key takeaway

Proposition 3 will appear on the November 2026 statewide ballot, asking California voters whether to make permanent the higher-income tax rates on the state’s highest earners. These top tax rates were first enacted by voters in 2012 and renewed in 2016 to help fund schools, health care, and other supports for working families. Without action, the current rates are set to expire after 2030, reducing state revenues by billions of dollars annually and threatening funding for schools and state programs and services that support Californians every day.

table of Contents

- What Would Prop. 3 Do?

- Background on Prop. 30 and Prop. 55

- Who Pays the Voter-Approved Top Tax Rates?

- Without Voter-Approved Tax Rates, the Top 1% Would Receive Another Tax Credit

- Top Earners’ Incomes Have Soared

- What Have the Top Income Tax Rates Accomplished?

- Why Renewing the Top Tax Rates Matters for California

What Would Prop. 3 Do?

Prop. 3 would make permanent the rates put in place since 2012, preserving a key element of progressivity (requiring households with higher incomes to pay higher tax rates) in the state’s revenue structure that funds critical investments that improve the quality of life for all Californians. The measure would not raise taxes or change existing income tax rates; it simply removes the expiration date on current tax rates for the state’s highest earners. Revenues would continue to support the entire state General Fund budget by helping meet the TK-14 constitutional funding guarantee and freeing up revenue for other programs and services, just as they have since 2012.

Background on Prop. 30 and Prop. 55

In 2012, after the state faced significant revenue losses as a result of the Great Recession, California voters approved Proposition 30, which added new income tax brackets for the state’s highest earners (10.3%, 11.3%, and 12.3%, depending on household income) and included a temporary sales tax increase. Both the income tax rates and the sales tax increase were temporary, with the sales tax set to expire in 2016 and the income tax rates in 2018. Proposition 30 also created the Education Protection Account, a state account in the General Fund that receives and disburses revenues from the top income tax rates.

what is the education protection account (epa)?

Proposition 30 (2012) established the Education Protection Account, a state account where revenues from the top income tax rates are deposited. Of the funds in the account, 89% are distributed to schools and 11% to community colleges. This revenue is treated as General Fund revenue, subject to constitutional requirements including Prop. 98 (1988), the state’s minimum funding guarantee for TK-14 education, and Prop. 2 (2014), which established rules for building state budget reserves and paying down state debts. The revenue deposited into the EPA increases the Prop. 98 guarantee and is used to help meet the guarantee, freeing up General Fund revenue for other state budget priorities.

In 2016, voters approved Proposition 55, which extended the income tax rates for another 12 years (to 2030), while allowing the sales tax to expire as scheduled. Prop. 55 also added a constitutional formula intended to increase funding for the Medi-Cal program when revenues exceed a certain threshold. This specific formula has never directed funds to Medi-Cal, and the current measure would allow it to expire. However, top tax rate revenues do support the Medi-Cal budget indirectly through the General Fund capacity generated by Prop. 55.

Since their initial enactment in 2012, these higher tax rates have generated around $120 billion for schools and other essential services. In recent years, the higher rates have generated around $10 billion annually. These revenues now form a core component of the state budget, supporting the TK-14 education budget, strengthening General Fund capacity to support other vital programs and services, and building reserves.

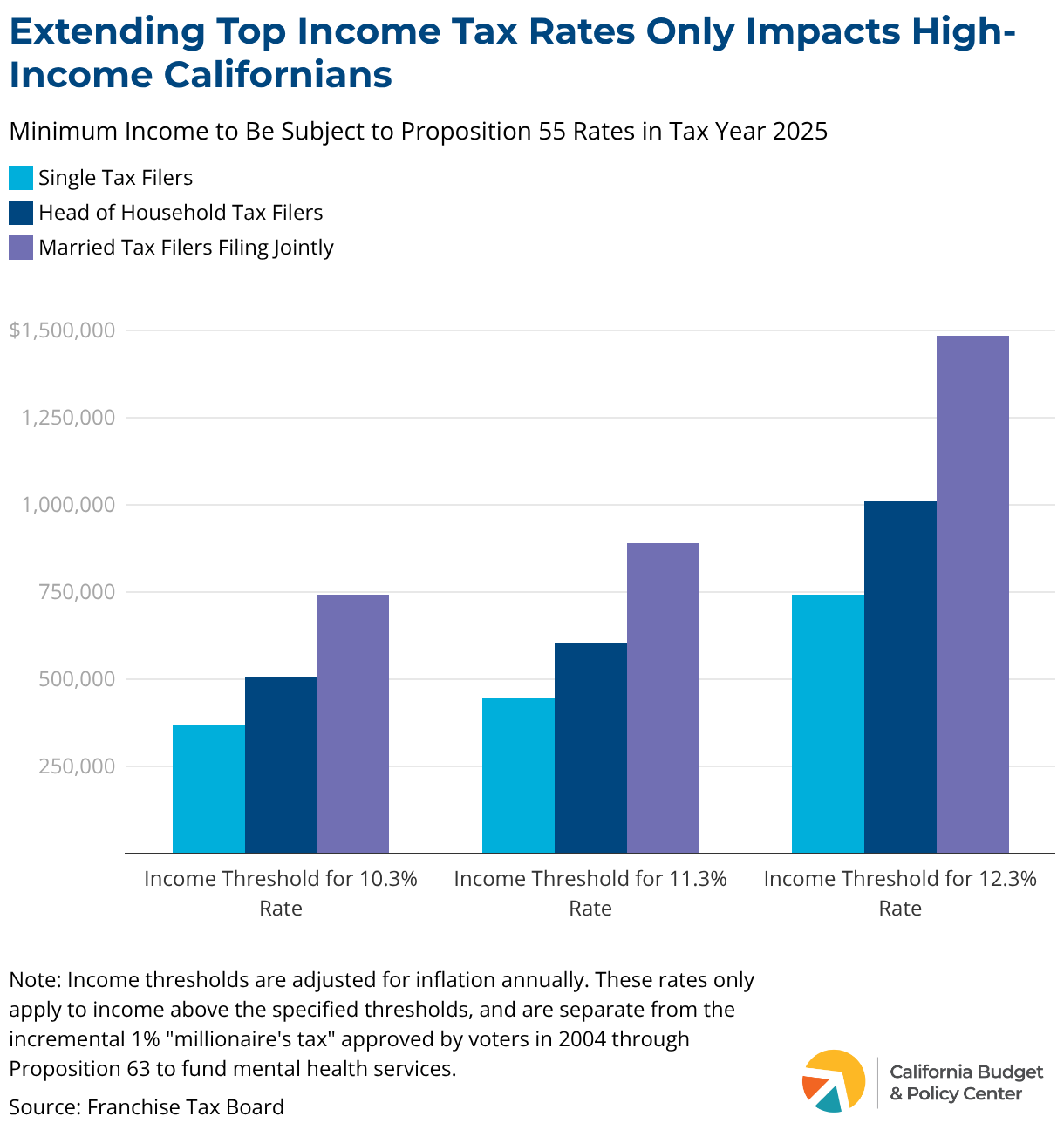

Who Pays the Voter-Approved Top Tax Rates?

