For the Center on Budget and Policy Priorities’ annual state policy conference, IMPACT 2017: Building Power, Advancing Equity, Senior Policy Analyst Sara Kimberlin delivered a presentation for: “EITC Workshop: May the (EITC) Force Be With You.”

You may also be interested in the following resources:

-

Fact Sheet

Young Californians Face Alarmingly High Rates of Poverty and Deep Poverty

key takeaway Young adults across California face higher-than-average poverty and deep poverty rates as they transition into adulthood, underscoring the need to strengthen core basic needs programs and investments that help young Californians achieve economic stability and meet their basic needs. Young adulthood is a crucial time to establish independence and start to build financial … ContinuedCalFreshMedi-CalPoverty & Inequality -

Report

Federal and State Budget Decisions Threaten AANHPI Women in California

key takeaway AANHPI women’s experiences vary widely across ethnicities, making disaggregated data essential to understanding the impacts of recent federal and state decisions. By examining the Women’s Well-Being Index indicators across multiple AANHPI ethnicities, this report highlights distinct challenges facing AANHPI women in California and identifies key steps state and local leaders can take to … ContinuedPoverty & Inequality

Stay in the know.

Join our email list!

For the California State Assembly Aging and Long-Term Care Committee’s “Informational Hearing on Consequences of Federal Policy Changes on California’s Seniors,” Director of Research Scott Graves provided an overview on federally supported long-term care and support services.

You may also be interested in the following resources:

-

Fact Sheet

Young Californians Face Alarmingly High Rates of Poverty and Deep Poverty

key takeaway Young adults across California face higher-than-average poverty and deep poverty rates as they transition into adulthood, underscoring the need to strengthen core basic needs programs and investments that help young Californians achieve economic stability and meet their basic needs. Young adulthood is a crucial time to establish independence and start to build financial … ContinuedCalFreshMedi-CalPoverty & Inequality -

Report

Federal and State Budget Decisions Threaten AANHPI Women in California

key takeaway AANHPI women’s experiences vary widely across ethnicities, making disaggregated data essential to understanding the impacts of recent federal and state decisions. By examining the Women’s Well-Being Index indicators across multiple AANHPI ethnicities, this report highlights distinct challenges facing AANHPI women in California and identifies key steps state and local leaders can take to … ContinuedPoverty & Inequality

Stay in the know.

Join our email list!

For the Association for Public Policy Analysis and Management’s (APPAM) fall research conference, “Measurement Matters: Better Data for Better Decisions.” Senior Policy Analyst Sara Kimberlin presented a research paper for the panel “Measuring the Impact of Policy Changes on Poverty in the United States.”

You may also be interested in the following resources:

-

Fact Sheet

Young Californians Face Alarmingly High Rates of Poverty and Deep Poverty

key takeaway Young adults across California face higher-than-average poverty and deep poverty rates as they transition into adulthood, underscoring the need to strengthen core basic needs programs and investments that help young Californians achieve economic stability and meet their basic needs. Young adulthood is a crucial time to establish independence and start to build financial … ContinuedCalFreshMedi-CalPoverty & Inequality -

Report

Federal and State Budget Decisions Threaten AANHPI Women in California

key takeaway AANHPI women’s experiences vary widely across ethnicities, making disaggregated data essential to understanding the impacts of recent federal and state decisions. By examining the Women’s Well-Being Index indicators across multiple AANHPI ethnicities, this report highlights distinct challenges facing AANHPI women in California and identifies key steps state and local leaders can take to … ContinuedPoverty & Inequality

Stay in the know.

Join our email list!

State and National Leaders Must Do More to Promote Economic Security and Opportunity

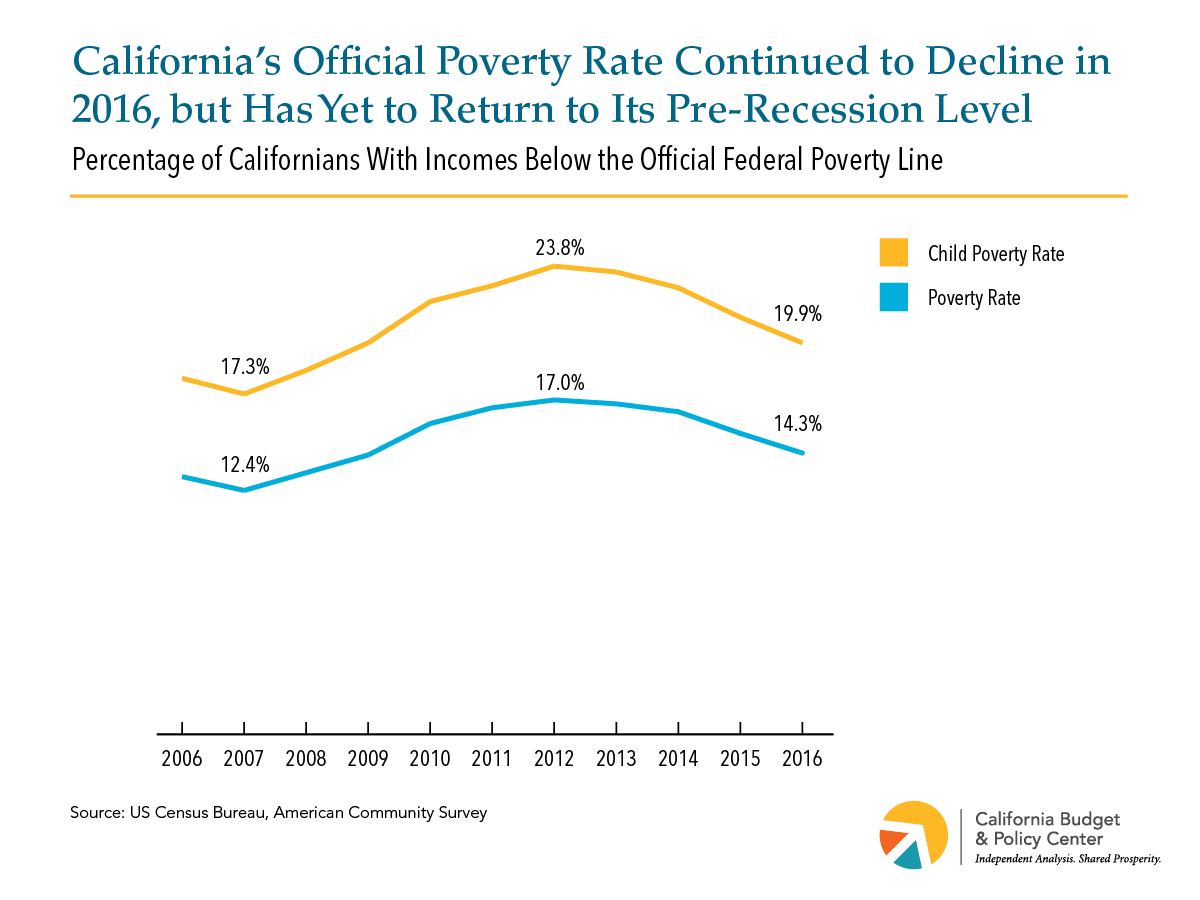

New Census figures released today show that millions of people in California continue to struggle to get by on extremely low incomes in spite of our state’s recent economic gains. More than 5.5 million Californians, including almost 1.8 million children, lived in poverty in 2016 based on the official poverty measure. In addition, poverty remained more widespread last year than it was in 2007 when the national recession began. Specifically, 14.3 percent of Californians had incomes below the official poverty line in 2016, down from a recent high of 17.0 percent in 2012, but still well above the state poverty rate in 2007 (12.4 percent). Also, roughly 1 in 5 California children lived in poverty last year (19.9 percent), down from a recent high of 23.8 percent in 2012, but still well above the child poverty rate in 2007 (17.3 percent).

