What is a Supermajority Vote and Why Does it Matter in California?

October 2025 | By the California Budget & Policy Center

Watch to learn more

Some decisions in California’s Legislature require more than a simple majority — they need a supermajority, or two-thirds vote. But what does that really mean, and why does it matter for Californians?

In this short explainer, we break down how Proposition 26 changed the rules around taxes and fees, what kinds of actions require a supermajority vote, and how this impacts the ability of lawmakers to make policy decisions that affect everyday people.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

El proceso legislativo, también conocido como el proceso de proyectos de ley, proporciona una vía clave para que los californianos que desean cambiar la ley estatal puedan hacerlo a través de la legislatura del estado.

Cada año, los miembros de la asamblea legislativa y el senado presentan conjuntamente miles de proyectos de ley que avanzan a través del proceso legislativo parcial o totalmente. Estos proyectos proponen cambios a uno o más de los casi 30 códigos estatales de California y estos cambios entran en vigencia solo si el proyecto de ley es aprobado por ambas cámaras y firmado por el gobernador.

Las propuestas de modificar la Constitución del estado también pasan por el proceso legislativo. Aunque las modificaciones constitucionales de la asamblea legislativa y el senado no requieren la firma del gobernador, sí necesitan la aprobación de los votantes para poder entrar en vigencia.

El proceso legislativo funciona de acuerdo a normas delineadas en la Constitución del estado, las leyes estatales y los acuerdos de ambas cámaras (“normas conjuntas”) adoptados por la asamblea legislativa y el senado al inicio de cada sesión legislativa de dos años.

Las normas escritas y no escritas exclusivas de cada cámara, así como de diversos comités dentro de cada cámara y que cambian de un año a otro, también moldean el proceso legislativo y las participaciones de participación del público.

Es importante resaltar que el proceso del presupuesto estatal ofrece una vía separada para cambiar la ley estatal a través de la legislatura (usando proyectos de ley “tráiler”). Comparado con el proceso legislativo, el proceso de presupuesto estatal tiene normas, plazos y, en algunos casos, encargados de tomar decisiones distintos. Quienes abogan por el cambio legislativo usan tanto el proceso de presupuesto estatal como el legislativo para impulsar sus metas políticas. Sin embargo, el resto de esta guía se concentra exclusivamente en el proceso legislativo.

Oportunidades para la participación del público en el proceso legislativo

El público tiene muchas oportunidades de interactuar con los legisladores estatales durante el proceso legislativo. Por ejemplo, las personas pueden:

Sugerir ideas de proyectos de ley a los miembros de la legislatura.

Desarrollar / renovar relaciones con los legisladores y su personal para desarrollar familiaridad y confianza, elementos cruciales para obtener autores de proyectos de ley e impulsar la legislación.

Conocer a los legisladores y a su personal, así como miembros del gobierno del gobernador para defender legislación y abordar cualquier inquietud.

Escribir cartas a los comités y a legisladores individuales para compartir opiniones sobre los proyectos de ley que se han presentado.

Asistir a audiencias de comités legislativos para compartir opiniones sobre los proyectos de ley durante los períodos de comentario público.

Instar al gobernador a que firme o vete una ley.

Comités de política

Los miembros de comités de políticas de la asamblea de legisladores y el senado consideran las consecuencias políticas de un proyecto de ley. El liderazgo de cada cámara asigna los proyectos de ley a comités de política según el tema de los proyectos y otros factores. Los proyectos de ley pueden ser revisados por un solo comité de política en cada cámara o por varios comités de política.

El senado estatal tiene más de 20 comités de política actuales, y la asamblea tiene más de 30. El Comité de Educación de la asamblea legislativa (Assembly Education Committee) y el Comité de Ingresos e Impuestos del senado son algunos ejemplos. Los proyectos de ley que se aprueban en esta etapa, potencialmente con modificaciones, se transfieren al comité de apropiaciones para revisarse en más profundidad.

Los comités de asignaciones y el “archivo de asuntos pendientes”

Los comités de asignaciones calculan el costo de los proyectos de ley. Si el costo alcanza o supera ciertos umbrales, en general el proyecto se coloca en el archivo de asuntos pendientes del comité, que esencialmente es una “sala de espera” para los proyectos que se examinan en mayor profundidad. Los umbrales de costo son relativamente bajos en ambas cámaras. En el senado, el umbral varía entre $50,000 y $150,000, depende del fondo estatal del que se tomará el dinero. El umbral en la asamblea legislativa es $150,000, sin importar cuál sea el fondo.

Dos veces por año, los comités de apropiaciones organizan audiencias donde anuncian rápidamente el destino de cientos de proyectos de ley que se encuentran en su archivo de asuntos pendientes. Los proyectos que se sacan del archivo de asuntos pendientes mediante un voto, frecuentemente con enmiendas, pasan a la asamblea legislativa o el senado. Los proyectos de ley que continúan “en suspenso” en el comité de apropiaciones quedan inactivas por el resto del año.

Los proyectos de ley pueden quedar en suspenso por una variedad de razones, inclusive preocupaciones por su costo. Sin embargo, típicamente los directores de los comités no explican públicamente por qué algunos proyectos pasan a la asamblea legislativa o el senado y otros se mantienen en suspenso.

Votos formales de toda la legislatura: Mayoría simple o súper mayoría

Una vez que un proyecto de ley es aprobado por el comité final en su “cámara de origen”, se programa para debatirse y votar en el pleno de la cámara. La mayoría de los proyectos de ley solo necesitan una mayoría simple para ser aprobados: 41 votos en la asamblea legislativa de 80 miembros y 21 votos en el senado de 40 miembros.

Sin embargo, se requieren dos tercios (una súper mayoría) de los votos en cada cámara si el proyecto de ley:

Genera un impuesto nuevo o aumenta un impuesto existente.

Contiene una cláusula de “urgencia” que le permite entrar en vigencia de inmediato en lugar de esperar hasta el 1 de enero (la fecha típica).

Propone enmendar la Constitución del estado, un cambio que en última instancia debe ser aprobado por una mayoría de los votantes en una elección estatal.

Enjuagar y repetir: El proceso se traslada al senado estatal

Si un proyecto de ley es aprobado en la primera cámara, pasa a la cámara alta, donde se repite el proceso: comités de política, comité de apropiaciones, voto de la cámara en pleno. Típicamente los proyectos de ley son modificados una vez más en esta etapa. Si se aprueban con enmiendas, el proyecto vuelve a la cámara baja para una votación de “conformidad”. Los proyectos de ley aprobados con un voto de conformidad pasan al gobernador para su consideración final.

Aprobación o veto: Los proyectos de ley aprobados se envían al gobernador.

Una vez que un proyecto de ley recibe la aprobación legislativa final, se le envía al gobernador, quien puede:

Firmar el proyecto de ley para que se convierta en ley.

Permitir que el proyecto de ley se convierta en ley sin una firma.

Vetar, rechazar, el proyecto de ley. La legislatura puede anular un veto con dos tercios de los votos en cada cámara. Sin embargo, la anulación de vetos es extremadamente infrecuente.

Típicamente, los proyectos de ley aprobados por mayoría simple entran en vigencia el 1 de enero del año calendario siguiente. Los estatutos urgentes, aumentos de impuestos y otros proyectos de ley específicos entran en vigencia en cuanto se convierten en ley.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Californians typically pay more in federal taxes than the state receives in federal spending each year, making California a “donor state.”1All years in this fact sheet represent federal fiscal years (FFYs), which begin every October 1 and end the following September 30. The data presented in this fact sheet differs from the data included in an earlier Budget Center fact sheet — published in February 2025 — for a few reasons. First, this fact sheet analyzes data for nine fiscal years (FFYs 2015 to 2023), whereas the earlier fact sheet displayed these data for only a single fiscal year (FFY 2022). Second, this fact sheet displays federal spending data in two ways — with and without federal COVID funds — whereas the earlier fact sheet displayed spending data only with COVID funds. Finally, the data for FFY 2022 differ across the two fact sheets because the Rockefeller Institute of Government recently revised the FFY 2022 data. Between federal fiscal years (FFYs) 2015 and 2023, federal taxes paid by California residents and businesses exceeded federal spending in every year except 2020, 2021, and 2023.2FFY 2023 is the most recent year for which the Rockefeller Institute of Government’s 50-state analysis is available. In other words, California was a donor state in six out of the nine fiscal years for which data are available.

California likely would have been a donor state in additional years during this period if not for federal COVID funding. Since 2020, federal expenditures have included the substantial — but temporary — support provided to states, businesses, and individuals to address the COVID pandemic. These one-time COVID funds caused federal expenditures in California to jump significantly, which in turn has understated California’s role as a donor state.3In the four years leading up to the start of the pandemic in FFY 2020, annual federal spending in California hovered between $400 billion and $450 billion. That number jumped to over $750 billion in FFY 2020 as the pandemic took hold and federal COVID spending ramped up. Federal spending in California remained above $600 billion as recently as FFY 2023.

Excluding temporary COVID funds from the analysis provides a more accurate picture of the long-term underlying fiscal trends and California’s true position as a donor state. Using this alternative analysis, between FFYs 2015 and 2023, Californians paid more in federal taxes than the state received in federal spending in eight out of these nine years (2020 is the exception). For example, Californians’ federal taxes exceeded federal spending — excluding COVID spending — by $55 billion in 2021, $101 billion in 2022, and $17 billion in 2023.

Why Is California a Donor State?

Why do Californians typically contribute more to the federal treasury than the state gets back in federal funding? The explanation touches on both the spending and revenue sides of the equation.

On the spending side:

States with higher poverty rates, a large population of older adults, major federal facilities (such as military bases), a large volume of federal contracts, and/or a substantial federal employee presence are likely to receive a disproportionate share of federal funds. These factors contribute to relatively higher federal spending in many other states (on a per capita basis) compared to California.

On the revenue side:

States with more wealthy residents and high per capita incomes — like California — account for a disproportionate share of federal tax revenue due to the progressive federal tax system.

With Trump-Era Federal Budget Cuts, the Gap Between California’s Federal Tax Contributions and Federal Spending in the State Will Increase

In July 2025, President Trump signed into law a budget bill (H.R. 1) that will deeply harm Californians by cutting spending for essential programs like health care, food assistance, and education in order to help fund massive tax breaks to the wealthy and corporations, and increased immigration enforcement. The spending cuts included in H.R. 1 will disproportionately impact families with low incomes, immigrants, and communities of color, pushing more people into poverty and widening racial and economic inequities across the state.

State policymakers can mitigate the harm of H.R. 1., however, the massive federal funding cuts are too large to be entirely backfilled with state dollars. As a result, essential services like Medi-Cal health coverage and CalFresh food assistance are in jeopardy as state leaders assess how to address the impact of harmful federal reductions.

H.R. 1 and the Federal Budget

H.R. 1, the harmful Republican mega bill passed in July 2025, will deeply harm Californians by cutting funding for essential programs like health care, food assistance, and education.

See how California leaders can respond and protect vital supports.

Moreover, as the provisions of H.R. 1 are implemented through 2028, the gap between what Californians pay in federal taxes and federal spending in the state will grow larger.

This is because Californians will continue to disproportionately contribute to federal revenues whereas California will get back even less of those dollars as deep cuts to health care, food assistance, and other vital services take effect.

Federal Tax Dollars Should Be Used to Strengthen Essential Services

California contributes much to the nation thanks to the creativity, vitality, and hard work of the nearly 40 million people of diverse backgrounds who call the Golden State their home.

Federal tax dollars — including Californians’ very generous contributions to the federal treasury — should be used to strengthen vital public services and help all people make ends meet, rather than helping corporations and the wealthy avoid paying their fair share of federal taxes.

Update: This fact sheet was revised in August 2025 to include newly released federal tax and spending data from the Rockefeller Institute of Government (federal fiscal years 2015–2023), with revised figures and updated charts.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

All years in this fact sheet represent federal fiscal years (FFYs), which begin every October 1 and end the following September 30. The data presented in this fact sheet differs from the data included in an earlier Budget Center fact sheet — published in February 2025 — for a few reasons. First, this fact sheet analyzes data for nine fiscal years (FFYs 2015 to 2023), whereas the earlier fact sheet displayed these data for only a single fiscal year (FFY 2022). Second, this fact sheet displays federal spending data in two ways — with and without federal COVID funds — whereas the earlier fact sheet displayed spending data only with COVID funds. Finally, the data for FFY 2022 differ across the two fact sheets because the Rockefeller Institute of Government recently revised the FFY 2022 data.

