Every Californian deserves quality education, health care, well-paying jobs, and the resources to build a secure future — and sustained public investment is how we get there. Recent experience shows that such investments are possible with voter-approved, progressive reforms that strengthen and expand California’s revenue base.

In 2012, California voters asked the state’s highest earners — the top 2% of Californians — to contribute a little more and use that money to invest in the services California’s communities need.

Proposition 30, approved by voters in 2012, temporarily raised income tax rates on just the top 2% of Californians. Four years later, voters chose to keep those rates in place through 2030 by passing Prop. 55. These tax rates have generated significant state revenue, securing investments in education and other important services.

The tax rate on the top 2% of Californians generates $9 to $10 billion per year, supporting investments in education, tax credits for Californians with low incomes, and strengthening the state’s finances.

What investments did the additional revenue secure?

California has used Prop 30/55 revenues to increase investments in education, increase access to health care, expand tax credits to Californians with low incomes, and strengthen state reserves, among other investments. The rate increases, along with a rising economy, made it possible for the state to increase education spending. During this period, the state implemented a major school finance reform and launched other initiatives such as the Universal Meals Program.

The top tax rates are set to expire in 2030, and voters will likely have an opportunity in November 2026 to renew this top tax rate to ensure the investments Californians make in schools, health care, and support for working families can continue.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Every Californian deserves affordable housing, health care, child care, well-paying jobs, and the resources to build a secure future — and sustained public investment is how we get there. Recent experience shows that such investments are possible with progressive reforms that strengthen California’s tax base, even when federal leaders push for the opposite.

In 2019, state leaders passed a budget that cleverly conformed to — adopted as part of state tax law — select provisions of the federal Tax Cuts and Jobs Act (TCJA), signed by President Trump in 2017. This federal tax package primarily slashed taxes for the wealthy and corporations, while cutting vital funding for food assistance and health care. California smartly chose to conform to only certain provisions that limited tax breaks for high-income households and businesses, thereby taking a step toward making the state’s tax system more fair and raising well over $1 billion in new, ongoing revenue each year.

key impact

Over $1 billion in new ongoing annual revenue, boosting K-14 education and expanding tax credits for working families

What Investments Did the Changes Make Possible?

This new revenue boosted funding for K-14 education and funded a significant ongoing investment in state refundable tax credits. Specifically, this new revenue allowed state leaders to fund the largest expansion of California’s Earned Income Tax Credit (the CalEITC) and the creation of the Young Child Tax Credit, both of which continue to provide hundreds or even thousands of dollars in tax refunds to families and individuals with very low incomes each year, helping them better meet basic needs.

CalEITC Expansion

The largest-ever expansion of the California Earned Income Tax Credit, putting hundreds to thousands of dollars back in the pockets of working families with the lowest incomes.

Young Child Tax Credit

A refundable tax credit, made possible by federal conformity, was created to provide direct financial support to families with young children and their futures.

How Did California Do It?

When the Republican-controlled Congress passed major federal tax legislation in 2017 — a package that largely benefited corporations and high-income households — California did not conform wholesale to federal law. Instead, state leaders, in collaboration with tax experts and advocates, carefully reviewed the changes and selectively adopted the provisions that scaled back tax breaks for wealthy households and corporations. Since these groups received generous federal tax giveaways, including tax rate cuts, many likely saw an overall decrease in taxes when considering both federal and state taxes.

By choosing which federal changes to incorporate into state law, California generated substantial new revenue without raising tax rates — making the tax system fairer while investing in communities.

While it seems to be an American pastime to complain about filing taxes, it’s an important day to reflect on what taxes represent and what tax revenues make possible. Taxes are a shared commitment to community and well-being — they are how we take care of one another and build toward a better future. State … Continued

What’s the difference between income and wealth? Taxes for individuals and corporations in California? Tax credits and deductions? Corporate revenues and corporate profits? Understanding these key terms is critical to navigating the state budget and its intersection with California’s tax and revenue system to generate ongoing resources and provide quality education, affordable health care, child care, housing, and other services for communities.

Generally, a tax filer’s total income before deductions. However, some types of income are not included in AGI; for example, income from Social Security and unemployment benefits is not included in California AGI. Additionally, certain “above-the-line” deductions can reduce AGI. Because federal and California law differ in these exclusions and deductions, a tax filer’s federal AGI may not match their California AGI.

Alternative Minimum Tax (AMT)

Certain tax filers must use an alternative calculation of tax liability if they benefit from certain tax expenditures and the tax that they would owe under the alternative method exceeds what they would owe under the regular method. The purpose of the AMT is to ensure that tax filers that take advantage of tax expenditures pay a minimum amount of tax on that preferentially treated income. California has an AMT for both individual tax filers and corporate tax filers. The corporate AMT is paid by only around 1% of corporate tax filers and accounts for less than 1% of corporate tax revenues. It does not prevent corporations from using tax credits to reduce their tax liability.

The corporate AMT is distinct from the $800 minimum franchise tax that is applied to most companies doing business in the state.

Apportionment

The process of dividing a corporation’s profits between jurisdictions where it operates in order to determine the share of the total profits that can be taxed in each jurisdiction. This is only applicable for businesses that do business both inside and outside of the state. In California, most corporations (as well as pass-through businesses) are required to apportion their profits by multiplying their total profits by their sales factor, which is the ratio of their California sales to their total sales. The result is the corporation’s state net income, the amount taxable in California. To arrive at the final tax bill, a corporation can then subtract net operating losses from its state net income, multiply the result by the applicable corporate tax rate, and subtract any available tax credits, which can result in a very low effective tax rate (well below the 8.84% rate for C corporations).

The only types of corporations that use a different apportionment formula are those in the agricultural and extractive industries (such as oil, gas, and mineral extraction corporations). These corporations instead use an apportionment factor that averages their California shares of their total sales, payroll, and property.

Asset

Property owned by an individual or business that is expected to provide a future economic benefit. Examples include financial assets such as stocks and bonds as well as physical assets such as real estate, vehicles, and business equipment.

C Corporation

A type of corporation that pays federal and state taxes based on its total profits (net income) at the entity level before profits are distributed to shareholders, who pay personal income tax on those distributions. C corporations are taxed differently from S corporations and other pass-through business entities. Corporations are subject to an 8.84% tax in California. Unlike S corporations, which can have up to 100 shareholders, C corporations can have unlimited shareholders; thus, most corporations listed on public stock exchanges, including most household-name companies, are organized as C corporations.

California Competes Tax Credit

A tax credit for businesses that commit to making investments and creating jobs in California. Credits are allocated through a competitive application process. The maximum amount of credits that can be awarded each year is $180 million.