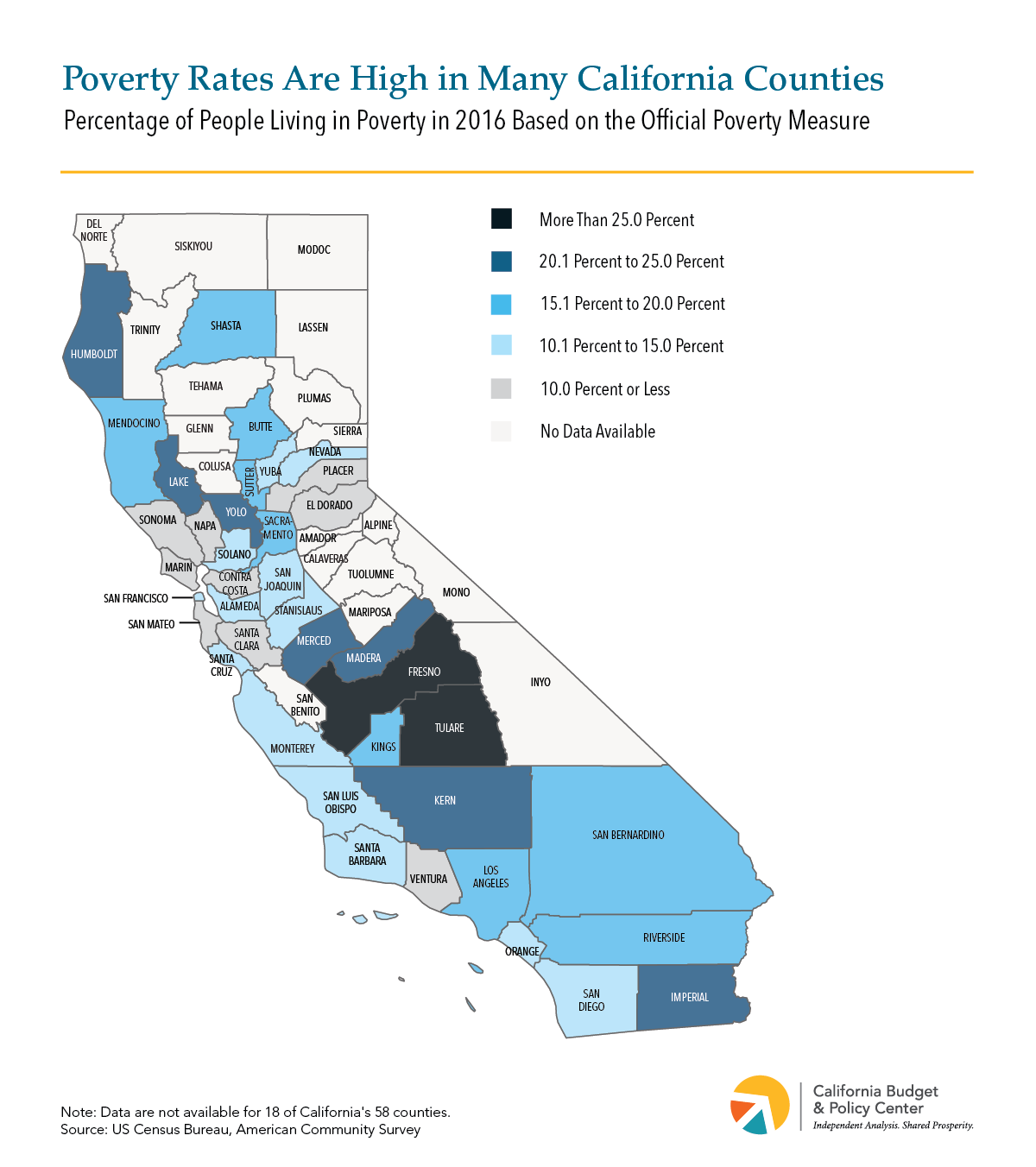

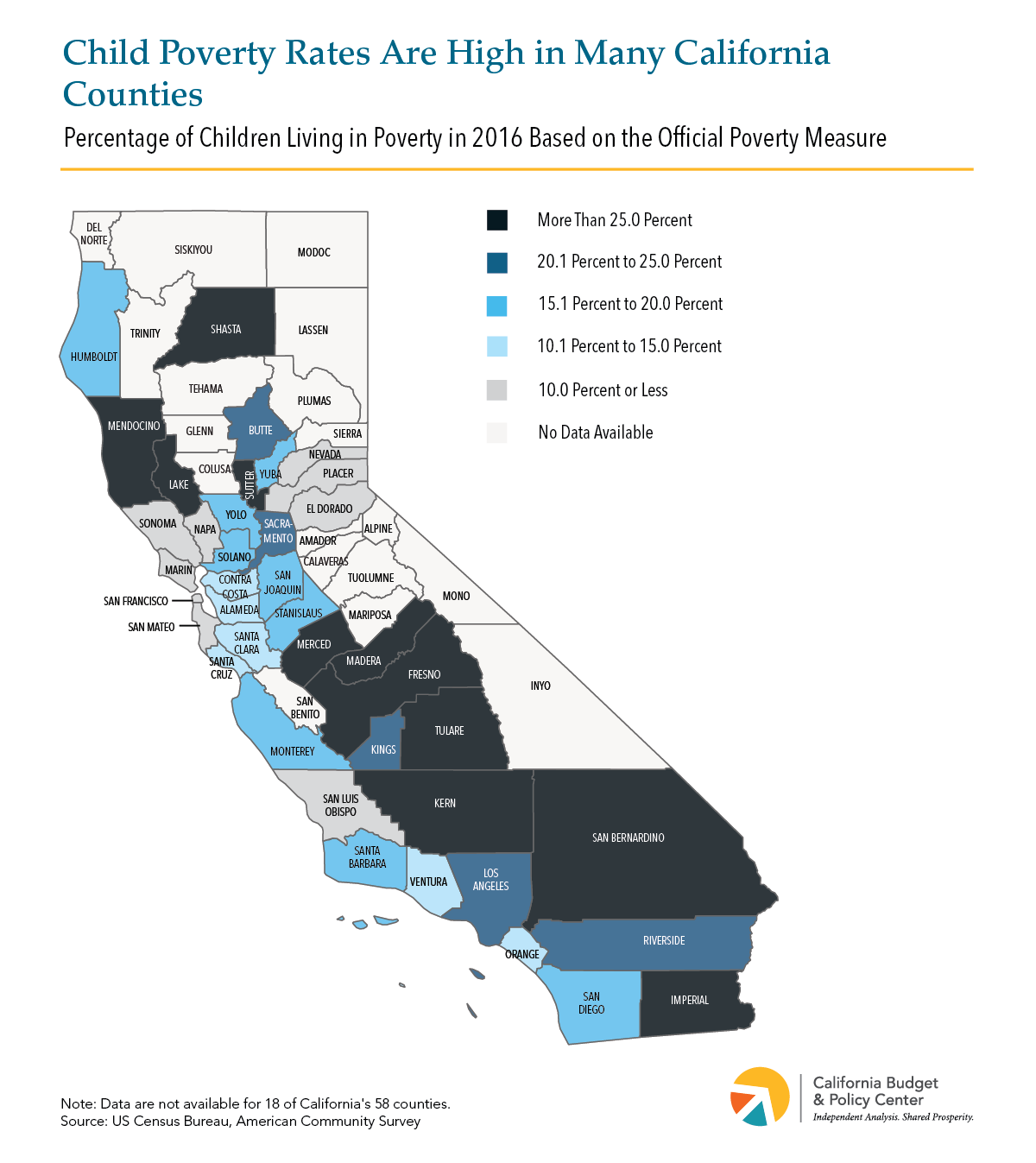

The latest Census figures also show that there are stark differences in people’s economic well-being across California’s counties. The 2016 official poverty rate ranged from a low of 6.5 percent to a high of 25.6 percent across the counties, while the official child poverty rate ranged from 5.2 percent to 37.9 percent. More than 1 in 5 people lived in poverty in nine counties, most of which are in the Central Valley (see Map 1). Additionally, more than 1 in 5 children lived in poverty in 16 counties, including six counties — again, most in the Central Valley — where over 30 percent of children were in poverty (see Map 2).

Map 1

Map 2

Download the data for the maps above.

Although the Census figures published today show that poverty remains high, they understate the extent of hardship in California because they reflect an outdated measure of poverty. Census figures released earlier this week based on an improved measure — the Supplemental Poverty Measure (SPM) — which accounts for the high cost of housing in many parts of the state, show that roughly 8 million Californians per year, 1 in 5 state residents (20.4 percent), could not adequately support themselves and their families between 2014 and 2016. Under this more accurate measure of hardship, California continues to have the highest poverty rate of the 50 states.

The new Census poverty figures underscore the need for state and national leaders to do more to ensure that all people can share in our state’s economic progress. Specifically, policymakers should:

- Reject steep cuts to economic security programs that help families make ends meet and get ahead. A majority of adults will experience economic hardship for at least one year during their prime working years, and nearly half will turn to a major public support, such as SNAP food assistance (CalFresh in California), to get back on their feet. These supports not only lift millions of Californians out of poverty each year, but also help children succeed over the long-term, according to research. Yet federal policymakers have proposed slashing critical supports that promote economic security and opportunity. If enacted, these cuts would drive California’s already high poverty rate even higher and threaten the future of our state’s children. People in communities all throughout the state would likely be harmed.

- Help families afford decent housing. With housing costs far outpacing many families’ earnings in recent years, it has become increasingly challenging for people with low incomes to keep a roof over their heads. Over half of California renters are housing “cost-burdened,” meaning that they pay more than 30 percent of their income toward housing, and nearly 30 percent are severely housing cost-burdened, spending over half of their income on housing. Since housing costs are most families’ biggest expense, addressing the housing affordability crisis is key to broadening economic security in California. The Legislature is considering a package of bills that would take important first steps toward addressing this crisis through policies that are designed to increase housing supply, including production of affordable units. Given the large scale of the housing crisis, additional strategies outside of the housing arena will also continue to be critical to help families with low incomes pay for basic necessities like housing.