In the four years leading up to the start of the pandemic in FFY 2020, annual federal spending in California hovered between $400 billion and $450 billion. That number jumped to over $750 billion in FFY 2020 as the pandemic took hold and federal COVID spending ramped up. Federal spending in California remained above $600 billion as recently as FFY 2023.

You may also be interested in the following resources:

SACRAMENTO, CA — The California Budget & Policy Center (Budget Center), in collaboration with the California Immigrant Policy Center (CIPC), released a new report today: How Federal and State Budget Cuts Threaten Latinx Californians. The report details how harmful recent federal and state budget cuts are slashing access to health care, food assistance, child care, … Continued

California policymakers should ensure that profitable corporations pay their fair share in state corporate taxes — which represent a tiny share of their expenses — to support the public services that Californians need. This is especially urgent to help mitigate the harms of the harmful federal cuts to health care, food assistance, and other basic needs programs.

State leaders should end the state’s most costly corporate tax break — the water’s edge loophole, which allows corporations to avoid around $3 billion in California taxes each year and deprives the state of needed resources to address the most pressing concerns facing Californians.

As state leaders look to blunt the harm of the federal budget on Californians with low incomes and the state’s finances, it’s clear that California’s corporate tax structure is in need of repair. While large, profitable corporations benefit from new federal tax breaks, California policymakers must ensure these businesses pay their fair share in state taxes. There is no one-size-fits-all solution: different options can all complement each other. For example, limiting corporate tax credit usage will raise revenues by itself but will also prevent erosion of the revenue potential from ending the water’s edge loophole.

MORE IN THIS SERIES

To learn more about the water’s edge election, net operating losses, tax credits, corporate tax rates, and options for common-sense reform, see the other fact sheets in this series:

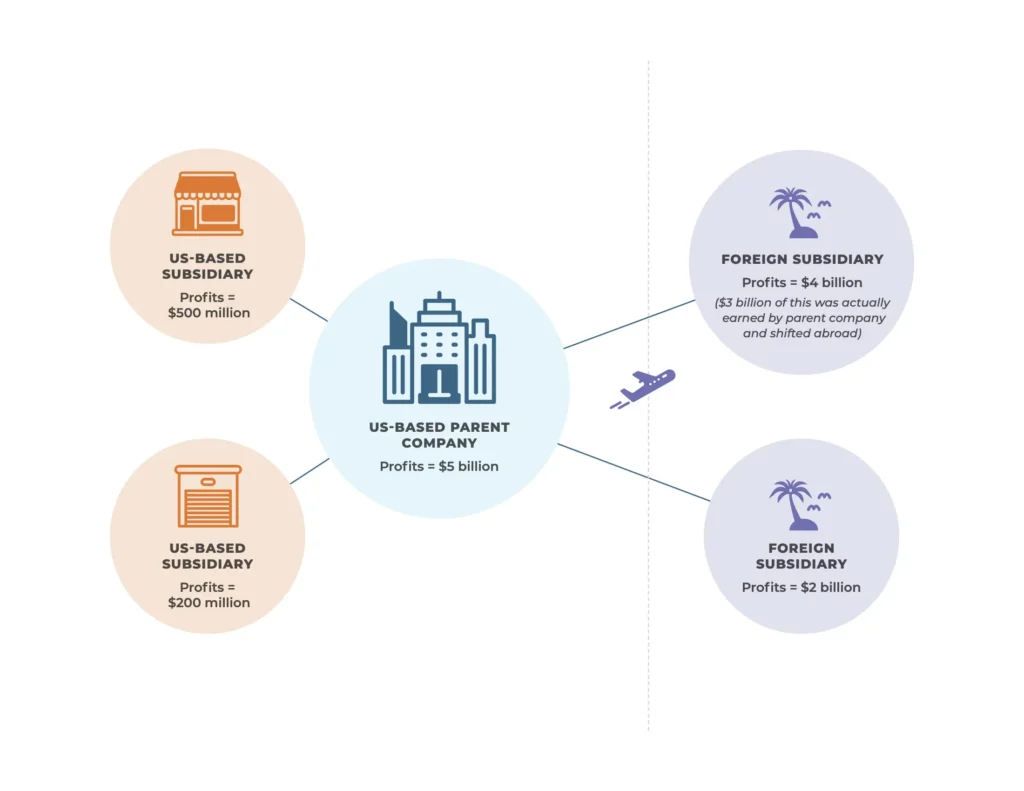

The Problem: Multinational Corporations Avoid Billions in State Taxes by Shifting US Profits Offshore

Large corporations that have affiliated companies outside of the US can use a variety of mechanisms to artificially shift hundreds of billions in US profits to foreign jurisdictions with low tax rates — known as tax havens — to reduce their federal and state taxes. In fact, corporations report to federal tax authorities that their profits in some well-known tax havens are multiple times larger than the entire economies of these places, indicating that most if not all of those profits are only there on paper.

As one example of how a corporation might accomplish this, a US corporation can transfer ownership of intellectual property like patents or trademarks to a foreign affiliate and pay the affiliate for the right to use them, effectively moving income off the books of the US corporation while keeping it within the larger corporate group. This is a tactic that industries such as tech and pharmaceuticals can easily employ, but corporations across the board have options to engage in offshore profit shifting and tax avoidance.

Corporations Can Greatly Reduce Profits Subject to Taxation — and Their Taxes — by Shifting Profits Abroad and Using the Water’s Edge Election

CORPORATE GROUP TOTAL PROFITS

If the example corporation above uses the default Worldwide Combined Reporting method, all worldwide profits are included: $5B + $500M + $200M + $4B + $2B = $11.7 Billion.

If the corporation chooses to use Water’s Edge Election, only domestic profits are included (yellow oval): $5B + $500M + $200M = $5.7 Billion.

Note: This is a simplified example.

California’s “water’s edge election” allows corporations to choose whether or not to include the profits of their foreign affiliates when they report their total profits that can be divided up among, or “apportioned” to, the states where they are subject to tax.1Additionally, while some groups of related corporations may elect to file a group tax return in California, each corporation may file separate returns but are still required to combine profits at the corporate group level first, before apportioning profits between taxing jurisdictions and individual corporate entities.Generally, profits are apportioned to states by multiplying the total profits by the “sales factor”, which is determined by dividing the corporation’s sales into the state by its total sales. For filers electing the water’s edge method, the denominator is only domestic sales.

The water’s edge election creates several issues:

Smaller, domestic businesses likely pay higher shares of their income in taxes than large multinational corporations because they are unable to shift profits overseas.

Giving corporations the option of two filing methods means they will always choose the one that lowers their tax bill. For corporations with significant offshore profits, the water’s edge method will likely result in lower taxes. If corporations have domestic profits and foreign losses, using the “worldwide combined reporting” method — where all worldwide profits and losses are combined — would result in a lower tax bill.

Allowing corporations to ignore foreign profits can encourage them to shift profits to foreign tax havens and avoid state taxes by using the water’s edge election.

Maintaining the water’s edge election will cost the state an estimated $3.1 billion in 2024-25, increasing to $3.5 billion by 2026-27, according to the Department of Finance.

The Solution: Close the Water’s Edge Loophole and Require Worldwide Combined Reporting

Requiring large multinational corporations to use the worldwide combined reporting method would eliminate the state tax benefit of shifting profits abroad and close this loophole, resulting in additional revenue for California. Under this method, corporations are required to include the income of all their domestic and foreign affiliates in their total profits before determining what share is taxable by each state. This is already the default tax filing method for corporations subject to tax in California that don’t elect the water’s edge method, so some corporations currently use this method when it is beneficial for them.

In tandem with requiring worldwide combined reporting, policymakers could take steps to prevent corporations from underreporting their sales into California, driving down the “sales factor” used to determine the share of their profits that can be taxed in California, and ultimately reducing their state taxes. For example, policymakers can clarify state law to ensure corporations report the final destination of their sales — not the location of intermediaries — for the purpose of the sales factor, and require more robust reporting on the locations of sales to allow tax authorities to better identify cases when a corporation may be underreporting. This is a reform that should generate additional revenue on its own, but would also help prevent the erosion of revenues that could be gained from requiring worldwide combined reporting, as requiring corporations to report their global profits may lead them to find other ways to reduce their California tax bill, like underreporting sales into the state.

Ending the water’s edge loophole for large corporations and requiring worldwide combined reporting is a common-sense reform to ensure corporations contribute a fair share of their profits in California taxes to support the state services and infrastructure that allow companies, their workers, and their consumers to thrive.

Want to Better Understand the State Budget?

The Budget Center’s essential resources for understanding and navigating the California state budget — all in one place.

Explore tools, videos, and expert insights designed to strengthen your advocacy and guide informed decision-making.

Additionally, while some groups of related corporations may elect to file a group tax return in California, each corporation may file separate returns but are still required to combine profits at the corporate group level first, before apportioning profits between taxing jurisdictions and individual corporate entities.

You may also be interested in the following resources:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

In California, workers’ wages have stagnated and families struggle to keep up with the rising costs of living, while corporate profits have skyrocketed. Yet many profitable corporations in California pay zero or very little in state taxes year after year.

California policymakers should ensure that profitable corporations pay their fair share in state corporate taxes — which represent a tiny share of their expenses — to support the public services that Californians need and help mitigate the harms of federal cuts to health care, food assistance, and other basic needs programs.

State leaders can prevent profitable corporations from completely wiping out their tax bills with amassed tax credits by instituting permanent annual caps on business credits and deductions. In practice, this would ensure that corporations contribute to the state services and infrastructure they rely on to operate their business, just like all Californians do.

As state leaders look to blunt the harm of the federal budget on Californians with low incomes and the state’s finances, it’s clear that California’s corporate tax structure is in need of repair. While large, profitable corporations benefit from new federal tax breaks, California policymakers must ensure these businesses pay their fair share in state taxes. There is no one-size-fits-all solution: different options can all complement each other. For example, limits on business tax credits and net operating loss (NOL) deductions are key to preventing the erosion of the potential revenues that could be generated from eliminating the water’s edge tax loophole and increasing the tax rate on highly profitable corporations.