The voter-approved top tax rates only impact the highest-income Californians.

These rates only apply to the top 2% of California tax filers. In tax year 2025, these top rates only applied to people with incomes above around $371,000 for single tax filers and about $743,000 for married couples filing jointly. These thresholds increase annually with inflation.

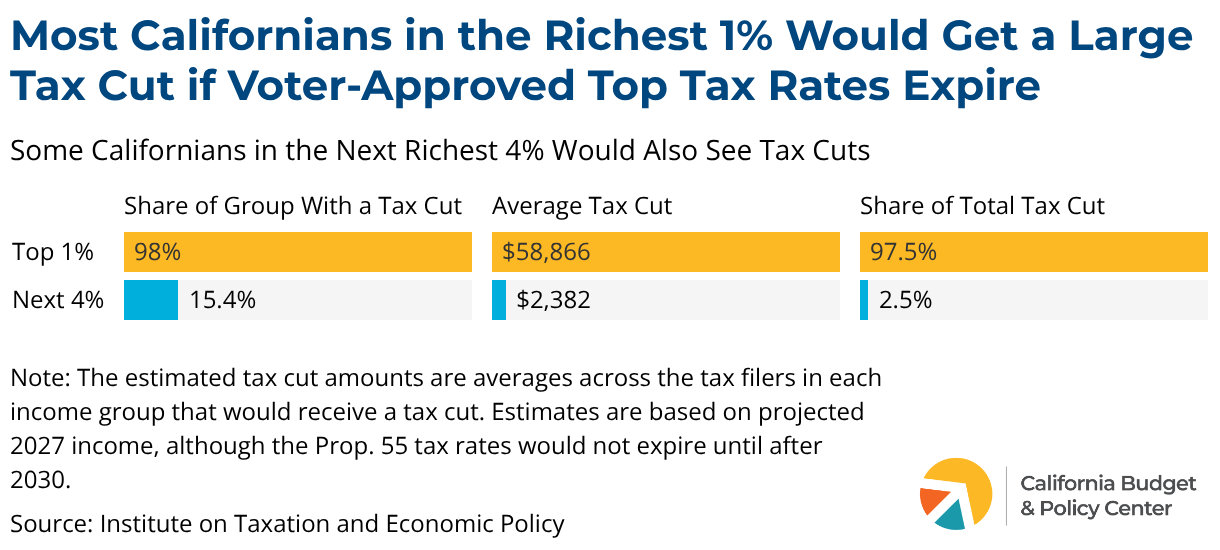

Without Voter-Approved Tax Rates, the Top 1% Would Receive Another Tax Cut

The top-earning 1% of Californians would receive a major tax cut if Prop. 55 rates are not extended. If the voter-approved top tax rates are allowed to expire, the vast majority of tax filers in the top 1% by income would receive an average annual tax cut of nearly $59,000, according to estimates from the Institute on Taxation and Economic Policy. This top 1% group would get about 98% of the total tax cuts. The remaining tax cuts would go to some households in the next 4% of highest-income filers.1Not all households in the top 5% or top 1% would receive tax cuts from the expiration of the top tax rates for several reasons. First, filers are subject to the top tax rates if their taxable income — that is, income after accounting for allowed exemptions and deductions — exceeds the thresholds established by Prop. 30 and Prop. 50. In contrast, the thresholds for the top 5% and top 1% used by the Institute on Taxation and Economic Policy for this analysis are based on total income before exemptions and deductions. So tax filers in the top 1% by total income may have taxable incomes under the threshold for the top rates. Second, some high-income filers that use specific tax preferences may be subject to an “alternative minimum tax,” which could be triggered if their regular tax bill were reduced. And finally, because thresholds for these rates vary by household type, a married couple filing a joint tax return with a total income of $500,000 falls into the top 5% of all tax filers, but their total income — even before accounting for exemptions and deductions — is below the threshold for the Prop. 55 taxes of around $743,000, for example. Around 15% of this group would receive a tax cut, averaging more than $2,000 annually. Californians in all other income groups would see no change to their taxes.