- Make sure workers earn enough to support themselves and their families. Most families in poverty work, which means that low pay and not enough work hours are key barriers to economic security and opportunity. California has recently made important strides to bolster workers’ economic well-being. For example, the state last year committed to gradually raise the state’s minimum wage to $15 per hour by 2023, and the lowest-paid workers in our state have already seen their hourly earnings increase significantly. California also created and then subsequently expanded the California Earned Income Tax Credit (CalEITC) — a refundable state tax credit that helps low-earning workers pay for basic necessities. Policymakers could build on this progress by increasing the size of the CalEITC and making sure that workers get the full benefit of the rising minimum wage by instituting practices that help part-time workers access additional work hours.

You may also be interested in the following resources:

-

Fact Sheet

Young Californians Face Alarmingly High Rates of Poverty and Deep Poverty

key takeaway Young adults across California face higher-than-average poverty and deep poverty rates as they transition into adulthood, underscoring the need to strengthen core basic needs programs and investments that help young Californians achieve economic stability and meet their basic needs. Young adulthood is a crucial time to establish independence and start to build financial … ContinuedCalFreshMedi-CalPoverty & Inequality -

Report

Federal and State Budget Decisions Threaten AANHPI Women in California

key takeaway AANHPI women’s experiences vary widely across ethnicities, making disaggregated data essential to understanding the impacts of recent federal and state decisions. By examining the Women’s Well-Being Index indicators across multiple AANHPI ethnicities, this report highlights distinct challenges facing AANHPI women in California and identifies key steps state and local leaders can take to … ContinuedPoverty & Inequality

Stay in the know.

Join our email list!

State and National Leaders Must Do More to Promote Economic Security and Opportunity

Around 8 million Californians — roughly 1 in 5 state residents (20.4 percent) — cannot adequately support themselves and their families, according to new Census figures released this morning based on the Supplemental Poverty Measure (SPM). This measure paints a more accurate picture of economic hardship than the official federal poverty measure in part because it better accounts for the state’s high cost of living (see note below).

The new data show that California continues to have the highest poverty rate among the 50 states largely due to high housing costs. This fact underscores the need for California to do more to increase access to affordable housing in order to promote greater economic security in the state. The new Census data also tell a cautionary tale about the potential impact of policies being pursued by federal policymakers. President Trump and congressional leadership have proposed slashing critical supports that help families afford basic necessities like food and housing, and that lift millions of people above the poverty line each year. If signed into law, these proposals would undoubtedly drive California’s already unacceptably high poverty rate even higher. Given this fact, California’s congressional representatives should reject steep cuts to vital public supports and instead prioritize policies that increase people’s economic security and opportunity.

California’s High Housing Costs Drive Up the State’s Poverty Rate

With 20.4 percent of state residents struggling to get by, California ranks first among the 50 states based on the SPM.[1] California’s No. 1 ranking largely reflects the state’s high housing costs. Unlike the official poverty measure, the SPM accounts for differences in housing costs across the US, and when these costs are factored in, a much larger share of the state’s population is living in poverty: 20.4 percent under the SPM, compared to 14.5 percent under the official measure. In fact, California’s poverty rate rises to the highest among the 50 states under the SPM, up from 16th highest under the official poverty measure.[2]

Housing costs are extremely high in many parts of California. Fair market rent for a modest two-bedroom apartment is more than $1,500 per month in the areas where nearly two-thirds of Californians live. At the same time, monthly rent affordable to a full-time worker at the state minimum wage is only $546 per month, which is less than the fair market two-bedroom rent anywhere in California. Thus there is no part of the state where a single mother with a minimum-wage job can expect to afford an apartment with a bedroom for herself and for her children.

Housing affordability is a problem throughout California, even in areas where housing costs are lower, because incomes are also lower in these areas. Statewide, more than half of renter households pay more than 30 percent of their incomes toward housing, making them housing cost-burdened, and nearly a third of renter households are severely cost-burdened, paying more than half of their incomes toward housing.

Given the crisis of housing affordability throughout the state, it is important to pursue policies that can help slow down rising housing costs and facilitate production of more affordable housing. State policymakers are currently considering a package of bills that would take an important step toward addressing this problem by increasing the production of housing and streamlining the local review process for certain housing projects in places that have not met their “fair share” housing goals. These measures would represent important first steps in providing some relief to families struggling to afford housing, a challenge that California will need to continue working to address in coming years.

Federal Policy Proposals Threaten to Plunge More Californians Into Poverty

The fact that around 8 million Californians struggle to get by — several years after the national recession ended — highlights the need for policies that allow more people to share in our recent economic gains. Yet the policies being pursued by President Trump and congressional leadership would decimate critical public supports that help struggling families and individuals make ends meet, inflicting serious hardship on millions of people.

Indeed, some of the proposed cuts target supports that are proven tools for reducing poverty. For instance, the Supplemental Nutrition Assistance Program (SNAP) — CalFresh in California — lifted around 800,000 Californians, including about 400,000 children, above the poverty line each year, on average, between 2009 and 2012. In addition, the federal Earned Income Tax Credit (EITC) and child tax credit (CTC) lifted nearly 1.4 million Californians, including roughly 700,000 children, out of poverty. Moreover, these supports not only help families get by day to day, but also may provide longer-term benefits to children. Research shows, for example, that food assistance, working-family tax credits, and other supports that help families afford basic needs help children to do better in school and increase their earning power when they grow up.[3] Given these facts, federal policymakers should reject any proposal that would weaken these vital public supports.

* * *

Note About the Census Bureau Data Released Today

The state-level figures released today reflect average annual poverty rates during a three-year period, from 2014 to 2016. The SPM addresses a number of shortcomings of the official poverty measure. One is the fact that under the official measure, the income threshold for determining who lives in poverty is the same in all parts of the US. For example, a parent with two children was considered to be living in poverty in 2016 if their annual income was below about $19,300, regardless of whether they lived in a low-cost place like rural Mississippi or a high-cost place like San Francisco. The SPM better accounts for differences in the cost of living by adjusting the poverty threshold to reflect differences in the cost of housing throughout the US. For example, the SPM poverty line for a parent with two children living in a renter household in the San Francisco metropolitan area was about $29,500 in 2016 — considerably higher than the poverty line based on the official measure.

Another shortcoming of the official poverty measure is that it fails to factor in the broad array of resources that families use to pay for basic expenses. The official measure only counts cash income sources, such as earnings from work, Social Security payments, and cash assistance from welfare-to-work programs. It does not take into account noncash resources, such as food or housing assistance, and it fails to consider how tax benefits, such as the federal Earned Income Tax Credit (EITC), increase people’s economic well-being. The SPM improves on the official measure by including these resources. It also better accounts for the resources people actually have available to spend by subtracting from their incomes what is needed to pay for necessary expenses, including work-related expenses, such as child care; medical expenses, such as health insurance premiums and out-of-pocket costs; and state and federal income and payroll taxes.

After incorporating these improvements over the official poverty measure, the SPM produces a more realistic picture of poverty in California: the state’s SPM poverty rate was 1.4 times the official poverty rate between 2014 and 2016 (20.4 percent versus 14.5 percent, respectively).

Although the SPM provides a more accurate picture of economic hardship in California, it does not indicate how much people need to earn to achieve a basic standard of living. Measures of what it actually takes to make ends meet in California show that families need incomes several times higher than the official poverty line to afford basic necessities.

Endnotes

[1] Florida ranks second among the 50 states with 18.7 percent of state residents living in poverty based on the SPM between 2014 and 2016, followed by Louisiana where the poverty rate was 18.4 percent.

[2] In addition, the SPM poverty rate is higher than the official poverty rate for most major demographic groups in California. See Alissa Anderson, A Better Measure of Poverty Shows How Widespread Economic Hardship Is in California (California Budget & Policy Center: October 2016).

[3] See Arloc Sherman and Tazra Mitchell, Economic Security Programs Help Low-Income Children Succeed Over Long Term, Many Studies Find (Center on Budget and Policy Priorities: July 17, 2017).

You may also be interested in the following resources:

-

Fact Sheet

Young Californians Face Alarmingly High Rates of Poverty and Deep Poverty

key takeaway Young adults across California face higher-than-average poverty and deep poverty rates as they transition into adulthood, underscoring the need to strengthen core basic needs programs and investments that help young Californians achieve economic stability and meet their basic needs. Young adulthood is a crucial time to establish independence and start to build financial … ContinuedCalFreshMedi-CalPoverty & Inequality -

Report

Federal and State Budget Decisions Threaten AANHPI Women in California

key takeaway AANHPI women’s experiences vary widely across ethnicities, making disaggregated data essential to understanding the impacts of recent federal and state decisions. By examining the Women’s Well-Being Index indicators across multiple AANHPI ethnicities, this report highlights distinct challenges facing AANHPI women in California and identifies key steps state and local leaders can take to … ContinuedPoverty & Inequality

Stay in the know.

Join our email list!