Capital Gain

Generally, the difference between the value of an asset when sold and when it was originally purchased. California and the federal government generally do not tax the increase in the value of an asset until it is sold; this is sometimes referred to as a capital gain being “realized.” In contrast, an “unrealized capital gain” refers to the increase in value of an asset that has not yet been sold. In California, capital gains are taxed at the same rate as income from employment, whereas at the federal level, they are subject to lower tax rates than employment income.

Corporate Revenues

The money a corporation receives from the sale of goods and services before accounting for expenses, such as wages and salaries and the costs of business inputs. This is distinct from profit (net income), which represents the income remaining after costs are deducted, and gross receipts, which is the sum of revenues from core operations and other types of income.

Corporate Profit (alternatively, Net Income)

The money a corporation has remaining after deducting its expenses from its gross receipts for a given period. California’s corporation tax is levied on the share of a corporation’s net income attributable to California based on the applicable apportionment formula.

Corporation Tax

A tax imposed on corporations that derive income from California — with the exception of insurance companies, which instead pay the insurance tax. California only taxes the share of a corporation’s profits (net income) earned in California, determined by an apportionment formula. In California, C corporations are subject to an 8.84% tax on their profits and S corporations are subject to a 1.5% tax, in addition to the personal income tax S corporation owners pay on their share of the corporation’s profits. Banks and other financial institutions pay an additional 2% bank tax, as they are exempt from personal property taxes and all other local business taxes paid by other corporations. Corporations must pay at least the minimum franchise tax, and a small share of corporations are also subject to an alternative minimum tax.

Deduction

A reduction in taxable income (or a reduction in Adjusted Gross Income, in some cases) for certain expenses. For individuals, deductions cannot reduce taxable income below zero. Many deductions are available only to tax filers who claim itemized deductions. Because the value of a deduction is based on a tax filer’s tax bracket, and higher-income households are subject to higher income-tax rates, they receive larger savings for each dollar deducted than do lower-income households, which are subject to a lower tax rate.

Corporations and other businesses can deduct costs such as salaries and wages, interest, advertising, and other expenses from their total income. If a business’s deductions exceed its income, this generates a net operating loss, which can be carried forward to future years to reduce taxable income across several years.

Dividends

A distribution of a corporation’s profits to its shareholders. Like capital gains, dividends are taxed as ordinary income in California but are subject to lower rates by the federal government.

Earned Income Tax Credit (EITC)

Arefundable tax credit that boosts the incomes of workers with low wages, and that is provided in both federal and California tax law. The credit increases as earnings rise up to a maximum point, after which the credit phases out. California’s Earned Income Tax Credit (CalEITC) is modeled on the federal EITC, but structured differently. California also provides an additional credit for CalEITC-eligible families with children under age 6, the Young Child Tax Credit.

Effective Tax Rate

The percentage of the tax base that is actually paid in tax after taking into account applicable credits, exemptions, deductions, and other tax preferences. Due to these preferences — as well as the graduated rate structure for the personal income tax — the effective tax rate is lower than the statutory or marginal tax rate.

Estate Tax

A tax imposed on someone’s estate, meaning the value of their assets upon their death. In contrast to an inheritance tax, an estate tax is paid by the estate prior to distribution to heirs and other beneficiaries. Currently, the federal government imposes an estate tax on high-valued estates, but California does not impose an estate tax. California voters approved Proposition 6 in 1982, which repealed the state’s existing inheritance tax and prohibited the enactment of future taxes on estates, inheritances, or any transfer occurring upon death. Thus, any proposed estate tax would need to be approved by California voters.

Excise Tax

A tax on the sale of a specific good, such as alcohol, tobacco, or gasoline.

Exclusion

A provision that allows certain types of income to be ignored in tax calculations. For example, California does not require tax filers to include income from Social Security or unemployment benefits in their total income for tax purposes.

Exemption

This can have different meanings in different contexts.

At the federal level, tax filers were able to claim “personal exemptions,” essentially a deduction of a flat dollar amount per tax filer and dependent, prior to 2018. However, the 2017 “Tax Cuts and Jobs Act” suspended personal exemptions through 2025.

California offers “exemption credits,” which are nonrefundable tax credits of a set dollar amount for each tax filer and dependent, with higher amounts for blind individuals, seniors, and dependents.

California law includes many sales tax exemptions, where certain types of items are not subject to the sales tax. The largest of these sales tax exemptions are for food products, prescription medications, and utilities.

Some organizations, such as nonprofit, educational, and religious organizations, can have tax-exempt status, meaning they are generally not subject to corporation taxes.

Filing Status

The category a tax filer belongs to based on their marital status and family structure. One’s filing status affects the applicable income thresholds for each tax bracket, the amount of the standard deduction, and the qualification criteria for some tax expenditures. There are five filing status at both the state and federal levels:

Single

Married filing jointly (also applies to Registered Domestic Partnerships in California)

Married (or Registered Domestic Partnership) filing separately

Head of household

Qualifying widow(er)

Film Tax Credit

A tax credit for businesses engaged in film and television production. California’s Film & Television Tax Credit Program allocates tax credit awards to film and television productions made in California through a competitive application process. For fiscal years 2025-26 through 2029-30, the maximum amount of credits that can be awarded each year is $750 million — up from $330 million for fiscal years 2015-16 through 2024-25. While the credit has historically been nonrefundable, businesses can elect to receive a refundable credit for 2025-26 through 2029-30 — meaning they can get cash back if their credit allocation exceeds their tax liability — but the credit amount would be reduced by 10% and must be claimed across a 5-year period. The credit can only be claimed once filming is completed, and can be taken over a multi-year period.

Graduated Income Tax

An income tax structure in which the tax rate increases with income, with the first x dollars subject to a low rate, the next y dollars subject to a higher rate, and so on. California has a graduated income tax structure, with rates ranging from 1% to 12.3% — before the application of a 1% surtax on income above $1 million to fund mental health services. This structure, along with tax preferences such as exemptions, deductions, and credits, reduces tax filers’ effective tax rate below their marginal tax rate.

Gross Receipts

The total amount of money a corporation or other business receives for a given period — including revenues from sales as well as other types of income, such as interest, dividends, and rental income — before deducting its costs. California’s corporation tax is not levied on gross receipts, but some other state and local governments have taxes applied to a company’s gross receipts.

Horizontal Equity

Along with vertical equity, one of the two principles of tax equity. Horizontal equity isthe concept that tax filers with similar economic circumstances should be taxed similarly. For example, under Proposition 13 of 1978, California’s local property tax is based on the inflation-adjusted purchase price of the property rather than its current market value, meaning two tax filers owning properties with the same market value may owe significantly different amounts of tax based on when they purchased the property. This Prop. 13 policy violates the principle of horizontal equity.

Income

Money received over a certain period by an individual, family, or household, such as money from employment, investments, business ownership, and other sources. Income is not equivalent to wealth.

