Billionaire Tax Explained: What Proposition 40 Would Mean for California

Implications of the One-Time Billionaire Wealth Tax for Californians

August 2026 | By the California Budget & Policy Center

key takeaway

Prop. 40 would institute a one-time 5% tax on the wealth of billionaires to raise tens of billions in temporary revenue to address the loss of federal funding and other threats to health, nutrition, and education services, largely a result of H.R. 1 — the 2025 budget reconciliation law known as the “One Big Beautiful Bill Act.” Prop. 40 could potentially raise tens of billions in revenue in the short-term to preserve critical services, but may also lead to some income tax revenue losses in future years to the extent that billionaires leave the state to avoid the tax.

California, like many other states, is facing a number of challenges to its ability to meet the needs of its residents, including the impending impacts of the deep federal cuts to public health care and nutrition assistance and the rising costs of providing services due to inflation, an aging population with more complex needs, and the state’s ongoing housing crisis. The federal cuts to Medi-Cal alone are expected to cost the state tens of billions of dollars in lost funding and could lead to around 1.3 million Californians losing health care access by 2029-30. Meaningfully addressing these challenges will require California to raise a substantial amount of revenue.

what is h.r. 1?

H.R. 1, the 2025 budget reconciliation law known as the “One Big Beautiful Bill Act,” signed by President Trump on July 4, 2025, will deeply harm Californians by cutting funding for essential health care and food assistance programs — while providing massive tax breaks to the wealthy and corporations. The spending cuts will disproportionately impact families with low incomes, immigrants, and communities of color, pushing more people into poverty and widening racial and economic inequities across the state.

Even prior to these more recent challenges, California was not generating enough revenue to meet the critical needs of all Californians through the state’s communities, evidenced by the state’s poverty rate remaining the highest in the nation. In addition to the human suffering caused by failing to ensure Californians can regularly access health care, put enough food on the table, and meet their other basic needs, such a failure dampens the state economy by preventing some individuals from fully participating in it and puts fiscal pressures on state and local governments as more households are forced to turn to costly emergency services and systems of last resort.

In the near term, Prop. 40 would likely generate tens of billions in revenue to prevent health coverage losses for Californians and stabilize the state’s health care system, and could provide additional support for nutrition assistance — which is also impacted by federal cuts — and for public education. Because the revenues would be one-time, the state would not be able to maintain these services in the future unless federal funding were fully restored or the state adopted alternative sources to raise this magnitude of revenue.

There is a strong rationale for taxing accumulated wealth — or taxing increases in wealth that currently go untaxed — given the profound wealth inequality and the vast unmet needs that exist in the state and across the country, as well as the ability of some ultrawealthy households to pay very little in income taxes as a share of their wealth.

At the same time, taxing wealth at the state level comes with some risks, particularly the potential for wealthy people to leave the state to avoid the tax, which would result in future state income tax losses if they did not return — putting at risk future funding for critical state services — and potential unknown impacts on the state economy. Prop. 40 attempts to counter that risk by applying the tax to billionaires who were California residents at the beginning of 2026, however it is likely this will be challenged in courts and the outcome is not certain.

In November, California voters will need to weigh the potential benefits of Prop. 40 against its potential tradeoffs.

Who Would Be Subject to the Tax Under Prop. 40 and How Would It Be Calculated?

Prop. 40 would institute a one-time tax on the worldwide wealth of billionaires. For the purposes of the measure, a billionaire subject to the tax could be an individual, a married couple, or a trust with net worth — as defined by the measure — above $1 billion. There are around 250 billionaires in California, with over $2 trillion in total wealth.1Forbes tracks the daily wealth of billionaires with its “Real-Time Billionaires” list, and the California-specific data was compiled in connection with Jasper Boll, Emmanuel Saez, and Gabriel Zucman, California Billionaires: Wealth, Taxes, and Wealth Tax Revenue Estimates (NBER Working Paper 35218, May 2026). Note: Saez is an author of Prop. 40.

The tax rate would be 5% for most billionaires, but the rate would be phased in for those with net worth between $1 billion and $1.1 billion.2Specifically, the 5% rate would be reduced by 0.1 percentage point for each $2 million that the household’s net worth falls below $1.1 billion. Taxpayers would have the option of paying the full amount of the tax with their 2026 tax returns or in installments across five years, with an annual deferral charge.

