In a state as wealthy as ours, no one should have to live in poverty

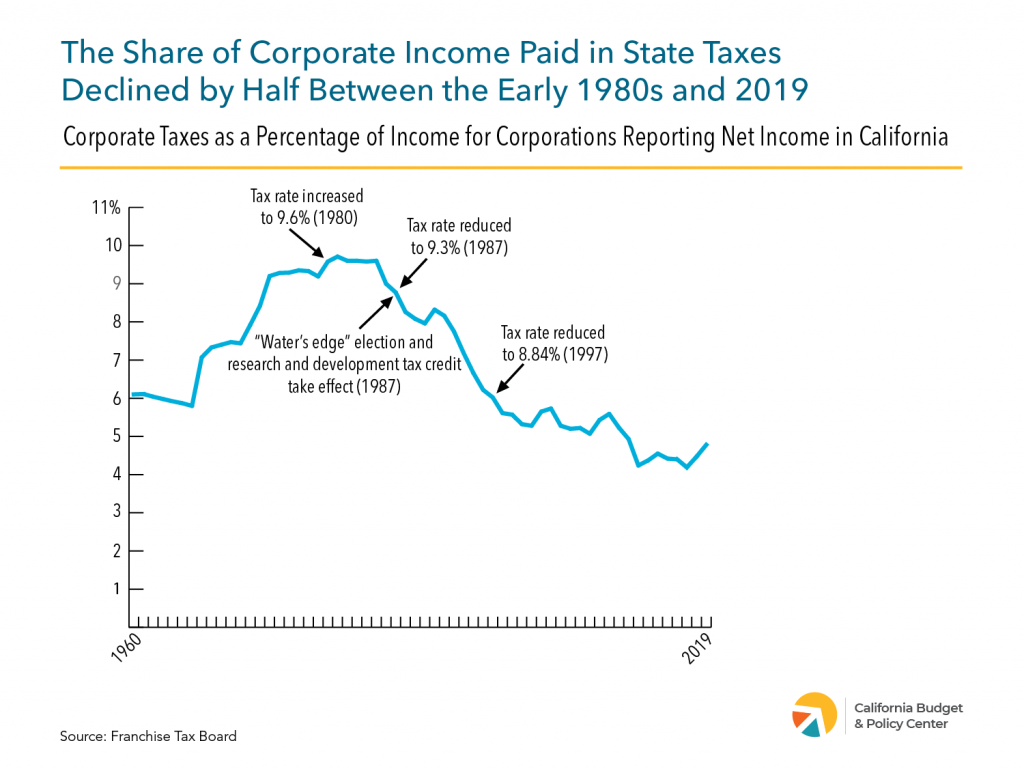

Corporations are contributing roughly half as much of their California profits in state taxes than four decades ago. In the early 1980s, corporations paid more than 9.5% of their profits in state corporation taxes. In contrast, corporations paid just 4.9% of their California profits in corporation taxes in 2020.

Corporations pay less of their income in taxes today than the 1980s in part due to tax rate reductions by state policymakers. Policymakers have also enacted several tax breaks that reduce the share of corporate income paid in California corporation taxes, such as the research and development tax credit.

California’s budget would have received $14.5 billion more revenue in 2020 had corporations paid the same share of their income in taxes that year as they did in 1981 – more than the state spends on the University of California, the California State University, and student aid combined.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Every Californian deserves to feel secure in their ability to keep a roof over their head, put food on the table, have transportation to get to their jobs, school, and other activities, and meet their basic needs. But even as California’s economy has recovered the jobs lost due to the COVID-19 recession, California workers, families, and individuals have been hit with another challenge in the rising costs of goods and services — including but not limited to gas prices. At the same time, corporations have been reaping record profits.

Governor Newsom proposed a “windfall tax” or “price gouging penalty” in fall 2022 to capture a share of the extraordinary recent profits of oil companies operating in the state and return it to Californians impacted by high gas prices. The governor has said that he will call a special session of the Legislature to take up this proposal. This Q&A discusses the concept of a windfall profits tax, why Governor Newsom is calling for such a tax on oil companies, and how it could impact Californians.