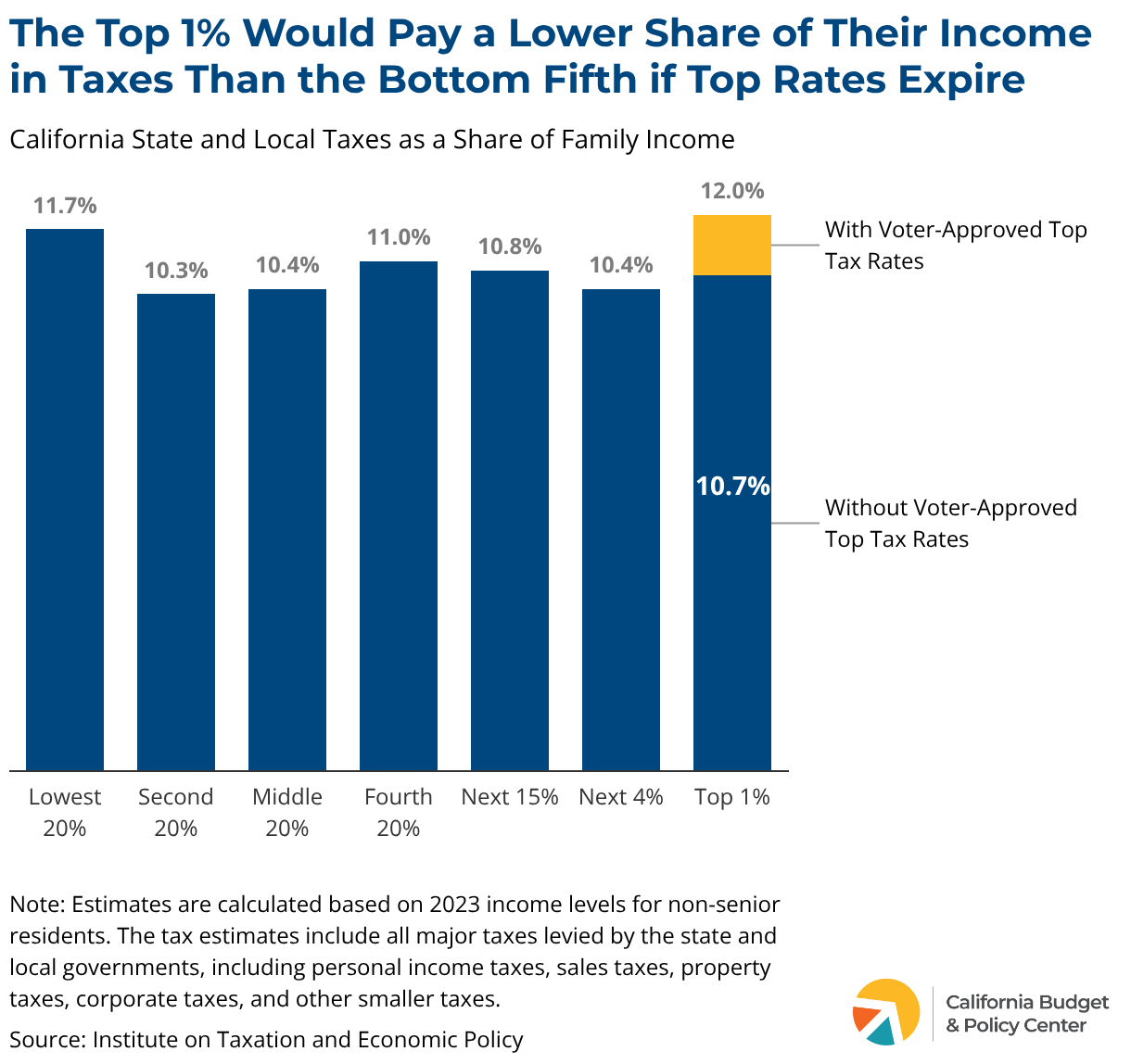

California’s tax system would be more regressive if the Prop. 55 tax rates expire. A regressive tax system is one in which lower-income households pay larger shares of their income in taxes than higher-income households. In contrast, in a progressive tax system, higher-income people pay higher shares of their income in taxes. California’s tax system is more progressive than many other state tax systems, in large part due to these voter-approved top tax rates that are up for renewal under Prop. 3.

When you add up the various state and local taxes that Californians pay — including the sales tax, property tax, and other types of taxes — the highest-income 1% currently pay about 12% of their income in taxes on average. That’s barely more than the 11.7% paid by Californians in the lowest 20% by income. If the top rates were not in effect, the top 1% would pay only about 10.7% of their income in state and local taxes — lower than what the bottom fifth of Californians pay.