Net worth is typically calculated as the total value of assets held by an individual, couple, or family minus their total debts. However, Prop. 40 allows some exclusions from the net worth calculation, including:

Real property holdings, which are subject to constitutional tax limitations due to Proposition 13, approved by California voters in 1978;

Tangible personal property — such as vehicles, jewelry, appliances, or business equipment — held outside of California;3Tangible personal property is excluded from the net worth calculation if it is held outside of California for at least 270 days during 2026 unless it was temporarily relocated for the purpose of tax avoidance. and

Certain pensions, retirement accounts, and deferred compensation arrangements.

The measure would apply the tax to billionaires who were California residents on January 1, 2026, and the amounts subject to the tax would be determined based on their net worth on December 31, 2026. There will likely be legal challenges to the application of the tax based on residency prior to the enactment of the tax. Federal and state tax measures often have retroactivity provisions to minimize tax avoidance and courts have upheld many of these laws, although it is unknown how courts would ultimately rule on this measure. The measure specifies that in the case the residency and valuation dates are invalidated by courts, these dates shall be construed to be the earliest dates consistent with law.

Prop. 40 establishes procedures for estimating the value of various types of assets that would be included in net worth for the purpose of the tax. Valuation is simple for some assets, such as holdings of publicly traded stock, which have a known market value at any given time. Other assets, such as shares of private businesses, intellectual property such as copyrights or trademarks, and artwork, are more difficult to value without a sale taking place. The measure has detailed valuation rules and formulas for different types of assets, and both the taxpayer and the state’s Franchise Tax Board — which would be responsible for administering the tax — could obtain certified appraisals in the case of valuation disputes. Additionally, the measure contains provisions intended to minimize the ability of taxpayers to avoid or evade their tax responsibility.4Tax avoidance reflects legal avenues to reducing tax liability, such as redirecting wealth holdings to exempted assets or relocating, whereas tax evasion encompasses illegal tactics to avoid taxes, such as hiding assets in tax havens, underreporting of asset values, or falsely claiming residency outside of the tax jurisdiction.

Example: Potential Impact of Prop. 40 on Mark Zuckerberg

Mark Zuckerberg, cofounder of Facebook, has a net worth of around $200 billion. Assuming he has approximately $200 billion in wealth subject to Prop. 40 on December 31, 2026, when net worth is to be determined for the purpose of the measure, he would owe around $10 billion in tax, which he could pay in five annual installments of $2 billion. His remaining wealth of around $190 billion would still be more than the entire economies of dozens of countries, roughly on par with the Gross Domestic Product of Morocco.

For comparison, Zuckerberg’s net worth increased 175% from 2023 to 2024 according to Forbes data, from $64.4 billion to $177 billion.

What Is the Difference Between Income and Wealth?

Capital Gains: Increases in Wealth

Households holding assets that have increased in value pay federal and state tax on those gains only when they sell those assets. This is known as a realized capital gain.

However, the value of an asset can grow exponentially and go untaxed as long as it is held onto — an unrealized capital gain. While the household doesn’t directly receive the proceeds from the gain until selling the asset, unrealized capital gains represent an increase in the household’s wealth and financial well-being.

For ultra-wealthy households, unrealized capital gains make up a large share of their total wealth.5For example, the Institute on Taxation and Economic Policy estimated that unrealized capital gains represent nearly 70% of total wealth for billionaires. In some cases, ultra-wealthy households — such as corporate founders — can avoid paying income taxes entirely in some years by not taking a salary, not selling any stocks or other assets, and simply borrowing against their wealth to pay their bills. There is evidence of some of the wealthiest Americans engaging in this behavior, detailed in analyses of leaked tax returns by investigative journalists,although recent research suggests that this is not a widespread phenomenon and that overall, wealthy households do have significant taxable income and their incomes allow them to cover their expenses while continuing to invest and grow their wealth.

Additionally, if someone holds onto assets until their death, their heirs do not have to pay any tax on the gain due to a provision in both federal and state law known as “stepped-up basis,” estimated to cost California around $5 billion each year.6Department of Finance, Tax Expenditure Report: 2025-26, p. 24. Note that the estimated annual cost of the provision is not equivalent to the revenue that could be generated from repealing it, and for this provision the revenue gains from repeal would start in the low hundreds of millions and increase with time, potentially reaching $5 billion annually in the future. Essentially, the combination of unrealized capital gains not being taxed and stepped-up basis results in some large wealth increases never being taxed.