In general, a “windfall profits tax” or “excess profits tax” is intended to tax the portion of a corporation’s profits that exceed some specified “normal” level. Excess profits might represent advantages a corporation has due to market concentration and lack of competition or due to an external event like a war, natural disaster, or a pandemic — or a combination of these factors.

For example, during WWI, WWII, and the Korean War, the US put in place excess profits taxes that were intended to discourage some corporations, such as weapons manufacturers, from receiving outsized benefits due to war.

In the 1980s, the US instituted a “Crude Oil Windfall Profits Tax,” but it was not a true tax on excess profits. Instead, it was an excise tax on domestic oil production applied to the difference between the market price of a barrel of oil and a base price.

There have also been proposals by some academics, advocacy groups, and federal policymakers for windfall profits taxes on corporations that have seen record profits during COVID-19 while many Americans have suffered the health and economic consequences of the pandemic.

What is the difference between a windfall profits tax and a corporate income tax?

There are several ways to structure a windfall profits tax. But the main difference between a windfall profits tax and a corporate income tax is:

A regular corporate income tax takes a percentage of a corporation’s total profits (revenues minus costs and other deductions allowed for tax purposes).

A windfall or excess profits tax is designed to get at those profits above a normal rate of return on investment or above the average profits during a baseline period.

And while a corporate income tax is levied on corporations’ profits every year, a windfall profits tax is generally a temporary tax in place for a specified period of time such as during a war or a period of high oil prices.

However, an excess profits tax could be implemented on a permanent basis if designed to tax profits above a specific rate of return or profit margin. In this case, the intent would be to capture some of the extraordinary profit a business receives by virtue of having a high degree of market power, control of some natural resource, or some other advantage, rather than just capturing the windfall profits received due to some external event like a war, pandemic, or natural disaster. In fact, a permanent tax may be a more effective policy since it is less likely to discourage investment as it is more stable and predictable.

Why is Governor Newsom proposing a windfall profits tax now?

Governor Newsom has drawn attention to the fact that oil companies have seen record profits recently while many Californians are struggling with high gas prices. He has suggested that oil companies are using their market power to price-gouge Californians. To the extent that this is true, it may be sensible for policymakers to recapture some of the undue profits oil companies have made and return them to Californians.

If policymakers do enact a windfall profits tax, California would likely be the first state to do so. However, some European countries have recently enacted various versions of temporary windfall taxes targeted at energy companies in response to rising prices in that sector.

Should California policymakers adopt a windfall profits tax on oil companies?

However, if policymakers choose to move forward with this proposal, they should be prudent when designing it to minimize unintended consequences that could harm Californians, such as reductions in supply leading to even higher prices. The “Crude Oil Windfall Profits Tax” that was in place in the US from 1980 to 1988 — which was actually a tax based on the price of a barrel of oil instead of oil company profits — was not very successful, raising significantly less revenue than projected and contributing to a reduction in domestic oil production and an increased reliance on foreign imports.

Policymakers have many options for ensuring that corporations making excessive profits — including but not limited to oil companies — are paying their fair share in state taxes. Since the early 1980s, theshare of corporations’ California income that they pay in state taxes has fallen by about half. This significant drop is a result of factors including reductions in the official corporate tax rate in the 1980s and 1990s as well as the enactment of multiple corporate tax breaks which disproportionately advantage large and multinational corporations, have uncertain economic effects, and cost the state billions in revenues each year.

Policymakers can eliminate or limit some of these costly tax breaks and increase the corporate income tax rate on the most profitable corporations. State leaders could also explore adopting a permanent tax on oil and gas extraction — known as a “severance tax” — as many other states already have. The additional revenue raised from these measures could then be used to help ensure all Californians can thrive in their communities.

How should California use the revenues from a windfall profits tax or other corporate tax increases?

Californians have been hit by rising costs of almost everything this year — from gas to groceries to rent and more. These price increases are especially harmful to Californians with low incomes, who struggle to afford the basics even in times when inflation is low. About 2 in 3 California households with incomes below $35,000 reported having trouble paying for their usual expenses in September and October 2022, as did nearly half of those with incomes between $35,000 and $75,000.