A tax on the value of inherited wealth received by an heir, in contrast to an estate tax, which is applied directly to the decedent’s estate before assets are distributed to beneficiaries. California voters approved Proposition 6 in 1982, which repealed the state’s existing inheritance tax and prohibited the enactment of future taxes on estates, inheritances, or any transfer occurring upon death. Thus, any proposal to reinstate an inheritance tax would need to be approved by California voters.

Insurance Tax

A tax on the premiums received by insurance companies. This tax is paid by insurance companies in lieu of the corporation tax.

Investment Income

Income received from investmenting in assets, including capital gains, dividends, and interest payments.

Itemized Deduction

A deduction for specific types of expenses. Major itemized deductions allowed under California’s tax law include those for mortgage interest, local property taxes, charitable contributions, an employee’s business-related and miscellaneous expenses, and large medical expenses. At both the federal and state levels, tax filers choose between taking a flat standard deduction or itemizing their deductions. Itemizing deductions generally benefits higher-income tax filers most, since they are more likely to have high-value homes — and therefore large expenses for mortgage interest and property taxes — and more likely to donate large sums to charity. However, California law does reduce the amount of itemized deductions allowed for tax filers with federal Adjusted Gross Income above specified thresholds (roughly $200,000 for single filers, $300,000 for heads of household, and $400,000 for joint filers).

Limited Liability Company (LLC)

A type of business that blends corporate and partnership structures and can elect to be taxed as a partnership or as a corporation. LLCs are also required under California law to pay an annual tax of $800 as well as a tiered fee based on income.

Marginal Tax Rate

The rate at which one’s highest increment of income is taxed. Due to California’s graduated income taxstructure, a tax filer’s marginal tax rate is higher than their effective tax rate. For example, under California’s 2021 personal income tax brackets, a single tax filer with a taxable income of $150,000 had a top marginal rate of 9.3%, but they only paid this rate on income above $61,214. The first $9,325 of their income was subject to a 1% rate, then income between $9,325 and $22,107 was subject to a 2% rate, and so on. Due to this tiered rate structure, this tax filer’s effective tax rate would be well below 9.3%.

Minimum Franchise Tax

An $800 tax that corporations doing business in California must pay if their regular corporate tax liability is lower than that amount. Corporations are exempt from this tax in their first year of operating in California.

Net Operating Loss (NOL)

The amount by which a business’ deductions exceeds its total income in years when it experiences a loss rather than a profit. Net operating losses incurred during loss years can be carried forward to reduce a business’ taxable income in future years when it is profitable — potentially down to zero.

Nonrefundable Tax Credit

A tax credit that cannot exceed a tax filer’s tax liability, or in other words, cannot reduce tax liability below zero. For example, if a tax filer has a tax liability of $1,500 and would otherwise qualify for a tax credit of $2,000, the credit would be capped at $1,500. This means that tax filers with low incomes who have little to no personal income tax liability often do not fully benefit from these credits. California’s Renter’s Credit and Child and Dependent Care Credit are nonrefundable.

Partnership

A type of pass-through business where the business’ income (or loss) is passed through to its partners. There are two common types of partnerships: limited partnerships, which are required to pay an annual entity-level tax of $800 in California; and general partnerships, which are not required to pay an entity-level tax.

Pass-Through Business

A type of business entity which is not subject to the regular federal or state taxes on corporations, and instead passes income (or losses) through to its owners, who report it on their personal income tax returns. Depending on the type of pass-through business, the entity may also be required to pay an annual tax or fee in California. Pass-through entities include S corporations, partnerships, limited liability companies, and sole proprietorships.

Personal Income Tax

A tax on the income of California residents as well as the income of nonresidents derived from California sources. The tax applies to income from employment, investments, pass-through businesses, and retirement plans. California’s personal income tax has a graduated rate structure that includes nine tax brackets, with rates ranging from 1% on the lowest share of income up to 12.3%. California also levies a 1% surtax on all income above $1 million to fund mental health services. Due to its graduated structure and other features, California’s personal income tax is a progressive tax. The personal income tax is California’s largest source of revenues.

Progressive Tax

A tax which takes up a higher share of income for higher-income households than for lower-income households. California’s personal income tax is a progressive tax.

Property Tax

A tax on real property (land and buildings) and certain types of personal property, including aircraft, watercraft, and business equipment and fixtures. Property taxes remain within the county where they are collected and are allocated among the county government, cities, K-12 schools and community colleges, and special districts based on formulas outlined in state law. While the property tax is a local revenue source, it is governed by provisions put into the state Constitution by Proposition 13 of 1978 and subsequent ballot measures. Under Prop. 13, the general property tax rate is capped at 1% of the assessed value of the property, which for real property is limited to its purchase price plus an annual inflation adjustment not exceeding 2%.

Proportional Tax

Also called a “flat” tax, a tax which takes up the same percentage of income for all households.

Refundable Tax Credit

A tax credit which can reduce a tax filer’s tax liability below zero and provide the difference as a refund. For example, if a tax filer has a tax liability of $1,500 and is eligible for a $2,000 credit, the credit will zero out their tax liability and provide a $500 refund. Because low-income families often have little to no tax liability, a tax credit will only fully benefit these families if it is refundable. The federal Earned Income Tax Credit and California’s Earned Income Tax Credit (CalEITC) and Young Child Tax Credit are refundable.

Regressive Tax

A tax that takes up a larger share of income for lower-income households than for higher-income households. Examples include the sales and use tax and excise taxes. Federal tariffs — or taxes on imported goods — also function as regressive taxes as they drive up the costs of consumer goods, which disproportionately impact households with lower incomes.

Research and Development (R&D) Tax Credit

A tax credit for businesses that make investments in research and development. In California, there is no limit on the amount of research and development credits that businesses can claim in any given year — any business that meets the eligibility criteria can claim the credit. The credit is generally nonrefundable, so a business cannot use credits to reduce its tax bill below zero and get a cash refund, but businesses may carry forward unused credits indefinitely to reduce their tax bills in future years. The R&D credit costs the state an estimated $2 billion to $3 billion each year.

S Corporation

Formally known as a “Subchapter S corporation,” a type of corporation that is taxed as a pass-through business and has no more than 100 shareholders. State law also requires S Corporations to pay the higher of a $800 minimum franchise tax or 1.5% of its California income.

Sales Factor

The ratio of a business’ California sales to its total sales. This percentage is used to apportion a business’ profits — or approximate the share of its total profits that is attributable to California and can be taxed in California.

Sales and Use Tax

A tax on the purchase of tangible goods in California (the sales tax) or on the use of tangible goods in California that were purchased elsewhere (the use tax). The sales and use tax is California’s second-largest revenue source. Services are excluded from the sales and use tax, as are other items exempted by law, including groceries and medications. The sales and use tax is a regressive tax, because lower-income households generally must spend a larger share of their incomes on necessities than higher-income households, so a larger share of their income goes to sales taxes.

