the Budget Center discusses how, by “piggybacking” on the federal EITC, state EITCs like that in California not only help families to better make ends, but also may enhance the various positive impacts of the federal EITC, such as reducing poverty, encouraging work, and potentially creating other long-term benefits for workers and their families.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

The California Work Opportunity and Responsibility to Kids (CalWORKs) program provides modest cash assistance to about 860,000 low-income children while helping parents overcome barriers to work and find jobs. Despite modest increases in recent years, CalWORKs grants still fall far short of allowing families to maintain a decent standard of living.[1] Although Governor Brown projects substantial positive state General Fund balances for the next few years, his proposed 2018-19 budget does not make any new investments in CalWORKs grants, leaving the maximum monthly grant for a family of three living in a high-cost county $9 lower than it was in 2006, without even adjusting for inflation.[2]

This lack of investment in CalWORKs is especially striking given that median monthly rents have steadily increased in recent years, widening the gap between housing costs and cash assistance. In other words, the Governor has chosen not to prioritize new investments in one of the state’s most vital supports for low-income families with children, even though these families are finding it harder each year to keep a roof over their heads.

Median Rents Far Exceed CalWORKs Grants

Regardless of where families live in California, the typical monthly rent far exceeds monthly CalWORKs grants. For example, the maximum monthly grant for a family of three in a high-cost county in 2018 ($714) covers just 43% of the median monthly rent for a two-bedroom unit ($1,658). This is down from covering 61% of the cost of rent in 2006, when the maximum monthly grant was $723 and the median rent was $1,180.[3] Viewed another way, the maximum monthly CalWORKs grant for a parent with two children now falls $944 short of covering the monthly cost of a two-bedroom rental, more than double the gap of $457 in 2006. Even in low-cost counties, median rents have exceeded maximum grant levels in recent years, although the gap between rents and grants is somewhat narrower than in high-cost counties. In these counties, the maximum grant for a family of three in 2018 ($680) falls $344 short of covering the cost of a two-bedroom rental ($1,024).

Unstable Housing Is Harmful to Children

Children in CalWORKs families pay the price when grants fall short of rent costs. Housing instability and overcrowding increase children’s stress and contribute to poor health, behavior problems, and difficulty learning.[4] When parents face high rent burdens, they have fewer resources to meet other basic expenses and to invest in their children’s development. Furthermore, high housing costs put children at risk of homelessness. According to the US Department of Housing and Urban Development (HUD), on a single night in 2017, a total of 21,522 people in families with children were homeless in California.[5] In Los Angeles County, the number of CalWORKS families who reported lacking a stable place to live almost tripled between 2006 and 2017, even as the number of all families served by the program declined by nearly 10% during that period.[6] Insufficient grants could therefore undermine the first goal of CalWORKs: reducing child poverty in California.

How Can Policymakers Help CalWORKs Families Better Afford Housing?

Helping families afford stable housing in California will require significant, sustained efforts by federal, state, and local leaders, and a long-term solution to the state’s housing crisis will likely take time to develop and implement. In the meantime, however, policymakers can provide families in the greatest need, such as CalWORKs families, with some relief by increasing their incomes through grants and reducing their costs of housing.

State Policymakers Should Raise CalWORKs Grants, Restore the Annual State Cost-of-Living Adjustment (COLA), and Improve Housing and Homelessness Assistance

Due to the elimination of the annual state COLA along with grant reductions during and after the Great Recession, the maximum CalWORKs grant for a family of three has lost more than one-quarter of its purchasing power since 2007-08. Moreover, since 1998-99, the first full fiscal year after the program was created, the maximum grant has lost 37% of its purchasing power.[7] While state leaders have provided some grant increases in recent years, they have not fully restored cuts made in prior years. The current grant is equal to just 41% of the federal poverty line (FPL), leaving it well below the deep-poverty line (50% of the FPL).[8] The Governor’s proposed budget for 2018-19 does not call for increasing CalWORKs grants or reinstating the annual COLA, despite the fact that state revenues are projected to exceed expenditures by billions of dollars.

In the short term, state policymakers should raise maximum grants to at least 50% of the FPL to ensure that no CalWORKs family lives in deep poverty, which is particularly detrimental to children.[9] Over the longer term, policymakers should boost grants further so that families can better meet our state’s high housing costs. Moreover, grants should more accurately reflect regional differences in the cost of living. In high-cost counties, the maximum monthly CalWORKs grant for a family of three is just $34 more than in low-cost counties, even though the actual median rent differential for two-bedroom units is $634. Lastly, state leaders should allow CalWORKs families to access housing and homelessness assistance when they need it throughout the year and should also expand the types of housing providers and arrangements for which families may receive assistance.[10]

Federal Policymakers Should Expand Rental Assistance

Federal rental assistance — particularly through the Housing Choice Voucher program — helps hundreds of thousands of Californians afford rent.[11] Research shows that by subsidizing rental costs, housing vouchers decrease overcrowding, housing instability, and homelessness.[12] Vouchers also free up resources that families can put toward other basic needs. However, voucher receipt has fallen due to federal budget cuts and rental assistance does not reach many struggling families. CalWORKs families face dire circumstances, as nearly 9 in 10 families (88%) did not receive federal housing assistance in 2016, based on Center on Budget and Policy Priorities (CBPP) estimates.[13] California’s needs gap is exacerbated by regional differences: a smaller share of families living in poverty with young children receive housing subsidies in high-cost counties than in low-cost counties.[14]

Despite this tremendous unmet need, President Trump’s proposed budget for the 2019 federal fiscal year (which begins on October 1, 2018) actually calls for raising rents on a substantial number of people receiving rental assistance, potentially affecting over 138,000 Californian households.[15] Additionally, the President’s call for cuts to housing vouchers could cause about 27,000 households in California to lose their housing vouchers.[16] Rather than taking steps backward, federal policymakers should instead strengthen investments in rental assistance so that families can better afford a roof over their heads.

[2] Accounting for inflation, the proposed 2018-19 maximum grant for a family of three in a high-cost county is $269 lower than in 2007-08. See Kristin Schumacher, CalWORKs Grants Are Overdue for a Significant Investment (California Budget & Policy Center: February 2018).

[3] Median rents reflect gross monthly rents, which include the cost of utilities and fuels. The median rent for high-cost counties reflects the median rent for all high-cost counties combined, while that for low-cost counties reflects the median rent for all low-cost counties combined. High-cost and low-cost counties were determined based on the definitions in California’s Welfare and Institutions Code (WIC), Section 11452.018, with one exception: San Benito County. Specifically, the US Census Bureau data used in this analysis do not allow San Benito County (a low-cost county) to be distinguished from Monterey County (a high-cost county). As such, San Benito County is grouped with high-cost counties. Since San Benito is not a very populous county, combining it with high-cost counties is unlikely to substantially affect the analysis. Rents for years 2006 to 2016 are from the US Census Bureau’s American Community Survey. For 2017 and 2018, median rents are estimated based on the compound annual growth rate in median rents between 2011 and 2016.

[5] The 21,522 figure from HUD is a point-in-time estimate and refers to “a person who lacks a fixed, regular, and adequate nighttime residence” on one day of the year. The number of homeless families with children is likely far greater, as this estimate does not include people who are living with friends or family or in motels because they do not have places of their own. For more on the gaps in HUD point-in-time numbers, see Alissa Anderson, Many People in Our Communities Lack a Home for the Holidays (California Budget and Policy Center: November 23, 2015). For HUD’s estimates, see US Department of Housing and Urban Development, The 2017 Annual Homeless Assessment Report (AHAR) to Congress: Part 1—Point-in-TimeEstimates of Homelessness (December 2017). For HUD’s methodology, see US Department of Housing and Urban Development, Point-in-Time Count Methodology Guide (September 2014).

[6] Personal communication with the Los Angeles County Department of Public Social Services on February 12, 2018. These figures reflect CalWORKs families in Los Angeles County in July 2006 and July 2017.

[7] Budget Center analysis of data from the Department of Social Services. If CalWORKs grants had been adjusted annually using the California Necessities Index, in the 2018-19 fiscal year the grant would have been $1,136. This would have been greater than the deep-poverty line (50% of the FPL), but still well below the poverty line.

[10] Current law provides homeless CalWORKs families temporary housing assistance, but mandates that families use the assistance for up to 16 consecutive days within 12 months or else lose their eligibility. In other words, even if a family accepts assistance for fewer than 16 days in a row, they become ineligible for additional assistance for the rest of the year even if they experience another spell of homelessness later. Additionally, the law allows families to receive funds once every 12 months to secure longer-term housing or to avoid eviction. However, this assistance only pays for housing arrangements through hotels and motels, shelters, or those with a history of renting properties. According to the County Welfare Directors Association of California, in some counties, families trying to secure housing through a shared housing arrangement such as a sublease have been unable to receive aid because of this restriction. For more, see Assembly Committee on Human Services, Analysis of AB 1921 (March 2, 2018).

[13] Personal communication with the Center on Budget and Policy Priorities (CBPP) on March 29, 2018. CBPP divided the number of households receiving federal housing assistance who report participating in CalWORKs by the annual monthly average CalWORKs caseload. CalWORKs caseload data come from California’s Department of Social Services and exclude Work Incentive Nutritional Supplement cases. Federal housing assistance data come from US Department of Housing and Urban Development (HUD) administrative data and reflect the following HUD-administered rental assistance programs: Public Housing; Section 8 Housing Choice Vouchers; Section 8 Project-Based Rental Assistance (including Moderate Rehabilitation); Supportive Housing for the Elderly (Section 202); Supportive Housing for People With Disabilities (Section 811); Rent Supplement; and the Rental Assistance program. This analysis does not include a relatively small number of households receiving assistance through homelessness programs, Housing Opportunities for Persons With AIDS, or the US Department of Agriculture’s Rural Rental Assistance program (Section 521).