Top Earners’ Incomes Have Soared

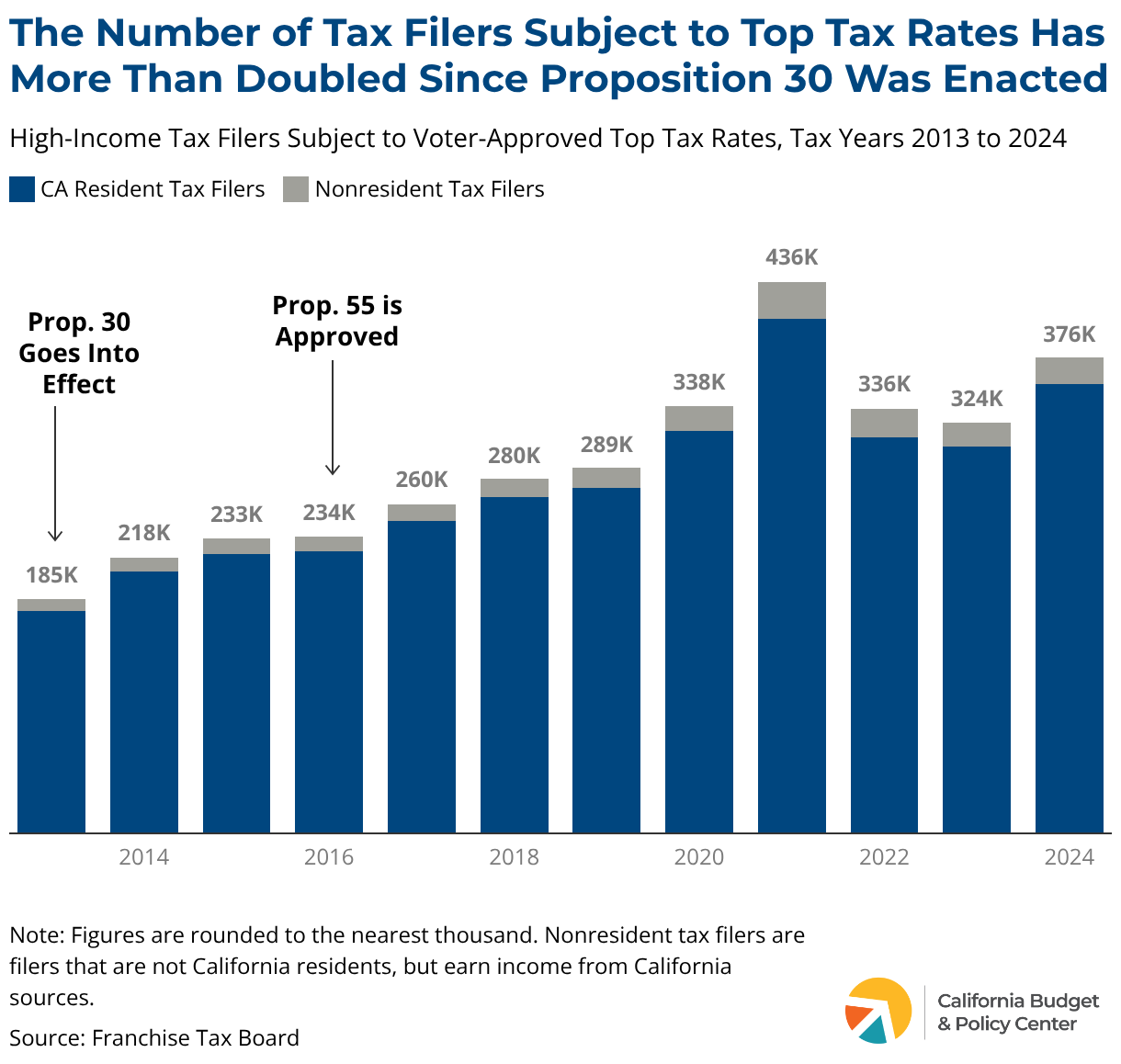

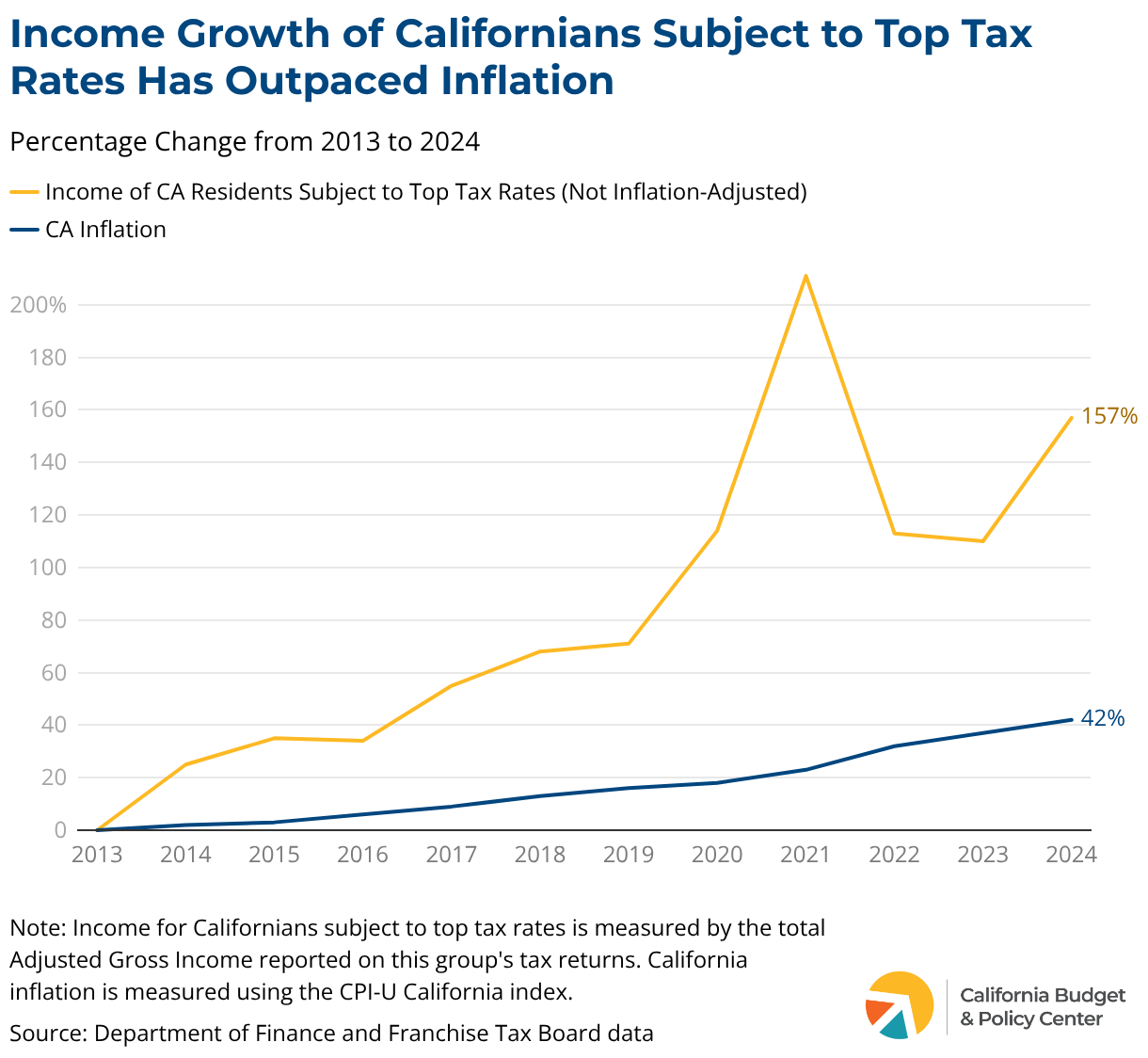

The number of Californians with incomes high enough to be subject to the voter-approved top tax rates has more than doubled, reflecting soaring incomes among top earners. Around 185,000 tax filers, including more than 175,000 California resident filers, had incomes above the thresholds for Prop. 30’s top tax rates in 2013, the first year the rates were in effect. By 2024 (the latest available data), the number had reached nearly 376,000, including around 355,000 California residents.2“Tax filer” represents a tax filing unit — the primary filer as well as any spouses and dependents included on the tax return. A tax filing unit can be an individual, a couple, or a family, and in some cases can include unrelated dependents. This increase is due to the incomes of these high-income households growing much faster than inflation over this period.