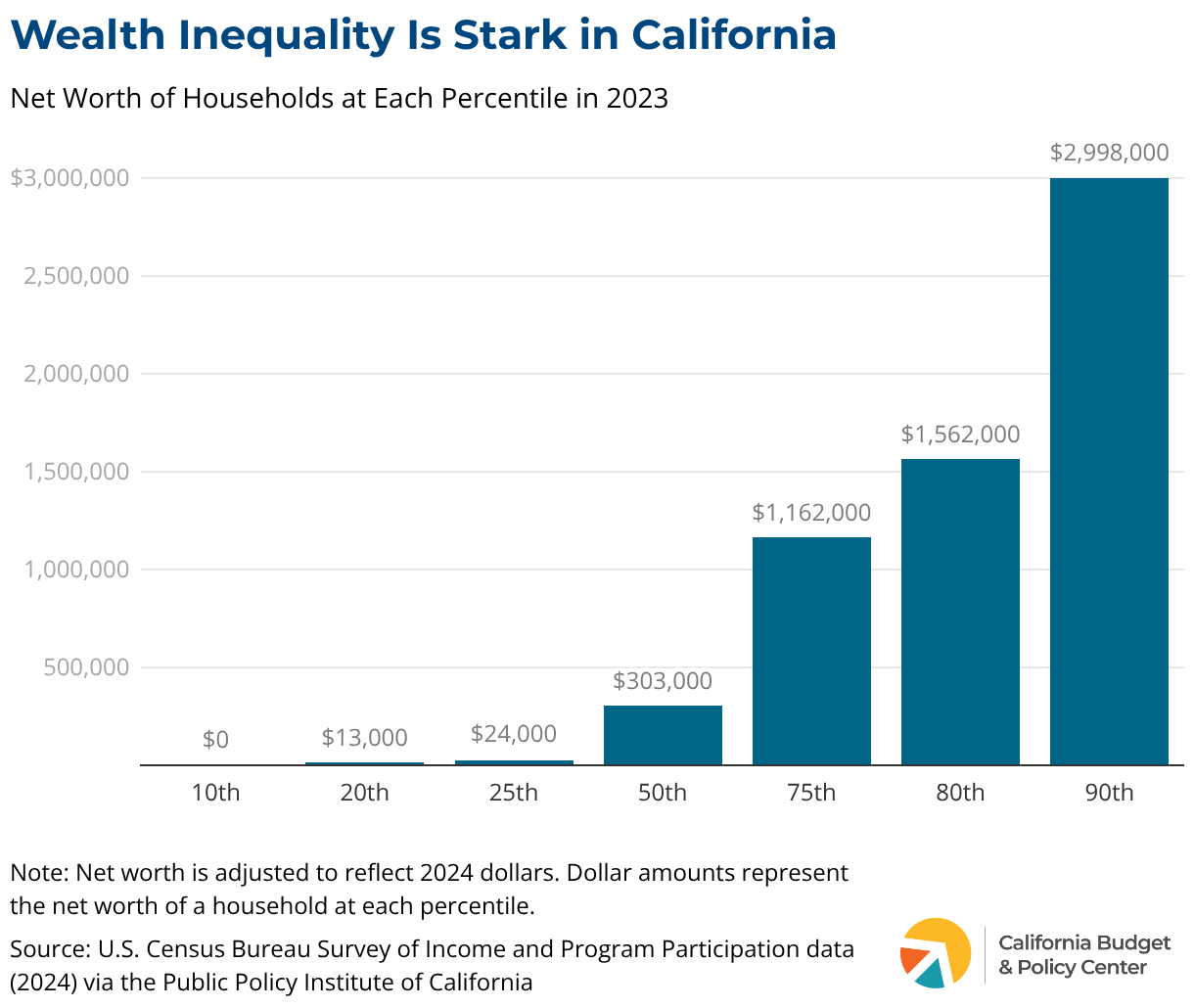

How Is Wealth Distributed Across California?

Across the country, the gaps in income and wealth have steadily grown with the top 10% of households seeing substantial growth in both income and wealth accumulation. Similarly, in California, only a tiny fraction of the population benefits from extreme income and wealth.

When focusing on the wealth distribution in the state, the data show an alarming gap between households with high and low wealth. Specifically, the wealthiest 20% of households have a net worth of over $1.5 million, while the bottom 20% of households have a net worth of $13,000 or less. Those who would be subject to the Prop. 40 tax — those with a net worth above $1 billion — have a net worth of over 3,000 times the median household.

Wealth is also unequally distributed across racial and ethnic groups. For example, the median net worth of white households in 2023 was almost ten times the median net worth of Latinx households, reflecting the historical barriers to wealth accumulation these communities have faced. Black, Latinx, and other households of color often have less wealth due to many factors including a lower likelihood of owning stocks, occupational segregation pushing them into lower-payer jobs, and a lack of inherited generational wealth. These factors likely contribute to the large wealth disparities that have persisted throughout history.