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

California Budget Perspective is the Budget Center’s annual “chartbook” publication that takes an in-depth look at the Governor’s proposed state budget.

California Budget Perspective 2018-19 examines the social, economic, and policy context for this year’s budget; discusses key elements of — and priorities reflected in — the Governor’s proposal; and highlights issues to watch in the coming months.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Executive Summary

On January 10, Governor Jerry Brown released a proposed 2018-19 budget that prioritizes building up reserves amid deep uncertainty about looming federal budget proposals, the impacts of the recently enacted federal tax bill, and future economic conditions. The Governor forecasts revenues that are $4.2 billion higher (over a three-year “budget window” from 2016-17 to 2018-19) than previously projected in the 2017-18 budget enacted last June, driven largely by continued economic growth. The Governor’s budget assumes no changes to current federal policies and funding levels and is not yet able to account for the potential impacts of the Republican tax bill passed in late December.

The Governor’s proposed budget reflects some notable advances, such as providing funding to fully implement the Local Control Funding Formula for K-12 education (designed to direct additional resources to disadvantaged students), continuing to invest in early education and higher education, and creating a home visiting pilot program that would offer a range of supports for families participating in welfare-to-work (CalWORKs). In addition, the proposal maintains resources to address the impact of federal actions targeting the state’s immigrant residents. Yet, the Governor also places a heavy emphasis on building California’s reserves. He proposes making a one-time supplemental deposit of $3.5 billion to the state’s rainy day fund, in addition to the $1.5 billion required by Proposition 2 (2014). This proposed $5.0 billion deposit would raise the rainy day fund balance to the Prop. 2 maximum of 10 percent of General Fund tax revenues.

While the prospect of major changes in federal policy is a reason for caution, this budget could strike a better balance between putting away funds for a rainy day and boosting investments now that would help more Californians make ends meet and advance economically. Opportunities include increasing basic income support provided by the California Earned Income Tax Credit (CalEITC), boosting cash assistance for low-income seniors and people with disabilities (SSI/SSP), raising CalWORKs grant levels, and advancing new proposals to address our state’s affordable housing crisis.

The 2018-19 state budget debate will move forward amid many unknowns at the federal level, making it critical that California’s congressional delegation and state lawmakers seek to advance smart policy choices that broaden economic opportunity and push back against federal proposals that would harm people and communities across the state.

The following sections summarize key provisions of the Governor’s proposed 2018-19 budget.

Download full report (PDF) or use the links below to browse individual sections of this report:

Administration Expects Modest Economic Growth, but Notes Potential Risks

Within the past year, both the US and California have seen their lowest unemployment rates since 2000. The Administration expects the state’s unemployment rate to remain low over the next few years, at around 5 percent. The Governor’s proposed budget assumes that California’s economy will grow modestly over the next five years, but with jobs added at a slower pace than during the past five years. This expected slowdown is due in part to the state’s high housing costs, which limit the ability of employers to recruit workers to move into or within the state to access jobs. As inflation has begun to rise nationally, California’s high housing costs are also expected to contribute to continuing higher inflation within the state compared to the US.

While projecting modest economic growth, the Administration points to the risk of a national recession, noting that this current period of growth has lasted more than eight years and that unemployment rates nationally and in California are at “levels only seen near the end of an expansion.” While this risk is worth keeping in mind, a recession in the next few years is not inevitable. The Legislative Analyst’s Office (LAO) and other experts have pointed out that the recent long period of expansion does not in and of itself mean that another recession is likely soon. Other potential economic risks noted by the Administration include a stock market correction and geopolitical events that disrupt global trade. It is important to note that the Governor’s budget does not incorporate projected economic impacts from the recently passed federal tax bill, with assessment of those effects postponed to the May Revision.

The Governor’s proposed budget projects higher-than-expected revenues due to an improved economic forecast. However, the Administration cautions that its revised revenue projections are subject to uncertainty. Most notably, the estimates do not take into account the impact of the recently enacted federal tax legislation, which will have significant implications for California. Budget documents note that the Administration’s revised forecast in May will include preliminary estimates of the impact of the new tax law.

The proposed budget projects that total General Fund revenues (before transfers) over the three-year “budget window,” from 2016-17 to 2018-19, will be about $4.2 billion higher than the projections included in the 2017-18 budget agreement. The stronger revenue forecast is largely driven by higher personal income tax (PIT) and sales and use tax (SUT) revenue projections. Specifically, the Governor expects PIT revenues during this three-year period to be nearly $2.9 billion higher, SUT revenues to be $1.5 billion higher, and corporation tax (CT) revenues to be $358 million lower than expected when the budget for the current fiscal year was signed into law. Higher PIT projections largely reflect stronger wage gains, particularly among higher-income taxpayers, while higher SUT projections are due to stronger-than-expected consumer spending and capital equipment spending by businesses. Lower CT revenues result from weaker-than-anticipated corporate tax receipts in spite of strong corporate profits.

The Governor’s Proposal Opts to Maximize the State’s Rainy Day Fund and Build Up State Reserves

California voters approved Proposition 2 in November 2014, amending the California Constitution to revise the rules for the state’s Budget Stabilization Account (BSA), commonly referred to as the rainy day fund. Prop. 2 requires an annual set-aside equal to 1.5 percent of estimated General Fund revenues. An additional set-aside is required when capital gains revenues in a given year exceed 8 percent of General Fund tax revenues. For 15 years — from 2015-16 to 2029-30 — half of these funds will be deposited into the rainy day fund, and the other half will be used to reduce certain state liabilities (also known as “budgetary debt”).

Based on the Governor’s revenue projections for 2018-19, Prop. 2 would constitutionally require the state to deposit $1.5 billion into the BSA (and to use an additional $1.5 billion to repay budgetary debt). In addition, the Governor proposes to make an optional, one-time supplemental transfer of $3.5 billion from the General Fund to the BSA. (The total transfer to the BSA would be $5.0 billion: $1.5 billion as required by the state Constitution, plus the $3.5 billion supplemental transfer.) As a result, the BSA would total $13.5 billion by the end of the 2018-19 fiscal year.

Under the scenario outlined by the Governor, the BSA would reach its constitutional maximum of 10 percent of General Fund tax revenues in 2018-19. When this limit is reached, Prop. 2 requires that any additional dollars that would otherwise go into the BSA be spent on infrastructure, including spending on deferred maintenance. In other words, Prop. 2 prohibits these additional dollars from being allocated to ongoing programs and services.

The BSA is not California’s only reserve fund. Each year, the state deposits additional funds into a “Special Fund for Economic Uncertainties” (SFEU). The Governor’s proposed budget calls for an SFEU balance of $2.3 billion. Including this fund, the Governor’s proposal would build state reserves to a total of $15.8 billion in 2018-19.

One additional implication of the Governor’s proposal is that the $3.5 billion supplemental transfer to the BSA may not be readily available to help the state meet needs created by future developments, such as federal budget cuts. In order to access the BSA funds, the Governor would need to declare a “budget emergency,” defined by Prop. 2 as a disaster or extreme peril, or insufficient resources to maintain General Fund expenditures at the highest level of spending in the three most recent fiscal years, adjusted for state population growth and the change in the cost of living. In contrast, an additional transfer to the SFEU would leave the funds more readily available to help the state address uncertainties. This is because funds in the SFEU can be accessed without the need to declare a budget emergency.

The California Earned Income Tax Credit (CalEITC) is a refundable state tax credit designed to boost the incomes of low-earning workers and their families and help them afford basic expenses. The credit was established by the 2015-16 budget agreement and was subsequently expanded as part of the 2017-18 budget deal.

Prior to this expansion, the CalEITC provided an average credit of more than $500 to around 370,000 families and individuals across the state. (Those with dependents received an average of more than $800, while those without dependents received an average of just over $100.) Many more Californians will likely benefit from the CalEITC this year due to the credit expansion.

The Governor’s proposed budget makes no changes to the CalEITC. Consistent with prior years, the Governor proposes maintaining the CalEITC “adjustment factor” at 85 percent for tax year 2018. (California policymakers must specify the CalEITC adjustment factor in each year’s state budget. This factor sets the state EITC at a percentage of the federal EITC, thereby determining the size of the state credit available in the following year.) Additionally, the Administration projects that the CalEITC will reduce state General Fund revenues by $343 million in 2017-18 and by $353 million in 2018-19.

The proposed budget also does not appear to include any funding to maintain community-based efforts to promote the CalEITC in order to boost credit claims. The 2016-17 and 2017-18 budget agreements each included $2 million for grants to community-based organizations and other local entities to support efforts to raise awareness of the CalEITC. Education and outreach efforts are important because evidence suggests that many families who were eligible for the credit missed out on it in recent years.

Increased Revenues Boost the Minimum Funding Level for Schools and Community Colleges

Approved by voters in 1988, Proposition 98 constitutionally guarantees a minimum level of funding for K-12 schools, community colleges, and the state preschool program. The Governor’s proposed budget assumes a 2018-19 Prop. 98 funding level of $78.3 billion for K-14 education, $3.1 billion above the revised 2017-18 minimum funding level. The Prop. 98 guarantee tends to reflect changes in state General Fund revenues and growth in the economy, and estimates of 2017-18 General Fund revenue in the proposed budget are higher than those in the 2017-18 budget agreement. As a result, the Governor’s proposed 2018-19 budget reflects a $75.2 billion Prop. 98 funding level for 2017-18, $688 million more than the level assumed in the 2017-18 budget agreement.