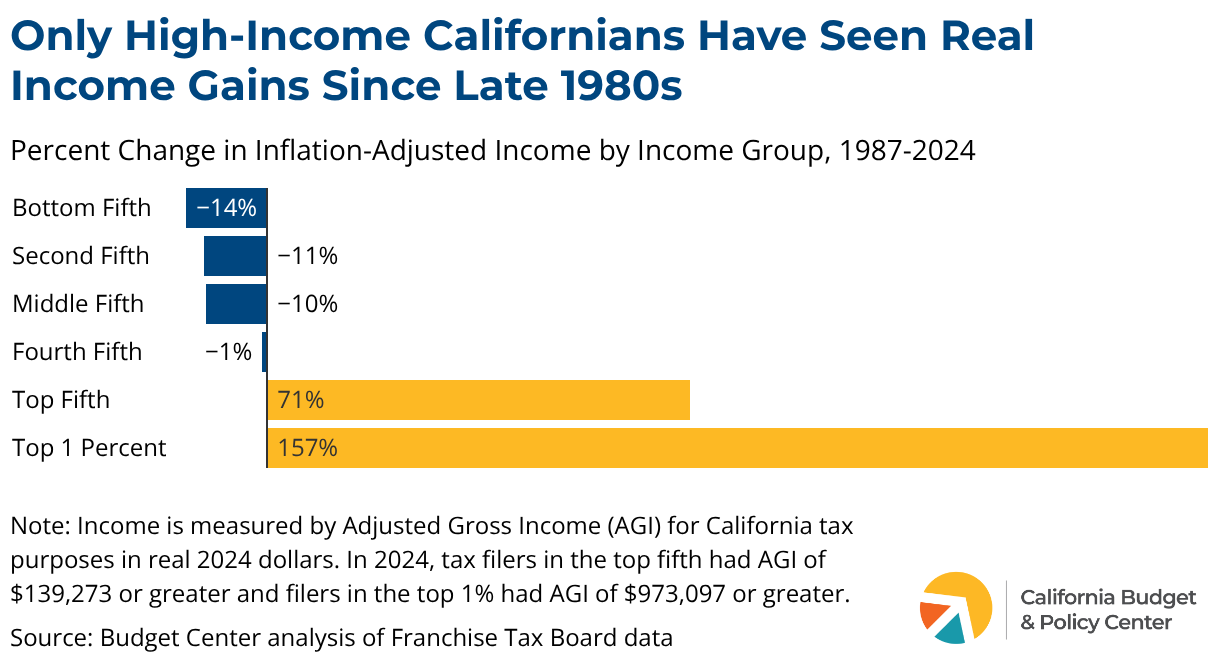

Californians subject to the top tax rates have seen their incomes grow dramatically over the past several decades, while most Californians have lost ground or experienced income declines after adjusting for inflation. The top 1% of Californians saw their inflation-adjusted incomes increase more than 2.5 times (157%) between 1987 and 2024, while those in the bottom 80% saw decreases in real income over that time.

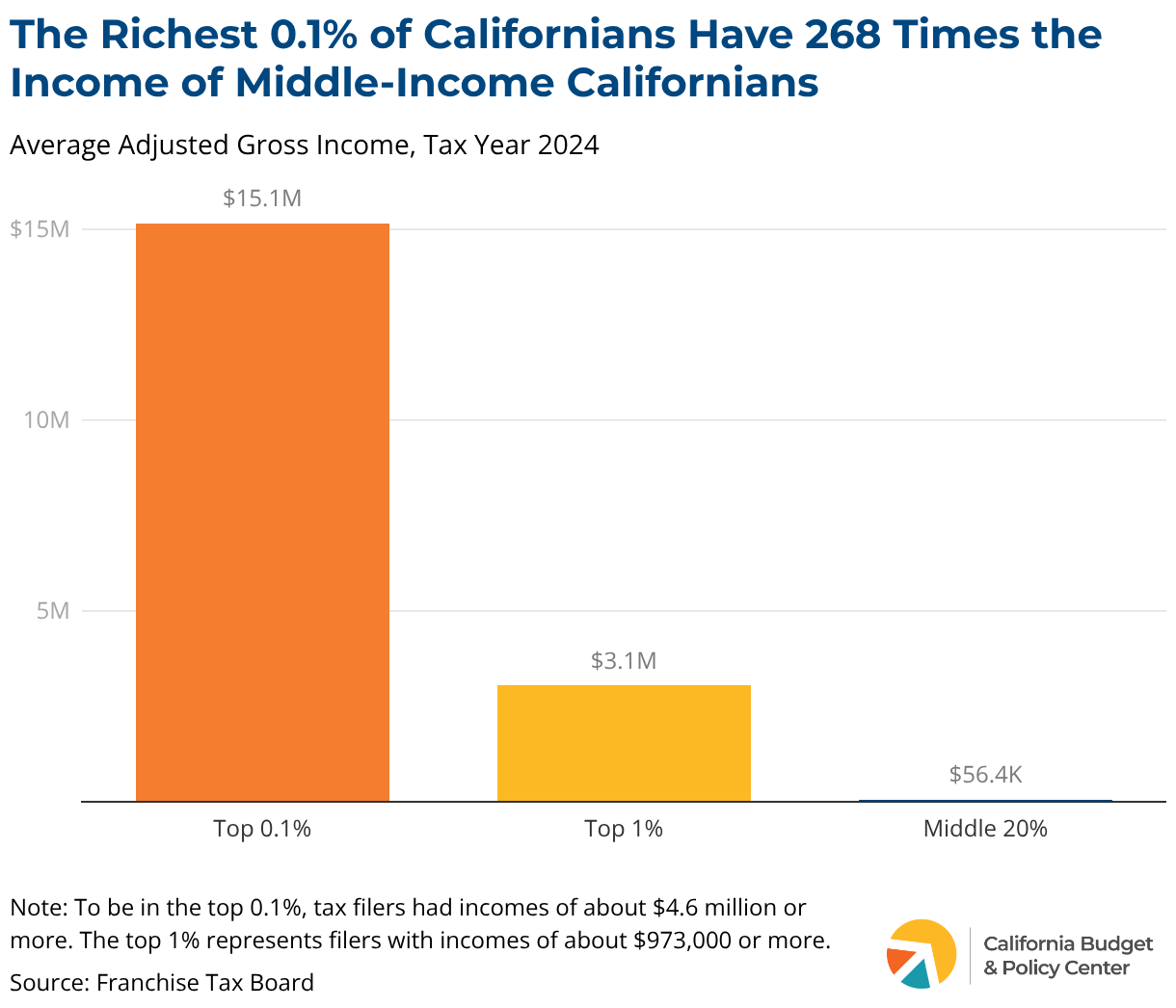

To be in the top 1%, a tax filer had an income of at least $973,097 in 2024. On average, this group reported more than $3 million per tax return in 2024 — about 54 times the income of the middle fifth of Californians, who earned around $56,000 on average. In even starker contrast, the top 0.1% had an average income of over $15 million — 268 times that of the middle fifth of Californians. In other words, someone in the top 1% can earn in just under one week what the average middle-income Californian earns in an entire year, and someone in the top 0.1% can earn that amount in just over a day.