How Much Revenue Will Prop. 40 Raise?

There is a high degree of uncertainty in estimating the potential revenue from this measure since it is impossible to accurately predict how billionaires and the courts will respond to the tax. It is likely there will be some avoidance and evasion of the tax, as billionaires may hide or underreport their assets, shift their asset holdings toward those that are exempt from the tax, attempt to sever their ties with California, or engage in other tactics to minimize or eliminate their tax liability.

After attempting to account for these factors, the Legislative Analyst’s Office estimates that the billionaire tax would likely raise “tens of billions” of dollars in the near term. It also suggests there could be some ongoing reductions in state income tax collections in the future — likely less than $1 billion per year — depending on the extent to which billionaires leave the state and no longer pay California tax on their income.

Authors of Prop. 40 estimate that the measure could raise around $100 billion over five years, after assuming that 10% of the potential tax base would be eroded due to avoidance and evasion. They assume a relatively low avoidance and evasion rate due to the one-time nature of the tax and its retroactive residency date as well as the inclusion of provisions in the measure intended to safeguard against the avoidance and evasion strategies seen with wealth taxes implemented in other countries, such as allowing fewer exemptions for certain asset types and applying the tax to trusts as well as individuals.

The large difference between estimates lies mainly in different assumptions about how many billionaires have or will successfully sever their residency ties with California to avoid the tax. The potential for migration and other avoidance efforts related to the measure and their implications are discussed below.

What Would Prop. 40 Funds Pay For?

All the revenue from the Billionaire Tax Act is intended to mitigate the harm from federal and state-level cuts to health care, food assistance, and K-14 public education programs. The measure would create a special fund — the 2026 Billionaire Tax Reserve Fund — to hold the revenue.

Revenues in the fund — after accounting for the costs incurred by the Franchise Tax Board to administer the tax — would be split between two subaccounts, with 90% of revenue going into the Billionaire Tax Health Account and 10% going into the Billionaire Tax Education and Food Assistance Account.

Dollars in the Billionaire Tax Health Account would support health care funding, which could include but is not limited to:

Restoring or addressing any reductions in federal or state funding to health care programs;

Protecting and expanding Medi-Cal and other health coverage programs for low- and moderate-income Californians;

Supporting safety net health care providers serving vulnerable populations; and

Other investments relating to health care access, coverage, benefits, funding, services, and payments to providers.

Dollars in the Billionaire Tax Education and Food Assistance Account would support funding for K-14 and food assistance programs, which could include but is not limited to:

Restoring or addressing any reductions in federal or state funding to public education and food assistance programs;

Making investments to preserve or expand the K-14 education system; and

Expanding food programs like CalFresh, the California Food Assistance Program, CalFood, and the California Universal Meals Program.

Because the measure does not contain specific requirements as to how the dollars within each fund must be spent, beyond being used for “health care funding” and “education-related and food assistance expenditures,” policymakers would have fairly broad authority to determine the allocation of funding within those categories. However, the measure specifies that funds may not be used to replace existing state funds for health care, education, or food assistance.

Additionally, each subaccount has a limit for how much can be appropriated in a fiscal year. The health subaccount has an appropriation limit of $22.5 billion per fiscal year, and the education and food assistance account has a limit of $2.5 billion per fiscal year. The entire amount does not have to be allocated each year and funds can be retained if determined necessary.

Prop. 40 specifies that the revenue generated by the billionaire tax would be excluded from three spending requirements in the state Constitution:

the state spending cap (Prop. 4, the “Gann Limit”), which restricts the usage of revenues above a certain level, based on spending in 1978-79 adjusted for changes in population and income.

How Would Prop. 40 Revenues Impact Californians?

The majority of the revenues from the Billionaire Tax Act would directly support Californians who are harmed by federal and state cuts to the Medi-Cal and CalFresh programs.

H.R.1 is estimated to result in around 1.3 million Californians losing Medi-Cal coverage by 2029-30 and tens of billions of dollars in lost federal funding every year. These provisions target a wide range of populations including, but not limited to, immigrant Californians and low-income adults without dependents. Policy changes impacting these populations include increasing eligibility checks for Medi-Cal, imposing ineffective work reporting requirements, and limiting retroactive coverage for adults. Federal policy changes, including provisions of H.R. 1 and the expiration of enhanced premium tax credits, could also result in around 400,000 to 500,000 fewer Californians receiving health coverage through Covered California — the state’s health insurance marketplace established through the Affordable Care Act. The revenue from Prop. 40 could help mitigate some of the harms of these federal policies, for instance by replacing some lost federal funding and providing counties with additional resources to administer Medi-Cal and help eligible Californians maintain coverage.