California’s school districts, charter schools, and county offices of education (COEs) provide instruction to approximately 6.2 million students in grades kindergarten through 12. The Governor’s proposed budget increases funding for the state’s K-12 education funding formula — the Local Control Funding Formula (LCFF) — providing sufficient dollars to reach the LCFF’s target funding level in 2018-19. The proposed budget also pays off outstanding state obligations to school districts. Specifically, the Governor’s proposed budget:

Increases funding by $2.9 billion to fully implement the LCFF. The LCFF provides school districts, charter schools, and COEs a base grant per student, adjusted to reflect the number of students at various grade levels, as well as additional grants for the costs of educating English learners, students from low-income families, and foster youth. The Governor’s proposal to increase LCFF funding is sufficient for all K-12 school districts to reach a target base grant in 2018-19 (all COEs reached their LCFF funding targets in 2014-15). As a result, all K-12 districts would reach their LCFF targets two years earlier than the Governor initially estimated when the Legislature enacted the LCFF.

Allocates $1.8 billion in one-time funding to reduce mandate debt the state owes to schools. Mandate debt reflects the cost of state-mandated services that school districts, charter schools, and COEs provided in prior years, but for which they have not yet been reimbursed.

Provides $212 million to support the Strong Workforce Program. The Governor’s proposed budget provides $200 million to establish a K-12-specific component of the Strong Workforce Program, which was established as part of the 2016-17 budget for the purpose of expanding the availability of community college career technical education (CTE) and workforce development programs. The Governor’s proposal also provides $12 million to fund local industry experts to provide technical support to K-12 districts that operate CTE programs.

Provides $133.5 million to fund cost-of-living adjustments (COLAs) for non-LCFF programs. The Governor’s proposed budget funds a 2.51 percent COLA for several categorical programs that remain outside of the LCFF, including special education, child nutrition, and American Indian Education Centers. The Governor proposes to use the increases in LCFF grants proposed for school districts and charter schools to fund the COLA for non-LCFF programs. The Governor’s budget also provides $6.2 million to fund a 2.51 percent COLA for COEs.

Allocates $100 million in one-time funding to increase and retain special education teachers. The Governor’s proposed budget includes $50 million for one-year, locally sponsored programs to prepare and retain special education teachers and $50 million for one-time competitive grants for K-12 school districts that create new, or expand existing, programs to address the need for special education teachers.

Provides $65.7 million in ongoing funding to implement a statewide system of support for K-12 school districts. To help address low student achievement in school districts identified by the state’s new accountability system, the Governor’s proposed budget includes $59.2 million for COEs and $6.5 million for the California Collaborative for Educational Excellence.

Governor Proposes New Funding Formula for California Community Colleges

A portion of Proposition 98 funding supports California’s community colleges (CCCs), which help prepare approximately 2.4 million full-time students to transfer to four-year institutions as well as obtain training and skills for immediate employment. The Governor’s budget proposes a new funding formula for CCC general-purpose apportionments and also calls for establishing a fully online community college. Specifically, the proposed budget:

Provides $175 million for a new general-purpose apportionment funding formula. The Governor’s proposal would allocate apportionments through three grants: a base grant, a supplemental grant, and a student success incentive grant. Each CCC district would receive a base grant based on a per-Full-Time Equivalent Student (FTES) funding rate that, similar to the current funding formula, would be applied to all districts. Each CCC district would also receive a supplemental grant based on the number of low-income students it enrolls as determined by two factors: students who receive a College Promise Grant fee waiver (formerly known as the Board of Governors Waiver) and students who receive a Pell grant. Each CCC district would also receive a student success incentive grant based on the number of students who “meet the following metrics: 1) the number of degrees and certificates granted and 2) the number of students who complete a degree or certificate in 3 years or less.” The student success incentive grant would also include additional funds for each Associate Degree for Transfer granted by the college. Under the new formula, funding for all CCC districts during the first year of implementation would be held harmless to the level of funding that the district received in 2017-18. The Governor’s proposal also assumes that approximately 50 percent of apportionment funding would be allocated initially as the base grant, 25 percent as part of the supplemental grant, and 25 percent as part of the student success incentive grant.

Includes $161.2 million to provide a 2.51 percent cost-of-living adjustment (COLA) for apportionments.

Allocates $120 million to establish a fully online community college. The proposed budget would allocate $100 million in one-time funding to set up the new online college and provide $20 million in ongoing funding. The Governor’s Budget Summary asserts that the online college “will not impact traditional community colleges’ enrollment because its enrollment base will be working adults that are not currently accessing higher education.”

Provides $46 million to support implementation of the California College Promise. Under the proposed spending plan, CCCs could use this funding to support last year’s enactment of Assembly Bill 19 — the California College Promise — which allows CCCs to waive some or all of the $46 per unit fee for all first-time California resident CCC students enrolled in 12 units or more per semester during their first year. The Governor’s budget proposal would also allow funding to be used for other purposes to “advance specific student success goals.”

Reduces enrollment growth funding by $13.7 million over the three-year budget window. The proposed budget increases funding available for enrollment growth by $60 million in 2018-19, but reduces funding by $73.7 million to reflect unused enrollment growth funding in 2016-17.

The Governor’s proposed budget also provides CCCs with $264.3 million in one-time funding for deferred maintenance and an additional $32.9 million to fund a new Student Success Completion Grant, consolidating funding for the Full-Time Student Success Grant and the Community College Completion Grant and basing the new grant on the number of units a qualifying student takes each semester or each year.

Budget Proposal Includes Modest Funding Increases for CSU and UC

California supports two public four-year higher education institutions: the California State University (CSU) and the University of California (UC). The CSU provides undergraduate and graduate education to roughly 479,000 students on 23 campuses, and the UC provides undergraduate, graduate, and professional education to about 273,000 students on 10 campuses.

The Governor’s proposed 2018-19 budget includes modest increases in General Fund spending for the CSU and the UC, with the expectation that these institutions will implement certain improvements. Specifically, the proposed spending plan:

Increases funding for the CSU by $92.1 million. The Administration expects the CSU to use these funds to improve the graduation rates of two-year transfer students and four-year graduation rates, as outlined in the CSU Graduation Initiative 2025.

Increases funding for the UC by $92.1 million. The Administration’s proposal increases funding for “base growth” by 3 percent. In addition, $50 million in funding from the 2017-18 budget package is contingent on the University providing evidence of meeting several budget and enrollment expectations by May 1, 2018.

Provides $7.9 million to reverse a scheduled decrease in Cal Grant tuition awards for private nonprofit institutions. The spending plan proposes to maintain the maximum award for new students attending private nonprofits accredited by the Western Association of Schools and Colleges at $9,084. The Governor’s proposal requires these institutions to admit at least 2,500 students in 2019-20 who have earned an Associate Degree for Transfer from the California community colleges and are guaranteed junior status, and 3,000 such students in 2020-21.

Does not reflect funding to cover increased Cal Grant costs that would result from potential tuition increases at the CSU and the UC. The Governor’s budget summary notes that both the CSU and the UC have indicated that they may present tuition increases to their governing bodies, which would require increased funding for Cal Grants. For 2018-19, the CSU is considering a 4 percent tuition increase, and the UC is considering a 2.5 percent tuition increase.

Administration Proposes “Inclusive” Competitive Grant Program for Child Care and Preschool Providers

California’s child care and development system allows parents with low and moderate incomes to find jobs and remain employed while caring for and preparing children for school. State policymakers dramatically cut funding for these programs during and after the Great Recession, which hampered families’ access to safe and reliable early care and education. Even as the state’s economy continues to grow and revenues increase faster than earlier forecasted, funding for the child care and development system in the current 2017-18 fiscal year remains more than $500 million below the pre-recession level, after adjusting for inflation.

The 2018-19 budget proposal creates a new competitive grant program with one-time funding of $167.2 million ($125 million Proposition 98, $42.2 million federal TANF funds). The stated goal of the Inclusive Early Education Expansion Program is to “increase the availability of inclusive early education and care for children aged 0 to 5 years old” in order to boost school readiness and improve academic outcomes for children from low-income families and children with exceptional needs. The grants are to be targeted to areas with low incomes and low access to care. In addition, the budget proposal:

Provides $47.7 million to increase the Standard Reimbursement Rate by 2.8 percent. For providers that contract directly with the state, the proposal increases rates effective July 1, 2018 ($31.6 million Prop. 98 General Fund, $16.1 million non-Prop. 98 General Fund).

Provides $13.3 million General Fund to make permanent a hold harmless provision for voucher-based child care providers. Families can access subsidized care by using a voucher to select a child care provider of their choice. The value of these vouchers is based on the state’s Regional Market Rate Survey, which is conducted on a periodic basis. The 2017-18 budget package updated the payment rate for these child care providers using the most recent survey and included a hold harmless provision to ensure that providers would not see a decrease in payment rates. The hold harmless provision in the 2017-18 budget was temporary, and the proposed 2018-19 budget makes this hold harmless provision permanent.

Provides $8.5 million Prop. 98 General Fund to increase the number of slots in the state preschool program. The proposed budget adds 2,959 full-day state preschool slots for Local Education Agencies beginning on April 1, 2018, as stipulated in a multiyear plan included in the 2016-17 budget agreement.

Proposed Budget Emphasizes the Uncertainty Over the Fate of Medicaid and the Federal Affordable Care Act

Last year, congressional leaders made multiple attempts to repeal the Affordable Care Act (ACA) and substantially reduce federal funding for Medicaid, which provides health coverage to tens of millions of Americans with low incomes, including more than 13 million in California. (Medi-Cal is California’s Medicaid program.) While these efforts failed, the federal government has pursued other changes that threaten to destabilize insurance markets and reduce the number of people with health coverage. For example, the Republican-backed tax bill – which President Trump signed into law last month – repealed the financial penalty (effective in 2019) for people who fail to opt in for health coverage. This change is expected to both reduce the number of people with health insurance and drive up premiums for those who continue to purchase coverage on the individual market. In addition, President Trump has used his executive authority to advance a number of policies designed to weaken the ACA.