MORE IN THIS SERIES

To learn more about the water’s edge election, net operating losses, tax credits, corporate tax rates, and options for common-sense reform, see the other fact sheets in this series:

Highly Profitable Corporations Can Largely Avoid State Taxes With Tax Credits and Net Operating Loss Deductions

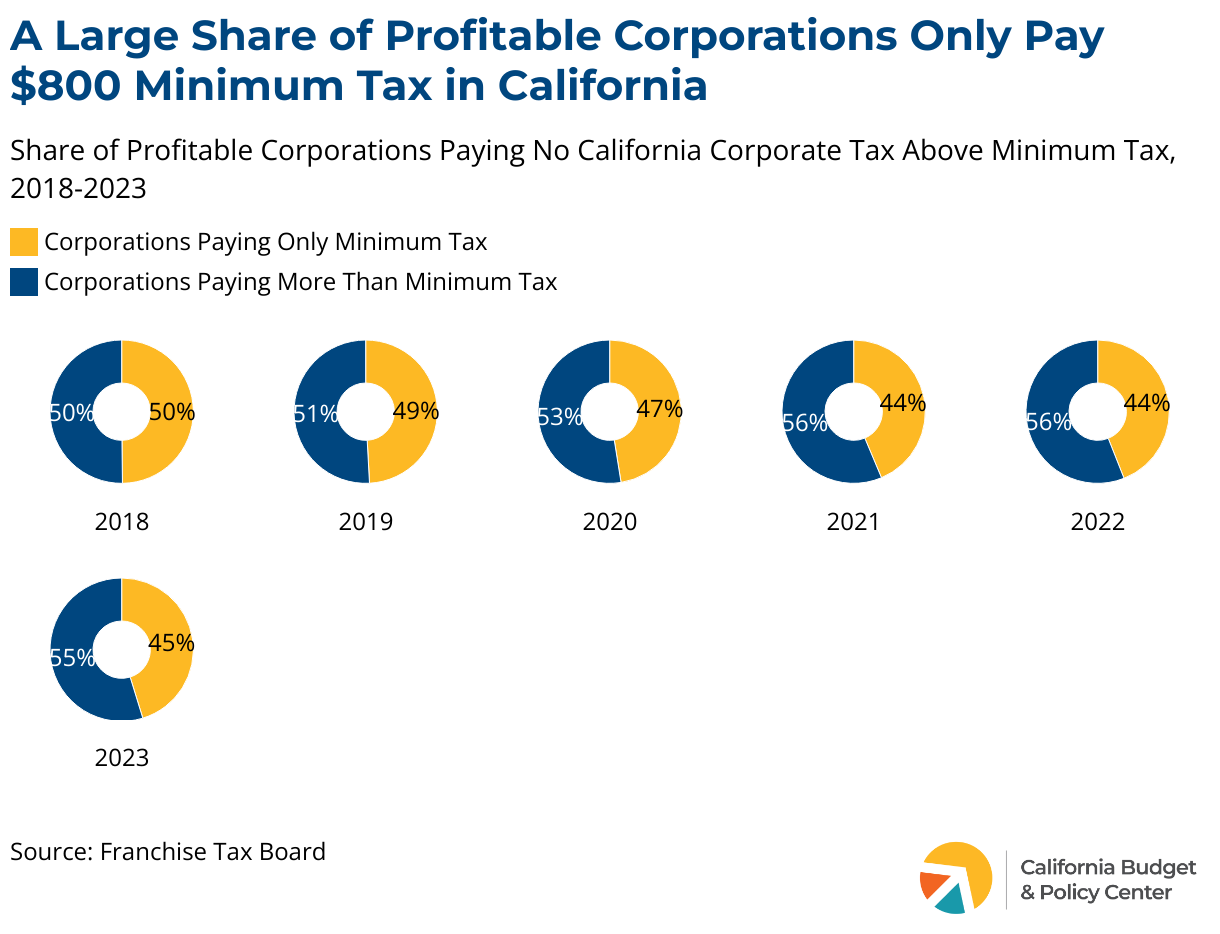

A large share of corporations in California pay nothing above the meager $800 minimum franchise tax that most businesses that are incorporated, registered, or doing business in California are required to pay. Nearly half of all profitable corporations filing tax in California in 2023 — more than 300,000 corporations — paid nothing more than the $800 minimum tax, even though they collectively had $11.7 billion in state profits, according to preliminary data from the state’s Franchise Tax Board. This means they were able to eliminate their regular tax liability by either zeroing out their taxable income with net operating loss deductions, zeroing out their tax bill with tax credits, or some combination of the two. This number does not include corporations that were able to greatly reduce their tax bills but still paid some amount above the minimum tax. Unfortunately, there is no public data available indicating the number of corporations that pay minuscule shares of their profits in state taxes, or which corporations they are. However, public data show that many profitable corporations are able to avoid paying taxes at the federal level. While there are some differences in tax avoidance opportunities for corporations between federal and state law, some corporations paying low or no federal taxes may also be able to reduce or zero out their state taxes using similar state-level tax breaks.

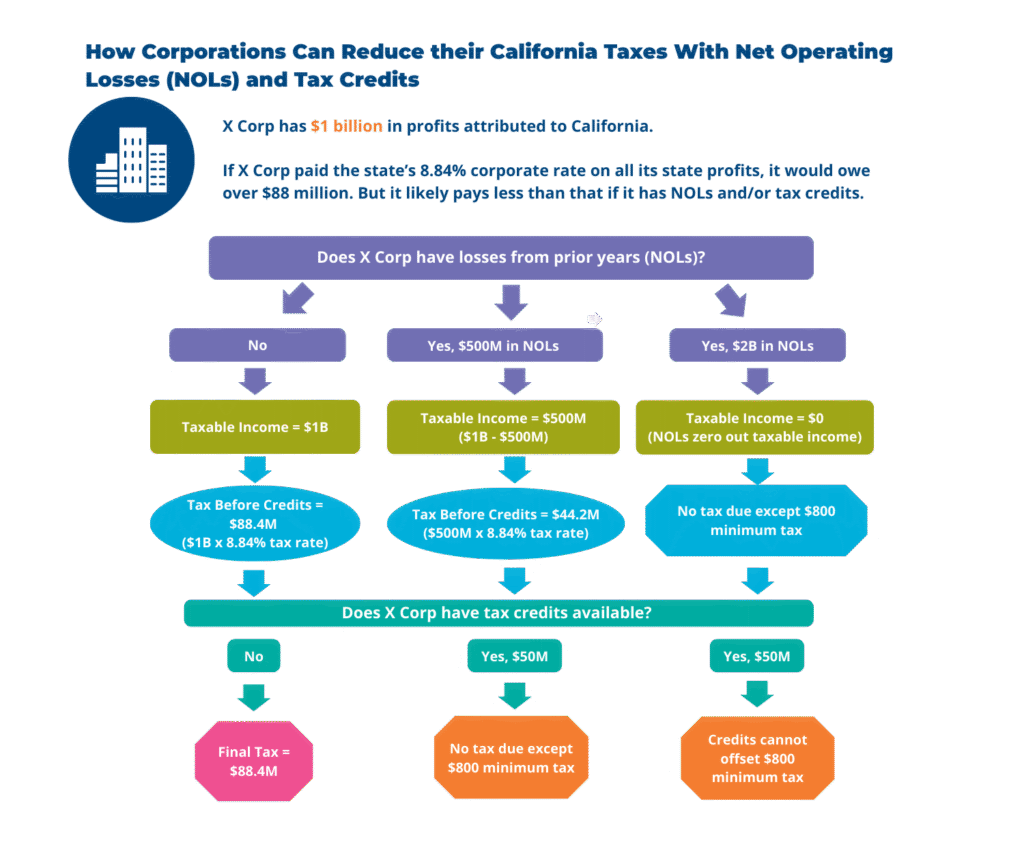

How can corporations pay next to nothing in state taxes when they are profitable?

While business tax calculations can be very complicated, in general a corporation1This is a simplified example that does not include all the complexities of corporate tax calculations.:

Determines its total profits by subtracting business expenses from its total revenues/sales. For corporations that are part of a group of affiliated corporations, this calculation includes the profits of the entire combined group. However, multinational corporations can choose to use the “water’s edge election” and exclude the profits of their foreign subsidiaries, which can reduce their profits subject to state taxes and therefore their tax bill.

Determines the share of these total profits that is attributable to Californiaand to each member of the corporate group by multiplying profits by a “sales” factor — the ratio of the corporations’ California sales to total sales.

Determines its taxable income for state tax purposes by deducting any net operating losses (NOLs) it has available.

Determines its taxes due before applying tax credits by multiplying its taxable income by the applicable tax rate.2 While the state does have an “alternative minimum tax” for C corporations that utilize certain tax preferences, this does not prevent corporations from wiping out their taxes with credits, and impacts very few corporations. In 2022 and 2023,only around 1% of C corporation filers paid the alternative minimum tax, generating $100 million or less in state revenues (data is preliminary for 2023).

Determines its final tax bill by subtracting any tax credits it has available.

A net operating loss occurs when a business experienced losses in prior years, meaning its expenses exceeded its revenues. Those losses can be carried forward and used to reduce its taxable income in future years, and thus its tax bill.3NOLs can be carried forward for up to 20 years after the loss occurred, at which time any unused NOLs expire. In total, corporations reduced their taxable income by around $30 billion in 2023 and had more than $1.3 trillion in unused NOLs that can be carried forward and deducted from profits in future years, according to preliminary Franchise Tax Board data. NOLs, if large enough, could reduce taxable income to zero, in which case the business would pay no more than the state’s $800 minimum franchise tax.

If a business still has taxable income after subtracting NOLs, the applicable tax rate — 8.84% for C corporations and 1.5% for S corporations — is then applied to determine its tax liability. But many businesses can then reduce their tax liability on a dollar-for-dollar basis if they have research and development (R&D) credits, film production credits, or other types of business credits. Some may even reduce their regular tax bill down to zero and would only pay the $800 minimum tax.

Like NOLs, business tax credits can also be carried forward to future years if their credits exceed the taxes they owe in the current year. According to data last reported by the Franchise Tax Board for the 2020 tax year, corporations had more than $40 billion in unused R&D credits that could be used to offset their future tax bills.4 This information is no longer reported by the Franchise Tax Board.

The R&D credit is by far the state’s largest business tax credit. The credit cost California more than $2.5 billion in 2023 and was claimed by over 4,600 corporations across various industrial sectors, according to preliminary Franchise Tax Board data. While research has generally found state R&D tax credits to increase the amount of R&D taking place in a state, the evidence is mixed on the size of the impact and their overall economic effects. Additionally, California’s credit has never been rigorously studied. The California State Auditor noted nearly ten years ago that, because there is no regular oversight or evaluation of the credit, the auditor’s office could not determine whether the credit was fulfilling its purpose or benefitting the state’s economy. Thus, it is unclear whether the billions of dollars the state spends on the credit each year are an effective use of public funds — especially given that those dollars are not available to spend on other public services that could potentially provide greater economic benefits.

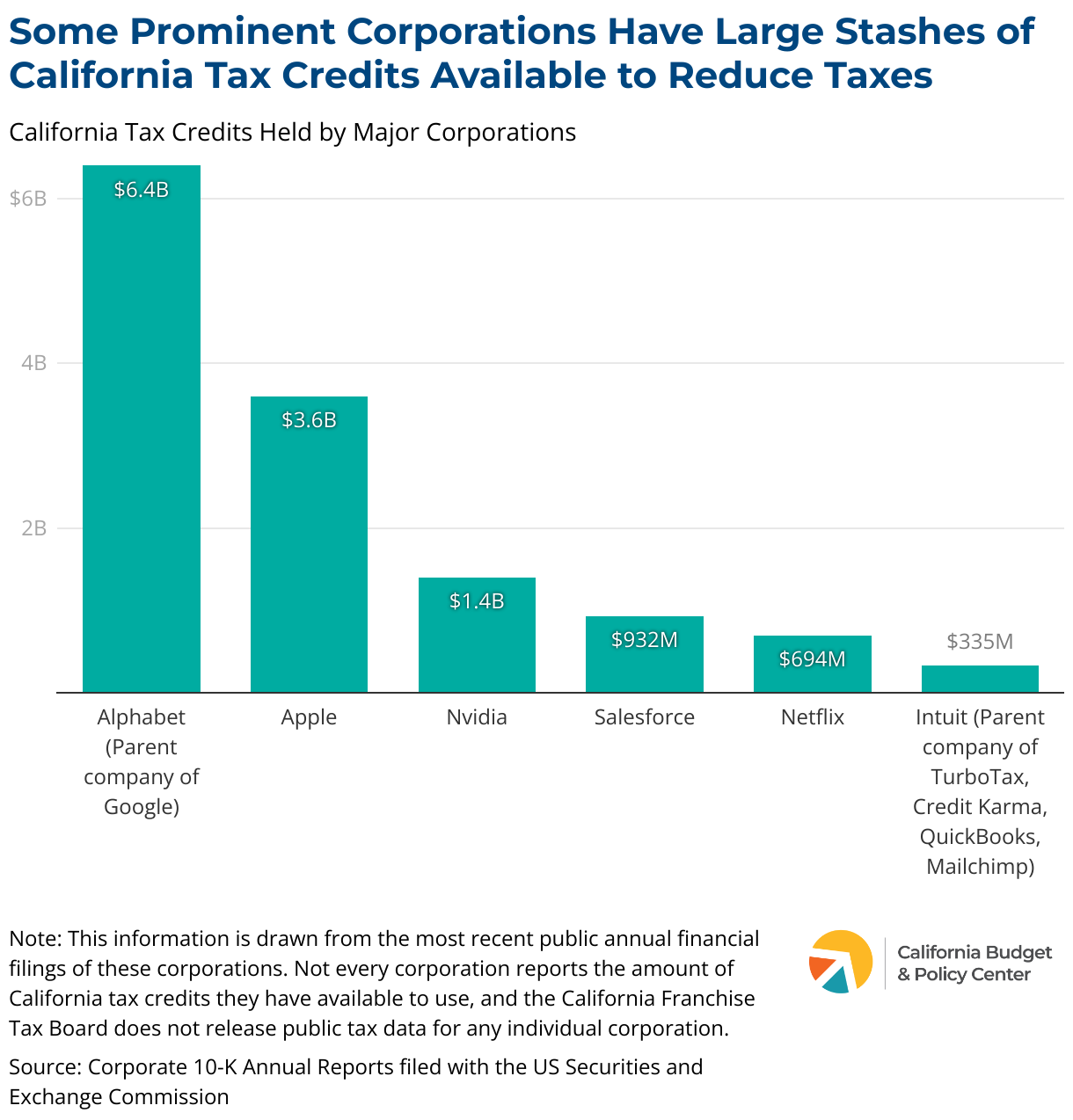

While the Franchise Tax Board does not report tax credit data for individual corporations, some of these corporations do report in their public financial filings the amount of California credits — particularly R&D credits — they have available to offset future tax liability. For example, Alphabet (Google’s parent company) and Apple report that they have $6.4 billion and $3.5 billion, respectively, in California R&D credits that they can use to reduce their California taxes in the future. This means that even if companies like this with large stockpiles of credits were subject to a higher tax rate in the future, some of them could largely avoid paying more in tax as long as they still have sufficient credits available for use.