People with low incomes are hit hardest by inflation because they need to spend larger shares of their income to meet their basic needs like food, housing, and transportation, which have been subject to large increases. They also have less ability to change their spending patterns to reduce the impact of inflation on their budgets, such as by switching to lower-cost versions of products, since they are likely already purchasing the lowest-cost versions. Black and Latinx households may also be disproportionately harmed by inflation as they are more likely to be renters than homeowners and rental inflation is generally higher than overall inflation.

Policymakers should keep these facts in mind when deciding how to distribute the revenue from a windfall tax — which likely would be much smaller than recent rounds of tax rebates for Californians — or other strategies to improve the taxation of profitable corporations. Additionally, as state leaders work to craft the state’s 2023-24 budget, they should avoid giving away tax breaks to corporations and prioritize the pressing needs of Californians who are struggling the most with the costs of living, such as by protecting and strengthening cash assistance and other supports to help families with the costs of child care, health care, and housing.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Calling California home means sharing in the responsibility of creating strong communities. Yet, corporations are contributing roughly half as much of their California profits in state taxes than four decades ago. In the early 1980s, corporations that reported profits in California paid more than 9.5% of this income in state corporation taxes. In contrast, corporations paid just 4.8% of their California profits in corporation taxes in 2019, the most recent year data are available. California’s budget would have received $14 billion more revenue in 2019 had corporations paid the same share of their income in taxes that year as they did in 1981 — more than the state spends on the University of California, the California State University, and student aid combined.

Corporations pay less of their income in taxes today than the 1980s in part due to tax rate reductions by state policymakers. The Legislature has cut the corporate tax rate twice: from 9.6% to 9.3% in 1987 and from 9.3% to 8.84%, its current level, in 1997.

In addition to cutting tax rates, state policymakers have enacted several tax breaks that reduce the share of corporate income paid in California corporation taxes. In the 1980s, policymakers established the “water’s edge” election and the research and development (R&D) tax credit — the state’s two largest corporate tax breaks that account for $6.1 billion of the $7.8 billion the state is projected to spend on corporate tax expenditures in 2021-22.

