key takeaway

Large profitable corporations in California have several strategies to avoid paying more than the minimum $800 state tax, costing the state billions in lost revenue each year. State leaders can take steps to reduce corporate tax breaks to better invest in the health and well-being of all Californians.

At a time when many Californians struggle with the state’s affordability challenges and millions will be harmed by the impacts of the deep federal cuts to health care and food assistance enacted by H.R. 1, the 2025 Republican megabill, highly profitable corporations continue to benefit from generous tax breaks at the state and federal levels. These corporations benefit from California’s skilled workforce, public infrastructure, and strong consumer base — all made possible by public investments supported by tax revenues. Yet some of these corporations pay next to nothing in corporate taxes in California, largely due to overly generous state tax breaks.

Reforming California’s corporate tax system to ensure all profitable corporations are contributing their fair share to support essential public services is a necessary step to generate ongoing revenues that the state needs to support the health and well-being of Californians and strengthen economic security for all.

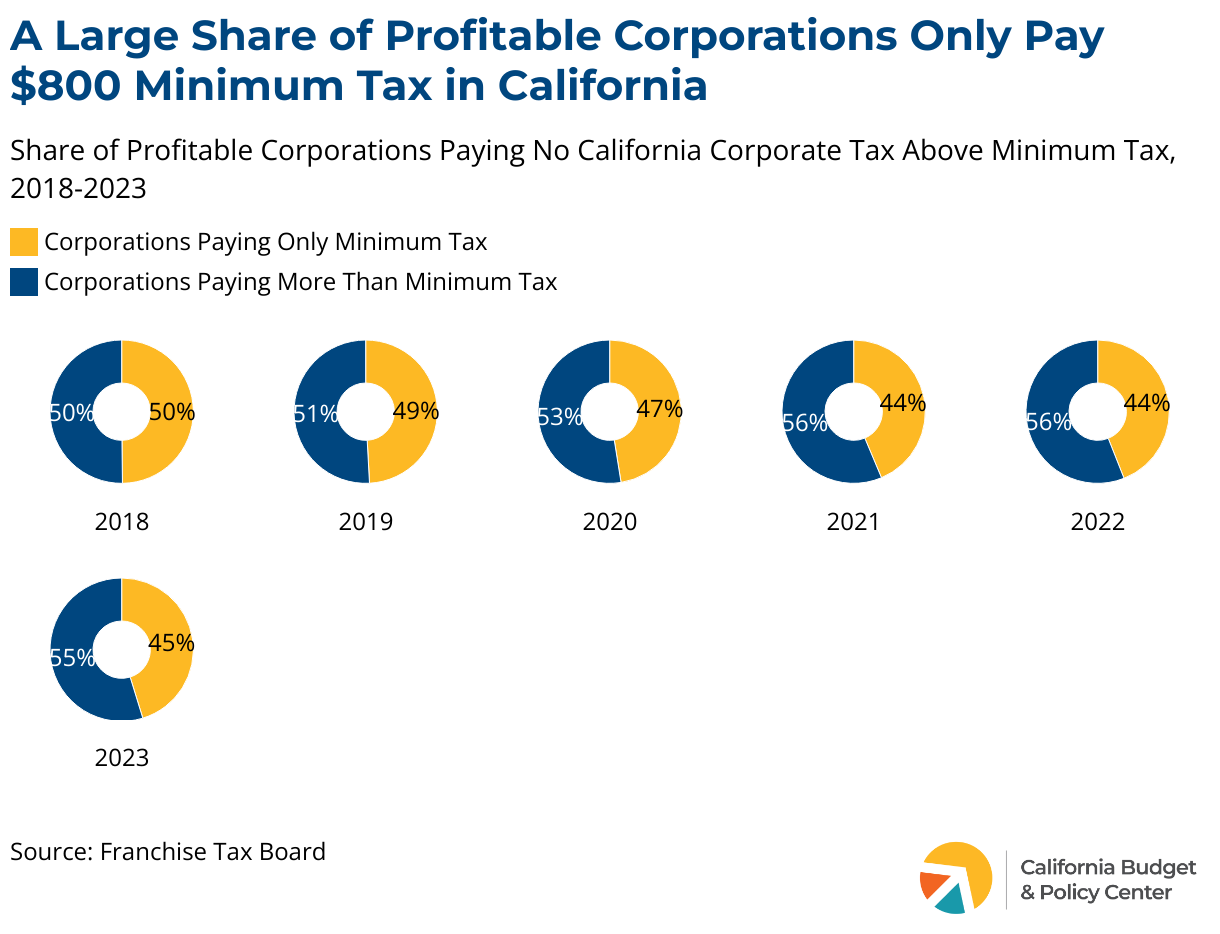

1. Many Corporations Only Pay the Minimum $800 State Tax

Most companies doing business in California are required to pay an $800 “minimum franchise tax” for the privilege of doing business in the state. Yet for nearly half of profitable corporations, this is all they pay in corporate tax to the state, even though they are turning a profit. They are able to do this by taking advantage of a variety of tax breaks that California policymakers have put into place over the years, such as generous tax credits that allow some corporations to essentially zero out their tax bills. For a corporation with $1 million in profits in California, paying only the $800 minimum state tax equates to an effective tax rate of 0.08% — while if it paid the full 8.84% statutory state corporate tax rate on those profits, it would owe $88,400.