Profitable Corporations Shouldn’t Be Able to Wipe Their Entire Tax Burden: State Policymakers Should Place Annual Limits on Net Operating Loss Deductions and Tax Credits

California policymakers can make sure profitable corporations pay their fair share in state taxes by enacting permanent annual limits on NOL deductions and tax credits.

State leaders have temporarily limited NOLs and tax credits multiple times in response to budget shortfalls. In 2020, in response to the COVID-19 economic crisis, state leaders enacted a $5 million limit on tax credits that businesses could use in a given year and a pause on the use of NOL deductions for businesses with state profits above $1 million. Those limitations were in effect for tax years 2020 and 2021. However, even with those limitations in place, a large share of profitable corporations still paid nothing more than the $800 minimum tax in those years, as shown in the first chart above.

The Legislative Analyst’s Office estimated in 2022 that the $5 million tax credit limit likely impacted fewer than 100 corporations, since most businesses claim tax credits below that amount. The credit limit is estimated to increase state revenues by $2 billion or more annually in years when it’s in effect.

Faced with another shortfall in 2024, policymakers still re-enacted these limits for tax years 2024, 2025, and 2026.

BAD BUDGETING

Breaking from tradition — and likely to appease corporate opponents to these limits — policymakers also included a provision in the 2024-25 budget that will allow businesses impacted by the temporary tax credit limitation to claim refunds after 2026 for the credits that they were prohibited from taking during the limitation period. In other words, they can receive cash back if their delayed credits exceed the taxes they owe in those years. Historically, refundable tax credits have only been available for low-income families and individuals in California as a way to boost their incomes. Allowing corporations to claim refunds for these credits will cost the state more than $1 billion annually for several years beginning in 2027, as the corporations electing to receive refunds must spread the refund out over several years. Policymakers could avoid these costs in the out years by repealing this refundability provision.

Policymakers have several options to limit business tax credits to a reasonable amount on an ongoing basis. They could opt to make the current temporary $5 million limit permanent instead of letting it expire in 2027. They could also reduce that limit in the near term to generate additional revenues immediately. Another option is to limit the total credits that a business can use in any year to a percentage of the taxes it would otherwise owe that year. In the longer term, rigorous analyses on the efficacy and the cost-effectiveness of specific business tax credits — such as the R&D credit and the film tax credit — are warranted, which would inform future policy reforms such as eliminating or restructuring credits determined to be ineffective or where the costs exceed the benefits.

Similar to limiting tax credits, state leaders could limit the amount of NOL deductions that can be taken in a given year as a percentage of the business’ state profits. While there are legitimate reasons to allow businesses to use NOL deductions to “smooth out” their income over multiple years, since income may be volatile for some businesses, there is also an argument to be made that businesses should not be able to pay nothing or next to nothing in years when they are generating significant profits. So it is reasonable to impose annual limits to prevent corporations from entirely wiping out their taxable income and in turn, their tax bill. At the federal level, NOL deductions are limited to 80% of a corporation’s taxable income. California could adopt that limit or enact a tighter limit to raise additional revenue and ensure corporations are paying taxes on more than 20% of their profits.

Placing reasonable caps on business credits and deductions — particularly in combination with the other corporate tax reforms such as eliminating the water’s edge loophole and increasing the tax rate on the most profitable corporations — will ensure corporations contribute a fair share of their profits in California taxes to support the state services and infrastructure that allow companies, their workers, and their consumers to thrive.

This is a simplified example that does not include all the complexities of corporate tax calculations.

2

While the state does have an “alternative minimum tax” for C corporations that utilize certain tax preferences, this does not prevent corporations from wiping out their taxes with credits, and impacts very few corporations. In 2022 and 2023,only around 1% of C corporation filers paid the alternative minimum tax, generating $100 million or less in state revenues (data is preliminary for 2023).

3

NOLs can be carried forward for up to 20 years after the loss occurred, at which time any unused NOLs expire. In total, corporations reduced their taxable income by around $30 billion in 2023 and had more than $1.3 trillion in unused NOLs that can be carried forward and deducted from profits in future years, according to preliminary Franchise Tax Board data.

4

This information is no longer reported by the Franchise Tax Board.

You may also be interested in the following resources:

Every year, California’s 58 counties — under state oversight — deliver essential public services that support Californians’ well-being, keep communities healthy and safe, and protect vulnerable populations, including children, older adults, and people with disabilities. These programs are funded with a broad range of revenues, including federal dollars, local county taxes, and funding provided by the state.

Counties’ responsibility for these services grew substantially beginning in the 1990s. The state restructured — or “realigned” — the state-county relationship in 1991 and again in 2011 by increasing counties’ fiscal and programmatic obligations for a number of services, while also providing counties with dedicated, ongoing revenues to help support their new costs.

These state-to-county “realignments” encompass vital programs that:

aim to protect vulnerable children and adults,

address health inequities,

support people facing mental health and/or substance use challenges,

keep people from cycling through carceral systems, and

improve Californians’ quality of life, particularly residents with low incomes.

Yet, while counties receive billions of dollars each year to deliver these critical public services, the concept of realignment is not well understood. Moreover, the framework and funding structures that underpin realignment are complex and can be challenging to grasp.

This report cuts through the complexity by explaining what realignment is, how it is structured, and key ways in which it has changed over time. This report does not describe every detail of these complex funding structures. It also does not evaluate realignment or assess how realigned services have been implemented. Instead, it provides a high-level overview that explains the basics, outlines the 1991 and 2011 realignment frameworks, and describes how realignment has evolved in recent decades.

Part 1: Realignment — The Basics

What Is Realignment?

California’s state government and the state’s 58 counties have long shared responsibility for financing and delivering a broad array of services, including public health, mental health care, and support for families with children with low incomes.

However, state and county roles are not static. Instead, they vary across programs and have shifted over time as state policymakers have redefined the state-county relationship. These periodic shifts in responsibility between the state and counties for the financing and implementation of public services are known as “realignment.”

Types of Realignment

The transfer of fiscal and programmatic responsibility for public services between the state and counties typically happens in one of two ways:

Realignment can modify how the state and counties share the cost of public services.

Historically, the state and counties have shared the cost of many public programs operated by counties. Often, these services are also supported with federal funding, in which case the state and counties split the nonfederal share of costs (although not usually 50/50).

Realignment can modify these state/county “cost-sharing ratios” so that one level of government pays more of the cost of a service and the other pays less. For example, counties’ share of costs for a program could be increased from 30% to 60%, with the state’s share reduced from 70% to 40%.

Realignment can transfer the full cost of a program to one level of government or the other.

Historically, the most common transfer scenario has been for state policymakers to eliminate General Fund support for a program that counties already operate and shift 100% of the cost of the program to counties.

The state may also require counties to take on new responsibility for a program or function that is operated at the state level, shifting 100% of the cost from the state General Fund to counties.

However, the most far-reaching realignments were adopted in 1991 and 2011 when counties took on additional responsibility for a broad range of services. These realignments — 20 years apart — expanded counties’ fiscal and programmatic responsibilities in several policy areas.

The 1991 and 2011 realignments encompass the following policy areas:

Social services for children, families, older adults, and people with disabilities

These include Child Welfare Services, Adult Protective Services, In-Home Supportive Services, and more.

Behavioral health services

These include community-based mental health services, substance use disorder treatment services, and more. Applying a different lens, these services include both 1) Medi-Cal specialty mental health and substance use disorder treatment services and 2) non-Medi-Cal services.

Health services

These include public health as well as health care for adults with low incomes who otherwise lack access to health coverage (this is known as indigent health care).

Public safety functions

These include — but are not limited to — trial court security, youth justice, and counties’ new role (as of 2011) in “community corrections” — managing, supervising, and rehabilitating adults convicted of certain low-level offenses.

See Part 2 and Part 3 for key facts about the 1991 and 2011 realignments, respectively, and the Appendix for a description of the programs included in each realignment.

Rationale for Realignment

The goals of realignment typically fall into three categories:

Realignment can help to address state budget deficits.

For example, Governor Pete Wilson and Governor Jerry Brown proposed major state-to-county realignments — in 1991 and 2011, respectively — in response to multibillion dollar state budget deficits.

Realigning responsibilities to the counties helped to address these shortfalls by shifting costs from the General Fund to the newly created realignment revenues that flowed directly to counties.

Realignment can help to improve funding stability.

Providing dedicated revenues to support realigned programs helps to insulate these programs from reductions when the state faces a budget shortfall.

For example, the health and mental health services included in the 1991 realignment were previously funded with state General Fund dollars. Due to state budget shortfalls, these programs were cut in previous budgets, according to the Department of Finance. Moreover, these health and mental health services “would have been subject to additional major reductions” in 1991 to help close the budget deficit if state policymakers had not adopted realignment that year.

Realignment can — but does not always — promote greater efficiency and effectiveness in service delivery.

A primary rationale for the 2011 realignment was that transferring funding and responsibilities to local governments would “allow governments at all levels to focus on becoming more efficient and effective,” helping to ensure that services are “delivered to the public for less money.” Similar claims were made for the 1991 realignment.

Two evaluations of the 1991 realignment — in 2001 and 2018 — found some evidence of progress in terms of efficiency and effectiveness. However, these evaluations also found that counties’ flexibility over these programs and their ability to control costs had diminished substantially since 1991 due to state law changes and other factors.

Funding to Support Realigned Services

When state policymakers shift responsibilities to counties, they provide dedicated annual funding to help counties pay for their additional costs. Annual funding to support counties’ 1991 and 2011 realignment responsibilities comes from two sources — the sales tax and the Vehicle License Fee (VLF). Specifically:

To fund the 1991 realignment, state policymakers increased the state sales tax rate by one-half cent and raised the state’s VLF. Counties continue to receive these dedicated funds each year to support the programs that were realigned to them in 1991.

To fund the 2011 realignment, state policymakers redirected a portion of the state’s existing sales tax and VLF revenues to counties, without raising taxes. In other words, these dollars were carved out of existing state revenue streams. Counties continue to receive these dedicated funds each year to support the programs that were realigned to them in 2011.

What is the sales tax?

The sales tax — formally, the “sales and use tax” — is a tax on the purchase of tangible goods in California (the “sales tax”) or the use of tangible goods in California that were purchased elsewhere (the “use tax”).

Services are excluded from the sales and use tax, as are other items exempted by law, including groceries, menstrual hygiene products, and medications.

The sales and use tax is a regressive tax because households with lower incomes generally spend a larger share of their incomes on necessities than households with higher incomes, so a larger share of their income goes to sales taxes.