A type of pass-through business owned by an individual, or couple, who reports the business’ income on their personal income tax return rather than being subject to corporation taxes.

Standard Deduction

A deduction that tax filers can claim on federal and California tax returns instead of claiming itemized deductions. A standard deduction is a set amount that only varies by filing status. For 2021, the California standard deduction was $4,803 for single filers and married couples filing separately, and $9,606 for married couples filing jointly, heads of household, and qualifying widow(er). These amounts are adjusted annually for inflation.

State and Local Tax (SALT) Deduction

A federal itemized deduction for state and local taxes paid, including property taxes and either income or sales taxes. The federal tax changes of 2017 (the “Tax Cuts and Jobs Act”) limited the deduction any tax filer can take to $10,000 (through 2025). California allows a similar deduction for property taxes and certain other state, local, and foreign taxes, but does not limit the amount of the deduction.

Stepped-Up Basis (alternatively, “Basis Step-Up”)

A tax provision in both federal and California law that allows heirs who have inherited assets to exclude the capital gain — or increase in value of the asset — that accrued before the inheritance for the purpose of calculating income taxes when they sell those assets.

For example, if a parent purchased an asset — such as shares of stock — for $100,000 and the value has increased to $200,000 by the time their child inherited the asset, the child could then sell those shares and pay no capital gain tax on that $100,000 increase in value. The child would only owe tax on any further increase in value starting from the time of inheritance — so if the child sold the asset one year later and it had increased in value to $250,000, they would only pay tax on the $50,000 increase in value after inheritance rather than the full $150,000 increase.

Surtax

An additional tax levied on top of the regular tax structure. For example, California voters approved Proposition 63 in 2004, which created a 1% surtax on taxable income over $1 million to fund mental health services. This is in addition to the tax owed according to the state’s regular personal income tax structure with a top rate of 12.3%, making the combined top tax rate 13.3%.

Tax Avoidance

Legal methods of reducing tax liability (in contrast to tax evasion).

Tax Base

The universe of income, assets, sales, or other economic activity subject to tax. Tax expenditures narrow the tax base, whereas eliminating or limiting tax expenditures broadens the tax base.

Tax Brackets

Ranges of taxable income that are subject to a given tax rate. The brackets vary by filing status; in California’s personal income tax system, the income thresholds for each bracket for couples filing taxes jointly are two times the thresholds for single filers. Additionally, the thresholds are higher for Californians who file as heads of household than for single filers.

Tax Conformity

This term refers to alignment between California’s tax law and the federal tax code. California’s tax law contains many references to federal tax law, but unlike many other states, California does not automatically adopt, or “conform to,” changes to the federal tax code. Instead, the Legislature must take action to incorporate federal tax changes — in part or in whole — into state law. At the time this glossary was published, references in California’s tax law to the federal Internal Revenue Code generally pointed to the federal code as it read on January 1, 2015. However, state policymakers have incorporated into state law selected federal tax changes that occurred after that date.

Tax Credit

A dollar-for-dollar reduction in tax liability for individual or corporate tax filers. Tax credits can be refundable or nonrefundable.

Tax Evasion

Illegal methods of avoiding or reducing taxes, such as deliberate non-payment or underpayment.

Tax Expenditure

Refers to exceptions to “normal tax law” that reduce the revenue governments would otherwise collect. These exceptions include, but are not limited to, exemptions, deductions, exclusions, tax credits, deferrals, elections, and preferential tax rates. Tax expenditures can be commonly referred to as tax breaks, tax loopholes, or tax preferences.

Tax Haven

A country or other type of jurisdiction with very low or zero tax rates. Businesses and individuals can transfer money into tax havens and reduce their tax liabilities through both legal tax avoidance and illegal tax evasion. These jurisdictions often also have features that provide secrecy for individuals and businesses holding money in those locations, making it more difficult for tax authorities to effectively identify cases of tax avoidance and evasion.

Tax Liability

The amount of tax owed. Tax credits can reduce tax liability; nonrefundable tax credits cannot reduce tax liability below zero, but refundable tax credits can.

Tax Rate Schedule

A table indicating the tax rates that apply to each interval of taxable income. California’s personal income tax has three tax rate schedules, which tax filers with taxable income above $100,000 must use to determine their tax liability: “Schedule X” applies to single filers and married/Registered Domestic Partnership couples filing separately; “Schedule Y” applies to married/Registered Domestic Partnership couples filing jointly and qualifying widow(er)s; and “Schedule Z” applies to head of household filers. Filers with taxable income of $100,000 or less consult a tax table to determine their state personal income tax liability instead of using the tax rate schedule.

Tax Table

A table that California tax filers with taxable incomes of $100,000 or less use to look up the amount of their state income tax liability. In contrast to California’s tax rate schedules — which include precise tax liability calculations — the tax table assigns one rounded tax amount to filers of a given filing status with taxable incomes within intervals of approximately $100.

Taxable Income

The result of subtracting a tax filer’s standard deduction or itemized deductions from their Adjusted Gross Income. A filer’s tax liability is determined by applying the applicable tax rates to their taxable income.

Vertical Equity

Along with horizontal equity, one of the two types of equity considered when evaluating tax policies. While horizontal equity is concerned with tax filers with similar economic circumstances, vertical equity is concerned with the distribution of taxes across the tax filers of different income levels. Progressive taxes are considered to be vertically equitable because they make up a largest share of income for the highest-income tax filers, who have the greatest ability to pay.

Water’s Edge Election

A provision that allows global corporations to choose to exclude the profits held in their foreign subsidiaries from their total profits before determining the share of their profits that is taxable in California with apportionment formulas. This is in contrast to the default tax filing method for corporations, worldwide combined reporting, which requires corporations to calculate the worldwide profits across all their subsidiaries before apportioning profits among taxing jurisdictions. The water’s edge election allows some corporations to make it appear that they have little or no profits in California by shifting US profits into tax havens abroad — reducing their California tax bills. Corporations electing to file taxes using this water’s edge method must make the election for a seven-year period.

Wealth

The value of the resources that an individual, family, or household owns. Wealth is often measured by net worth, which is the sum of the value of all assets minus all liabilities, or debts, like money owed on loans.