A number of current proposals at the federal level, put forth by the Trump Administration and congressional leaders, call for deep spending cuts to many important public services and systems that improve the lives of individuals and families across California. These cuts are proposed at a time when both President Trump and leaders in the House of Representatives have signaled support for major tax cuts that would largely benefit the wealthy and large corporations.

Although federal spending deliberations occur far from California, their outcomes have deep potential impacts right here at home, in every part of our state. In order to shed light on the local importance of federal budget choices, as well as underscore what’s at stake in the votes cast by members of California’s congressional delegation, we are pleased to provide these House district Fact Sheets. They provide district-by-district figures on public services and supports across four areas — food and shelter, health care, income support, and education — along with local information on social and economic conditions.

Click below to get the Fact Sheet for your district. (Find your representative)

You may also be interested in the following resources:

-

Report

First Look: Understanding the Governor’s 2026-27 May Revision

Stronger-than-expected revenues do not solve all of the state’s challenges. The 2026–27 budget is Governor Newsom’s last opportunity to fully respond to the harmful federal cuts enacted through H.R. 1.California Budget -

Report

California’s Rainy Day Fund and Other Budget Reserves Overview

key takeaway California’s state budget reserves, including the “rainy day fund” and other reserve accounts, serve as a financial safety net for services like education, health care, and child care during economic downturns. The rules for depositing and withdrawing funds are complex, and policymakers should consider reforms, such as excluding reserve deposits from the Gann … ContinuedBudget AcademyCalifornia Budget

Stay in the know.

Join our email list!

California’s 2017-18 budget agreement included a major advance for working families who struggle to get by on low incomes. A “trailer bill” included in the budget package significantly expands eligibility for California’s Earned Income Tax Credit, the CalEITC — a refundable state tax credit that helps people who earn little from their jobs to pay for basic necessities.[1] Specifically, this bill 1) allows previously ineligible self-employed workers to qualify for the CalEITC and 2) raises the credit’s income eligibility limits so that workers higher up the income scale can qualify for it. These changes could extend the credit to well over 1 million additional low-income working families beginning in tax year 2017.[2] This represents a significant expansion of the CalEITC given that around half a million families might have been eligible for it prior to the expansion and that roughly 360,000 have annually claimed the credit since it was established in 2015.[3]

This report provides an in-depth look at what the expanded CalEITC means for low-earning Californians. It finds that the higher income limits will allow many more workers living in or near poverty, including single parents working full-time minimum wage jobs, to become eligible for the credit. However, these newly eligible workers will qualify for very modest credits — less than roughly $230 for those with children and under about $84 for those without children. Thus, while the budget agreement makes an important advance for working families by greatly expanding access to the CalEITC, state policymakers could further strengthen this critical tax credit by increasing the benefit these newly eligible workers can receive in future years.

More Low-Earning Self-Employed Workers Will Gain Access to the CalEITC

Prior to the expansion, the CalEITC was the only EITC in the nation that excluded many self-employed workers, such as small-business owners and independent contractors.[4] This exclusion undermined a fundamental purpose of the EITC: to encourage and reward work. The 2017-18 budget agreement ends this exclusion beginning in tax year 2017. As a result, all self-employed workers who meet all other requirements for the CalEITC will be able to benefit from the credit. This change better aligns California’s EITC with the federal EITC and ensures that the state credit incentivizes all types of paid work.

The Income Limits to Qualify for the CalEITC Will Increase Significantly

Prior to the expansion, many workers who struggled to get by were not eligible for the CalEITC because the income limits to qualify for the credit were extremely low. The budget agreement raises these limits in order to allow additional low-earning workers to qualify for the credit. For workers with qualifying children, the new income limit will be $22,300 beginning in tax year 2017 (Table 1). This is more than double the previous income limit for parents with one child and more than one-and-a-half times the previous limit for parents with two or more children. The budget agreement also more than doubles the income limit for workers without qualifying children, from about $6,700 in tax year 2016 to roughly $15,000 in tax year 2017.

Table 1

Higher Income Limit Means More Minimum Wage Workers Will Qualify for the CalEITC

The higher CalEITC income limits will allow more minimum wage workers to benefit from the credit. Prior to the expansion, many minimum wage workers earned too much to qualify for the credit, even though they earned too little to make ends meet given California’s high cost of living. For example, in tax year 2016, families with one child were not eligible for the CalEITC unless they earned less than about $10,000 a year, a salary that translates into working just 19 hours per week at the state minimum wage (Table 2).[5] Families with two or more children did not qualify for the credit unless they earned less than about $14,000 annually, equivalent to working 27 hours per week at the minimum wage. The CalEITC expansion will allow families to work up to 41 hours per week at the state minimum wage to benefit from the credit.[6] This means, for example, that the CalEITC will become available to single parents working full-time at the minimum wage (Figure 1).

Table 2

Figure 1

For workers without qualifying children, the new CalEITC income limit will increase to $15,010. Since this is less than a full-time minimum wage salary, the credit will not be available to full-time minimum wage workers without qualifying children. Nevertheless, this higher threshold means that these workers will be able to work up to 27 hours per week at the minimum wage and still qualify for the credit, up from just 13 hours per week to qualify previously.[7]

Higher CalEITC Income Limit Means More Working Families in Poverty Will Qualify for the CalEITC

Raising the income limits to qualify for the CalEITC will not only allow more minimum wage workers to benefit from the credit, but will also make the credit available to more workers living in or near poverty. Prior to the expansion, the CalEITC’s income limits fell well below the official federal poverty line. As a result, many workers living in poverty were not eligible for the credit. For example, single parents with one child had to earn less than about 62 percent of the poverty line to qualify for the credit. Beginning in tax year 2017, these parents can have incomes up to about 135 percent of the poverty line and still be eligible for the credit (Figure 2). Raising the income limits closer to or above the poverty line is important because many families with incomes this low struggle to afford basic expenses, particularly in high-cost areas of the state.

Figure 2

CalEITC Will “Phase Out” More Gradually, Allowing Workers Higher Up the Income Scale to Qualify

The size of the CalEITC for a particular family or individual depends on how much they earn and how many children they support. Specifically, the credit “phases in” (increases) for higher levels of earnings up to a certain maximum point, after which the credit “phases out” (decreases) for higher levels of earnings until it reaches $0. The budget agreement extends the CalEITC to workers higher up the income scale by phasing out the credit more slowly beginning at an income of $13,794 for workers with two qualifying children (Figure 3).[8] This is the income level at which these parents are estimated to qualify for a CalEITC of $250 in tax year 2017. For workers without qualifying children, the budget package phases out the CalEITC more gradually beginning at an income of $5,354 — the point at which these workers are estimated to qualify for a CalEITC of $100 in tax year 2017.

Figure 3

Most workers who previously qualified for the CalEITC will see no change in the size of the credit, while some will receive slightly larger credits. For example, there will be no change in the credit for parents with two qualifying children and earnings of up to $13,794 (Table 3). Those with incomes between $13,794 and $14,529 will qualify for slightly larger credits. For instance, a parent with two children and earnings of $14,000 will qualify for an estimated $244 from the CalEITC under the expansion, up from an estimated $180 if the credit had not been expanded. Workers with two children and incomes between $14,529 and about $22,300 will newly qualify for the CalEITC.

Table 3

Newly Eligible Workers Will Qualify for Very Modest Credits

Workers who become eligible for the CalEITC because of the higher income limits will qualify for very modest credits. Those with qualifying children will be eligible for roughly $230 or less, depending on their earnings. For example, a worker with two children could qualify for about $214 if she earns $15,000 or $126 if she earns $18,000 (Figure 4). Workers without qualifying children who become eligible for the CalEITC under the expansion will be able to receive about $84 or less, depending on their earnings. For instance, these workers would be eligible for about $84 if they earn $7,000 annually or $52 if they earn $10,000 annually.

Viewed another way, families working a total of 30 hours per week in 2017 at the state minimum wage (earning an annual salary of $16,380) will be eligible for an estimated $115 from the CalEITC if they have one qualifying child, $174 if they have two qualifying children, or $176 if they have three or more qualifying children (Table 4).[9] If the CalEITC had not been expanded in this year’s budget agreement, these workers would not have qualified for the credit at all.

Figure 4

Table 4

Conclusion

Creating the CalEITC was an important advance in how our state helps workers with low incomes to better afford basic necessities and move toward financial security. The 2017-18 budget agreement greatly strengthens this vital tax credit by extending it to well over 1 million additional low-income working families. Although many of the newly eligible workers will qualify for very modest credits, the budget deal lays the foundation for further strengthening the CalEITC, as state policymakers can build on these changes in coming years by increasing the size of the credit that newly eligible workers can receive.

Endnotes

[1] Senate Bill 106 (Committee on Budget and Fiscal Review, Chapter 96 of 2017).