What is the vehicle license fee?

The VLF is an annual state fee that is based on the purchase price or value of a vehicle.

In 2011, state leaders shifted to counties part of the base 0.65% VLF rate in order to help fund counties’ increased responsibilities under the 2011 realignment.

The sales tax provides most of the revenue that counties receive to support their responsibilities under the 1991 and 2011 realignments. While sales tax revenues generally grow over time, they can decline from year to year, such as during recessions. When sales tax revenues fall, counties receive less realignment funding than they received the year before. When the economy improves, realignment revenues begin to grow again, providing counties with more resources to carry out their responsibilities.

However, under the 1991 realignment, the revenue shortfalls created during economic downturns are not filled. Even when revenues begin to grow again — providing additional funding for realigned programs — this growth comes on top of a permanently lowered funding base. This leaves counties with less revenue to carry out their 1991 realignment responsibilities over the long term. In contrast, under the 2011 realignment, counties’ funding base is restored when revenues begin to recover following a recession.

Moreover, counties are not reimbursed for their actual costs for realigned programs. Instead, counties receive dedicated revenue that is intended to cover their costs over time. However, this revenue often falls short of meeting the need for and growing cost of services, including counties’ health, public health, and behavioral health responsibilities under both realignments.

Realignment revenue comes closer to covering counties’ actual costs for social services programs, such as Child Welfare Services and In-Home Supportive Services. Under the 1991 realignment, these “entitlement” or “caseload” programs are first in line for sales tax revenue growth, with these growth revenues supporting counties’ rising costs for these services.

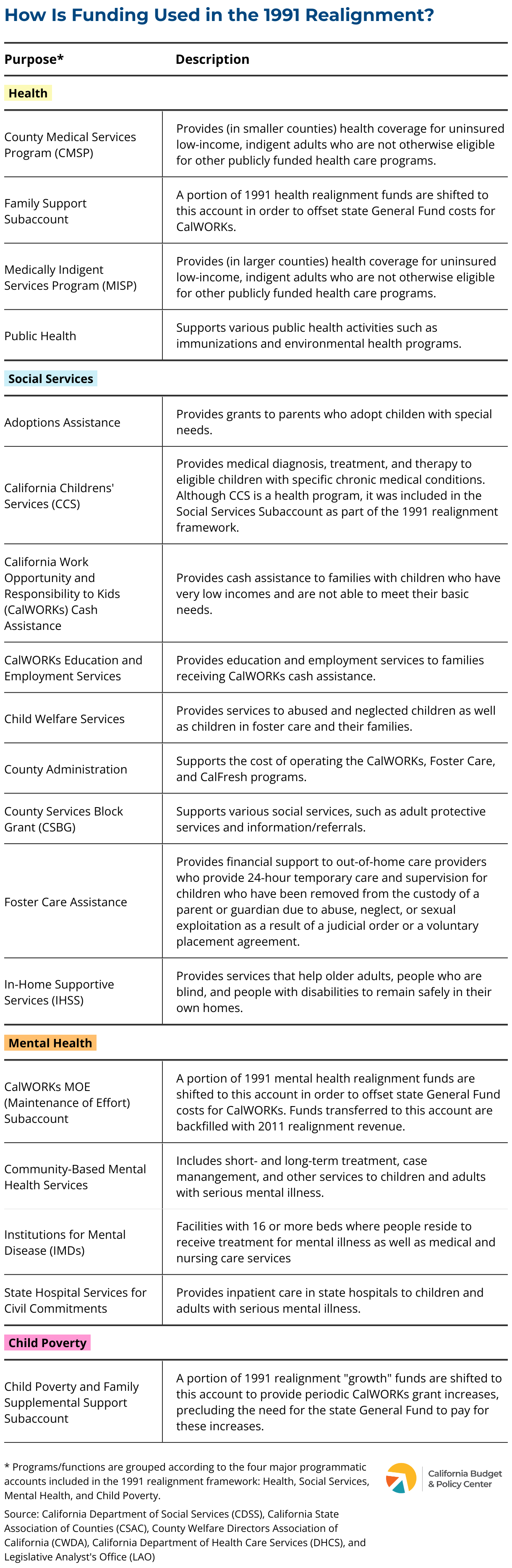

Part 2: Key Facts About the 1991 Realignment

What Did the 1991 Realignment Do?

In 1991, counties took on increased responsibility for a number of health, mental health, and social services programs. (See the Appendix for descriptions of these programs.) This “realignment” changed the state-county relationship in two major ways:

The state transferred responsibility for certain health and mental health programs to counties.

Specifically, counties took full responsibility for key health and mental health programs and also absorbed larger costs as the state eliminated General Fund support for those programs (although the state still maintained an oversight role).

The transferred services included community-based mental health, public health, and health care provided to uninsured adults with low incomes (commonly known as indigent health care).

The state generally increased counties’ share of the nonfederal costs for multiple social services programs as well as for one health program.

Prior to realignment, the state paid most or all of the nonfederal costs of major health and social services programs using General Fund dollars.

Realignment generally shifted more of these nonfederal costs to counties, which lowered the state’s share of costs, freeing up state General Fund dollars for other purposes.

Child Welfare Services and In-Home Supportive Services (IHSS) were among several social services programs for which counties’ share of cost increased under the 1991 realignment. (IHSS is generally considered a social services program but may be referred to as a health program.)

Counties also took on a larger share of the cost for California Children’s Services (CCS), a health program for children with certain diseases or health problems. (CCS was grouped with social services programs for the purpose of the 1991 realignment.)

In some cases, the state reduced counties’ share of cost — and increased the state’s share — to reflect counties’ relatively limited control over spending. The state began to pay a larger share of the cost for:

Cash assistance for low-income families with children, which was integrated into the new CalWORKs program in the mid-1990s.

County administration, which reflects counties’ operational costs for key social services programs.

How Is the 1991 Realignment Funded?

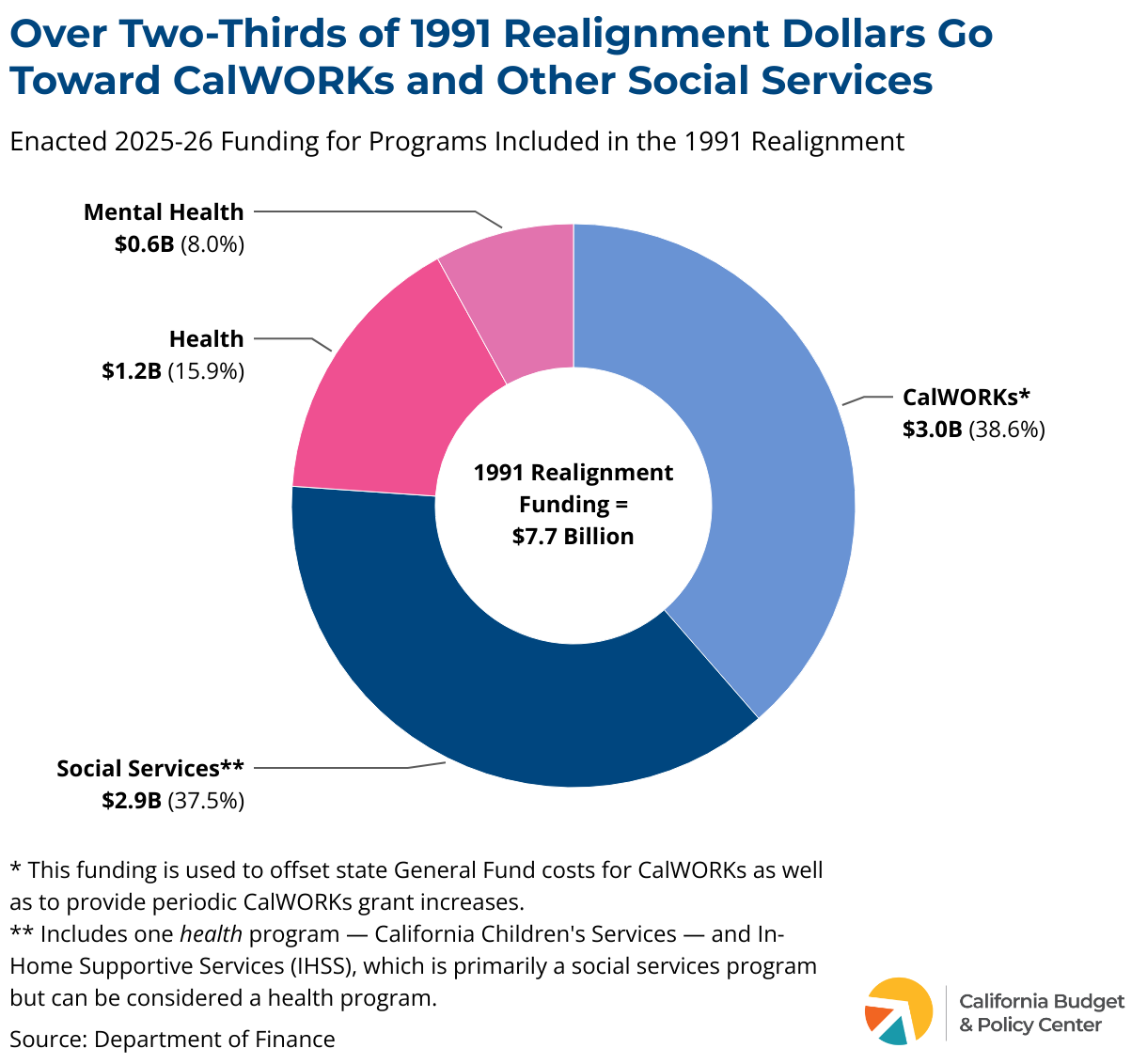

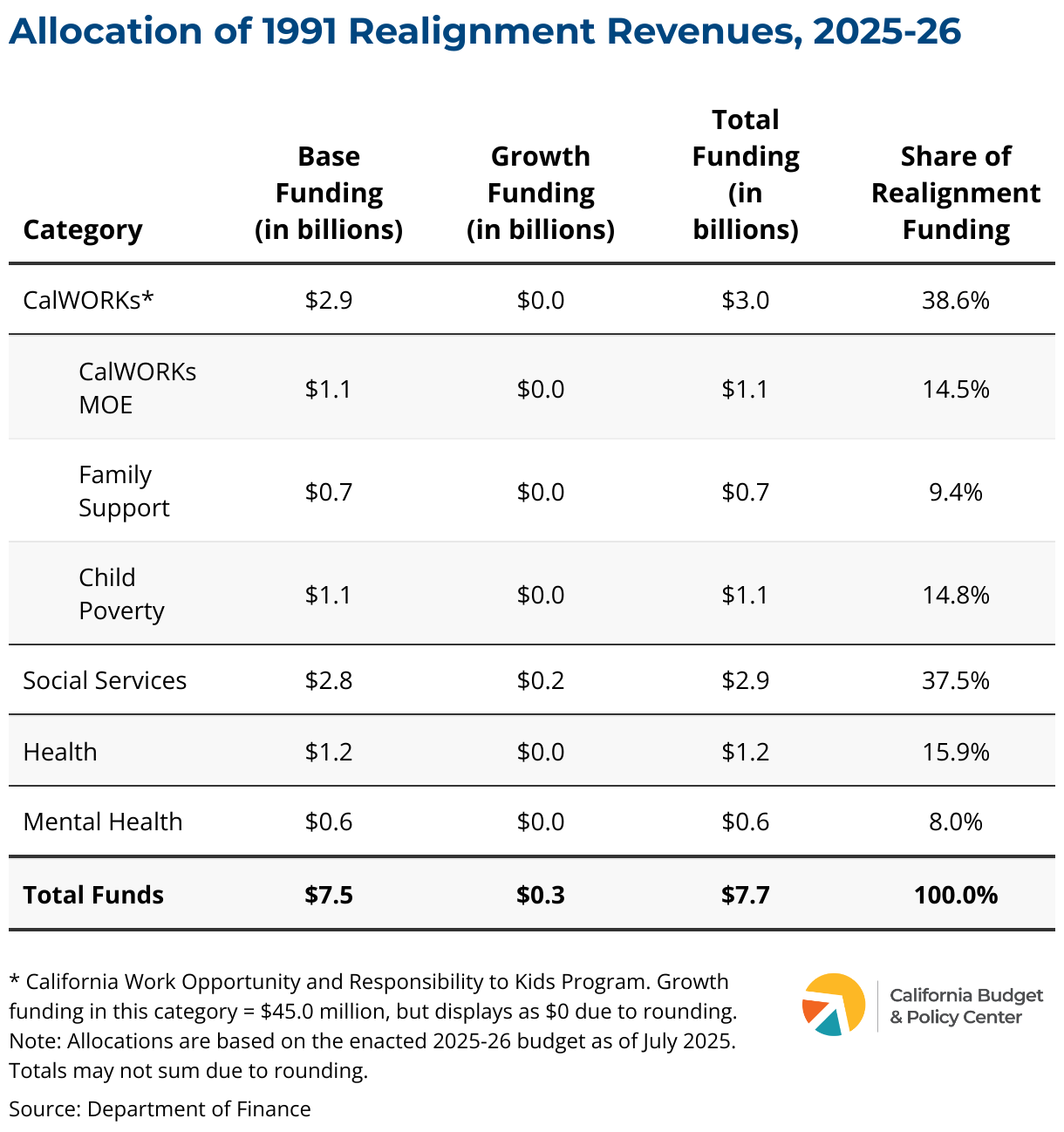

In order to support the programs included in the 1991 realignment, the state Legislature increased taxes and dedicated the revenues to the realigned programs. In 2025-26, these taxes are estimated to raise $7.7 billion. Specifically:

The Legislature raised the state sales tax rate by one-half cent and increased the state’s Vehicle License Fee (VLF), allocating all of the revenue to counties to support the realigned programs.