Worldwide Combined Reporting

The default method for corporations to determine their total profits — before determining the share of their profits that is taxable in California with apportionment formulas. This method requires a corporation to combine the profits of the parent company and all its subsidiaries worldwidebefore apportioning profits between taxing jurisdictions. Instead of using the worldwide combined reporting method, corporations can exclude the profits of their foreign subsidiaries when calculating total profits by using the water’s edge election, which can reduce their California taxes.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Communities across California face many challenges during President Trump’s second administration, from deep federal budget cuts that threaten to undermine Californians’ health, economic security, and well-being, to mounting affordability pressures and persistent inflation that have exacerbated communities’ longstanding unmet need for more affordable housing, health care, and child care. People with low incomes, immigrants, communities of color, and other marginalized Californians are bearing the brunt of these challenges, as harmful and discriminatory federal policies compound existing inequities based on race and wealth.

State leaders have an opportunity to chart a different path for California, and they have both the responsibility and the ability to respond. This report shows that:

Policymakers have the tools to better meet Californians’ needs and the evidence to prove it. Recent progress — from improvements in health coverage, to gains in affordable housing and declines in homelessness, to increased child care enrollment and lower child poverty — shows that when the state invests in people’s essential needs, quality of life improves.

Progress is now under threat from federal cuts and policy rollbacks. Federal cuts are targeting the very programs that have improved Californians’ lives, hitting the most vulnerable communities hardest and widening existing inequities.

Policymakers have the resources and revenue solutions to fight back. California has the fourth-largest economy in the world and is home to a large share of the nation’s wealthy as well as some of the largest, most profitable corporations, all of which benefit from the state’s public services and infrastructure. Yet California loses billions of dollars each year due to tax breaks and loopholes that benefit corporations and the wealthy — resources that could be better spent meeting the needs of California families.

H.R. 1 and the Federal Budget

H.R. 1, the harmful Republican mega bill passed in July 2025, will deeply harm Californians by cutting funding for essential programs like health care, food assistance, and education.

See how California leaders can respond and protect vital supports.

Tax Revenue Funds the Public Investments That Improve Californians’ Lives

Every Californian deserves affordable housing, health care, and child care, well-paying jobs, and the resources to build a secure future — and public investment is how we get there. Recent experience shows that when policymakers invest in meeting people’s essential needs, Californians’ quality of life improves. In recent years:

California’s uninsured rate fell to a historic low following investments to expand access to health coverage

In 2014, California fully implemented federal health care reform, which, along with more recent state initiatives to expand full-scope Medi-Cal to all income-eligible Californians regardless of immigration status, helped the state reach a historically low uninsured rate of 5.9% in 2024.

case Study: How a Tax on Wealthy Households Funds Schools, Health Care & More

Voters asked the top 2% of earners to contribute more — generating $9 to $10 billion per year for education, tax credits for families with low incomes, and a stronger, more resilient state budget.

Expanding Medi-Cal to undocumented children led to significant improvements in their health

Undocumented children in California became eligible for full-scope Medi-Cal in 2016, and coverage was fully expanded to cover all income-eligible Californians in 2024. Research shows that after the expansion to undocumented children took effect, the percentage of non-citizen children who reported being in excellent health increased by 10 percentage points from 20% to 30%, suggesting that investing in health coverage for all contributed to significant improvements in people’s health.

More Californians are exiting homelessness — thanks to public investments

This is in large part due to significant state investments in the Homeless Housing, Assistance and Prevention (HHAP) program, which allows communities across California to fund solutions tailored to their local needs. In 2024 alone, homeless service providers assisted over 330,000 Californians experiencing homelessness. HHAP has helped drive a 24% decline in youth homelessness since 2019 and supported more than 90,000 Californians in moving into permanent housing since 2023. These and other state homelessness investments have led to a statewide 9% drop in unsheltered homelessness in 2025.

California has doubled the production of new affordable homes in recent years

According to the California Housing Partnership, California produced more than 17,900 units in 2024. This increase was largely driven by major state investments in various affordable housing programs between 2019 and 2023, which helped thousands of developments pencil out and open their doors. More homes are still needed — but the gains are spreading, with more counties becoming affordable for California households with middle and lower incomes.

Enrollment in publicly funded child care has steadily increased following the partial expansion of subsidized child care spaces

In 2021, the Newsom administration promised to expand affordable child care to more than 200,000 children. Around 60% of that promise has been fulfilled: the share of eligible children enrolled in publicly funded child care grew from 11% in 2022 to 16% in 2024. That means thousands more children are getting the care that supports their healthy development and thousands more families have the economic security to thrive.

California’s child poverty rate dropped by 40% in one year following the significant temporary expansion of the federal Child Tax Credit

In 2021, the federal Child Tax Credit was increased and made fully refundable, allowing millions of families with very low incomes to access the full credit for the first time. This expansion drove a 40% drop in California’s child poverty rate and was associated with reductions in food insecurity and racial income inequities. This demonstrates that poverty is a policy choice and that a significant expansion of California’s own tax credits could have a widespread impact for families and individuals experiencing poverty.

case Study: Clever Strategy Allowed California to Raise New Revenue Following Federal Tax Cuts

In 2019, California selectively conformed to parts of the federal Tax Cuts and Jobs Act, enacted during President Trump’s first term, and raised over $1 billion in new, ongoing annual revenue — boosting K-14 education and expanding tax credits for working families.

There are still 1.8 million children in California who are eligible for publicly funded child care but not enrolled, underscoring the state’s need to fulfill its promise or risk forcing tens of thousands of families to make the impossible decision between going to work or caring for their child.

When COVID-era investments expired, the child poverty rate rapidly increased, and California continues to have the highest poverty rate of the 50 states, tied with Louisiana, pointing to the need for state leaders to do more to help Californians meet basic needs.

Yet recent and projected budget shortfalls make clear that California’s tax system isn’t generating enough resources even to maintain recent progress — let alone build on it. And now, deep federal funding cuts and other harmful actions are upending California’s progress toward a more equitable future.

Federal Cuts Are Threatening California’s Hard-Won Progress

The progress California has made didn’t happen by accident — it took sustained public investment. Now federal cuts are targeting the very programs that made that progress possible, and the communities bearing the greatest burden are those that were already struggling most.

If state leaders fail to raise additional revenue and expand public investments, here’s what’s at risk for California families:

Up to 2 million Californians may lose their Medi-Cal coverage

Federal cuts to health care could cause up to 2 million Californians with low and modest incomes, who are disproportionately Latinx and other Californians of color, to lose their Medi-Cal coverage. While this will impact all Californians, immigrants’ access to care is specifically restricted, including the elimination of health insurance coverage for many immigrants, such as refugees, asylees, and trafficking survivors. This is estimated to leave 200,000 Californians without crucial health insurance they need to survive. Recent state action to restrict coverage for immigrants will add to the harm by reversing progress made towards providing health care for all.

As people lose health insurance, clinics and hospitals — especially in rural areas — will face additional financial strain, leading to overcrowded clinics, fewer options for care in local communities, and higher premiums, among other ripple effects that will impact the entire health care system. Proposed additional state cuts to health care access for immigrants would further exacerbate the harm by causing even more Californians to lose coverage.