The Governor’s budget summary acknowledges the uncertainty surrounding these potential federal policy changes, including whether they would “ultimately be approved or when they would take effect.” As a result, the Governor’s proposals assumes that current federal and state health policies will remain in place.

In addition, the Governor’s proposed budget:

Projects total Medi-Cal enrollment of 13.5 million in 2018-19. This is up from 7.9 million in 2012-13, an increase that is due primarily to California’s full implementation of federal health care reform.

Projects total Medi-Cal spending of $101.5 billion in 2018-19, which is comprised primarily of federal dollars. Federal support for Medi-Cal is projected to be $67.1 billion in 2018-19, roughly two-thirds of total funding for the program. State General Fund support for Medi-Cal is projected to be $21.6 billion in the upcoming fiscal year, with other non-federal funds providing the remaining $12.8 billion.

Estimates that the state’s share of cost for the “optional” Medi-Cal expansion will be $1.6 billion in 2018-19, substantially lower than the projected federal share ($21.3 billion). In January 2014, California – as allowed by the ACA – expanded Medi-Cal eligibility to certain low-income adults who previously did not qualify for the program. For the first three years, the federal government paid 100 percent of the costs for these new Medi-Cal enrollees, who are projected to number 3.9 million in 2018-19. California began to pay a small portion of the cost in 2017, with the state’s share set to gradually increase to 10 percent in 2020 and beyond under current federal law.

Estimates that Proposition 56 (2016) will raise $1.3 billion in tobacco tax revenues during 2018-19, with most of these funds allocated to Medi-Cal. Approved by voters in 2016, Prop. 56 increased the state’s excise tax on cigarettes by $2 per pack effective April 1, 2017. The measure also triggered an equivalent increase in the excise tax on other tobacco products and – for the first time – applied the state excise tax to electronic cigarettes that contain nicotine. Prop. 56 requires that the majority of the revenues raised by the measure go to Medi-Cal. The Administration projects that Medi-Cal will receive $850.9 billion from this new funding source in 2018-19, with these dollars proposed to be allocated as follows:

$649.9 million for supplemental payments and rate increases for Medi-Cal providers;

$169.4 million “to support new growth in Medi-Cal compared to the 2016 Budget Act”; and

$31.6 million to boost funding for certain home health providers.

Governor Highlights Uncertainty of Federal Funding for the Children’s Health Insurance Program (CHIP)

CHIP is a joint federal-state program that supports health insurance for almost 9 million children throughout the US during the course of a year, including over 2 million in California. In California, CHIP-eligible children from families with incomes up to 266 percent of the federal poverty line (FPL) —$65,436 for a family of four — receive health care services through Medi-Cal. (These children previously would have been enrolled in the Healthy Families Program, which was eliminated in 2013). Through separate, smaller programs, CHIP also supports health care services for certain children whose families earn up to 322 percent of the FPL in San Francisco, San Mateo, and Santa Clara counties, as well as for pregnant women in families with incomes up to the same level.

Since late 2015, the federal government has paid 88 percent of CHIP costs in California, with the state covering the remaining 12 percent. Previously, the federal share was set at 65 percent. Last year, with the program authorized only through September 2017, the Governor assumed that Congress would reauthorize CHIP at the 65 percent level effective October 1, 2017. However, Congress failed to allocate long-term federal funding for CHIP and has only managed to approve temporary funding that expires in March 2018. The short-term extension funded CHIP at 88 percent, and the Governor expects about $150 million General Fund savings to be reflected in the May Revision. These savings are not reflected in the January proposal because the funding extension occurred after the budget was finalized.

The Governor’s proposed 2018-19 budget still assumes that Congress will eventually renew CHIP funding, at the lower 65 percent level. If Congress does not reauthorize CHIP, however, the Affordable Care Act requires California to continue coverage for those children receiving care through Medi-Cal, with a 50 percent federal share. On a conference call with stakeholders, Administration officials did not confirm that the state would continue to cover the 32,000 children and pregnant women who do not qualify for federally funded Medi-Cal.

Governor Proposes One-Time Increase to CalWORKs Single Allocation, Provides Funds to New Home Visiting Pilot Program

The California Work Opportunity and Responsibility to Kids (CalWORKs) program provides modest cash assistance for 860,000 low-income children while helping parents overcome barriers to employment and find jobs. CalWORKs is the state’s version of the federal Temporary Assistance for Needy Families (TANF) program. Counties receive most of their funding to support CalWORKs activities (including employment services and certain child care services) through the “CalWORKs single allocation,” which has historically been budgeted based on projected caseload.

Last year, in response to the continued decline in the CalWORKs caseload, the 2017-18 budget agreement reduced the single allocation by about $140 million and required the Administration and the counties to devise a new budgeting methodology to “address the cyclical nature of the caseload changes and impacts to county services.” The Governor’s 2018-19 proposed budget includes a one-time increase in the single allocation of $187 million until the revised methodology is adopted; this is an 11 percent increase relative to the 2017-18 allocation of $1.7 billion. Additionally, with the state minimum wage scheduled to increase from $11 to $12 on January 1, 2019 for large businesses, CalWORKs spending is expected to decrease by $1.2 million General Fund as more families earn an income that is above the eligibility limit (but still far below the level needed to make ends meet).

At their current levels, CalWORKs grants fail to lift most families out of “deep poverty,” which is defined as having an income that is below half of the federal poverty line ($10,210 for a family of three in 2017). The Governor does not propose any increase to CalWORKs grant levels or time limits, even though this would be necessary to fully restore cuts that state policymakers made to the program during and after the Great Recession.

The Governor’s proposal does allocate a total of $158.5 million in one-time TANF funds through 2021 for a new voluntary home visiting pilot program, with $26.7 million in the first year. Evidence-based home visiting programs offer resources and parenting skills development to new and expecting parents, particularly those who are at-risk. The proposed initiative would apply existing models currently in place in the state to serve first-time CalWORKs parents with the aim of encouraging healthy development of low-income children, promoting healthy parenting, and preparing parents for work. On a conference call with stakeholders, Administration officials indicated an implementation target date of January 2019 for the pilot program.

Governor Projects a Federal Increase for SSI/SSP Grants in 2018-19, but Does Not Provide a State Increase

Supplemental Security Income/State Supplementary Payment (SSI/SSP) grants help well over 1 million low-income seniors and people with disabilities to pay for housing, food, and other basic necessities. Grants are funded with both federal (SSI) and state (SSP) dollars. State policymakers made deep cuts to the SSP portion of these grants in order to help close budget shortfalls that emerged following the onset of the Great Recession in 2007. The SSP portions for couples and for individuals were reduced to federal minimums in 2009 and 2011, respectively. Moreover, the annual statutory state cost-of-living adjustment (COLA) for SSI/SSP grants was eliminated beginning in 2010-11, after having been suspended for several years.

California took a modest step toward reinvesting in SSI/SSP by funding a 2.76 percent COLA for the SSP portion of the grant in the 2016-17 fiscal year. This boosted the monthly SSP grant to $160.72 for individuals (an increase of $4.32) and to $407.14 for couples (an increase of $10.94). However, SSP grants were not further increased in 2017-18, and these grants would continue to remain frozen at the current levels under the Governor’s proposed 2018-19 budget.

The Administration does project that the federal government will increase the SSI portion of the grant by 2.6 percent effective January 1, 2019. As a result of this projected federal increase:

The maximum monthly combined SSI/SSP grant for individuals who live independently would increase from the current level of $910.72 to $930.72 on January 1, 2019. This projected 2019 grant level equals 92.6 percent of the current federal poverty guideline for an individual ($1,005 per month).

The maximum monthly combined SSI/SSP grant for couples who live independently would increase from the current level of $1,532.14 to $1,562.14 on January 1, 2019. This projected 2019 grant level equals 115.5 percent of the current poverty guideline for a couple ($1,353 per month).

Proposed Budget Highlights Impact of Proposition 57, Which Provides New Tools for Reducing Incarceration

Currently, about 130,000 people who have been convicted of a felony offense are serving their sentences at the state level — down from a peak of around 173,600 in 2007. Most of the individuals who are currently incarcerated — nearly 114,300 — are housed in state prisons designed to hold slightly more than 85,000 people. This level of overcrowding is equal to 134.3 percent of the prison system’s “design capacity,” which is below the prison population cap — 137.5 percent of design capacity — established by a 2009 federal court order. (In other words, the state is in compliance with the court order.) In addition, California houses nearly 15,700 individuals in facilities that are not subject to the court-ordered cap, including fire camps, in-state “contract beds,” out-of-state prisons, and community-based facilities that provide rehabilitative services.

The sizeable drop in incarceration has resulted largely from a series of policy changes adopted by state policymakers and the voters in the wake of the federal court order. The most recent reform was Proposition 57, a 2016 ballot measure that provided state officials with new tools to address ongoing overcrowding in state prisons. Prop. 57:

Gave the California Department of Corrections and Rehabilitation (CDCR) broad authority to award sentencing credits to reduce the amount of time that people spend in prison.

Requires parole consideration hearings for state prisoners who have been convicted of a nonviolent felony and have completed the full term for their primary offense.

Requires juvenile court judges to decide whether a youth accused of a crime should be tried in adult court.

With the implementation of Prop. 57, the average daily number of incarcerated adults is projected to drop from just over 130,300 in 2017-18 to about 127,400 in 2018-19 (a 2.2 percent decline), according to Administration estimates. Moreover, the Administration anticipates that by freeing up space in state prisons, Prop. 57 — along with other recent criminal justice reforms — will allow the state to end the use of one of two remaining out-of-state prison facilities by the end of the current fiscal year (June 30), and to end the use of the other facility by the fall of 2019. Currently, more than 4,200 Californians are housed in facilities in Arizona and Mississippi because there is no room for them in state prisons given the court-imposed prison population cap.