What Have the Top Income Tax Rates Accomplished?

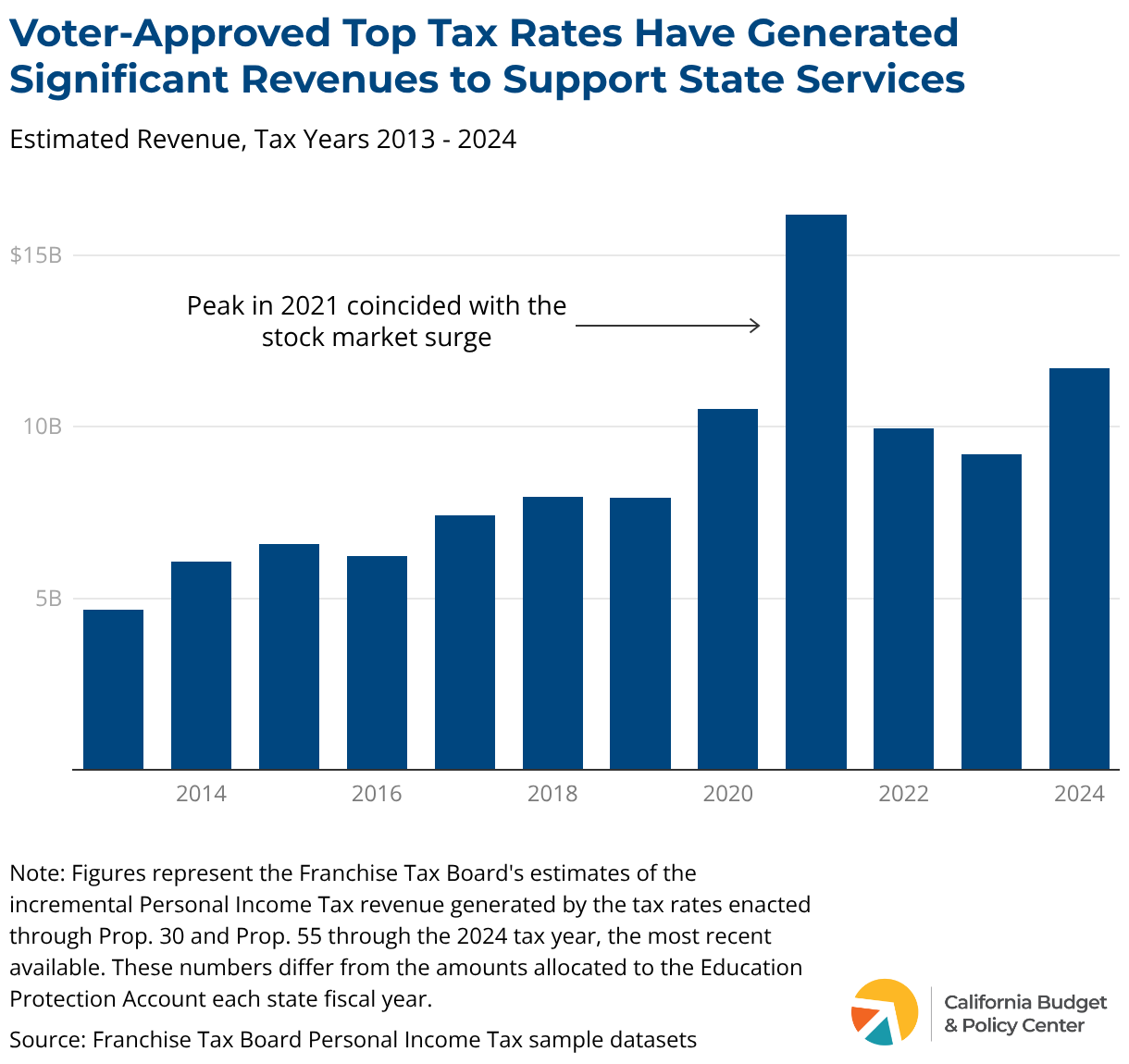

Since the passage of Prop. 30 in 2012, the top tax rates have generated about $120 billion in state revenue.3This figure reflects revenues from the top tax rates allocated to TK-14 education from the Education Protection Account (EPA) through the 2024-25 fiscal year. On average, this revenue has represented about 5.5% of total General Fund revenues. The funds raised by the top tax rates approved by voters through Prop. 30 and Prop. 55 have been a major revenue source for the state, supporting critical services including education, health care, and economic security programs. This revenue has also helped the state to build up budget reserves to be better prepared for downturns when revenues decline or come in lower than expected.

The annual revenue raised by the top tax rates has increased in line with overall state revenues. These revenues are sensitive to stock market fluctuations, as a large share of the income of high-income households comes from earnings on investments such as dividends and capital gains. For example, Prop. 55 revenues peaked at more than $16 billion when the stock market surged in 2021 and then subsequently fell in line with the stock market decline in the following years, before growing to nearly $12 billion in 2024. The sensitivity of these revenues to economic conditions makes it all the more important that state leaders have the capacity to save revenues during high-revenue years in the state’s budget reserves for future downturns, as required under Prop. 2 of 2014 — which may be modified to require additional savings in some strong-revenue years if voters approve changes to the existing measure with Prop. 2 on the November 2026 ballot.