Over 3 million California households are at risk of losing some of all food assistance

Federal cuts to food assistance could put more than 3 million households with very low incomes, disproportionately Black, Latinx, and other people of color, at risk of losing some or all assistance. The harshest cuts target some of the most marginalized state residents, including refugees, asylees, and other humanitarian immigrants, as well as former foster youth, veterans, and people experiencing homelessness. Without state action to offset the cuts, food insecurity and poverty will rise, and an entire ecosystem of jobs and businesses connected to the food economy will be damaged.

At least 75,000 Californians could fall into homelessness

Federal threats to housing and homelessness programs, combined with inadequate state support, could undermine California’s progress in reducing homelessness and supporting housing stability for Californians with the lowest incomes, a large share of whom are older adults and people with disabilities. Harmful changes to federal Continuum of Care funding are expected, and current federal appropriations still fall short of covering nearly 15,000 California families with an Emergency Housing Voucher — putting homelessness services and households who have already secured housing at risk of falling back into homelessness. At the same time, a proposed federal rule targeting mixed-status households could put roughly 7,190 California families at risk of losing HUD-assisted housing, most of which include children, and impose new red-tape on more than 820,000 U.S. citizens in California. Proposed cuts to HHAP and the failure to provide new General Fund investments in affordable housing add to these challenges.

State Leaders Have Common-Sense Options to Raise Revenues and Protect Californians From Federal Harm

The choices state leaders make will determine who bears the burden and who benefits from H.R. 1. Maintaining the status quo means choosing to protect tax breaks for corporations and the wealthy at the expense of everyone else. Without bold action, people with low incomes, immigrants, communities of color, and other marginalized Californians will be left to bear the full brunt of federal cuts. California has commonsense options to minimize the harm, including:

Closing the “water’s edge” loophole, the most costly state corporate tax break

The “water’s edge” loophole allows global corporations that shift US profits to tax havens to avoid $3 to $4 billion in state taxes each year, at the expense of everyday people. This tax break rewards large profitable corporations that engage in aggressive tax planning by making it appear they are less profitable in the US and in California than they actually are — something small domestic businesses and individuals working for a living cannot do.

Putting reasonable limits on corporate tax credits and deductions

Reasonable caps on corporate tax credits and deductions would ensure corporations cannot use them to reduce their tax bill to the mere state $800 minimum tax. Policymakers can continue the temporary limit on business tax credits put in place by the 2024-25 budget agreement — which capped the use of credits to $5 million per business each year from 2024 through 2026 — and reverse course on the provision allowing businesses to claim refunds for the credits that exceeded the cap after the temporary limit expires. These refunds are estimated to cost the state $6.8 billion across fiscal years 2026-27 and 2034-35, a time when millions of Californians will be dealing with the harms of the federal budget cuts and the state will be ill-positioned to protect Californians without substantially raising revenue.

Ensuring that wealthy individuals inheriting valuable assets don’t escape taxation

This can be done by eliminating the state’s “basis step-up” tax break so that people inheriting assets pay tax on the full increase in value of those assets when they sell them and reinstating an estate or inheritance tax on large estates or inheritances. Most California estates go untaxed due to California’s lack of a state-level estate or inheritance tax and the overly generous exemption from the federal estate tax, which allows wealthy families to pass up to $30 million to their heirs tax-free ($15 million per individual). The basis step-up tax break is estimated to cost the state around $5 billion each year — although revenue gains from repealing it would start small and accrue over time. The potential revenue from enacting an estate or inheritance tax — which would have to be approved by state voters — would depend on the design, but by one estimate could raise between about $900 million and $3.6 billion, depending on the size of estates that would be subject to the tax.

The Path Forward: Equitable Revenue, Public Investment, and a California Where Everyone Thrives

Strengthening California’s revenue base is long overdue — and now, as the federal government abandons its responsibility to support the health and well-being of all Americans, it is more urgent than ever. California can and must chart a different course. By ensuring the most profitable corporations and wealthiest Californians pay their fair share, state leaders can generate the resources needed to protect communities from federal harm, build on hard-won progress, and move toward a California where everyone can thrive.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

Millions of Californians are struggling to make ends meet and the affordability crisis continues to drive up the cost of basic necessities like groceries and rent. Simultaneously, the 2025 Republican megabill — H.R.1 — is further straining the budgets of low-income households, by making unprecedented cuts to health care and food assistance, and giving out over a trillion dollars worth of tax breaks to the already wealthy and corporations.

Specifically, under Governor Gavin Newsom’s budget proposal, the state is estimated to spend almost six times more on tax breaks for corporations than on state tax credits for low-income Californians during the 2026-27 fiscal year.

Expanding refundable tax credits and closing corporate tax breaks are common sense policies as the federal safety net is being weakened and corporations are showered with new federal handouts. Policymakers can support Californians in combating the state’s affordability challenges by closing the “water’s edge” loophole and placing reasonable limits on corporate tax credits and deductions so that no profitable corporation pays next to nothing in corporate taxes.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

Large profitable corporations in California have several strategies to avoid paying more than the minimum $800 state tax, costing the state billions in lost revenue each year. State leaders can take steps to reduce corporate tax breaks to better invest in the health and well-being of all Californians.

At a time when many Californians struggle with the state’s affordability challenges and millions will be harmed by the impacts of the deep federal cuts to health care and food assistance enacted by H.R. 1, the 2025 Republican megabill, highly profitable corporations continue to benefit from generous tax breaks at the state and federal levels. These corporations benefit from California’s skilled workforce, public infrastructure, and strong consumer base — all made possible by public investments supported by tax revenues. Yet some of these corporations pay next to nothing in corporate taxes in California, largely due to overly generous state tax breaks.

Reforming California’s corporate tax system to ensure all profitable corporations are contributing their fair share to support essential public services is a necessary step to generate ongoing revenues that the state needs to support the health and well-being of Californians and strengthen economic security for all.