In addition, the Governor’s proposed 2018-19 budget includes:

Overall General Fund support of $11.7 billion for the CDCR, up slightly from $11.5 billion in the current fiscal year (2017-18). Spending on state corrections now makes up roughly 9 percent of total General Fund expenditures, down from 11.4 percent of total General Fund spending in 2011-12.

$131.1 million General Fund to address failing roofs and mold in various facilities, aging communications equipment, and outdated medical transport vehicles.

$26.6 million General Fund to establish a firefighter training program for formerly incarcerated adults.

$20.1 million General Fund to “address mental health treatment bed capacity issues” as well as to “monitor health care data reporting and patient referrals.”

$9.2 million General Fund to expand rehabilitative programming activities for incarcerated adults, including both career technical education and self-improvement programs.

$3.8 million General Fund for certain changes related to juvenile justice, including increasing to age 25 both the “ward age” for juvenile court commitments (up from age 23) and the “age of confinement” for superior court commitments (up from age 21). These changes are intended to allow youth involved with the juvenile justice system to benefit from rehabilitative activities designed for their age group as well as to “be more successful upon release,” according to the Governor’s budget summary.

Finally, the Administration estimates that Prop. 47 will generate net state savings of $64.4 million in 2017-18, with ongoing annual savings expected to be approximately $69 million. Approved by California voters in 2014, Prop. 47 reduced penalties for certain nonviolent drug and property crimes from felonies to misdemeanors and generally allowed people who were serving a felony sentence for these crimes at the time of Prop. 47’s passage to petition the court to have their sentence reduced to a misdemeanor term. The annual state savings from Prop. 47 are required to be allocated as follows: 65 percent to mental health and drug treatment programs, 25 percent to K-12 public school programs for at-risk youth, and 10 percent to trauma recovery services for crime victims.

Governor’s Budget Maintains Additional Resources to Address Impact of Federal Actions on Immigration

The Administration notes that more than half of all children born in California have at least one foreign-born parent and that immigrants have been critical to California’s labor force and economic growth throughout the state’s history. Given the prominence of immigrants in California’s population and the state’s economy, recent and ongoing federal actions to limit immigration and aggressively enforce immigration laws particularly impact California. These issues have been an area of particular tension between the Trump Administration and California’s state and local governments.

The Governor’s proposed budget continues an expansion of state resources included in last year’s budget to address federal actions that affect California’s immigrant residents. The proposed 2018-19 budget includes $45 million General Fund dedicated to legal services for people seeking help with securing legal immigration status, defense against deportation, and other immigration services, as well as $3 million to assist undocumented immigrants who are unaccompanied minors, both through the Department of Social Services. The Governor’s budget also maintains increased funding for the Attorney General’s office to address federal actions and proposes to make this increased funding permanent.

Budget Proposal Reflects New Funding For Transportation Approved in 2017

Last year, the Governor and Legislature passed the Road Repair and Accountability Act of 2017 (Senate Bill 1), a 10-year, $55 billion transportation package. SB 1 funds improvements in state and local transportation infrastructure by increasing the state gas tax for the first time since 1994 (raising it to its inflation-adjusted level relative to 1994) and through a series of other fuel taxes, vehicle fees, and other transportation-related fees. The Governor’s proposed 2018-19 budget includes $4.6 billion in funding provided by SB 1, split evenly between state and local transportation projects.

Administration’s Housing Proposals Implement the 2017 Legislative Housing Package

The Governor’s proposed budget includes several references to California’s high housing costs and their implications for families and individuals as well as the economy. The Governor notes the large percentage of Californians paying more than half of their incomes toward housing, the negative impact of high housing costs on job growth and inflation, and the significant gap between housing production and demand. To begin to address California’s housing affordability crisis, last year the Legislature passed, and the Governor signed, a comprehensive package of housing legislation. These bills included multiple strategies to improve housing affordability, including directly financing affordable housing production, facilitating private-market housing production, and increasing local accountability for accommodating a fair share of new housing development.

The housing proposals in the Governor’s budget reflect implementation of components of the legislative housing package. Specifically, the Governor’s proposed budget:

Allocates $245 million from the real estate transaction fee established by Senate Bill 2 for affordable housing and homelessness programs. Funds from this new fee, which are expected to total $258 million annually, must be primarily targeted to homelessness services and local government capacity building for housing planning in this first year of implementation (with funds in future years largely dedicated to affordable housing development).

Provides $3 million General Fund to the Department of Housing and Community Development to implement various changes included in the housing package.

Anticipates voter approval of the $4 billion housing bond that will be placed on the November 2018 ballot as another component of the legislative housing package, while allocating $277 million of new housing bond funds toward the Multifamily Housing Program. This program supports development, rehabilitation, and preservation of rental housing affordable to lower-income households.

These proposals, combined with continuation of existing programs, loans, and tax credits administered through various state departments and agencies, bring the total proposed state funding for affordable housing and homelessness to $4.37 billion.

Governor Proposes Extending and Expanding the California Competes Tax Credit Program

California Competes provides income tax credits to certain businesses in order to encourage companies to move to, stay in, or expand in California. The program was established in 2013, together with two other economic development programs, as a replacement for the state’s Enterprise Zone programs. Under current law, California Competes will expire in 2017-18.

The Administration proposes extending California Competes for five years and making $180 million in credits available to qualifying businesses in each of those years. The proposed budget also provides $20 million annually to assist small businesses and “reconstitutes” $50 million per year to encourage businesses to hire people facing barriers to work, such as parolees, CalWORKs parents, and veterans.

A recent Legislative Analyst’s Office (LAO) report recommended that the Legislature end California Competes based on a preliminary evaluation of the program. Specifically, the LAO found that while the “executive branch has made a good faith effort to implement California Competes,” the program produced “windfall benefits” to businesses in some cases without any increase in overall state economic activity. Additionally, the LAO noted that it is difficult to assess the effectiveness of targeted tax incentives and suggested that “broad-based tax relief” for all businesses would be preferable.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

The tax plan proposed by President Trump and Republican congressional leaders would among other provisions permanently repeal the federal estate tax, which affects only the very wealthiest Americans – those with estates valued in the top 0.2 percent. Eliminating the estate tax would reduce federal revenue at the same time that the President and Congress have proposed significant spending cuts that would harm many important public services and systems that improve the lives of individuals and families. Outright repeal of the estate tax would follow congressional actions that have eroded this tax over the past couple of decades. Since 2001, for example, Congress has cut the top rate for the estate tax from 55 percent to 40 percent, increased the size of estates that are exempt from the tax, and phased out the portion of the estate tax that is shared with states, a move that eliminated all estate tax revenue received by California.

To help shed light on what’s at stake with the proposed elimination of the federal estate tax, this post describes how this tax works, shows the very small share of Americans it affects, and discusses some fundamental concerns raised by its potential repeal.

What Is the Estate Tax?

The estate tax is levied on large accumulations of wealth that are transferred from the estate of a person who has died to the estate’s beneficiaries. The estate tax serves as a “back stop” to the income tax, ensuring that income that is not taxed during an individual’s lifetime, such as unearned capital gains, is taxed when it passes from one generation to the next.

Repealing the Estate Tax Would Eliminate a Revenue Source That Supports Key Services

The estate tax will raise an estimated $20 billion in 2017, according to the Tax Policy Center, and its repeal would reduce federal revenue by an estimated $240 billion over the next decade. While estate tax revenues are small in comparison to overall federal revenue, they provide funding for a range of essential public services and systems from health care to education to environmental protection. To put this in perspective: The estate tax will raise significantly more in a decade than the federal government will spend on the Food and Drug Administration, the Centers for Disease Control and Prevention, and the Environmental Protection Agency combined, according to the Center on Budget and Policy Priorities. This is despite a decline in estate tax revenue since the late 1990s. For example, during the 10-year period from 1997 through 2006 the estate tax raised more than $300 billion, after adjusting for inflation. This is one-fourth more than the estate tax is projected to raise during the next decade.

The Very Small Share of Americans Who Pay Estate Taxes Today Is a Fraction of Those Who Paid the Tax 20 Years Ago

In 2017, just 2 out of every 1,000 estates are estimated to owe any estate tax. This is one-tenth of the share of estates subject to the tax 20 years ago. In the late 1990s, more than 45,000 estates each year — around 2 percent of those who died — paid estate taxes, but that number is estimated to fall to 5,500 in 2017 (see chart below). This drop is due to a large increase in the size of estates that are exempt from tax. Congress increased the estate tax exemption from $650,000 per person ($1.3 million per couple) in 2001 to $5.49 million per person ($10.98 million per couple) in 2017. Moreover, large loopholes enable many estates to avoid taxes altogether. As a result, less than half of the estimated 11,300 estates that are expected to file an estate tax return will owe any taxes in 2017. And while estate tax opponents claim that the tax burdens small farms and businesses, just 80 of these entities are expected to pay any estate tax this year, according to Tax Policy Center estimates.

The Largest Share of Federal Estate Tax Revenue Comes from California

The federal government collects a much larger share of estate tax revenue from California than from any other state. Californians paid $3.9 billion in estate taxes — more than 20 percent of total federal estate tax revenue — in 2016, the most recent year for which IRS data are available. And more than 1 out of every 5 Americans who paid estate taxes last year resided in California.

The Few Who Owe Estate Taxes Pay Far Less Than the Top Tax Rate

Although the top estate tax rate is currently 40 percent, the Tax Policy Center estimatesthat in 2017 the average tax rate paid by the few estates subject to the tax will be less than half that amount (17.0 percent). Taxable estates worth between $5 million and $10 million will pay less than a 9 percent tax rate, on average, and those estates worth more than $20 million will pay an average estate tax rate of less than 20 percent. One reason for such a low tax rate is that estate taxes are levied only on the portion of an estate’s value that exceeds the exemption level. For example, the estate of a couple worth $12 million would owe taxes on only around $1 million, based upon the current $5.49 million exemption per person (nearly $11 million a couple). Moreover, policymakers have enacted generous deductions and other discounts that can shield a large portion of an estate’s remaining value from taxation.