Some corporations may also be profitable overall but make it look like they have no profits in the US or in California by shifting profits into foreign tax havens. They can then use the state’s water’s edge election to exclude those “foreign” profits from their total profits for the purposes of their California tax calculations and avoid paying taxes beyond the $800 minimum tax in California. Those corporations are not accounted for in the figures above, which only reflect the share of corporations reporting profits in California that only pay the minimum tax. There is no available data that would allow for distinguishing between corporations that are truly unprofitable and those that have used accounting mechanisms to shield profits from the reach of the state’s tax system.

2. Corporations are Receiving New Federal Tax Cuts, and Many are Paying No Federal Corporate Taxes

In 2017, Congress and the first Trump administration enacted major tax cuts, including slashing the federal corporate tax rate by 40%. In the first four years after those tax cuts, the largest and consistently profitable US corporations collectively saved about $240 billion in federal taxes, according to ITEP estimates. Moreover, after the 2017 law reduced the statutory tax rate from 35% to 21%, many corporations paid effective tax rates — the actual ratio of their tax bills to their profits — far below 21%. ITEP found that the effective tax rate was just 14% on average for Fortune 500 and S&P 500 companies that were consistently profitable from 2018 to 2022. Among this sample, 55 corporations had effective rates of less than 5%, and 23 paid nothing in federal tax across the entire 5-year period.

With H.R. 1, Congress and the second Trump administration doubled down on corporate tax cuts — making permanent some of the temporary tax breaks created in 2017 and rolling back provisions that were meant to raise corporate tax revenues to partially offset the cost of the steep corporate tax rate cut. Over a 10-year period, H.R. 1 will give corporations and other business tax cuts of more than $900 billion, while at the same time making the largest funding cuts to health care and food assistance in US history, which could result in up to 2 million Californians losing Medi-Cal coverage and more than 3 million households in the state losing some or all of their CalFresh food assistance — making life even less affordable for people struggling with the costs of living in the state.