[2] Institute on Taxation and Economic Policy (ITEP). ITEP’s estimate is subject to some uncertainty. This estimate is largely based on Internal Revenue Service (IRS) data on California tax filers who claim the federal EITC. However, only around 75 percent of Californians who are eligible for the federal EITC are estimated to actually claim the credit each year. This means that California’s federal EITC participation rate is implicitly assumed in ITEP’s estimate. In other words, this estimate may be understated to the extent that expanding the CalEITC encourages workers who qualify for the federal EITC, but who do not typically file their taxes, to file in order to benefit from the state credit. On the other hand, ITEP’s estimate could be overstated given that the CalEITC appears to be undersubscribed. ITEP estimates that 553,000 tax units could have claimed the CalEITC in 2016, but actual claims were around 360,000. This suggests that ITEP’s estimate of the number of families who could benefit from the expanded CalEITC could be too high if many workers who are eligible for the credit continue to miss out on it in coming years.

[3] It is not known exactly how many families are eligible for the CalEITC. Estimates prior to the expansion ranged from around 400,000 to 600,000. Soon after the credit was signed into law, the Franchise Tax Board estimated that roughly 600,000 families would likely be eligible for it. (Personal communication with the Franchise Tax Board on September 22, 2015.) Similarly, a Stanford University analysis of US Census Bureau data estimated that approximately 600,000 families would have been eligible for the CalEITC if it had been in place in tax year 2013. (Christopher Wimer, et al., Using Tax Policy to Address Economic Need: An Assessment of California’s New State EITC (The Stanford Center on Poverty and Inequality: December 2016).) A more recent Budget Center analysis of US Census Bureau data estimated that around 416,000 families might have been eligible for the credit in tax year 2015. Additionally, ITEP’s analysis of IRS data suggests that about 550,000 families were likely eligible in tax year 2016. (Personal communication with the Institute on Taxation and Economic Policy on May 6, 2016.)

[4] Prior to the expansion, families and individuals who had self-employment income in addition to “earned income” qualified for the CalEITC if their federal adjusted gross income (AGI) was below the income limit. (“Earned income” was defined as annual wages, salaries, tips, and other employee compensation subject to wage withholding pursuant to the state Unemployment Insurance Code. Federal AGI includes both earned income and self-employment income, as well as several other types of income.) For these tax filers, the size of the CalEITC was based on their “earned income” if their federal AGI was below the income level needed to qualify for the maximum CalEITC. In contrast, if their federal AGI was at or above this threshold, then the size of the CalEITC was based on either their “earned income” or their federal AGI, whichever resulted in a smaller credit. Prior to the expansion, self-employed workers who had no “earned income” were not eligible for the CalEITC. These workers will qualify for the CalEITC beginning in tax year 2017, as long as they meet all other requirements for the credit.

[5] Earnings refer to annual earnings for the entire family.

[6] This means that in a family with one working parent, that parent can work up to 41 hours per week and still qualify for the credit. Families with two married working parents who file joint tax returns could work a combined total of up to 41 hours per week at the minimum wage and still qualify for the credit.

[7] This means that single workers without qualifying children can work up to 27 hours per week at the minimum wage and still qualify for the credit, while married workers without qualifying children can work a combined total of up to 27 hours per week and still qualify for the credit. Most state EITCs base their credits on the same eligibility rules as the federal EITC, which means that all workers who qualify for the federal credit also qualify for the state credit. In contrast, prior to the expansion, the CalEITC was available to just a fraction of those who qualified for the federal EITC because the income limits to qualify for the state credit were extremely low. Beginning in tax year 2017, the new CalEITC income limit for workers without children will match the federal EITC threshold that applies to these workers (Table 1). As a result, all Californians without qualifying children who are eligible for the federal EITC will also be eligible for the CalEITC. The new CalEITC income limits for parents will also be closer to the federal EITC thresholds, which range from about $39,600 to about $48,300 for single parents, depending on the number of children they are supporting.

[8] For workers with three or more qualifying children, the credit begins to phase out more slowly at an income of $13,875 and for workers with one qualifying child, the credit begins to phase out more slowly at an income of $9,484. These income levels do not reflect the income levels specified in SB 106 due to errors in the bill. These income levels will be corrected in a subsequent bill later this fall. (Personal communication with the Department of Finance (DOF) on July 24, 2017.)

[9] Eligibility for the CalEITC is based on annual earnings for the tax filer (for unmarried workers) or the combined annual earnings of the tax filer and his or her spouse (for married couples filing taxes jointly). In other words, families will be eligible for an estimated CalEITC of $115 if they have one working parent who earns $16,380 or two married working parents who earn a combined total of $16,380.

You may also be interested in the following resources:

-

Fact Sheet

Young Californians Face Alarmingly High Rates of Poverty and Deep Poverty

key takeaway Young adults across California face higher-than-average poverty and deep poverty rates as they transition into adulthood, underscoring the need to strengthen core basic needs programs and investments that help young Californians achieve economic stability and meet their basic needs. Young adulthood is a crucial time to establish independence and start to build financial … ContinuedCalFreshMedi-CalPoverty & Inequality -

Report

Federal and State Budget Decisions Threaten AANHPI Women in California

key takeaway AANHPI women’s experiences vary widely across ethnicities, making disaggregated data essential to understanding the impacts of recent federal and state decisions. By examining the Women’s Well-Being Index indicators across multiple AANHPI ethnicities, this report highlights distinct challenges facing AANHPI women in California and identifies key steps state and local leaders can take to … ContinuedPoverty & Inequality

Stay in the know.

Join our email list!

The California Earned Income Tax Credit (CalEITC), established in 2015, is a refundable state tax credit that helps low-earning workers and their families make ends meet and build toward economic security.[1] Yet, fewer than 1 in 5 visitors to county human services offices who were likely eligible for this new tax credit had heard of it, according to a Budget Center survey.[2] (County office visitors were surveyed because many would likely be eligible for the CalEITC or know people who are eligible for it.) In addition, only half of respondents who were likely eligible for the CalEITC filed their taxes for tax year 2015. These findings suggest that California needs to do more to raise awareness of the credit in order to boost participation.[3] The survey also found that most people who were likely eligible for the CalEITC and did file their taxes paid a tax preparer even though they would have qualified for free tax assistance. This means that many people did not get the full benefit of the CalEITC because they paid tax preparation fees. This report recommends strategies to maximize the success of the CalEITC, including by supporting research to better assess CalEITC utilization gaps and determine which outreach strategies are most effective, bolstering efforts by community organizations and county offices to promote the credit, and expanding and promoting free tax preparation services.

What Is the CalEITC and How Does It Work?

The CalEITC is a refundable state tax credit, modeled after the federal EITC, that helps working families who earn very little to better afford the basics. (Refundable credits allow people whose credit is larger than the amount of income taxes they owe to get the difference in a tax refund. This means that people who do not owe state income taxes, but who do pay other taxes, like the sales tax, can benefit from the credit.)

People qualify for the CalEITC based largely on how much they earn and how many qualifying children they are supporting. Families with multiple children qualify for the credit for tax year 2016 if they have earnings that do not exceed $14,161, while those with just one child qualify if their earnings do not exceed $10,087. Individuals without qualifying children can benefit from the CalEITC if their earnings do not exceed $6,717.

The size of the credit people can receive from the CalEITC also depends on how much they earn and how many children they are supporting. Working families with three or more qualifying children can receive up to $2,706 for tax year 2016, those with two children can receive as much as $2,406, and those with one child can receive up to $1,452. Individuals who do not have qualifying children are eligible for a much smaller credit — a maximum of $217.

The CalEITC is designed to build on federal working-family tax credits. Families with three or more children who qualify for the maximum CalEITC, for example, can see their incomes rise by as much as 92 percent from the CalEITC, in combination with the federal EITC and federal child tax credit. In this way, the CalEITC may enhance the federal EITC’s well-documented benefits to children, families, and communities.

Very Few People Who Were Likely Eligible for the CalEITC Had Heard of the Credit

Promoting the CalEITC will be key to its success because this new tax credit targets workers who — due to their very low earnings — are not required to file state personal income taxes and may not realize that they can receive cash back if they do.[4] However, a Budget Center survey of visitors to county human services offices found that:

- Just 18 percent of those who were likely eligible for the CalEITC had heard of the credit (Figure 1).[5] Similarly, just 15 percent of all respondents had heard of the credit.

- Among all respondents, Latinos were far less likely to have heard of the CalEITC. Only 10 percent of Latinos surveyed had heard of the credit compared to 25 percent of white respondents.[6]

Only Half of People Who Were Likely Eligible for the CalEITC Filed Their Taxes

- Just half (50 percent) of people surveyed who were likely eligible for the CalEITC filed their taxes for tax year 2015 — the first year the credit was available (Figure 2).[7] In other words, a large number of workers may have missed out on hundreds or thousands of dollars in tax credits, not only from the CalEITC, but also from the federal EITC. (As noted earlier, many people who qualify for the CalEITC are not required to file state income taxes.)

- These are dollars that are clearly needed. The vast majority of respondents who were likely eligible for the CalEITC (80 percent) had faced at least one major hardship in the past year, such as not being able to afford enough food, falling behind on rent or on utility bills, or having to forego necessary health care due to a lack of money.