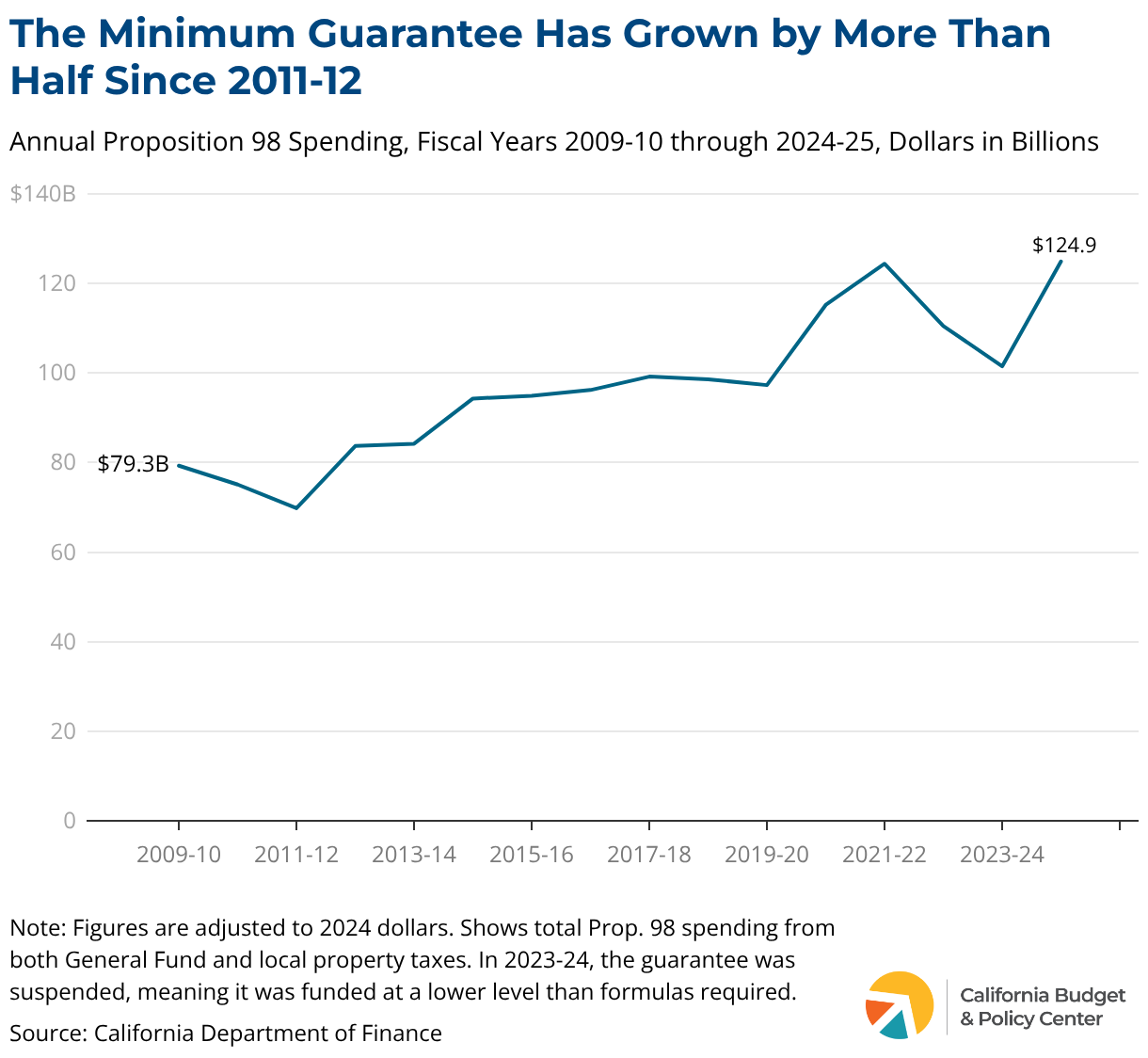

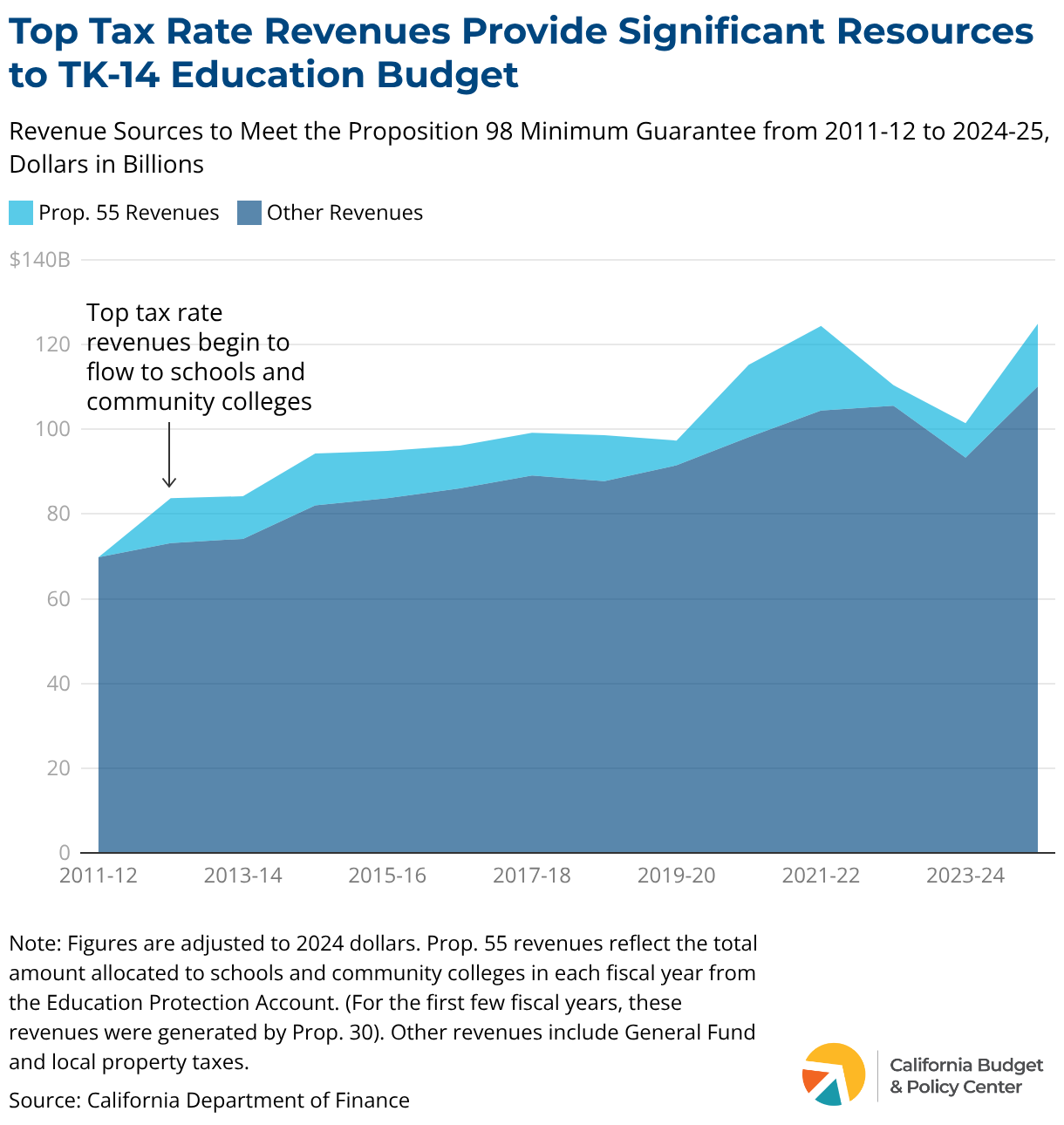

Top tax rate revenues provide critical support for schools and community colleges. Top tax rate revenues serve two purposes for the TK-14 education budget: 1) increase the Prop. 98 minimum guarantee’s annual calculation and 2) provide the revenues needed to meet the guarantee. Because top tax rate revenues count as General Fund revenues, they directly affect how the annual Prop. 98 level is calculated. In years when the General Fund experiences strong growth, the guarantee is set as a share (about 40%) of General Fund revenues, establishing a higher floor.4The minimum guarantee is determined using one of three formulas: 1) approximately 40% of General Fund revenue, 2) the prior year level adjusted for K-12 attendance growth and growth in per capita personal income, or 3) the prior year level adjusted for K-12 attendance growth and per capita General Fund revenue growth. In other years, the guarantee builds on the prior year’s level, carrying forward the growth built when revenues were strong. Regardless of how the guarantee is calculated, the effect of the top tax rate revenue is cumulative. As shown in the chart below, the guarantee has grown on an ongoing basis since 2012-13, with part of this growth attributable to the top tax rates.

what is proposition 98?

Prop. 98 is a constitutional amendment adopted by California voters in 1988 that establishes an annual minimum funding level for TK-14 education each fiscal year, commonly referred to as the minimum guarantee. Prop. 98 funding comes from a combination of state General Fund revenue and local property taxes. Prop. 98 spending supports TK-12 schools, community colleges, county offices of education, the state preschool program, and state agencies that provide direct TK-14 instructional programs. While Prop. 98 establishes a required minimum funding level for programs falling under the guarantee as a whole, it does not protect individual programs from reduction or elimination.

In addition to raising the guarantee’s calculation, Prop. 55 revenues directly help meet the guarantee. Revenues from the top tax rates are used to meet the Prop. 98 obligation, which frees up General Fund dollars that would otherwise be needed to meet the guarantee. These freed-up dollars are used to support non-TK-14 programs, build state reserves, and pay down debts. Since 2012-13, when these revenues began to flow to schools and community colleges, Prop. 55 revenues have provided about $120 billion to help meet the TK-14 budget.5While the top tax rate revenues have provided approximately $120 billion to the TK-14 budget through the EPA, because these revenues also reduce the General Fund dollars to meet the guarantee, the overall education funding impact is approximately 40% of total revenues.

The chart below shows the growth in the minimum guarantee, and the share provided by the top tax rate revenues, adjusted to 2024 dollars. Throughout this period, top tax rate revenues have enabled the state to implement key educational programs. For example, in the 2013-14 school year, policymakers began implementing a major school finance reform to more equitably allocate dollars to school districts based on student need.

- Top tax rate revenues have also created more General Fund capacity to support critical economic security, housing, and health programs.

- Prop. 30 and Prop. 55 have increased the state’s capacity to save for a rainy day and pay down debts.

Why Renewing the Top Tax Rates Matters for California