This measure could also allocate funding to counteract the harmful enacted provisions from recent state budget packages that further harm Medi-Cal recipients. In combination with the federal cuts, state policy changes like freezing Medi-Cal enrollment for certain undocumented adults, imposing burdensome monthly premiums, reinstating the Medi-Cal asset limit, and denying full-scope Medi-Cal to certain immigrants could nearly double the uninsured rate to 14.7% by 2030.

A smaller proportion of the revenue could also go towards offsetting H.R.1’s harmful cuts to CalFresh. H.R.1 puts more than 3 million households at risk of losing some or all of their food assistance and could cost California between $2.3 billion and $5.1 billion annually. The provisions include applying time limits to previously exempt populations like veterans, older adults, and former foster youth and eliminating CalFresh for tens of thousands of lawfully present immigrants.

The Prop. 40 revenues could also help sustain and support funding for public education which has been facing federal threats such as funding freezes, grant cancellations, and proposed budget cuts. Public education would receive less support under the measure than if the revenues were allocated to the General Fund — due to the Prop. 98 minimum funding guarantee — but that would also mean less funding available for health care and food assistance. Additionally, because the measure does not require any specific share of funding in the Billionaire Tax Education and Food Assistance Account to go to any of the specified allowable uses, it is possible that all of these funds would be used to support food assistance and none for education — or alternatively, all of the funds could go to education and none to food assistance. Again, policymakers would have significant flexibility in allocating the dollars in this fund to specific programs that align with the intended purposes of the fund.

What Are the Concerns About Prop. 40?

Prop. 40 Would Provide One-Time Revenues to Respond to Ongoing Federal Funding Losses

While the revenue that would be generated by Prop. 40 is mainly intended to address the harms of the federal cuts to health care and food assistance resulting from H.R. 1 and other federal threats, the revenue from this one-time tax would only be available for a few years. If the federal government does not reverse those deep cuts within the next several years, the state will again be presented with the choice of cutting services and letting Californians impacted by federal cuts fall through the cracks or finding new alternative revenue sources to help keep them afloat.

The Revenue from Prop. 40 Would Not Be Available to Support Other Core State Services

Because the revenue would be earmarked, state programs and services that help Californians — beyond health care, food assistance, and education — would not receive any of the one-time revenue under Prop. 40. For example, none of the revenue would be available to support other critical needs such as affordable housing and renter supports, homelessness response, subsidized child care, or other safety net programs. As noted above, because the measure does not specify how the funds in the Education and Food Assistance Account would be allocated, it is possible that the funds could be used only for food assistance or only for education, so there is no guarantee that funding is allocated for both of these purposes.

On one hand, there is a clear need for increased health care funding to respond to the dramatic federal cuts that could strip millions of Californians of their health insurance and put immense strain on health clinics and hospitals, particularly in rural areas. This need supports the rationale for dedicating the vast majority of the revenue to health care programs.

On the other hand, Californians facing barriers to economic security have many critical needs, and the state has long underinvested in meeting those needs. New revenues are essential to protect and expand vital state services — including services beyond what Prop. 40 revenues are allowed to fund. If the revenues from a new tax on wealth went into the state’s General Fund, policymakers would have the flexibility to deliberate and decide how to allocate funding to address the most pressing and changing needs of Californians.

There Are Uncertain Impacts of a State-Level Wealth Tax on the State’s Longer-Term Budget and Economy

Imposing a state tax on wealth for a small share of the population is a novel and untested approach in the United States, and novel approaches always come with some risks. Concerns have often been raised about the potential impacts of such a tax on the behavior of the ultra-wealthy: the extent to which they will engage in tax avoidance behaviors that have consequences for the state. The majority of these concerns focus on the risk that billionaires will leave the state to avoid the tax, which would lead to some loss of future income tax revenues from those households if they do not return later. A related concern often raised is how these potential migration impacts could affect the state’s economy if wealthy business founders/owners choose to relocate some of their business activities or if future company founders opt to start businesses in another state for fear of a future wealth tax.