The half-cent sales tax rate provides almost two-thirds of annual 1991 realignment revenues, totaling an estimated $4.9 billion in 2025-26.

The VLF increase generates about one-third of annual realignment revenues, totaling an estimated $2.8 billion in 2025-26.

What is the sales tax?

The sales tax — formally, the “sales and use tax” — is a tax on the purchase of tangible goods in California (the “sales tax”) or the use of tangible goods in California that were purchased elsewhere (the “use tax”).

Services are excluded from the sales and use tax, as are other items exempted by law, including groceries, menstrual hygiene products, and medications.

The sales and use tax is a regressive tax because households with lower incomes generally spend a larger share of their incomes on necessities than households with higher incomes, so a larger share of their income goes to sales taxes.

What is the vehicle license fee?

The VLF is an annual state fee that is based on the purchase price or value of a vehicle.

In 2011, state leaders shifted to counties part of the base 0.65% VLF rate in order to help fund counties’ increased responsibilities under the 2011 realignment.

How Is the 1991 Realignment Structured?

The 1991 realignment revenues flow through a series of accounts that grew increasingly complex as the Legislature modified the original framework in the decades after the 1991 realignment took effect. (See Part 4 for details on this point.)

Revenue

Annual revenues generated by the higher sales tax rate and the VLF increase first flow into “base funding” accounts.

Realignment “base” revenue is allocated through the Sales Tax Account or the Vehicle License Fee Account, with these funds supporting the various services included in the 1991 realignment.

Realignment revenues sometimes fail to reach the base level of funding, such as when sales tax revenues decline during a recession. When this happens, counties’ funding base is reduced for a fiscal year to match the (lower) available revenues. In other words, counties receive less realignment funding than they received the year before.

Under this scenario, funding for the realigned programs increases only when realignment revenues grow again in future years. However, counties’ realignment base is permanently lowered — that is, the revenue that counties lose during tough budget years when revenues fall short is not made up in future years.

What is realignment “Base” revenue?

“Base” revenue for a fiscal year = the amount of realignment revenue allocated to counties in the prior fiscal year. In other words, the total amount of realignment revenue that counties receive in one year becomes the base level of funding for the next fiscal year.

If available, annual revenues generated by the higher sales tax rate and the VLF increase next flow into “growth funding” accounts.

Growth revenue — if available — is allocated through the Sales Tax Growth Account or the Vehicle License Fee Growth Account, with these funds supporting 1991 realignment services based on a complex set of funding priorities.

Sales tax growth revenues go first to social services programs, including but not limited to Child Welfare Services and In-Home Supportive Services. (Social services are called “caseload” programs in the 1991 realignment framework).

Any remaining sales tax growth revenues go to the health and mental health accounts as well as to support certain increases to CalWORKs grants. As discussed in Part 4, the state began using sales tax growth revenues to fund periodic CalWORKs grant increases in 2013.

Vehicle License Fee Growth Account

VLF growth revenues go first to the County Medical Services Program to support counties’ role in providing health care to low-income, uninsured adults (known as indigent health care).

Any remaining VLF growth revenues go to health and mental health programs as well as to support certain increases to CalWORKs grants. As discussed in Part 4, the state began using VLF growth revenues to fund periodic CalWORKs grant increases in 2013.

what is realignment “growth” revenue?

“Growth” revenue = the amount of realignment revenue left over (if any) after the base level of revenue for a fiscal year has been reached.

In other words, sales tax and VLF revenue that exceeds the base level of funding for a fiscal year flows to counties on top of their base allocations.

Allocations: Big Picture

Originally, revenue raised by the 1991 realignment solely supported the realigned health, mental health, and social services programs. However, in the early 2010s, state leaders redirected a portion of 1991 realignment revenue to offset some state costs for CalWORKs. To implement these shifts, state leaders added three CalWORKs-focused accounts to the 1991 realignment framework. (See Part 4 for details.)

With the addition of these new CalWORKs accounts, 1991 realignment revenue — which is estimated to total $7.7 billion in 2025-26 — is divided among four spending categories:

CalWORKs,

Social Services,

Health, and

Mental Health.

CalWORKs Allocation

Nearly 40% of realignment funding — an estimated $3.0 billion in 2025-26 — is used to achieve state savings by offsetting the state’s cost for CalWORKs.

These funds flow into three accounts created in the early 2010s: the CalWORKs MOE [Maintenance of Effort] Subaccount, the Family Support Subaccount, and the Child Poverty and Family Supplemental Support Subaccount. (See Part 4 for details.)

Using 1991 realignment dollars to offset a portion of the state’s General Fund cost for CalWORKs frees up state dollars for other purposes and reduces pressure on the state budget.

Social Services Allocation

More than one-third of realignment funding — an estimated $2.9 billion in 2025-26 — supports multiple social services programs as well as one health program.

These funds flow into the Social Services Subaccount, supporting programs like Child Welfare Services, Foster Care, and In-Home Supportive Services. (IHSS is generally considered a social services program but may be referred to as a health program.)

These revenues also support California Children’s Services (CCS), which assists children with certain diseases or health problems and is the only health program included in the Social Services Subaccount.

All of the programs in the Social Services Subaccount are known as “caseload” programs in the 1991 realignment framework.

Health Allocation

About 16% of realignment funding — an estimated $1.2 billion in 2025-26 — supports counties’ role in delivering health services.

The Health Subaccount includes funding for public health activities as well as for indigent health care (care provided to low-income, uninsured adults).

Counties’ role in indigent health care diminished substantially starting in 2014 when California adopted the Medi-Cal eligibility expansion as allowed by the Affordable Care Act. With this expansion, millions of uninsured adults who previously accessed health care through county programs became newly eligible for Medi-Cal. With fewer adults turning to counties for health care, the state redirected some indigent health care dollars away from counties, as described in Part 4.

Mental Health Allocation

Less than 10% of realignment funding — an estimated $618 million in 2025-26 — supports counties’ role in delivering mental health services.

The Mental Health Subaccount includes funding for community-based mental health services, state hospital services for civil commitments, and Institutions for Mental Disease (IMDs) — facilities with 16 or more beds where people reside to receive treatment for mental illness as well as medical and nursing care services.

Looking at it through a different lens, these services include both 1) Medi-Cal specialty mental health services and 2) non-Medi-Cal services.

What Else Changed with Realignment in 1991?

In addition to establishing dedicated revenue streams and allocation formulas, the 1991 realignment legislation included other significant elements. Specifically:

Counties may transfer a limited amount of their annual revenue from one realignment account to another.

Counties are allowed to transfer funds among the Health, Mental Health, and Social Services subaccounts.

Specifically, up to 10% of one account’s annual allocation may be shifted to the other two subaccounts.

In addition, under certain circumstances, counties may transfer:

An additional 10% of funds from the Health account to the Social Services subaccount.

An additional 10% of funds from the Social Services subaccount to the Health or Mental Health subaccounts.

Realignment legislation included “poison pill” provisions — one of which remains in effect today.

When the realignment legislation was advancing, state leaders were uncertain whether any of its provisions would be challenged through a lawsuit or a “mandate” claim filed by a county seeking reimbursement from the state.

As a result, state leaders added several “poison pills” to the legislation that were intended to nullify key components of realignment if a challenge was successful.

Some of the hurdles created by these poison pills were ultimately overcome — specifically, provisions that would have rolled back the half-cent sales tax increase or the Vehicle License Fee increase, either of which would have reduced the revenue available to support the realigned programs.

However, one of the poison pills remains active: If any county makes a mandate claim that results in state costs of more than $1 million, the 1991 realignment would come to an end.

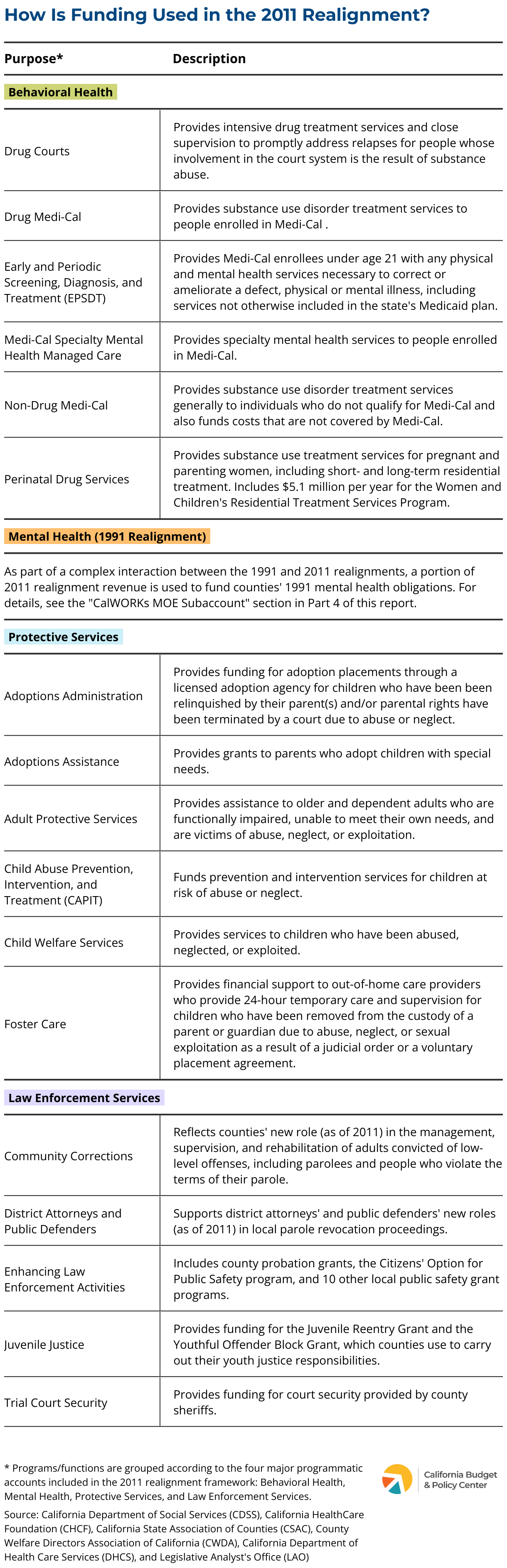

Part 3: Key Facts About the 2011 Realignment

What Did the 2011 Realignment Do?

In 2011, the Legislature built on the 1991 realignment by further increasing counties’ responsibility for several health and social services programs while also realigning certain public safety functions. (See the Appendix for descriptions of these programs.) This new realignment in 2011 revised the state-county relationship in two key ways:

Counties became fully responsible for funding — supported with realignment revenue — certain behavioral health, social services, and public safety programs that they were already administering.