The Majority of Tax Filers Who Were Likely Eligible for the CalEITC Paid a Tax Preparer

- Seven in 10 people surveyed who were likely eligible for the CalEITC and filed their taxes in 2015 (70 percent) paid a tax preparer even though they would have qualified for free tax assistance given their extremely low incomes (Figure 3).[8] This suggests that many workers did not receive the full benefit of the CalEITC or other tax credits because some of their tax refund went to tax preparation fees.

- Although tax preparation fees are rarely transparent and can vary widely, studies suggest that they tend to range in the low hundreds of dollars. For example, the US Government Accountability Office found, in one metro area, fees ranging from $160 to $408 for a single mother with one child who qualified for the federal EITC in tax year 2013.[9] Also, a national survey of tax preparers found that the average fee charged for filing a federal and state tax return without any itemized deductions was $176 in 2016.[10] By comparison, heads of household with one child received an average CalEITC of $610 during the credit’s first year, according to state data.[11] This suggests that tax preparation fees could have substantially reduced the benefit of the CalEITC for many low-earning workers.

Few Tax Filers Who Were Likely Eligible for the CalEITC Knew That Free Tax Preparation Services Were Available

- Lack of awareness of free tax preparation services may help explain why many workers who were likely eligible for the CalEITC paid to file their taxes. Only 25 percent of tax filers surveyed who were likely eligible for this credit knew of a free tax preparation service in their community (Figure 4).[12]

- High use of paid tax preparers may also reflect insufficient access to free tax services. California has over 900 Volunteer Income Tax Assistance (VITA) sites, which provide free tax preparation services by volunteers who are trained and certified by the Internal Revenue Service (IRS).[13] However, nearly half of the ZIP codes with the highest percentages of households that are potentially eligible for the CalEITC have no VITA sites at all, according to United Ways of California.[14] In addition, many VITA sites lack the capacity to meet the need for free tax preparation.[15]

Only About 2 in 5 People Who Were Likely Eligible for the CalEITC Had Heard of the Federal EITC

- Just 42 percent of people surveyed who were likely eligible for the CalEITC had heard of the federal EITC, even though most of them likely qualified for it (Figure 5).[16] By contrast, awareness of the federal EITC among very-low-income parents nationwide ranges between 55 percent and 66 percent.[17]

- Latino respondents were far less likely to have heard of the federal EITC than were other survey respondents. This is similar to national surveys, which find lower rates of awareness among Latinos, and particularly those who completed surveys in Spanish.[18]

Policy Options for Maximizing the Success of the CalEITC

Findings from the Budget Center’s survey suggest that California needs to do more to raise awareness of the CalEITC and to connect tax filers to free tax preparation services so that they can get the full benefit of their tax refunds. Such efforts could also increase federal EITC claims, drawing additional federal dollars into the state that would both help working families make ends meet and boost California-based businesses and the state economy.[19] Specifically, state policymakers could:

- Use state data to more precisely assess CalEITC utilization gaps as well as evaluate the effectiveness of targeted outreach strategies. While the survey findings described in this report, together with other research, suggest that many eligible Californians may have missed out on the CalEITC in its first year, a precise participation rate is not known. This is because, as discussed earlier, the CalEITC targets workers who are not required to file state personal income taxes, which means that tax filer data alone cannot be used to determine how many people likely qualify for the credit.[20] California could better assess CalEITC utilization — overall and across demographic groups — by linking data across state agencies. For example, California could pursue a data-sharing effort similar to one undertaken by Virginia, which facilitated a collaboration between that state’s tax board and social services department to produce a more accurate picture of federal EITC participation among people receiving major public benefits.[21] Specifically, Virginia used a combination of state tax filer and social services data to estimate which public benefits participants were likely eligible for the EITC, and then determined how many of those participants actually filed their taxes and claimed the credit. This revealed that 34 percent of public benefits participants who were likely eligible for the EITC did not claim the credit in 2006, largely because those individuals did not file their taxes.[22] More importantly, these data allowed Virginia to target EITC outreach efforts specifically to this group of nonfilers and to measure the effectiveness of these efforts by tracking whether they boosted EITC participation over time.[23] A similar data-sharing effort in California — potentially linking the Medi-Cal Eligibility Data System (MEDS) to Employment Development Department (EDD) and Franchise Tax Board (FTB) data — could provide valuable information that would help better tailor CalEITC outreach strategies to groups who are less likely to claim the credit and to learn which strategies work best in boosting claims.[24]

- Increase support for community-based efforts to promote the CalEITC. The 2016-17 budget agreement included $2 million for grants to help communities expand their efforts to raise awareness of the CalEITC. However, the Governor’s proposed budget for 2017-18 (the state fiscal year that begins on July 1, 2017) does not include funding to maintain or expand these efforts. Given that awareness of the CalEITC appears to be low, state policymakers could continue, and potentially expand, this grant program so that community groups can maintain their promotional efforts year-round and build on the educational strategies that they have developed.[25] Indeed, efforts to raise awareness of the CalEITC need to be ongoing because the workers who qualify for the credit will likely change from year to year.[26] In addition, because little is known about which educational strategies are most effective, policymakers could require a more robust evaluation of the strategies supported by this grant program.[27]

- Provide support to expand promotional efforts at county human services offices. County offices are ideally positioned to promote the CalEITC because they serve families and individuals with low incomes, many of whom likely qualify for the new credit. Yet many counties lack the resources to undertake robust promotional efforts. California could allow counties to expand their efforts by establishing a state-funded competitive grant program in which counties could apply to participate. The funds provided through this program could support a range of activities to raise awareness of the CalEITC, the federal EITC, and free tax preparation services. For example, funds could:

- Support an EITC coordinator to facilitate efforts to raise awareness of the state and federal EITCs among county clients and connect them to free tax preparation services.

- Support peer-to-peer learning opportunities, where counties could share best practices and learn to replicate effective promotional strategies. For instance, some counties train CalWORKs participants to be Volunteer Income Tax Assistance (VITA) tax preparers as part of their welfare-to-work plans, either as volunteer work experience or as subsidized employment. These workers help to both expand the capacity of local VITA sites and promote tax credits and free tax services in their communities. Counties that have established such programs could provide technical assistance to other counties interested in developing similar programs.

- Help counties operate VITA sites at their offices to facilitate free tax preparation for their clients. For example, state funds could cover the costs of keeping county offices open outside of standard business hours in order to provide tax services. Alternatively, counties could partner with local VITA programs.

- Support the development and implementation of assisted self-filing workshops where clients learn how to set up free, online tax filing accounts and receive technical assistance with filing their taxes.[28] Such workshops could be easier to establish than VITA sites.[29] Moreover, they would provide a valuable service because many adults — particularly those with low incomes — lack the literacy skills needed to file their taxes on their own.[30]

- Finance text messaging services to notify clients about tax credits and free tax services.

- Cover outreach costs, such as printing flyers to be included in required mailers to clients.

- Strengthen and expand free tax preparation services. Workers with incomes low enough to qualify for the CalEITC struggle to pay for basic expenses and cannot afford to lose part of their tax refunds by paying tax preparers.[31] Although these workers qualify for free tax services, VITA programs that run sites lack the capacity to meet the need and increasing demand for free tax preparation.[32] State funds could help expand the number of VITA sites in high-need communities and enable existing sites to serve more clients.[33] State support could also help VITA programs promote their services and better compete with marketing by paid tax preparers.[34] In addition, state funds could help communities assist people with filing their taxes on their own.[35] Self-filing assistance could be easier for some communities to provide because it would not require as many highly trained and certified volunteers as VITA sites require.[36]

- Promote free tax filing services, particularly targeting “nonfilers” who could benefit from the CalEITC and federal EITC.[37] One of the key challenges to maximizing participation in the CalEITC is that this credit targets workers who are not required to file state income taxes, as discussed earlier. This means that the credit’s success largely depends on encouraging “nonfilers” to file. Two research projects underway at Stanford University are testing whether mailing postcards with information about free tax filing services increases the use of those services.[38] If these mailings appear to be effective, California could consider promoting free tax filing services through mailers, particularly targeting people who are likely eligible for the CalEITC and federal EITC, but who have not recently filed state income taxes.[39] In addition, California could consider expanding the existing requirement that employers notify workers of their potential eligibility for the CalEITC and federal EITC to include information about accessing free tax filing services.[40] Under current law, this notification is not required to include specific information about how workers can claim these credits.

Overview of the Budget Center’s Survey

The Budget Center surveyed 938 visitors to county human services offices in eight counties during the fall of 2016. The primary purpose of the survey was to determine whether the visitors had heard of the CalEITC, since many would likely be eligible for the credit or know people who are eligible for it.

Budget Center staff designed the survey in consultation with academic researchers and other experts, and whenever possible utilized questions from long-standing national surveys. Initial drafts of the survey were pilot-tested in the late summer of 2016, and several questions were revised based on this testing.

Thirteen counties volunteered for the survey and, of these, the Budget Center selected the following eight to participate: Contra Costa, Los Angeles, Merced, Orange, San Bernardino, Stanislaus, Tehama, and Yolo. These counties were chosen in order to include communities in most major regions of the state as well as ensure a mix of urban and rural locations.