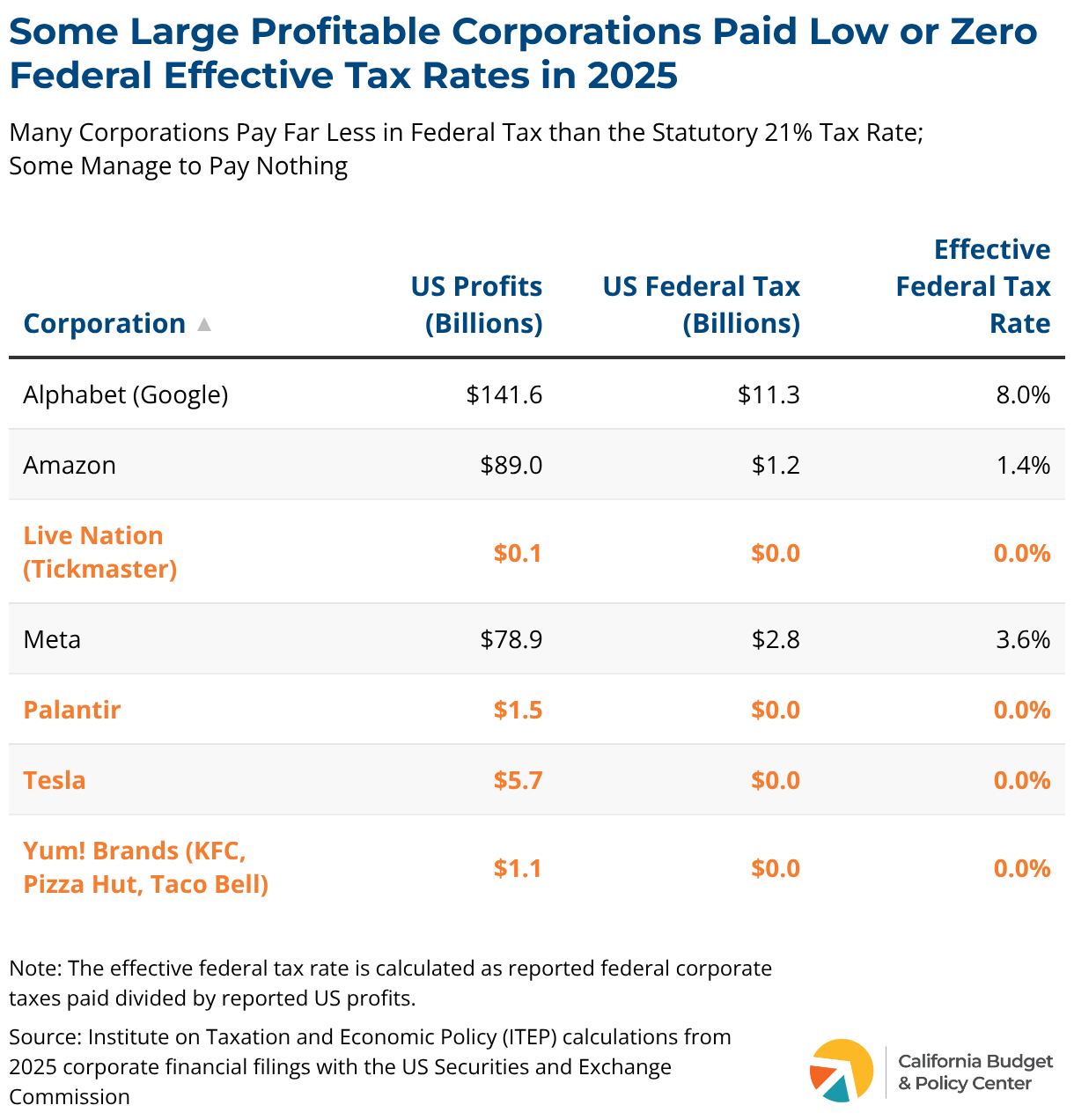

In the wake of H.R. 1, some huge corporations are already reporting that they are paying nothing in federal tax or very low effective tax rates despite soaring profits, at least in part thanks to provisions of the new tax law — including Alphabet (parent company of Google), Amazon, Live Nation (parent company of Ticketmaster), Meta, Palantir, Tesla, and Yum! Brands (parent company of Kentucky Fried Chicken, Pizza Hut, and Taco Bell).

3. Corporate Taxes Do Not Limit Businesses’ Ability to Pay Workers

California’s corporate tax is an 8.84% tax on the “net income” of corporations. Net income, or profit, represents the income left over after the corporation’s costs are accounted for — or total revenues minus total expenses. So corporations pay corporate taxes only in years when they are profitable, after they have paid their workers and accounted for other costs. If a corporation breaks even or has a net loss — if expenses exceed revenues — it is only subject to the flat $800 minimum tax. Additionally, it can use that “net operating loss” to offset its taxable income in future years when it is profitable, potentially reducing its tax bill to the minimum tax for several years.

4. Reducing Corporate Tax Avoidance Strategies for Large Corporations Will Not Push Businesses Out of State

For corporations doing business both in and outside of California, the state only taxes a portion of a corporation’s profits. For most types of corporations, this is equal to the portion of the corporation’s total sales made in the state (this proportion is known as its “sales factor”). The tax is not based on where a corporation’s workers, founders, headquarters, or other properties are located. This means a corporation moving its headquarters or other locations out of state will not reduce its tax liability as long as it continues to make sales to California’s customer base of nearly 40 million people.

In fact, an examination of corporate tax returns by the state’s Franchise Tax Board found evidence that corporate taxes are not driving corporations to leave the state. Looking at the tax returns of more than 100 corporations that made a public announcement about leaving or shifting some operations out of California, they found that more than 60% were paying nothing more than the $800 minimum tax and that, on the whole, they paid more in corporate tax to California in the year after their announced departures.

5. Corporate Tax Breaks Worsen Racial Disparities

Corporate tax breaks mainly benefit those who own stock in those corporations, who are disproportionately wealthy and white. Black, Latinx, and other households of color are less likely to own stock either directly or through retirement plans or other investment funds — and even among those who do own stock, the median value of stock holdings is lower among families of color than among white families. These differences reflect generations of disparities in economic opportunities — stemming from racist policies and practices — that have hindered wealth-building for families of color. For example, families of color are less likely to inherit generational wealth, occupational segregation has funnelled workers of color into lower-paying jobs with less access to retirement savings plans, and higher unemployment risks may make some families of color less willing to invest in riskier assets like stocks.

Due to these disparities, white households receive about 88% of the benefits of a corporate tax cut, despite making up only 67% of the population, according to national-level estimates from the Institute on Taxation and Economic Policy (ITEP). Meanwhile, Black and Latinx households each only receive about 1% of the benefits, even though they represent 12% and 9% of all households nationwide.

State Policymakers Should Ensure Profitable Corporations Pay Their Fair Share to Help Build a More Prosperous California for All

The maintenance of corporate tax breaks in California law has meant billions of dollars in lost revenues over the years — revenues that could have gone a long way in supporting the health, economic security, and well-being of Californians who have been excluded from economic opportunities and face impossible choices between paying the rent, feeding their families, and accessing health care.

Reining in corporate tax breaks and strengthening the state’s revenue base is long overdue, and even more critical now as the unmet needs of Californians are only growing and the federal safety net is being weakened. Two common-sense solutions are to close the “water’s edge loophole” and place reasonable limits on corporate tax credits and deductions so that no profitable corporation pays next to nothing in corporate taxes.