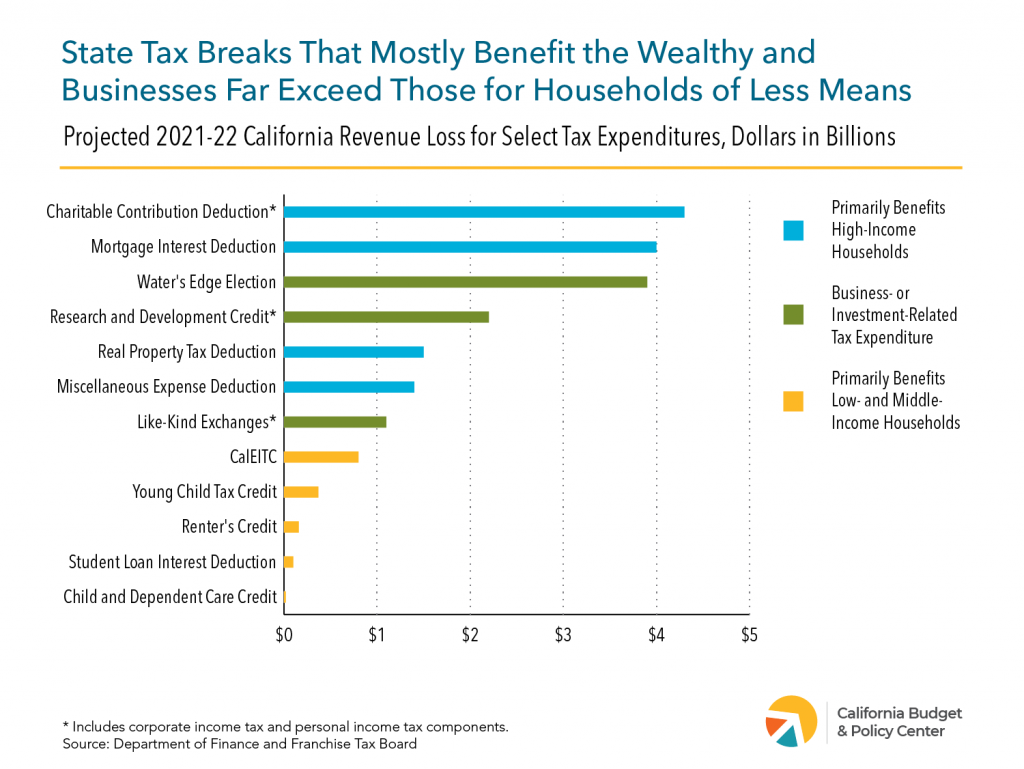

California’s tax break spending for corporations far exceeds tax benefits for Californians with low incomes. In tax year 2020, California spent $1.3 billion on the state’s two largest tax credits targeted to Californians with low incomes — the California Earned Income Tax Credit (CalEITC) and the Young Child Tax Credit (YCTC).1Reflects credits from tax returns processed by the Franchise Tax Board through November 27, 2021. The CalEITC and YCTC benefited 6.6 million Californians in tax year 2020 by boosting the incomes of those with annual earnings of less than $30,000, a large majority of whom are people of color.2The 6.6 million Californians figure reflects the total number of tax filers, spouses, and dependents in 4.2 million “tax units.” Yet, most people get less than $200 from the CalEITC, far too little to help people earning low wages and living in poverty. Policymakers can make tax credits more equitable by providing a larger minimum CalEITC for eligible workers and pay for it by eliminating or reducing tax breaks for corporations that can afford to contribute more to support California communities.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

California will lose an estimated $69.2 billion in state General Fund revenues in 2021-22 to personal and corporate income tax breaks — or “tax expenditures.”1Department of Finance, Tax Expenditure Report 2021-22, 5, https://www.dof.ca.gov/Forecasting/Economics/Tax_Expenditure_ Reports/documents/2021-22%20Tax%20Expenditure%20Report.pdf. Many of the state’s largest tax breaks primarily benefit higher-income households and businesses, while just a fraction of the state’s tax breaks are targeted to Californians with low and middle incomes.2For a more detailed examination of California’s tax expenditures, see Kayla Kitson, Tax Breaks: California’s $60 Billion Loss (California Budget & Policy Center, January 2020), https://calbudgetcenter.org/resources/tax-breaks-californias-60-billion-loss/.This revenue loss equals approximately one-third of the state’s 2021-22 General Fund budget and represents dollars the state could otherwise use to support Californians to live, work, and thrive across the state.

The state will forgo more than $18 billion in revenue due to just four itemized deductions that mostly benefit higher-income households and three tax incentives for businesses and investors. In comparison, California will spend less than $1.5 billion on tax breaks that primarily benefit low- and middle-income households, including the California Earned Income Tax Credit (CalEITC), the Young Child Tax Credit, the Renter’s Credit, the Student Loan Interest Deduction, and the Child and Dependent Care Credit.

Some of California’s tax expenditures also widen racial income and wealth disparities. Since Black and Latinx households are underrepresented in higher-income groups due to legacies of racist policies and ongoing discrimination, these households benefit less than white households from tax breaks skewed toward richer households. Additionally, many tax breaks reward wealth-building activities such as homeownership and retirement savings, to which households of color have less access.

When policymakers choose to spend public dollars via tax expenditures that largely benefit wealthy Californians and businesses, they are also choosing not to spend those dollars to help individuals and families who struggle with the costs of housing, child care, education, and other necessities. Eliminating or scaling back these tax expenditures would free up revenue that could be used to invest in resources that broaden economic security and create wealth and opportunity for more Californians.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Introduction

Californians need quality public health and schools, access to affordable housing and clean water, and safe roads and neighborhoods along with many more services to live and thrive – no matter one’s zip code. Accordingly, the state’s tax and revenue system must raise adequate revenue to cover the services provided by state and local governments and make ongoing investments to meet the needs of Californians. However, policy choices of the past and present shape whether revenues are equitably raised and who is contributing a fair share of their income to California’s revenue. State policymakers can make the tax and revenue system more equitable by strengthening taxation of Californians with high incomes and wealth while providing more support to Californians with low incomes and Californians of color who have been blocked from income- and wealth-building opportunities.