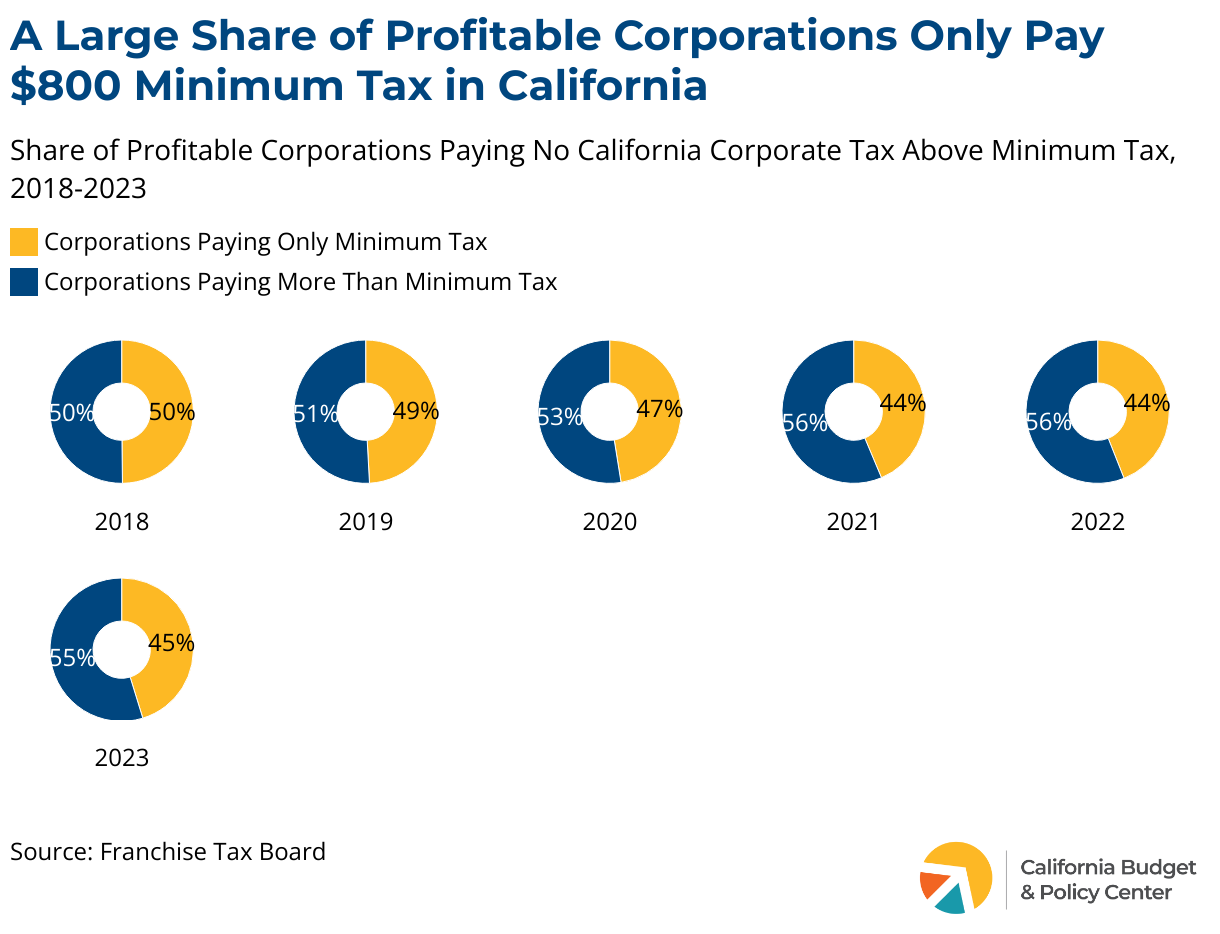

1. Many Corporations Only Pay the Minimum $800 State Tax

Most companies doing business in California are required to pay an $800 “minimum franchise tax” for the privilege of doing business in the state. Yet for nearly half of profitable corporations, this is all they pay in corporate tax to the state, even though they are turning a profit. They are able to do this by taking advantage of a variety of tax breaks that California policymakers have put into place over the years, such as generous tax credits that allow some corporations to essentially zero out their tax bills. For a corporation with $1 million in profits in California, paying only the $800 minimum state tax equates to an effective tax rate of 0.08% — while if it paid the full 8.84% statutory state corporate tax rate on those profits, it would owe $88,400.

Some corporations may also be profitable overall but make it look like they have no profits in the US or in California by shifting profits into foreign tax havens. They can then use the state’s water’s edge election to exclude those “foreign” profits from their total profits for the purposes of their California tax calculations and avoid paying taxes beyond the $800 minimum tax in California. Those corporations are not accounted for in the figures above, which only reflect the share of corporations reporting profits in California that only pay the minimum tax. There is no available data that would allow for distinguishing between corporations that are truly unprofitable and those that have used accounting mechanisms to shield profits from the reach of the state’s tax system.