While a significant outmigration of billionaires could reduce the one-time revenue yield from the billionaire tax, the bigger concern for the state is the potential impact on ongoing state income tax revenues, which could put a strain on the state budget in the future. The outcome here is also uncertain. The income taxes paid by billionaires are very small relative to their overall wealth, and some billionaires can essentially avoid income taxes entirely in some years by not selling any assets or receiving a salary. For example, researchers — including an author of Prop. 40 — examined public data reported to the US Securities and Exchange Commission and found that Google founders Larry Page and Sergey Brin did not sell stock, receive dividends, or take any compensation related to Alphabet (Google’s parent company) in 2019, 2020, or 2023, so they likely would not have paid any income taxes related to their Alphabet holdings or involvement. Additionally, it is not clear that migration and income tax losses would be permanent in response to a one-time tax.

Prop. 40 aims to address the potential concerns about migration by applying the wealth tax to billionaires who were California residents as of January 1, 2026. This retroactive residency date is likely to be challenged in court. However, if it is upheld, any billionaire leaving after this date would not be able to avoid the tax. Additionally, even billionaires who announced moves out of California before this date may not have sufficiently severed their residency with the state for tax purposes, as the state’s Franchise Tax Board considers many factors when verifying residency status beyond simply whether a filer claims to be resident of another state or has purchased property in another state.

There is no way to accurately predict how billionaires would respond to the tax — or the prospect of being subject to the tax, as there is uncertainty about whether the measure will be approved by voters and whether the retroactive residency date will be upheld. There is a body of research on how income and wealth tax policies may impact interstate and international mobility of taxpayers, but the findings vary widely depending on the geographical scope, the type and magnitude of the tax change, the population impacted, the data available, and the research methodology.7For a summary of research focused on the mobility of high-income and high-wealth households in response to income and wealth taxes, see Fernando Rodrigo Sauco, “Millionaires on the Run? Taxation of the Rich and Induced Mobility: A Literature Review,” Hacienda Pública Española/Review of Public Economics 253, no. 2 (June 2025): 91-127.

Research on the impacts of state-level income taxes on interstate migration has generally found very minor effects on the numbers of high-income people in a state relative to the state’s total population of high-income people.8While some studies have found statistically significant effects of taxes on migration rates among high-income tax filers, this translates to small changes in the stock of high-income people in a state. For example, Young et al. (2016) examined federal tax return data for all tax filers with incomes of at least $1 million across all states for 1999 to 2011 and estimated that a one percentage point increase in the income tax rates is associated with an 8% reduction in the net migration flows into the state — people moving in minus people moving out — but this only translates to only a 0.1% change in the population of millionaires. They also find that while millionaires are somewhat more sensitive to tax rates than the general population, they are also less likely to move between states overall. Rauh and Shyu (2024) examined the impacts of California’s income tax increases on high-income households enacted by Prop. 30 (2012) and estimated that the the tax increase was associated with a one-time increase in the outmigration rate of top-tax bracket filers of 0.8% — translating to around 535 out of the nearly 67,000 tax filers in the new top tax bracket. Notably, since the enactment of these top tax rates established by Prop. 30 and extended by Prop. 55 (2016), the numbers of tax filers with incomes placing them in these top tax brackets has grown significantly, along with the incomes of this group and the state revenue collections from the top rates. Additionally, there is evidence that state differences in tax rates have more significant effects on the choice of location among movers than on the probability of moving. For example, a study by Young and Lurie (2025) suggests millionaires in higher-tax states were no more likely to move than the general public in response to a 2017 federal tax change that impacted higher-income taxpayers in higher-tax states, but those that did move were more likely to move to lower-tax states. While taxes may be one factor in where people decide to live, they are one of many, and they may not outweigh other factors such as professional and family considerations, public amenities, weather, and lifestyle preferences. Indeed, survey data from the US Census Bureau show that the vast majority of people moving between states move for job or family reasons. Some research also finds that high-income people are generally less likely to move between states than the general population and are more embedded in their communities due to family, social, and business connections — they are more likely to be married, have children, and own businesses.9Young and Lurie (2025) did find an elevated migration of millionaires out of higher-tax states during the COVID pandemic when in-person social and business networks were disrupted, but this effect had generally subsided by the beginning of 2023.

However, the impact of a wealth tax on California billionaires may be different than the impact of income taxes on high-income households. There are no direct parallels to draw on, as no state has enacted this type of tax, and most wealth taxes in other countries have been imposed at the national level and applied to a broader segment of the population. These other wealth taxes have had substantial differences in design — including the tax rates, exemptions for specific types of assets, and the wealth thresholds above which the tax applies — as well as enforcement capacity. All of these factors can influence the impact of the tax, so the findings on migration and other avoidance behaviors are not uniform across studies of different wealth taxes and may not be directly relevant to the potential impact of a California billionaire tax.