This 5 Facts explains main concepts associated with tax equity and illustrates how elements of California’s tax and revenue system further or impede the goals of economic and racial equity for households, communities, and the state.

1. Taxes Can Be Progressive, Proportional, or Regressive — Depending on How They Impact People Across Income Levels

A key aspect to tax equity is how a tax — or a tax system as a whole — impacts households across income levels. One way to measure this is by comparing effective tax rates —meaning the share of one’s income paid in a tax — of people in different income groups. A tax is considered progressive when households with higher incomes have higher effective tax rates than those with lower incomes. The opposite of a progressive tax is a regressive tax. With regressive taxes, people with lower incomes have higher effective tax rates than people with higher incomes. Finally, a tax is considered proportional when people at all income levels have the same effective rates. Progressive taxes are the most equitable taxes, since they ask the most from people who have the most ability to pay.

People with lower incomes must spend larger shares of their income just to meet their basic needs, leaving them with less ability to pay taxes. For example, almost 6 in 10 low-income California households spend more than half of their income on housing alone, compared to just 2% of high-income California households.1Aureo Mesquita and Sara Kimberlin, Staying Home During California’s Housing Affordability Crisis (California Budget & Policy Center, July 2020), https://calbudgetcenter.org/resources/staying-home-during-californias-housing-affordability-crisis/. Data are for 2018. “Low-income California household” is defined as a household with income below 200% of the federal poverty threshold — roughly $51,000 for a family of four in 2018 — and “high-income California household” is defined as a household with income of at least four times the federal poverty threshold — roughly $102,000 for a family of four in 2018. In other words, after covering the basics, Californians with lower incomes have much smaller portions of their total incomes available to pay taxes than higher-income Californians. It follows that a fair tax system should take a smaller fraction of the income of low-income households.

2. California’s Personal Income Tax Is Highly Progressive, Asking the Most from Those with the Highest Ability to Pay

Californians with higher incomes pay a larger percentage of their income in personal income taxes than people with lower incomes because higher portions of income are subject to higher tax rates.2California’s personal income tax rates range from 1% to 13.3%. The top rate for each tax bracket, or range of income, is only applied to the amount of income that exceeds the income threshold for that bracket. In other words, high-income people face the highest effective tax rates with regard to the personal income tax. Additionally, the state has two refundable tax credits, the California Earned Income Tax Credit (CalEITC) and the Young Child Tax Credit, that provide refunds to families with very low incomes, creating a negative effective tax rate for them. The personal income tax is the state’s largest revenue source.

The progressive structure of the personal income tax also improves racial equity, since Latinx and Black Californians have lower average incomes than white Californians due to racist policies and practices in employment, education, and every other facet of society.3Carl Davis, Marco Guzman, and Jessica Schieder, State Income Taxes and Racial Equity: Narrowing Racial Income and Wealth Gaps with State Personal Income Taxes (Institute on Taxation and Economic Policy, October 2021), 11, https://itep.sfo2.digitaloceanspaces.com/State-Income-Taxes-and-Racial-Equity_ITEP_October2021.pdf; Adriana Ramos-Yamamoto and Monica Davalos, Confronting Racism, Overcoming COVID-19, and Advancing Health Equity (California Budget and Policy Center, February 2021), https://calbudgetcenter.org/resources/confronting-racism-overcoming-covid19-advancing-health-equity/. As a result, the effective state personal income tax rate is lower on average for Latinx and Black families (3.6% and 4.0%, respectively) than for white families (5.0%).4Davis, Guzman, and Schieder, State Income Taxes and Racial Equity, 11-12. Tax agencies do not collect racial or ethnic information, so the Institution on Taxation & Economic Policy estimates effective tax rates by race/ethnicity by combining tax data and US Census Bureau American Community Survey data using a methodology explained here: https://itep.org/itep-tax-model/iteps-approach-to-modeling-taxes-by-race-and-ethnicity.

3. California’s Sales and Excise Taxes Are Regressive, Asking the Most from Those with the Least Ability to Pay

In contrast to the personal income tax, the sales and use tax is regressive. This is because people with lower incomes need to spend larger shares of their income to cover basic needs, so sales taxes take up larger shares of low-income households’ budgets. The sales and use tax is the state’s second-largest revenue source.