The Very Wealthiest Americans Pay the Largest Share of the Estate Tax

The estate tax is the most progressive part of the US tax code because it affects only Americans who are most able to pay. As a result, the estate tax helps make the US tax system more equitable and fair. And the very wealthiest not only account for the largest share of the few Americans subject to the estate tax, but their estates account for the largest share of estate tax revenue. The top 10 percent of income earners account for two-thirds of all estates subject to tax and will pay 88 percent of all estate taxes in 2017, according to Tax Policy Center estimates. Further, the top one-tenth of 1 percent of income earners account for only 4 percent of taxable returns, but will pay $5.5 billion — more than one-quarter of all estimated estate tax revenue this year.

Repealing the Estate Tax: Benefitting the Wealthy Few Would Cost a Lot

Repeal of the federal estate tax would provide a significant tax break to the very wealthiest Americans, including Californians, with this loss of revenue very likely paid for by cuts to vital services that help the less fortunate make ends meet and access greater opportunity. Although the estate tax affects only a small number of the very wealthy, it raises substantial revenue that supports key public systems and services. This makes the proposal to repeal the estate tax particularly unfair, as it comes at the same time that the President and Congress have proposed significant cuts to many of these important services. If Congress acts to eliminate the estate tax, less well-off taxpayers would have to make up for the lost revenue in order to help pay for these services, face reductions to these services, or bear the burden of increases in the national debt, which could eventually force cuts to health care, education, scientific research, and other vital programs.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

This post is the first in a California Budget & Policy Center series that will discuss the tax cuts proposed by President Trump and Republican congressional leaders and explore the implications for Californians and the nation.

Now that Republican leaders in Washington, DC, have moved on from their latest failed effort to repeal the Affordable Care Act, they have quickly turned their attention to a combination of tax cuts and deep spending reductions that together would have dire implications for many low- and middle-income people in California and across the nation. In September, the Trump Administration and leaders in the US House of Representatives and Senate unveiled their unified tax framework, which would provide significant tax cuts that predominantly benefit the wealthy.

Republican leaders are developing the full details of their tax plan in parallel with efforts to enact a budget for fiscal year 2018, and in order to offset the costs of tax cuts they are also seeking draconian cuts in spending on an array of critical programs and services. Congressional rules allow for a “fast track” process to pass tax cuts and certain spending reductions with a simple majority in the Senate (without needing any Democratic votes) — a process known as “reconciliation.” If GOP leaders pursue their proposed tax cuts, they will enact a massive redistribution of wealth that would be, in part, paid for through budget cuts to programs that help low- and middle-income families make ends meet and access greater economic opportunity.

Latest GOP Tax Plan Skews Benefits to the Wealthy

Despite their stated goal of providing a tax cut for middle-class families, the latest GOP framework would provide the vast majority of its benefits to wealthier Americans and corporations. For instance, the current tax framework is most specific about repealing the estate tax; ending the Alternative Minimum Tax (AMT); cutting corporate tax rates; potentially lowering the highest income tax rates; and preserving tax preferences for mortgage interest — in short, a range of benefits that accrue disproportionately to wealthier households.

In contrast, the tax proposal’s benefits for working families are less explicit — and apparently far less substantial. Based on information released so far, the clearest proposals benefiting middle-class households are a doubling of the standard deduction and an unspecified increase in the Child Tax Credit, though the tax framework also includes some vague language about future “additional measures.” However, accounting for changes like the elimination of personal exemptions and an increase in the bottom marginal income tax rate for some filers, many low- and middle-income families could see little benefit, if any.

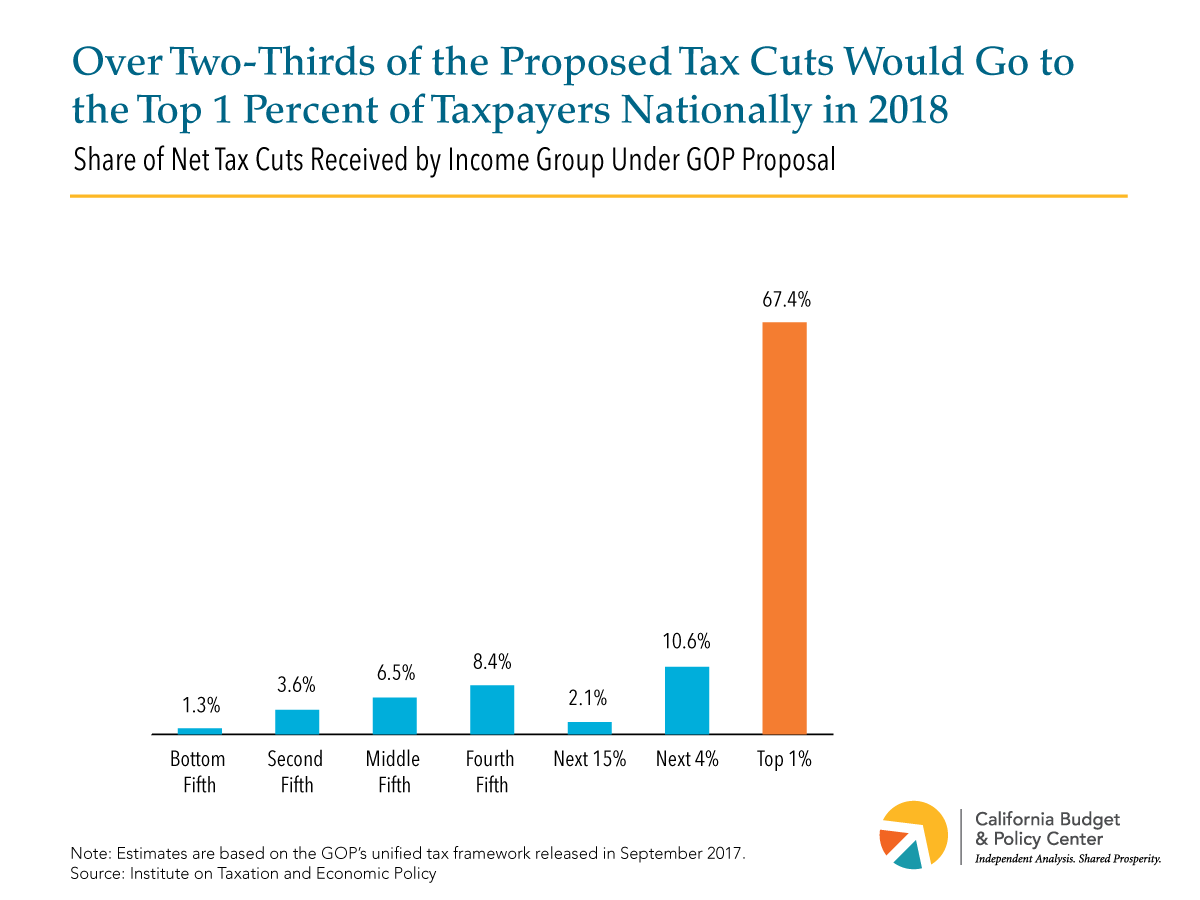

Though the President had promised that the rich “will not be gaining at all with this plan,” the numbers tell a different story. In fact, a recent analysis of the GOP tax package points to a vastly unfair distribution of its benefits. According to the nonpartisan Institute on Taxation and Economic Policy, the top 1 percent of households — a group whose annual incomes are at least $615,800 and average over $2 million — would receive over two-thirds of the tax cuts in 2018 (see chart below), an amount equivalent to 4.3 percent of this group’s pre-tax income. The bottom 60 percent of Americans, however, would receive 11.4 percent of the tax cuts, equal to a meager 0.7 percent of this group’s total income. What’s more, these Americans would be most likely to be affected by corresponding federal spending cuts that GOP leaders are proposing to offset the overall cost of the tax cuts.

In other words, the latest GOP tax plan is heavily skewed to benefiting the wealthiest households in the US, likely at the expense of many low- and middle-income households.