Several countries, mainly in Europe, have levied taxes on their residents’ net worth in the past, but most have since repealed them. Among high-income countries — members of the Organization for Economic Cooperation and Development (OECD) — four currently impose taxes on wealth: Colombia, Norway, Spain, and Switzerland. This is down from 12 OECD countries with wealth taxes in 1990. A few other countries still have fairly comprehensive taxes on wealth — including Argentina (althougFor example, the Spain wealth tax study did find higher responses for people in higher wealth tax brackets, and a study on the impact of state-level estate taxes — essentially a one-time wealth tax levied when someone dies — on the state residence of US billionaires in the Forbes 400 found this population to be quite sensitive to the presence of an estate tax. However, this finding may not extend to a one-time wealth tax given that people are more likely to be mobile after retirement and may factor estate planning into their location decisions — and the estate tax study did find a stronger response for older billionaires.h this tax is being phased down), Bolivia, Uruguay — and additional countries including Belgium and Italy have taxes on the value of narrower categories of assets.10Washington State Department of Revenue, Wealth Tax Study Report(November 2024); PwC, Worldwide Tax Summaries: Net wealth/worth tax rates (Accessed July 6, 2026). Italy levies a 0.2% tax on foreign financial assets, and Belgium levies a 0.15% tax on securities accounts of at least 1 million euros.

Studies on wealth taxes in Spain and Switzerland — the only countries that have subnational wealth tax regimes instead of uniform national wealth taxes — found migration responses related to variation in tax rates between regions. The studies estimate that a one percentage point change in a wealth tax rate was associated with a change of around 8% to 10% in the population impacted by the tax. If billionaires in California had a similar response, a 5% wealth tax could result in substantial outmigration.

However, there are some caveats to extrapolating these findings — beyond the retroactive residency provision in Prop. 40 that may render billionaire outmigration after January 1, 2026 moot for the purpose of the tax. The subdivisions of Spain and Switzerland are much smaller than California, the taxes are ongoing instead of one-time, they are present across most or all regions of the countries, and they apply to a much broader population than billionaires — these factors could pull in opposite directions with regard to the applicability of these findings. It is also likely that some of the reported residence changes are fraudulent. Researchers found some suggestive evidence that false residency changes — such as a taxpayer claiming that a second home is their primary home — are responsible for some of the effect in Spain. The prevalence of this phenomenon could be limited with adequate enforcement.

There is a possibility that wealthier people are more likely to move in response to taxes, which would have implications for a tax specifically targeted to billionaires.

For example, the Spain wealth tax study did find higher responses for people in higher wealth tax brackets, and a study on the impact of state-level estate taxes — essentially a one-time wealth tax levied when someone dies — on the state residence of US billionaires in the Forbes 400 found this population to be quite sensitive to the presence of an estate tax.11Note that this finding is specific to the ultra-wealthy Forbes 400 group, so it cannot be generalized to a broader group of wealthy households. Previous research examining the effect of estate and inheritance taxes on state migration rates of older adults and the locations of wealthy older adults estimated insignificant or modest effects. However, this finding may not extend to a one-time wealth tax given that people are more likely to be mobile after retirement and may factor estate planning into their location decisions — and the estate tax study did find a stronger response for older billionaires.

There is limited research on the overall economic impacts of wealth taxes. One recent study on now-repealed national-level wealth taxes in Sweden and Denmark — looking at the effects of tax reductions and repeals — estimated that a one percentage point increase in top wealth tax rates decreases the number of wealthy taxpayers in the country by about 2%, and because the wealthy are disproportionately business owners, there are some broader economic impacts. However, the estimated effects were very modest, as a large portion of business activity lost due to the outmigration of business owners is absorbed by other remaining businesses. Again, the differences in geography, nature of the tax changes studied (tax cuts versus tax increases), and the fact that these were recurring rather than one-time taxes mean that these findings may not be generalizable to a one-time state-level tax.

Research on one-time or temporary wealth taxes is limited. Several countries in Europe enacted national-level, short-term wealth taxes in the wake of WWI and WWII, and some levied narrow temporary taxes targeting wealth holdings after the Great Recession, with varying levels of success depending on the circumstances. The vast differences in historical context, geographic focus, and design elements — such as tax rates, payment periods, exemption levels, and assets targeted — make these experiences not particularly relevant comparisons for the Prop. 40 proposal, and there has not been empirical research on the migration or general economic impacts of these temporary taxes.