Excise taxes, which are taxes on specific goods including gasoline, alcohol, and tobacco, are also highly regressive. Like sales taxes, excise taxes hit people with lower incomes hardest since any money they spend on items subject to excises taxes will generally make up a larger share of their overall budgets compared to high-income people. In addition, since excise taxes are generally based on the volume of the purchase rather than the price, people at all income levels pay the same tax on a given amount of a product, whether they buy an economical brand or a more expensive brand.5Meg Wiehe et al., Who Pays: A Distributional Analysis of the Tax Systems in All Fifty States (Institute on Taxation and Economic Policy, October 2018), 19-20, https://itep.sfo2.digitaloceanspaces.com/whopays-ITEP-2018.pdf.

The 20% of California families with the lowest incomes pay 7.4% of their incomes in combined state and local sales and excise taxes, compared to 0.8% for the richest 1%. Again, because Black, Latinx, and many other Californians of color are more likely to have low incomes than white Californians, regressive taxes like sales and excise taxes exacerbate racial inequity.

4. California’s State and Local Tax System Could Be More Progressive

The overall impact of the state and local tax system on Californians is determined by the combination of the progressive personal income tax and regressive sales and excise taxes, as well as other taxes levied by the state and localities — most notably local property taxes and corporate income taxes. The combined impact is a state and local tax system that is regressive for people with lower incomes and progressive for people with very high incomes. The richest 1% of California tax filers pay the largest share of their income in state and local taxes (12.3%), but the 20% of filers with the lowest incomes pay the next highest share (11.4%). While the richest Californians pay a smaller portion of their income in sales, excise, and property taxes than any other group, it is made up for by the larger share of their income that goes to income taxes. Conversely, while the bottom 20% of Californians on average get money back from the personal income tax system via refundable tax credits, this is not enough to make up for paying larger shares of their income in sales, excise, and property taxes.

5. California’s Tax System Rewards Wealth but Doesn’t Tax Wealth

Wealth inequality is even more pronounced than income inequality, and racial wealth gaps are larger than racial income gaps. Many state tax policies contribute to wealth inequality and racial wealth gaps by providing substantial tax benefits to families who have assets like homes and retirement plans — such as the deductions for mortgage interest and property taxes, the partial tax exemption on the proceeds of home sales, and tax-privileged retirement accounts. Black, Latinx, and other people of color receive less of these tax benefits because — due to structural racism and discrimination — they are less likely to be homeowners, to be in jobs with access to employer-sponsored retirement plans, and to have the financial means to save or invest in assets.6Kayla Kitson, Promoting Racial Equity Through California’s Tax and Revenue Policies (California Budget & Policy Center, April 2021), 5, https://calbudgetcenter.org/resources/promoting-racial-equity-through-californias-tax-and-revenue-policies; Kayla Kitson, Tax Breaks: California’s $60 Billion Loss (California Budget & Policy Center, January 2020), 6-8, 10-11, https://calbudgetcenter.org/resources/tax-breaks-californias-60-billion-loss. At the same time, accumulated or inherited wealth is not taxed in California. Policymakers can eliminate or limit tax benefits that most advantage wealthy families and explore other options to better tax Californians who have amassed large amounts of wealth. The resulting revenues could then be directed to investments that help families who have been shut out from wealth-building opportunities achieve economic security and build wealth.

“

California policymakers can make the tax and revenue system more equitable.

”

Conclusion

There are many dimensions to ensuring that a tax system equitably generates the revenue needed for Californians to care for their families, build healthy communities, and contribute to a strong economy. Policymakers need to consider how any tax policy could have disparate effects on Californians by income, wealth, and race/ethnicity — as well as other factors not discussed in this fact sheet, such as gender, family structure, and income source.

The state’s current tax and revenue system is not fair for all Californians. People with the lowest incomes should not be paying larger shares of their incomes in state and local taxes than most other income groups, and the state’s tax policies should work to narrow racial wealth gaps, not widen them.