Prior to 2011, counties, the state, and the federal government shared the cost of operating the child welfare system and key behavioral health services. With the 2011 realignment, the state stopped using its own General Fund dollars to help pay for the nonfederal costs of these programs. Instead, counties started paying 100% of the nonfederal costs using realignment funds to help pay for those costs. This change applied to:

Nearly the entire child welfare system, including Child Welfare Services, Foster Care, Adoptions Administration, Adoption Assistance, and Child Abuse Prevention, Intervention, and Treatment.

Major behavioral health programs, including Drug Medi-Cal services, Medi-Cal Specialty Mental Health Managed Care, and the Early and Periodic Screening, Diagnosis, and Treatment (EPSDT) program.

The state also eliminated General Fund support for several other programs that counties were administering in 2011. Instead, counties began to use the revenue provided by the 2011 realignment to fund these programs. This change applied to:

The Adult Protective Services program.

Key substance use treatment programs, such as drug courts and the Women and Children’s Residential Treatment Services Program.

Certain local public safety programs and functions, including trial court security, counties’ youth justice responsibilities, and local grants focused on law enforcement and county probation.

Counties took on new responsibility — supported with realignment revenue — for certain public safety functions that previously had been carried out by the state.

In order to help reduce overcrowding in state prisons, the 2011 realignment included a new role for counties in managing, supervising, and rehabilitating adults convicted of certain low-level offenses — a change commonly called “community corrections.” Previously, people convicted of low-level offenses served their sentences in state prison and were supervised by state parole agents upon their release.

The Legislature also created new roles for county district attorneys and public defenders in parole revocation hearings. These proceedings determine whether people who violate the terms and conditions of their local supervision should be punished with county jail time.

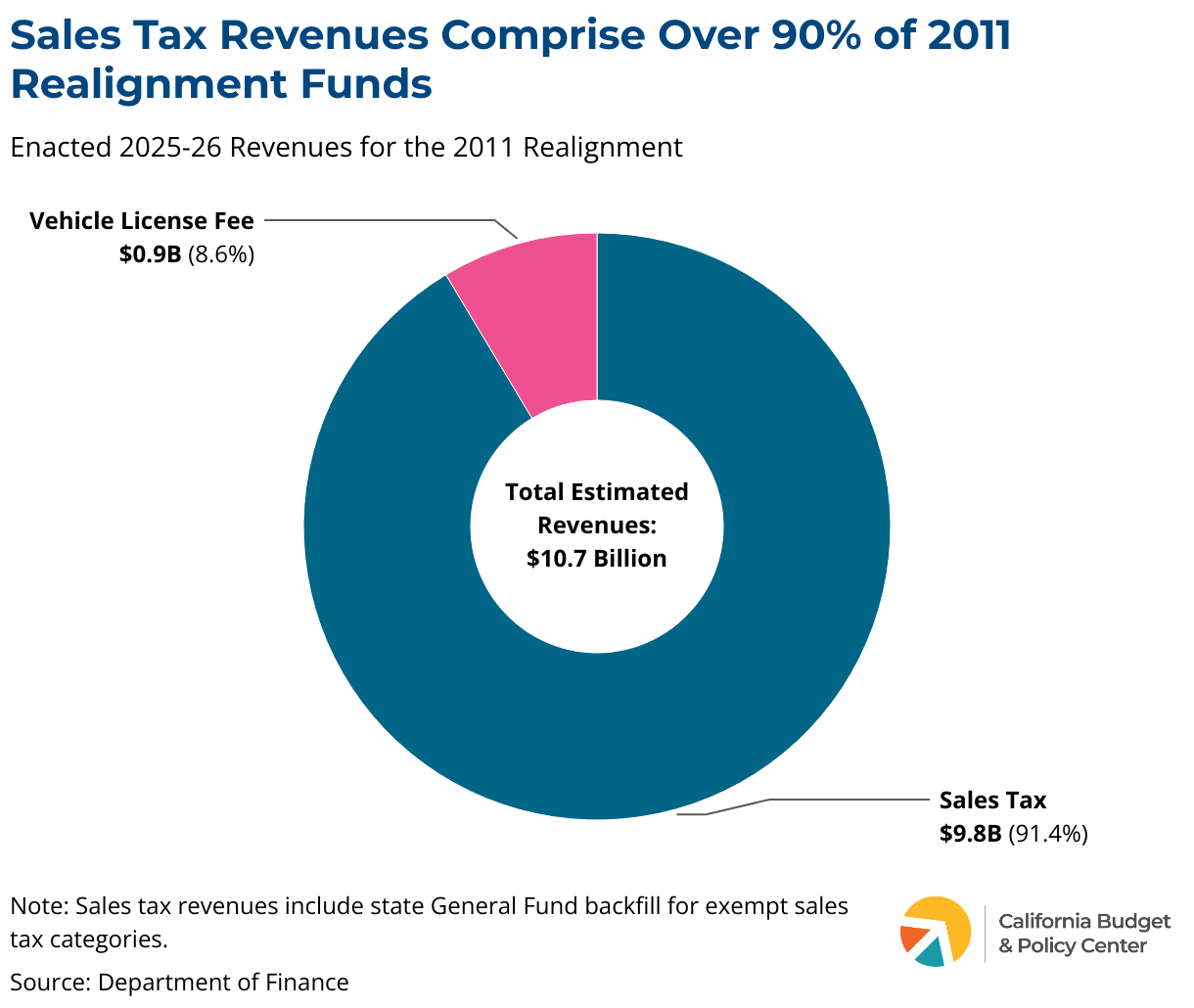

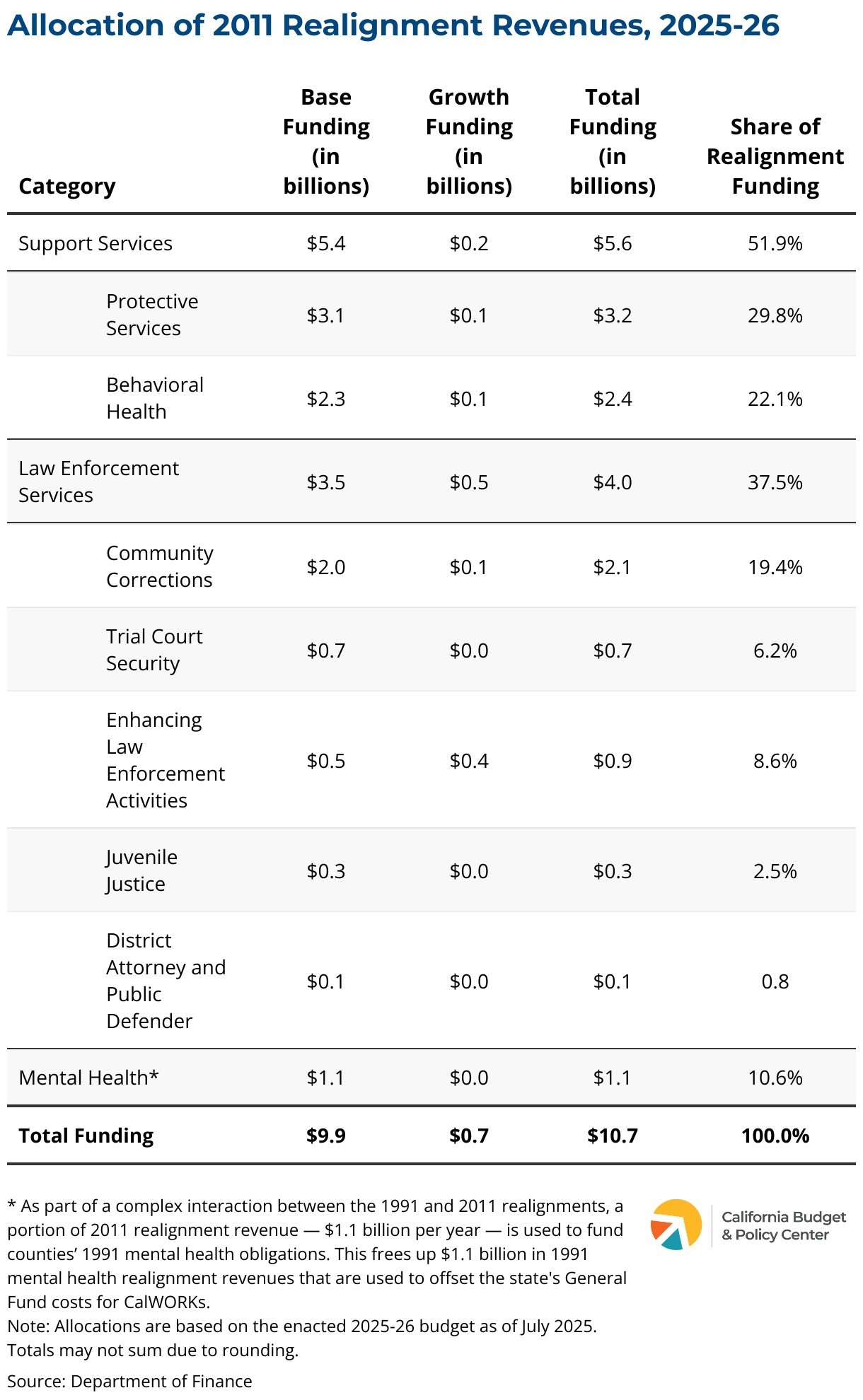

How Is the 2011 Realignment Funded?

To fund the 2011 realignment, state leaders carved out portions of two existing revenue streams and dedicated those revenues to counties. These revenues are estimated to total $10.7 billion in 2025-26.

The Legislature redirected to counties a portion of state sales taxes as well as a portion of Vehicle License Fee (VLF) revenue in order to fund the realigned programs.

The Legislature shifted revenues equal to 1.0625 cents of the state sales tax rate to counties. In other words, slightly more than 1 cent of the sales tax rate on each $1 in taxable purchases bypasses the state treasury and goes directly to counties. In 2025-26, these diverted sales tax dollars are estimated to total $9.8 billion — more than 90% of all revenues that counties receive through the 2011 realignment.

In addition, the state uses General Fund dollars to backfill for certain exempt sales tax categories. This provides a relatively small amount of additional revenue to support counties’ 2011 realignment responsibilities. This General Fund backfill is estimated to total $44.2 million in 2025-26.

The Legislature also redirected a portion of VLF revenues to counties. In 2025-26, the VLF revenues shifted to counties are estimated to total $919.3 million — about 9% of all revenues that counties receive through the 2011 realignment.

What is the sales tax?

The sales tax — formally, the “sales and use tax” — is a tax on the purchase of tangible goods in California (the “sales tax”) or the use of tangible goods in California that were purchased elsewhere (the “use tax”).

Services are excluded from the sales and use tax, as are other items exempted by law, including groceries, menstrual hygiene products, and medications.

The sales and use tax is a regressive tax because households with lower incomes generally spend a larger share of their incomes on necessities than households with higher incomes, so a larger share of their income goes to sales taxes.

What is the vehicle license fee?

The VLF is an annual state fee that is based on the purchase price or value of a vehicle.

In 2011, state leaders shifted to counties part of the base 0.65% VLF rate in order to help fund counties’ increased responsibilities under the 2011 realignment.

How Is the 2011 Realignment Structured?

The 2011 realignment revenues move through a complicated set of accounts that the Legislature last modified in 2012, the year after this realignment was adopted.

Revenue

The state sales tax and Vehicle License Fee (VLF) revenues that fund the 2011 realignment flow into an account called the “Local Revenue Fund 2011” until this fund reaches its “base” level for a fiscal year.

These base funds support counties’ role in providing the services included in the 2011 realignment.

Realignment revenues sometimes fail to reach the base level of funding, such as when sales tax revenues decline during a recession. When this happens, counties receive less funding, but the gap is tracked and the base is gradually restored when revenues begin to grow again.

In other words, under the 2011 realignment, counties’ base funding is temporarily lowered when revenues decline. In contrast, when 1991 realignment revenues fail to reach the base level, counties’ base funding is permanently lowered because there is no requirement for base restoration in the 1991 realignment.