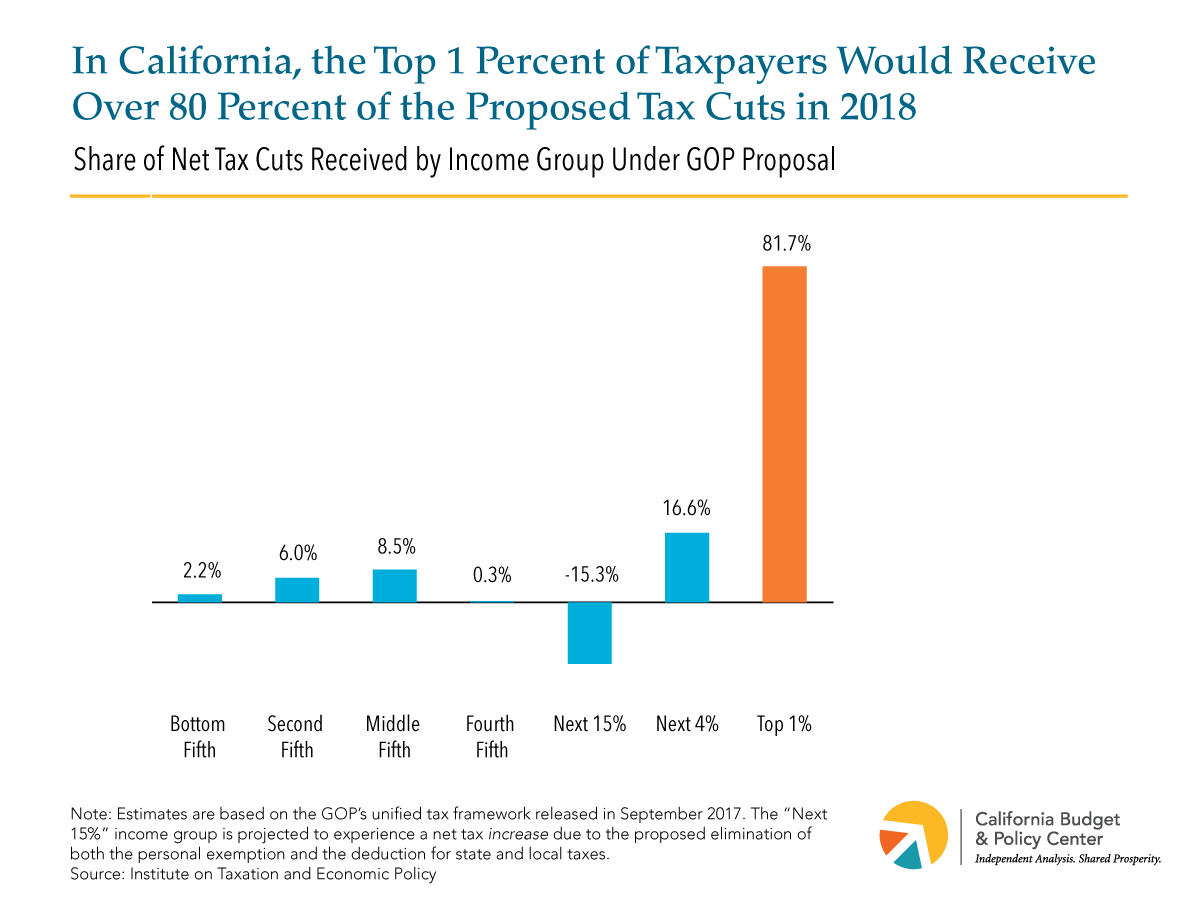

The regressive impacts of this tax framework may be even greater in some states. Here in California, an even larger share of the tax cuts — almost 82 percent — would go to just the top 1 percent of earners in 2018, with another 16.6 percent going to the next 4 percent, and the rest of the benefits spread across the remaining income levels (see chart below). The richest 1 percent of California earners — those making more than $864,900 a year — would receive an average tax cut of $90,160. In contrast, middle-income households — making between $47,200 and $75,500 a year — would receive a much smaller average tax cut of $470, and the lowest income households — those making less than $27,300 a year — would receive a tax cut of $120. For many of these low- and middle-income households the benefits of these marginal tax cuts would likely be offset by significant cuts to federal programs and services including health care, housing, food assistance, and job training assistance, among others.

Revenue Losses Would Hurt the Economy and Struggling Households

The latest GOP plan would also come at a huge cost in lost revenues. Estimates of the resulting revenue loss vary from $2.2 trillion to $2.4 trillion over the next decade. While the plan purports to add $1.5 trillion to the federal debt over the next decade, yet-to-emerge details about the plan and likely compromises on some of the plan’s more controversial proposals (such as the elimination of the federal deduction for state and local taxes, widely known as the “SALT” deduction) could result in a much larger increase in federal debt.

The Trump Administration insists that the tax cuts will boost economic growth and pay for themselves, but analysts agree that this scenario is highly unlikely. Rather, in order to minimize the costs of the tax plan, the GOP would likely respond by attempting to further slash entitlement programs like the Supplemental Nutrition Assistance Program (SNAP), Medicaid, Medicare, and other parts of the federal budget that include funding for housing, job training, and other assistance. These cuts would likely have negative impacts on the economy by destabilizing economic conditions of millions of households who rely upon those programs to help make ends meet and to access greater economic opportunity.

Tax Plan Is Particularly Bad for California

The combination of GOP tax and budget proposals would be particularly harmful for many Californians and for the state of California.

In terms of budget cuts, the significant cuts to Medicaid and SNAP (Medi-Cal and CalFresh in California) would likely result in reduced or eliminated benefits for millions of Californians with low incomes — over 13 million (34.2 percent) who are enrolled in Medi-Cal and over 4 million (10.8 percent) who receive food assistance through CalFresh.

These cuts would also likely undermine California’s fiscal health, forcing state leaders to choose between destabilizing the state budget by trying to fill fiscal holes as a result of federal tax and budget cuts or, on the other hand, destabilizing vulnerable individuals and communities across the state by reducing benefits.

Some California taxpayers would also see significant increases in their tax bills. For instance, the majority of Californians earning $129,500 to $303,200 annually — which can actually be considered a “middle class” income in the many parts of California where costs of living are significantly higher than much of the country — would see a nearly $4,000 increase in their annual federal tax bills. This increase is largely the result of the repeal of the SALT deduction, mentioned earlier.

In short, the GOP tax and budget plans would increase the tax bills of some Californians, providing minimal tax cuts for many others, while reducing vital public assistance, all in pursuit of providing large tax cuts to the very wealthiest households and corporations.

A Better Path

Congress can still choose a more fiscally and economically responsible path. Instead of providing tax cuts that overwhelmingly go to the wealthiest households and corporations, cutting vital public programs and services, losing trillions of dollars in revenues, and adding significantly to the federal debt, Congress could seek to enact policies that move our nation in the right direction. Federal tax and budget policies should focus on making investments that enable our communities to thrive, help the most vulnerable, and broaden economic prosperity. Any federal tax cuts should be weighted toward those who need them most, and should be revenue-neutral, with lost revenues from tax cuts offset by other revenue increases (new taxes or closed loopholes) that are fairly distributed across the income spectrum.

It will be important to pay attention to which path our elected officials in Washington choose in the coming weeks and months. Their actions may mean that Californians would face the prospect of holding their congressional representatives accountable for decisions that would disproportionately — and negatively — impact our state.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

State and National Leaders Must Do More to Promote Economic Security and Opportunity

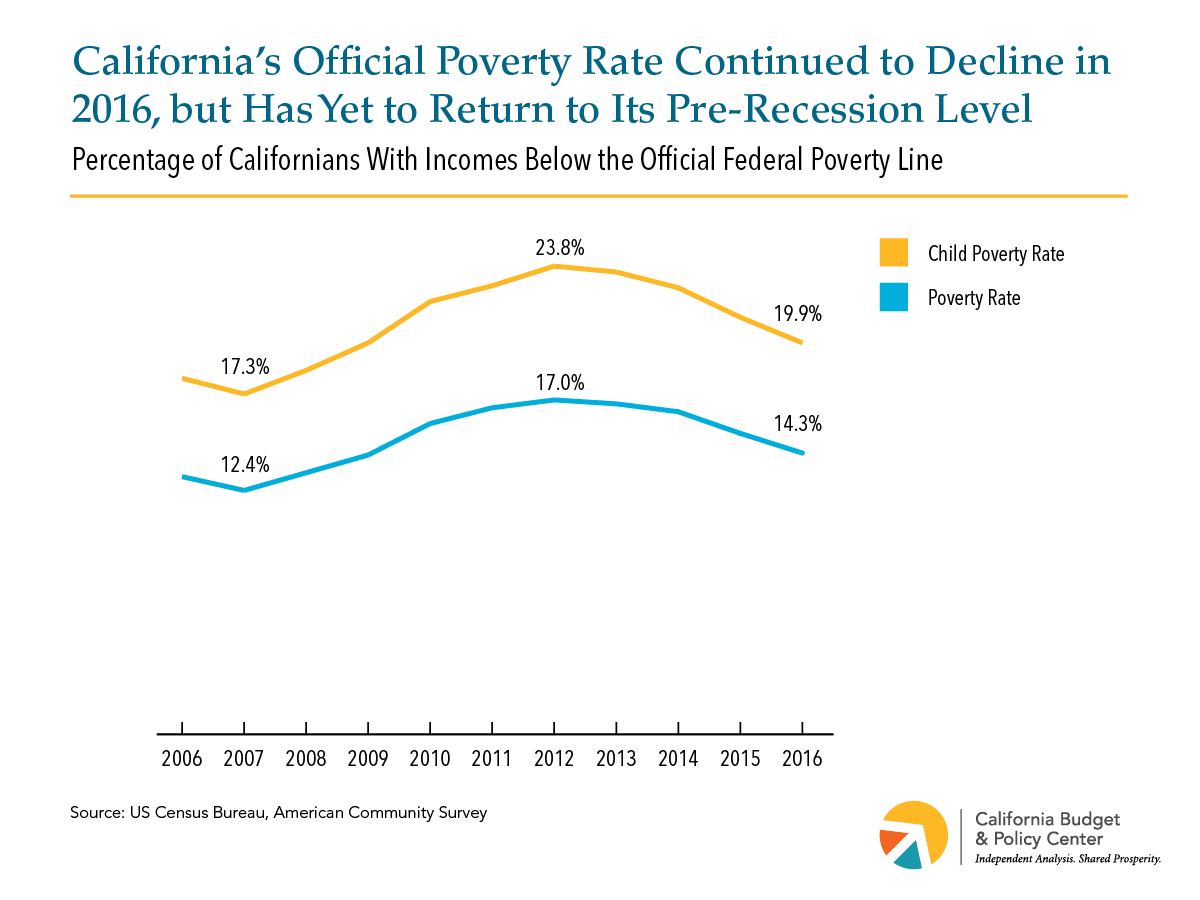

New Census figures released today show that millions of people in California continue to struggle to get by on extremely low incomes in spite of our state’s recent economic gains. More than 5.5 million Californians, including almost 1.8 million children, lived in poverty in 2016 based on the official poverty measure. In addition, poverty remained more widespread last year than it was in 2007 when the national recession began. Specifically, 14.3 percent of Californians had incomes below the official poverty line in 2016, down from a recent high of 17.0 percent in 2012, but still well above the state poverty rate in 2007 (12.4 percent). Also, roughly 1 in 5 California children lived in poverty last year (19.9 percent), down from a recent high of 23.8 percent in 2012, but still well above the child poverty rate in 2007 (17.3 percent).