Surveys were administered between August and November 2016 on days that the counties identified as likely to have a high volume of walk-in traffic. All people who visited the county offices on those days were asked to participate in the survey. (It was not possible for the counties to identify in advance which of their clients were most likely to be eligible for the CalEITC. Therefore, eligibility had to be estimated through the survey using respondents’ self-reported earnings and family characteristics.)

Participation in the survey was voluntary and, when feasible, respondents were given a $5 gift card for their time. Most surveys were completed online using computers in the county offices. In a few counties that could not accommodate an online survey, Budget Center staff and volunteers distributed paper surveys to county visitors. Respondents could choose to take the survey in either English or Spanish.

While the number of survey respondents is large, and large samples increase the reliability of the survey results, the survey was not designed to be representative of all county human services clients or of all people who are eligible for the CalEITC. Also, many of the analyses reported are based on small subsets of the respondents. For example, just over one-quarter of the respondents (266 out of 938) appeared to be eligible for the CalEITC.

Determining Whether Respondents Were Likely Eligible for the CalEITC

An estimated 28 percent of survey respondents were likely eligible for the CalEITC for tax year 2015. This determination was based on respondents’ estimated annual earnings from work and the number of children they were living with and financially supporting, which are two key factors that determine eligibility for the credit. Respondents who reported that they lived with their spouse and that someone else in the household worked in 2015 were assumed to not be eligible for the CalEITC in case their spouses had earnings that would have disqualified them for the credit.[41] In addition, a small number of respondents who reported hourly wages below the 2015 statewide minimum wage were assumed to not be eligible for the CalEITC in case these respondents were being paid under the table. (To qualify for the CalEITC, workers must have earnings subject to wage withholding.) The survey did not collect any information about the immigration status of respondents or their family members, and therefore it is not possible to determine whether some of those who otherwise appeared to be eligible for the CalEITC did not actually qualify for the credit. (To qualify for the CalEITC, all family members reported on the tax form must have valid Social Security numbers.) Also, in order to keep the survey short and simple, respondents were not asked to report how much of their earnings came from self-employment, and since self-employment earnings are not counted in determining eligibility for the CalEITC, it is possible that some respondents’ assumed eligibility status is incorrect.

Determining Whether Respondents Had Heard of State and Federal Tax Credits

The survey asked respondents whether they had heard of the federal EITC, child tax credit, CalEITC, and a fictitious tax credit, the Family Support Tax Credit (FSTC). The share of people who reported that they had heard of the CalEITC and the federal EITC excludes all of those who reported having heard of the FSTC. This fictitious credit was included on the survey in order to identify potential “false positive” responses. (Respondents may report having heard of a credit when they actually had not because, for example, they believe that an affirmative answer is the response that researchers are looking for.)

Respondents were not asked whether they actually received the CalEITC or other tax credits. According to experts who have conducted similar surveys, such questions do not tend to provide accurate information because tax filers often do not know exactly which tax credits they received.

The survey also collected information regarding how people learned about the CalEITC. However, so few respondents had heard of the CalEITC that it was not possible to reliably report the most common ways that clients learned about the credit.

Characteristics of Respondents

Three-quarters of the survey respondents were women (75 percent) and the majority of all respondents were living with and financially supporting children (76 percent). The majority of respondents had worked in 2015 (58 percent), and these respondents had median annual earnings of $13,173.[42] Four in 10 of the respondents (40 percent) were the only workers in their household, and another 19 percent reported that they and others in their household worked.[43] Nearly half of the respondents (47 percent) were Latino, close to one-quarter (23 percent) were white, and 11 percent were black. The remaining 19 percent were of another race or ethnicity or reported multiple races or ethnicities. Respondents’ ages ranged from 17 to 80, with an average age of 35.

[1] This new credit is modeled after the federal EITC, which has provided extensive benefits to families, children, and communities, according to decades of research. For a summary of this research, see Alissa Anderson, State Earned Income Tax Credits (EITCs) Build on the Well-Documented Success of the Federal EITC (California Budget and Policy Center: March 9, 2017).

[2] The Budget Center surveyed 938 people who visited county human services offices in eight counties during the fall of 2016 to gauge awareness of the CalEITC. Of these individuals, just over one-quarter (266) appeared to be eligible for the CalEITC based on their estimated annual earnings from work as well as the number of children they were living with and financially supporting (see survey methodology for more information). Most people who participated in the survey reported that they visited the county office to apply for or renew benefits or to access employment services. The vast majority of respondents reported that they and/or their spouse and/or children currently participate in a major public program, such as Medi-Cal, CalFresh, or CalWORKs.

[3] CalEITC claims also suggest that many people who were eligible for the credit did not claim it. About 385,000 tax filers benefited from the CalEITC for tax year 2015. It is not possible to determine a precise participation rate because it is not known how many “tax units” (families) are eligible for the credit. In 2015, the Franchise Tax Board estimated that around 600,000 families would be eligible. (Personal communication with the Franchise Tax Board on September 22, 2015.) Similarly, a Stanford University analysis of US Census Bureau data also estimated that roughly 600,000 families would be eligible. (Christopher Wimer, et al., Using Tax Policy to Address Economic Need: An Assessment of California’s New State EITC (The Stanford Center on Poverty and Inequality: December 2016).) However, other estimates suggest that only about 466,000 families would be eligible. (Personal communication with the Institute on Taxation and Economic Policy on May 6, 2016.) This suggests that between 64 percent and 83 percent of those who were eligible for the CalEITC claimed it in tax year 2015. By comparison, around 75 percent of California families that are eligible for the federal EITC are estimated to claim it each year. However, EITC eligibility estimates have limitations. For more information, see Alan Berube, Earned Income Credit Participation: What We (Don’t) Know (Brookings Institution: February 15, 2005) and Dean Plueger, Earned Income Tax Credit Participation Rate for Tax Year 2005 (Internal Revenue Service: no date).

[4] It is likely that the majority of people who are eligible for the CalEITC are not required to file state personal income taxes. Personal communication with the Franchise Tax Board on April 7, 2017.

[5] Just over one-quarter of the people surveyed were likely eligible for the CalEITC. See survey methodology for more information.

[6] Since few respondents who were likely eligible for the CalEITC had heard of the credit, it is not possible to reliably report demographic information for this group. Therefore, these figures refer to the share of all people surveyed who had heard of the CalEITC, regardless of whether they were likely eligible for the credit. In this report, white respondents and Latino respondents are mutually exclusive groups and refer to people who said that they identify with only one race or ethnicity. Data for other race and ethnic groups could not be reported individually due to the small number of respondents in each of those groups.

[7] For simplicity, the survey asked, “Did you or your spouse file income taxes this year?” without asking respondents to specify the tax year, or whether they filed state or federal income taxes or both.

[8] By comparison, 65 percent of Californians who claimed the federal EITC paid a tax preparer in tax year 2014, according to Internal Revenue Service data compiled by the Brookings Institution. Brookings Institution, Earned Income Tax Credit (EITC) Interactive and Resources (December 21, 2016).

[9] US Government Accountability Office, Paid Tax Return Preparers: In a Limited Study, Preparers Made Significant Errors, testimony presented to the US Senate Committee on Finance (April 2014).

[10] National Society of Accountants, 2016-2017 Income & Fees of Accountants and Tax Preparers in Public Practice Survey Report (no date). Some tax preparers charge tax filers per form, which means that fees would be higher for people who claim credits like the federal EITC and CalEITC because claiming these credits requires additional paperwork.

[11] Personal communication with the Franchise Tax Board on November 15, 2016.

[12] Surprisingly, awareness of free tax preparation services did not always translate into use of those services. More than one-third of all tax filers surveyed who knew of a free tax preparation service in their community (37 percent) paid a tax preparer when they filed for tax year 2015.

[13] VITA sites offer free tax assistance to people who generally make $54,000 or less annually. Only 2.3 percent of California tax filers who claimed the federal EITC filed their taxes at a free tax preparation site such as VITA in 2014. Brookings Institution, Earned Income Tax Credit (EITC) Interactive and Resources (December 21, 2016).

[14] Personal communication with United Ways of California on March 8, 2017.

[15] For example, United Ways of California, which supports member United Ways that operate many VITA sites, reports that the majority of California VITA sites offer services for limited hours during the week, many lack enough volunteers to meet the demand for services, and that few sites have full-time, paid coordinators who can help the sites run more efficiently. In addition, some sites report that appointments often fill up quickly, limiting their ability to accept additional clients. Personal communication with United Ways of California on March 22, 2017 and April 5, 2017.

[16] A slightly smaller share of all people surveyed (37 percent) had heard of the federal EITC.

[17] Percentages refer to parents with incomes below half of the official federal poverty line (FPL) and those with incomes between 50 percent and 100 percent of the FPL, respectively. See Katherine Ross Phillips, Who Knows About the Earned Income Tax Credit? (The Urban Institute: January 2001), Table 1. Another national survey found that around 58 percent of low-income parents had heard of the federal EITC. See Elaine Maag, Disparities in Knowledge of the EITC (Urban Institute and Brookings Institution Tax Policy Center: March 14, 2005).