As the revenues from the current top tax rates have become a critical source of funding for education, health care, and other state services, their expiration after 2030 would likely lead to significant budget shortfalls. If Prop. 3 does not pass — and state leaders or voters do not approve alternative revenues — funding for essential state services would be put in jeopardy. This is especially concerning given that state officials already project ongoing budget deficits in upcoming years, as the cost of existing state services is growing due to inflation and a changing population, and revenue growth is not keeping up. Those projected deficits, compounded by federal cuts resulting from H.R. 1, the 2025 federal budget reconciliation law known as the “One Big Beautiful Bill Act,” would put significant pressure on the state budget and the programs it supports.

In recent years, the top tax rates have contributed around $10 billion annually to the state budget, and the Legislative Analyst’s Office projects that making these rates permanent would bring in between $5 billion and $15 billion annually in the future — depending on the economy and stock market performance. The loss of $5 billion to $15 billion could mean:

- Reduced General Fund resources to protect and strengthen services that keep Californians healthy, housed, and economically secure. In recent years, more than two-thirds of state spending growth from available revenues has gone simply to sustaining existing levels of services, including keeping pace with rising costs and growing caseloads in programs like Medi-Cal, In-Home Supportive Services, and child care. The loss of Prop. 55 revenues would worsen existing deficit projections, making it harder for the state to maintain even current levels of services, potentially leading to programmatic cuts to essential programs.

- The loss of a key revenue stream and increased pressure to meet the Prop. 98 minimum guarantee. In the near term, without Prop. 55 revenues, the state would need to replace billions in funding from other General Fund sources to meet the guarantee, crowding out other budget priorities. This is because Prop. 98 would not automatically be reduced to account for the immediate and substantial General Fund revenue decline. Over time, lower General Fund growth absent top tax rate revenues could result in the guarantee growing more slowly than it otherwise would. Overall, the loss of a dedicated revenue stream and a potentially slower-growing guarantee could result in approximately $2 billion to $6 billion less annually for the TK-14 budget than would otherwise be available.

- A reduced capacity to save and prepare for economic downturns. Without the additional revenues from the current top tax rates, deposits into the state’s rainy day fund and debt repayments required by Prop. 2 would be lower. This would leave the state less resilient when the next recession arrives, making critical state services more vulnerable to cuts.

- Diminished ability to respond to anticipated federal cuts. The 2025 budget reconciliation package, H.R.1, includes significant cuts to health care and food assistance. Cuts to health care could total tens of billions each year. On top of that, cuts to food assistance could cost the state more than $5 billion annually. Currently, the state budget does not have the General Fund capacity to fully address these cuts, and the loss of top tax rates would only increase the millions of Californians at risk of losing these critical services.