2. Corporations are Receiving New Federal Tax Cuts, and Many are Paying No Federal Corporate Taxes

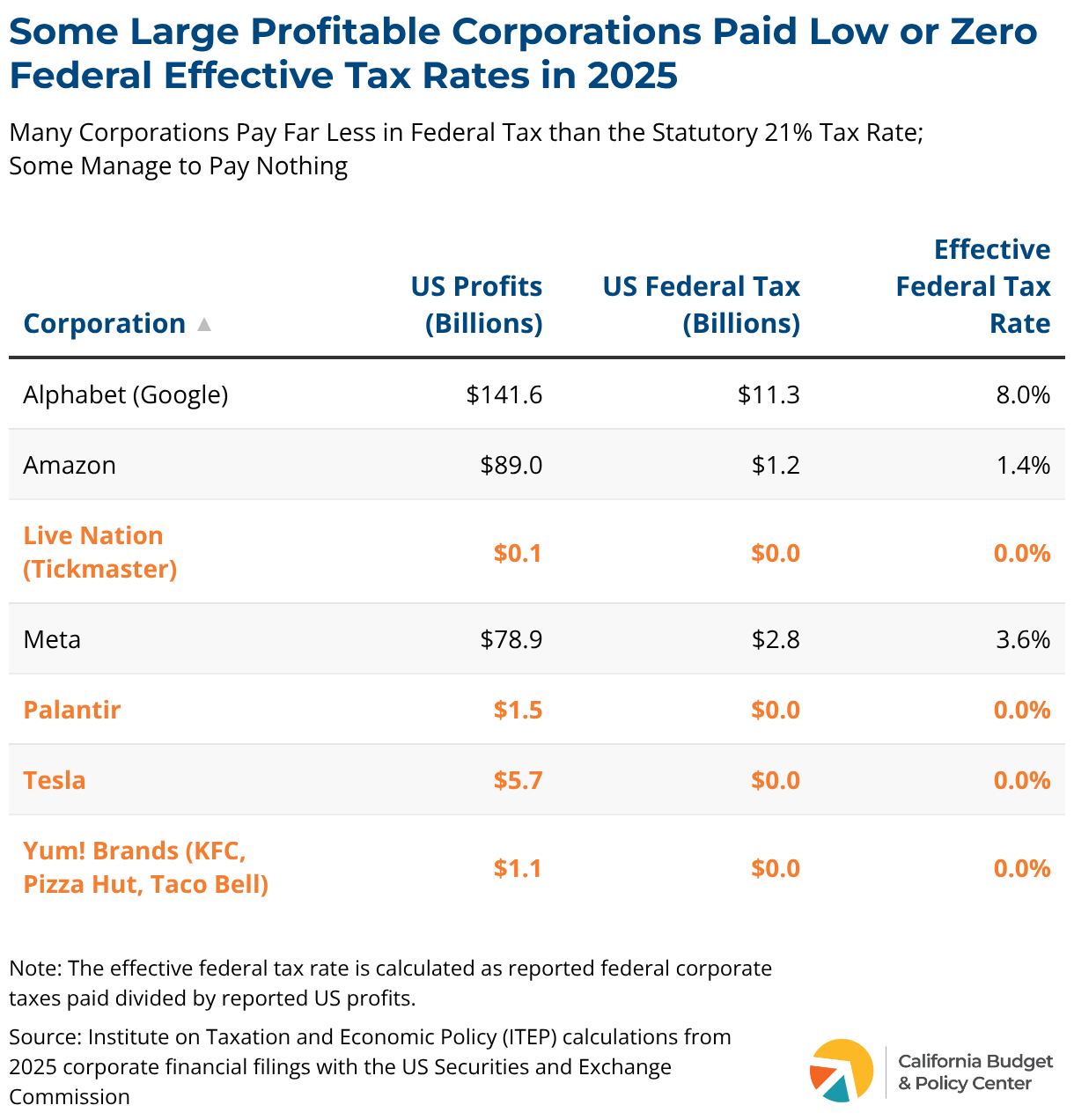

In 2017, Congress and the first Trump administration enacted major tax cuts, including slashing the federal corporate tax rate by 40%. In the first four years after those tax cuts, the largest and consistently profitable US corporations collectively saved about $240 billion in federal taxes, according to ITEP estimates. Moreover, after the 2017 law reduced the statutory tax rate from 35% to 21%, many corporations paid effective tax rates — the actual ratio of their tax bills to their profits — far below 21%. ITEP found that the effective tax rate was just 14% on average for Fortune 500 and S&P 500 companies that were consistently profitable from 2018 to 2022. Among this sample, 55 corporations had effective rates of less than 5%, and 23 paid nothing in federal tax across the entire 5-year period.

With H.R. 1, Congress and the second Trump administration doubled down on corporate tax cuts — making permanent some of the temporary tax breaks created in 2017 and rolling back provisions that were meant to raise corporate tax revenues to partially offset the cost of the steep corporate tax rate cut. Over a 10-year period, H.R. 1 will give corporations and other business tax cuts of more than $900 billion, while at the same time making the largest funding cuts to health care and food assistance in US history, which could result in up to 2 million Californians losing Medi-Cal coverage and more than 3 million households in the state losing some or all of their CalFresh food assistance — making life even less affordable for people struggling with the costs of living in the state.

In the wake of H.R. 1, some huge corporations are already reporting that they are paying nothing in federal tax or very low effective tax rates despite soaring profits, at least in part thanks to provisions of the new tax law — including Alphabet (parent company of Google), Amazon, Live Nation (parent company of Ticketmaster), Meta, Palantir, Tesla, and Yum! Brands (parent company of Kentucky Fried Chicken, Pizza Hut, and Taco Bell).

3. Corporate Taxes Do Not Limit Businesses’ Ability to Pay Workers

California’s corporate tax is an 8.84% tax on the “net income” of corporations. Net income, or profit, represents the income left over after the corporation’s costs are accounted for — or total revenues minus total expenses. So corporations pay corporate taxes only in years when they are profitable, after they have paid their workers and accounted for other costs. If a corporation breaks even or has a net loss — if expenses exceed revenues — it is only subject to the flat $800 minimum tax. Additionally, it can use that “net operating loss” to offset its taxable income in future years when it is profitable, potentially reducing its tax bill to the minimum tax for several years.

4. Reducing Corporate Tax Avoidance Strategies for Large Corporations Will Not Push Businesses Out of State

For corporations doing business both in and outside of California, the state only taxes a portion of a corporation’s profits. For most types of corporations, this is equal to the portion of the corporation’s total sales made in the state (this proportion is known as its “sales factor”). The tax is not based on where a corporation’s workers, founders, headquarters, or other properties are located. This means a corporation moving its headquarters or other locations out of state will not reduce its tax liability as long as it continues to make sales to California’s customer base of nearly 40 million people.

In fact, an examination of corporate tax returns by the state’s Franchise Tax Board found evidence that corporate taxes are not driving corporations to leave the state. Looking at the tax returns of more than 100 corporations that made a public announcement about leaving or shifting some operations out of California, they found that more than 60% were paying nothing more than the $800 minimum tax and that, on the whole, they paid more in corporate tax to California in the year after their announced departures.

5. Corporate Tax Breaks Worsen Racial Disparities

Corporate tax breaks mainly benefit those who own stock in those corporations, who are disproportionately wealthy and white. Black, Latinx, and other households of color are less likely to own stock either directly or through retirement plans or other investment funds — and even among those who do own stock, the median value of stock holdings is lower among families of color than among white families. These differences reflect generations of disparities in economic opportunities — stemming from racist policies and practices — that have hindered wealth-building for families of color. For example, families of color are less likely to inherit generational wealth, occupational segregation has funnelled workers of color into lower-paying jobs with less access to retirement savings plans, and higher unemployment risks may make some families of color less willing to invest in riskier assets like stocks.

Due to these disparities, white households receive about 88% of the benefits of a corporate tax cut, despite making up only 67% of the population, according to national-level estimates from the Institute on Taxation and Economic Policy (ITEP). Meanwhile, Black and Latinx households each only receive about 1% of the benefits, even though they represent 12% and 9% of all households nationwide.

State Policymakers Should Ensure Profitable Corporations Pay Their Fair Share to Help Build a More Prosperous California for All

The maintenance of corporate tax breaks in California law has meant billions of dollars in lost revenues over the years — revenues that could have gone a long way in supporting the health, economic security, and well-being of Californians who have been excluded from economic opportunities and face impossible choices between paying the rent, feeding their families, and accessing health care.

Reining in corporate tax breaks and strengthening the state’s revenue base is long overdue, and even more critical now as the unmet needs of Californians are only growing and the federal safety net is being weakened. Two common-sense solutions are to close the “water’s edge loophole” and place reasonable limits on corporate tax credits and deductions so that no profitable corporation pays next to nothing in corporate taxes.

SACRAMENTO, CA — The California Budget & Policy Center (Budget Center) released a new four-part series examining how California’s corporate tax code allows highly profitable corporations to avoid paying their fair share — and what state leaders can do to fix it. The series highlights how corporate tax loopholes, flat tax rates, and unlimited deductions … Continued

This website uses cookies to analyze site traffic and to allow users to complete forms on the site. The California Budget & Policy Center does not share, trade, sell, or otherwise disclose personal information. By using our website you agree to our Privacy Policy.