[18] Katherine Ross Phillips, Who Knows About the Earned Income Tax Credit? (The Urban Institute: January 2001).

[19] Estimates suggest that roughly 1 in 4 eligible California families or individuals do not claim the federal EITC each year, depriving California of more than $1 billion in federal funds annually. See Internal Revenue Service, EITC Participation Rate by States, downloaded from https://www.eitc.irs.gov/EITC-Central/Participation-Rate on March 1, 2017 and Antonio Avalos, The Costs of Unclaimed Earned Income Tax Credits to California’s Economy: Update of the “Left on the Table” Report (Commissioned by the California Department of Community Services and Development: March 2015). Studies suggest that workers who are eligible for, but do not claim, the federal EITC tend to have lower incomes than eligible workers who do claim this credit. Since the CalEITC is available only to workers with extremely low incomes, this group likely includes people who are missing out on the federal EITC. In other words, promoting the CalEITC provides an ideal opportunity to raise awareness of the federal EITC.

[20] See endnote 3.

[21] See Erik Beecroft, EITC Take-Up by Recipients of Public Assistance in Virginia, and Results of a Low-Cost Experiment to Increase EITC Claims (Virginia Department of Social Services: May 2012) and Erik Beecroft, To What Extent Do VDSS Clients Claim the Federal Earned Income Credit? (Virginia Department of Social Services: January 31, 2008).

[22] Indeed, national estimates suggest that almost two-thirds of people who were likely eligible for the federal EITC, but who did not claim it, did not file federal income taxes, underscoring the need to target outreach strategies to “nonfilers.” Dean Plueger, Earned Income Tax Credit Participation Rate for Tax Year 2005 (Internal Revenue Service: no date), Table 8.

[23] Specifically, Virginia’s social services department conducted a “random assignment” study to test whether mailers and automated phone calls boosted EITC claims. Researchers, sometimes in collaboration with the Internal Revenue Service, have conducted similar studies to evaluate EITC outreach efforts nationwide. See, for example, work by Day Manoli at http://www.daymanoli.com/researchpapers/ .

[24] Specifically, California could explore the possibility of linking MEDS, a database of people participating in major public programs, to wage withholding data from the EDD in order to identify public benefits recipients who are potentially eligible for the CalEITC based on their earnings from work. This information could then be shared with the FTB to determine which of these individuals did not file state income taxes in the prior year. These “nonfilers” who are potentially eligible for the CalEITC could then be targeted for direct outreach on the credit, and the effectiveness of this outreach could be evaluated by tracking whether these individuals eventually filed their state taxes and claimed the CalEITC. See endnotes 38 and 40 for information about researchers who have conducted, or are currently conducting, such evaluations.

[25] Currently, these grants support CalEITC promotional efforts for a limited time, from November 2016 through May 2017. For more information about this grant program, see Department of Community Services and Development, Notice of Funding Availability (NOFA) California Earned Income Tax Credit Education and Outreach Grant: 2016 Cal EITC NOFA (August 15, 2016).

[26] Research shows that many people at the low-end of the income scale experience large swings in their incomes from year to year. See, for example, Andrew Stettner, Michael Cassidy, and George Wentworth, A New Safety Net for an Era of Unstable Earnings (The Century Foundation: December 15, 2016). In addition, studies find that a sizeable share of the US population falls into poverty for short periods of time. See Bernadette D. Proctor, Jessica L. Semega, and Melissa A. Kollar, Income and Poverty in the United States: 2015 (US Census Bureau: September 2016), p. 3 and Robin J. Anderson, Dynamics of Economic Well-Being: Poverty, 2004-2006 (US Census Bureau: March 2011).

[27] The Legislature could direct the Department of Community Services and Development, which administers the current grant program, to contract with an independent, research-based institution with expertise in program evaluation. The Legislature has required such evaluations in the past. See, for example, SB 1041 (Committee on Budget and Fiscal Review, Chapter 47 of 2012), which required the Department of Social Services to contract with a research organization to evaluate changes in the California Work Opportunity and Responsibility to Kids (CalWORKs) program.

[28] There are many free online filing programs that could be used in these workshops, including: MyFreeTaxes.org, which is operated by United Ways of California; Free File (freefilealliance.org), a nonprofit coalition of tax software companies in partnership with the IRS; and CalFile (https://www.ftb.ca.gov/online/calfile/), a free, online filing program operated by the Franchise Tax Board that allows tax filers to automatically import information from their W-2 forms, which summarize workers’ annual wages and the amount of taxes withheld from their paychecks.

[29] Self-filing workshops would not require as many volunteers as VITA sites require, and the volunteers would not necessarily need to be as highly trained. VITA sites typically provide one-on-one tax preparation services by volunteers who must be certified by the IRS after completion of a tax-training course and passage of an exam.

[30] Research suggests that “a substantial majority of [federal] EITC filers have such limited literacy as to seriously compromise their capacity to prepare their own tax return.” See Michael I. O’Conner, Tax Preparation Services for Lower-Income Filers: A Glass Half Full, or Half Empty? (Tax Notes: January 8, 2001), p. 8. An estimated 40 million to 80 million Americans lack the skills necessary to fill out IRS forms. Edward E. Gordon and Elaine H. Gordon, Literacy in America cited in Joseph Bankman, Simple Filing for Average Citizens: The California ReadyReturn (State Tax Notes: June 13, 2005). Also, more than one-quarter of adults living in households with annual incomes below $10,000 lack basic literacy skills. Mark Kutner, et al., Literacy in Everyday Life: Results From the 2003 National Assessment of Adult Literacy (US Department of Education: April 2007), p. 32.

[31] The majority of Californians who claim the federal EITC pay to have their taxes prepared in spite of their modest incomes (see endnote 8), and many people who claimed the CalEITC in 2015 also appear to have paid to file.

[32] VITA sites offer free tax assistance to people who generally make $54,000 or less annually. According to United Ways of California, the majority of California VITA sites offer services for limited hours during the week, many sites lack enough volunteers to meet the demand for services, and few have full-time, paid coordinators who can help them run more efficiently. Also, as noted earlier, many communities where large shares of households are likely eligible for the CalEITC lack VITA sites altogether.

[33] State support could allow VITA sites to hire a full-time coordinator, train additional volunteers, and expand their hours of service. Iowa and Virginia have provided state funds to support EITC outreach and expand free tax preparation services. For more information, see National Conference of State Legislatures, Tax Credits for Working Families: Earned Income Tax Credit (EITC) (February 21, 2017).

[34] Tax preparation fees are rarely transparent, as discussed earlier. Therefore, it would also be useful for California to require tax preparers that charge for their services to specify their fees before tax filers begin the process of preparing their taxes. For example, preparers could be required to display their fees for each tax form and service they provide. See Chi Chi Wu, It’s a Wild World: Consumers at Risk From Tax-Time Financial Products and Unregulated Preparers (National Consumer Law Center: February 2014), pp. 18-19.

[35] These services could be provided at various community locations, such as schools, libraries, food banks, and one-stop centers, which offer employment-related services to people who are searching for work.

[36] VITA sites typically provide one-on-one tax preparation by volunteers who must complete a tax-training course, pass an exam, and be certified by the IRS. Communities that have difficulty establishing or expanding these services could consider establishing self-filing assistance programs, in which volunteers help clients file their taxes on their own using free, online tax filing software. Some VITA sites provide such self-filing services, called Facilitated Self-Assistance (FSA), in order to expand their capacity without having to recruit additional IRS-certified volunteers. See Shervan Sebastian, Ezra Levin, and David Newville, Strengthening VITA to Boost Financial Security at Tax Time & Beyond (CFED: June 2016) and Rebecca Thompson, Learn More About Facilitated Self Assistance for Your Clients! (CFED: February 22, 2017).

[37] Free tax filing programs are underutilized, suggesting a need to better promote these services. For example, less than 2 percent of the nation’s tax returns in 2016 were filed through Free File (freefilealliance.org), a nonprofit coalition of tax software companies in partnership with the IRS, even though this service is available to 70 percent of tax filers. See Jessica Huseman, “Filing Taxes Could Be Free and Simple. But H&R Block and Intuit Are Still Lobbying Against It,” ProPublica (March 20, 2017).

[38] These two projects are being conducted by Jacob Goldin, an assistant professor of law at Stanford University. The first study, which is being conducted in Colorado in collaboration with the Colorado United Way Network, is testing the effect of sending postcards promoting United Way’s free, online tax service, MyFreeTaxes, to a random sample of households in low-income neighborhoods. The second study, which is being conducted in collaboration with the US Treasury Department and the IRS, is testing the effect of sending postcards promoting various types of free tax preparation services to people who are likely to qualify for these services and who prepared their own tax returns in the prior year. The preliminary results of this research should be available in the late spring or early summer of 2017.