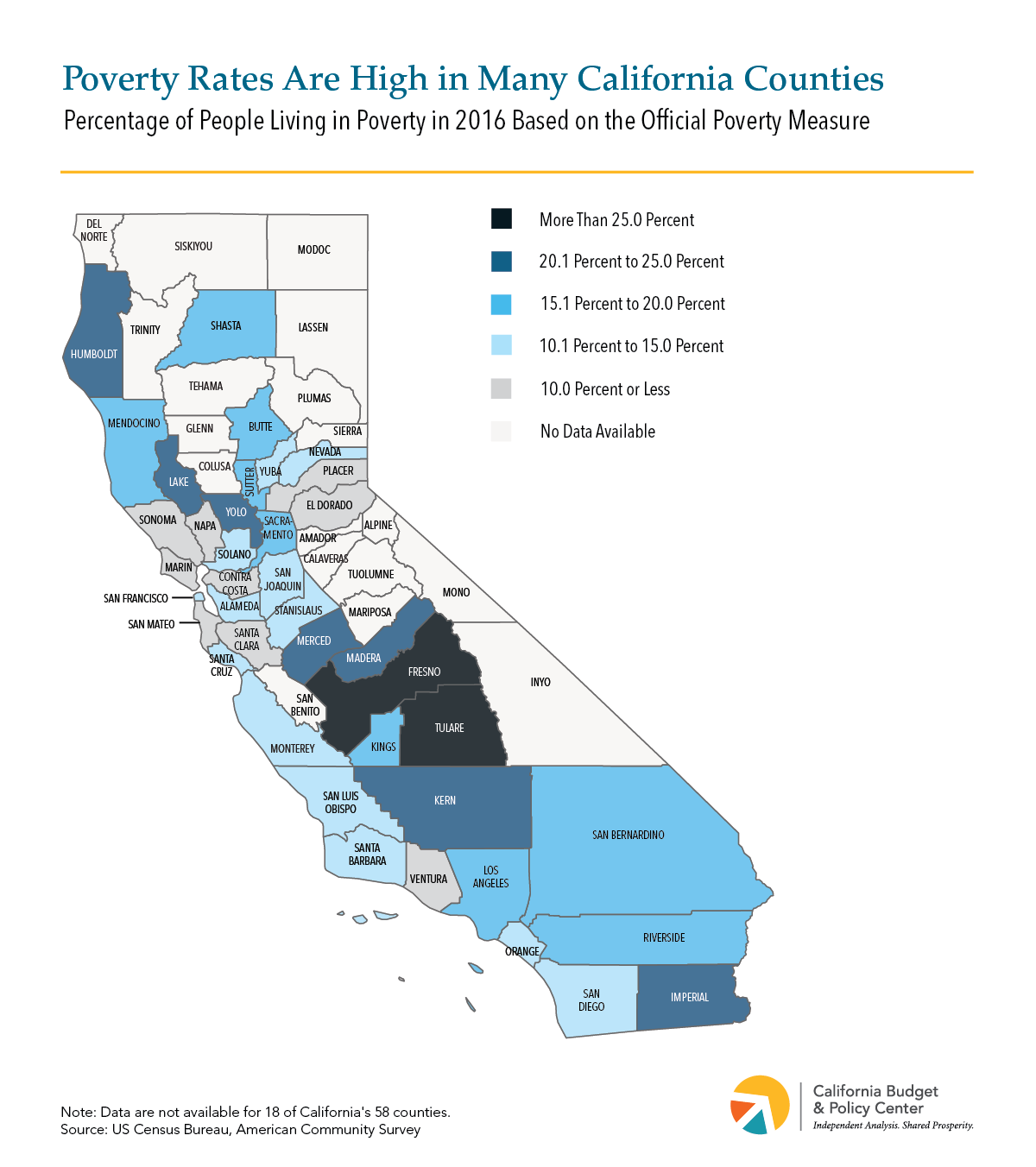

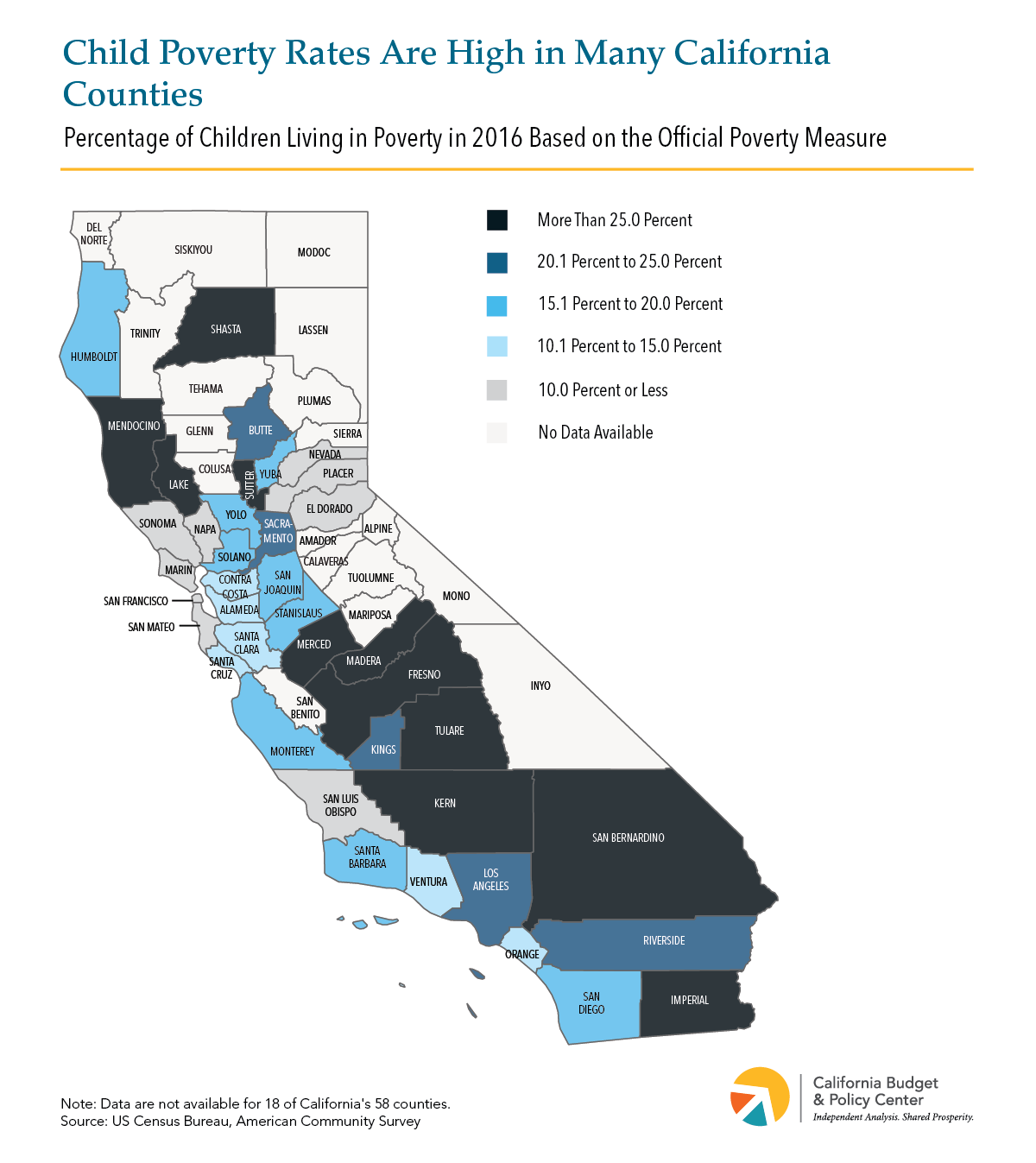

The latest Census figures also show that there are stark differences in people’s economic well-being across California’s counties. The 2016 official poverty rate ranged from a low of 6.5 percent to a high of 25.6 percent across the counties, while the official child poverty rate ranged from 5.2 percent to 37.9 percent. More than 1 in 5 people lived in poverty in nine counties, most of which are in the Central Valley (see Map 1). Additionally, more than 1 in 5 children lived in poverty in 16 counties, including six counties — again, most in the Central Valley — where over 30 percent of children were in poverty (see Map 2).

Although the Census figures published today show that poverty remains high, they understate the extent of hardship in California because they reflect an outdated measure of poverty. Census figures released earlier this week based on an improved measure — the Supplemental Poverty Measure (SPM) — which accounts for the high cost of housing in many parts of the state, show that roughly 8 million Californians per year, 1 in 5 state residents (20.4 percent), could not adequately support themselves and their families between 2014 and 2016. Under this more accurate measure of hardship, California continues to have the highest poverty rate of the 50 states.

The new Census poverty figures underscore the need for state and national leaders to do more to ensure that all people can share in our state’s economic progress. Specifically, policymakers should:

Reject steep cuts to economic security programs that help families make ends meet and get ahead. A majorityof adults will experience economic hardship for at least one year during their prime working years, and nearly half will turn to a major public support, such as SNAP food assistance (CalFresh in California), to get back on their feet. These supports not only lift millions of Californians out of poverty each year, but also help children succeed over the long-term, according to research. Yet federal policymakers have proposed slashing critical supports that promote economic security and opportunity. If enacted, these cuts would drive California’s already high poverty rate even higher and threaten the future of our state’s children. People in communities all throughout the state would likely be harmed.