What is realignment “Base” revenue?

“Base” revenue for a fiscal year = the amount of realignment revenue allocated to counties in the prior fiscal year. In other words, the total amount of realignment revenue that counties receive in one year becomes the base level of funding for the next fiscal year.

Any sales tax and VLF revenue that exceeds the base funding level for a fiscal year becomes “growth” revenue.

Growth revenue — if available — is allocated to the programs included in the 2011 realignment based on complex rules that set funding priorities.

For example, if sales tax revenue grows year-over-year, about two-thirds of that growth is divided among the behavioral health and social services programs, while the remaining one-third of those growth dollars go to the public safety programs.

what is realignment “growth” revenue?

“Growth” revenue = the amount of realignment revenue left over (if any) after the base level of revenue for a fiscal year has been reached.

In other words, sales tax and VLF revenue that exceeds the base level of funding for a fiscal year flows to counties on top of their base allocations.

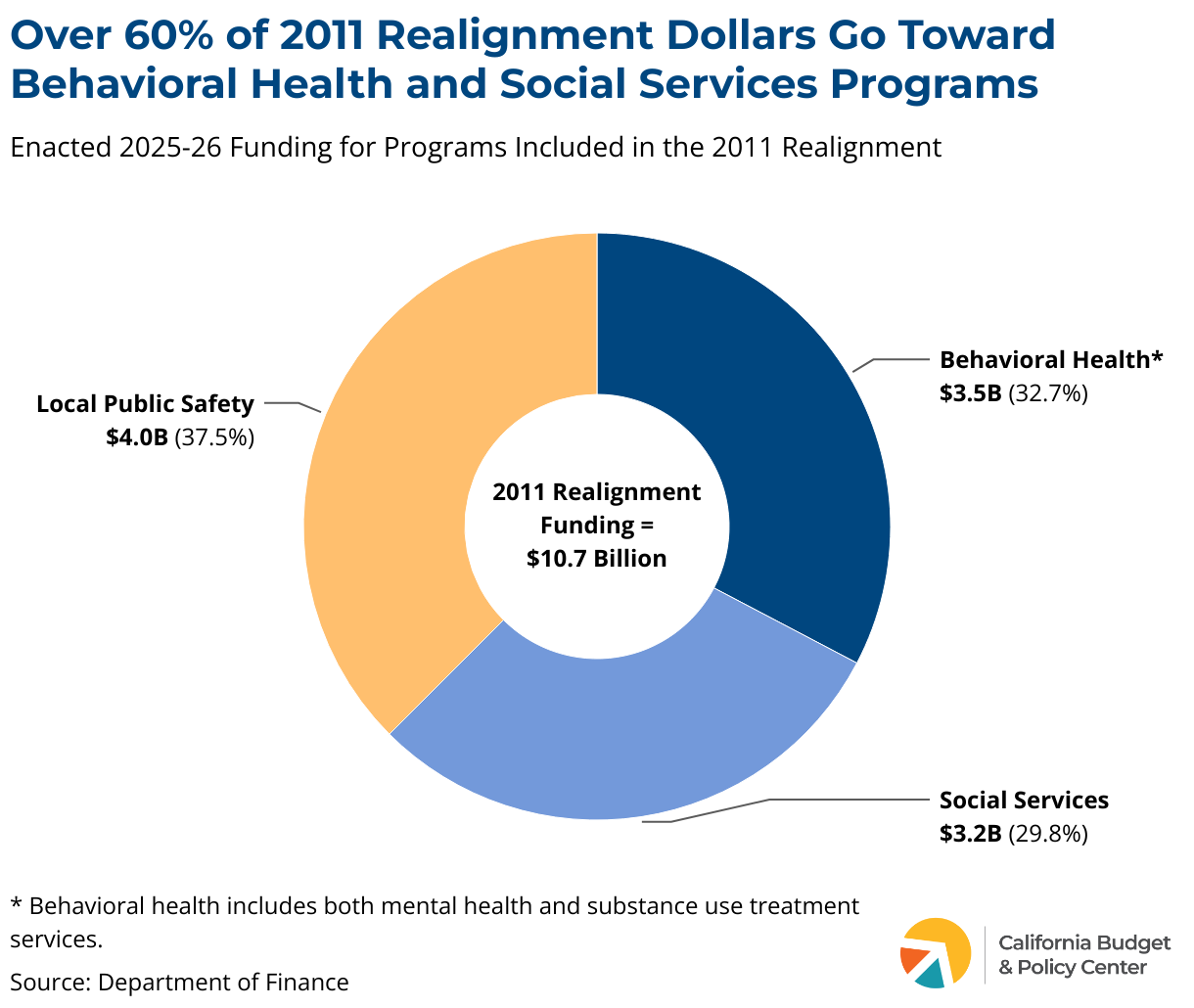

Allocations: Big Picture

More than 60% of revenues provided through the 2011 realignment — an estimated $6.7 billion in 2025-26 — support counties’ role in delivering behavioral health and social services. The remaining funds — an estimated $4.0 billion — go to public safety programs that were realigned to counties in 2011.

Behavioral Health Allocation

Nearly one-third of 2011 realignment funding — an estimated $3.5 billion in 2025-26 — supports behavioral health services. This includes funding for both 1) the mental health and substance use disorder treatment services that counties took increased responsibility for starting in 2011 and 2) the mental health services that were shifted to counties as part of the earlier realignment in 1991.

$2.4 billion of these funds flow into the Behavioral Health Subaccount, which was created as part of the 2011 realignment.

This subaccount supports both 1) Medi-Cal specialty mental health and substance use disorder treatment services and 2) non-Medi-Cal services, including:

Early and Periodic Screening, Diagnosis, and Treatment (EPSDT) services for children and youth,

Medi-Cal Specialty Mental Health Managed Care (MHMC), and

Substance use treatment services, including perinatal drug services and drug courts.

In 2011, counties were already administering these programs. The primary impact of the 2011 realignment was to increase counties’ costs — and eliminate the state’s costs — for these programs, with the new realignment revenue intended to help counties meet their larger financial obligations.

For example, since 2011 counties have been fully responsible for the nonfederal share of costs for EPSDT and MHMC.

The remaining $1.1 billion of these 2011 realignment funds flow into the Mental Health Subaccount, which was created as part of the 1991 realignment.

These funds — which are capped at $1.1 billion per year — support the mental health responsibilities that counties took on in 1991 as part of the first major state-to-county realignment.

In other words, counties’ 1991 mental health responsibilities are largely funded with revenues provided by the 2011 realignment rather than with 1991 realignment dollars — a fund switch that benefited the state’s General Fund. See Part 4 for details about this switch.

Social Services Allocation

Around 30% of 2011 realignment funding — an estimated $3.2 billion in 2025-26 — supports counties’ role in providing social services for children, youth, and older and dependent adults.

These funds flow into the Protective Services Subaccount, supporting Child Welfare Services, Foster Care, Adoption Assistance, and related programs for children and youth as well as Adult Protective Services.

In 2011, counties were already administering these programs, most of which were also included in the 1991 realignment. The primary impact of the 2011 realignment was to increase counties’ costs — and eliminate the state’s costs — for these programs, with the new realignment revenue intended to help counties meet their larger financial obligations.

For example, since 2011 counties have been fully responsible for the nonfederal share of costs for the child welfare system.

Public Safety Allocation

Over one-third of 2011 realignment funding — an estimated $4.0 billion in 2025-26 — supports public safety programs.

These funds flow into the Law Enforcement Services Account and primarily support counties’ role in “community corrections” — the management, supervision, and rehabilitation of people convicted of certain low-level offenses who, prior to 2011, served their sentences in state prison and were supervised by state parole agents upon release.

What Else Changed with Realignment in 2011?

In addition to establishing dedicated revenue streams and allocation formulas, the 2011 realignment legislation included other significant elements. Specifically:

Counties may transfer a limited amount of revenue between the Behavioral Health and Protective Services subaccounts, both of which are part of the Support Services Account.

Specifically, counties may shift — in either direction — an amount of funding that does not exceed 10% of the funds in the smaller account, based on the prior fiscal year’s funding level. (Certain counties are not subject to the 10% cap.)

Any transfer applies only for the fiscal year in which it is made, meaning that transfers do not create a permanent funding shift.

Counties are not allowed to transfer funds between the Support Services Account and the Law Enforcement Services Account.

This means that funding for behavioral health programs and social services cannot be used for law enforcement purposes (or vice versa) — even on a temporary basis.

The 2011 realignment includes constitutional protections approved by California voters.

In 2012, California voters strengthened the 2011 realignment by approving Proposition 30, which enshrined significant protections for the state and counties in the state Constitution. Specifically, Prop. 30:

Constitutionally protects the state revenue that was shifted to counties to fund their responsibilities under the 2011 realignment. This means the state cannot reduce or eliminate these revenues without voter approval.

Requires the state to provide counties with alternative funding if current realignment revenues are eliminated.

Allows counties to disregard state policy changes that increase realignment program costs if the state does not provide funding to offset those costs.

Requires the state to pay at least half of any 2011 realignment program cost increases that stem from federal court or administrative decisions or federal law or regulations.

Constrains the state’s ability to submit federal plans or waivers that would increase counties’ costs for realigned programs.

Protects the state from mandate claims related to the 2011 realignment.

Part 4: How State Leaders Reshaped Realignment to Benefit the State Budget

In the early 2010s, as California struggled to emerge from the Great Recession, state leaders made three major changes to the 1991 realignment framework to reduce cost pressures on the state’s General Fund. Notably, one of these changes involved shifting funds between the 1991 and 2011 realignments.

Taken together, these changes today provide a roughly $3 billion annual benefit to the state budget. These adjustments to the 1991 realignment funding structure — and the new accounts that were created to implement them — are described below.

CalWORKS MOE Subaccount

In 2011, state leaders approved a complex funding shift between county-run mental health programs and CalWORKs, creating over $1 billion in annual state General Fund savings.

In 2011, as state leaders were developing California’s second major state-to-county realignment, they decided to use a portion of the revenue from this new realignment — capped at $1.1 billion per year — to pay for counties’ mental health obligations, which were shifted to counties as part of the first major realignment in 1991.

This fund shift freed up $1.1 billion of 1991 realignment revenue that otherwise would have remained in the Mental Health Subaccount and supported counties’ mental health responsibilities. In other words, counties no longer needed those 1991 realignment dollars for mental health because those funds were replaced with revenue from the 2011 realignment.

These freed-up revenues were redirected to a CalWORKs MOE Subaccount that was added to the 1991 realignment framework (MOE = “maintenance of effort”). These dollars replaced, or offset, the state’s cost for CalWORKs grants, resulting in ongoing annual state General Fund savings of $1.1 billion.

Because this policy change implemented a funding shift rather than a funding cut, there was no detrimental impact on county-run mental health programs or on the CalWORKs program.

Family Support Subaccount

In 2013, state leaders shifted some 1991 realignment revenue from county-run indigent health care programs to CalWORKs, generating hundreds of millions of dollars in ongoing state General Fund savings.

Prior to 2014, Californians with low incomes who were ineligible for Medi-Cal (Medicaid) received care through county indigent health care programs, which were part of the 1991 realignment and funded with realignment revenues.

With the passage of the federal Affordable Care Act (ACA) in 2010, states were allowed to expand — starting in 2014 — their Medicaid programs to millions of adults who previously were excluded due to Medicaid’s stringent rules. California implemented this expansion in 2014. This change shifted primary responsibility for providing health care to these adults — along with the cost — from counties to the state and federal governments.

Given counties’ diminished role — and the state’s significantly expanded role — in indigent health care, state leaders created a complex set of formulas to capture county savings. In other words, a portion of counties’ 1991 realignment revenue for indigent health care was shifted to the state. These changes were included in Assembly Bill 85 (Committee on Budget, Statutes of 2013), as modified by Senate Bill 98 (Chapter 358, Statutes of 2013).

These redirected 1991 realignment revenues:

Are deposited into the Family Support Subaccount, which was added to the 1991 realignment framework by AB 85.