California policymakers can make the tax and revenue system more equitable. This includes ensuring that Californians with high incomes and wealth pay their fair share to support critical state services, providing further support for Californians with low incomes — such as by increasing and expanding refundable tax credits and making other tax credits refundable to benefit more low-income households — and eliminating or reforming tax benefits that primarily help wealthy Californians. Moving toward more robust taxation of Californians with higher income and wealth would also generate revenues that can be spent equitably to help more low-income households and Californians of color live and thrive, and expand opportunities to build wealth for themselves, their children, and their communities.

Aureo Mesquita and Sara Kimberlin, Staying Home During California’s Housing Affordability Crisis (California Budget & Policy Center, July 2020), https://calbudgetcenter.org/resources/staying-home-during-californias-housing-affordability-crisis/. Data are for 2018. “Low-income California household” is defined as a household with income below 200% of the federal poverty threshold — roughly $51,000 for a family of four in 2018 — and “high-income California household” is defined as a household with income of at least four times the federal poverty threshold — roughly $102,000 for a family of four in 2018.

2

California’s personal income tax rates range from 1% to 13.3%. The top rate for each tax bracket, or range of income, is only applied to the amount of income that exceeds the income threshold for that bracket.

Davis, Guzman, and Schieder, State Income Taxes and Racial Equity, 11-12. Tax agencies do not collect racial or ethnic information, so the Institution on Taxation & Economic Policy estimates effective tax rates by race/ethnicity by combining tax data and US Census Bureau American Community Survey data using a methodology explained here: https://itep.org/itep-tax-model/iteps-approach-to-modeling-taxes-by-race-and-ethnicity.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Californians deserve to have quality education and affordable health care, child care, and housing. To support such services, California’s tax and revenue system needs to generate adequate ongoing resources. Policymakers must regularly examine the state’s revenue system and revise it as needed to fairly raise enough revenue to support services and investments that help Californians thrive in their communities.

California largely relies on three revenue sources — the personal income tax, the sales and use tax, and the corporation tax. Together, they make up 95% of General Fund revenues. General Fund money may be used for any purpose and is the primary source of state support for health and human services, K-12 education, and higher education.

The personal income tax provides more than two-thirds of General Fund revenue. Individuals are taxed on income from sources such as wages, salaries, investments, pensions, and certain types of businesses. Higher portions of income are subject to higher tax rates, ranging from 1% to 12.3%, plus a 1% surtax on income over $1 million for a mental health services special fund.

The next largest revenue source for California is the sales and use tax, making up about one-sixth of General Fund revenues. The sales and use tax is levied on purchases of tangible goods in the state — not services — or the in-state use of goods purchased elsewhere. The statewide sales and use tax rate is 7.25%, but local governments may levy additional taxes.

California’s third-largest revenue source is the corporation tax, providing about one-tenth of General Fund revenues. This is a tax levied on the California profits of corporate businesses at a rate of 8.84%, or 10.84% for financial corporations. California generally taxes the share of a corporation’s income equal to the proportion of their sales that are attributable to California. The remainder of General Fund revenues come from taxes on insurance company premiums, alcoholic beverages, and cigarettes as well as non-tax revenue sources.

It is critical for policymakers and advocates to understand how California raises revenue and identify opportunities to improve the state’s tax and revenue system to equitably generate enough revenues to support services Californians need to thrive. This Fact Sheet is one of a series of publications looking at: the state’s tax and revenue system, tax breaks for the wealthy and large corporations, and how tax policies can better promote economic security for Black, Latinx, Asian, American Indian, and undocumented Californians, and families with low incomes.

SACRAMENTO — A new report by the California Budget & Policy Center shows that how California policymakers choose to raise and allocate resources — taxes and ongoing revenue — contributes to the economic inequities for Californians of color and low-income households while providing many more advantages to wealthy individuals. In a 5 Facts report —Promoting Racial Equity Through California’s Tax and Revenue Policies— the Budget Center outlines how a legacy of racist state and federal policies and practices, along with aspects of the tax code, block people of color from opportunities to build income and wealth.

This website uses cookies to analyze site traffic and to allow users to complete forms on the site. The California Budget & Policy Center does not share, trade, sell, or otherwise disclose personal information. By using our website you agree to our Privacy Policy.