In sum, although existing research can provide some insights into the potential impacts of a one-time California billionaire wealth tax, there are many unknowns given the unique nature of the proposal. Additionally, the findings from research on tax policy impacts may not always identify causality or precisely measure effects due to the many potential confounding factors. Finally, even if effects are precisely measured, the research attempts to isolate the effects of tax policies holding all else equal, when in the real world there are a variety of factors influencing location decisions beyond taxes. Ultimately, California voters will need to decide if the benefits of the revenue generated by a tax on billionaires outweigh the concerns about the uncertain future fiscal and economic effects.

Which Other Measures on the November Ballot Conflict with Prop. 40?

Two other constitutional amendment measures appearing on the November ballot, Prop. 41 and Prop. 42, contain provisions that conflict with Prop. 40 and could invalidate it in part or in full if they receive more votes. These measures could also make it harder to raise state revenues in the future to invest in the well-being of Californians, which could result in cuts to essential services that Californians want and need.

Proposition 41

Prop. 41 would:

Require the State Auditor to conduct audits of programs that would receive revenue from new or higher special taxes, which are taxes that are dedicated to specific purposes rather than going into the state’s General Fund. This would include ongoing audits — every four years — of programs receiving funds from special taxes enacted on January 1, 2026 or later by either the Legislature or state voters. Additionally, pre-election audits would be required for programs that would receive revenues from a new or increased special tax that would appear on the statewide ballot. The pre-ballot and ongoing audits would be required to, among other things, contain recommendations on how the programs could reduce its costs by at least 10% annually. Policymakers would be under no obligation to implement these recommendations, but if they did, it could result in cuts to core services rather than simply “inefficient spending.”

Prohibit revenues raised by special taxes enacted since January 1, 2026 from being excluded from the state’s spending cap, also known as the “Gann Limit.” The measure also specifies that if another measure on the same ballot imposes a tax and exempts its revenues from the Gann Limit, the entirety of the other measure would be invalidated if Prop. 41 receives more votes. However, this would not prevent voters from approving future amendments to the state Constitution that would exclude certain tax revenues from the Gann Limit.

Because Prop. 40 would exclude the revenue generated by the billionaire tax from the Gann Limit, this is in direct conflict with Prop. 41. If both measures are approved, but Prop. 41 receives more votes, Prop. 40 could be invalidated. Alternatively, if both measures pass but Prop. 40 receives more votes, the billionaire tax could be collected, but it is possible that audits would be required of Medi-Cal and other programs receiving Prop. 40 dollars. If both measures pass, there may be litigation regarding the application of conflicting provisions, and the final decision would be made by the courts.

Proposition 42

Prop. 42 would:

Prohibit the imposition of any new tax on the ownership of financial assets (such as bank accounts, stocks, bonds, or mutual funds), retirement accounts, interests in businesses, intellectual property, and other personal property (such as vehicles, jewelry, artwork, and other movable, physical property). Essentially, this would limit the taxation of assets to real estate assets, which are already subject to constitutional tax limitations under Prop. 13. However, if this measure is passed, it would not prevent voters from amending the state Constitution to tax any of these assets in the future, but state policymakers would not be able to enact taxes on any of the assets covered by Prop. 42 without voter approval.

Prohibit the imposition of new retroactive taxes, and in particular taxes based on residency prior to the effective date of the new tax — except in cases where the revenues would be used to respond to a governor-declared emergency and the tax does not apply retroactively for more than one year before the effective date. Once again, the approval of Prop. 42 would not impact the ability of voters to approve retroactive taxes in the future, but would impact state policymakers’ ability to do so. As noted above, many tax laws do have limited retroactivity periods — such as dating back to the beginning of a tax year — for several reasons, including preventing tax avoidance.

Both of these provisions conflict with Prop. 40, as the billionaire tax would apply to financial assets, business interests, and other personal property, and it would be retroactively based on the taxpayer’s residence as of January 1, 2026. If both measures pass and Prop. 42 receives more votes, Prop. 40 could be invalidated. If Prop. 40 receives more votes, the wealth tax could be collected, but Prop. 42’s tax restrictions would likely apply to future legislative tax proposals. Again, conflicts may ultimately be decided in courts if both measures pass.

The Bottom Line on Prop. 40

Prop. 40 is a bold proposal that would create a first-in-the-nation tax on wealth, raising significant — temporary — revenue by taxing the fortunes of California’s more than 250 billionaires. Proponents argue this unprecedented measure is needed to help offset deep federal cuts and protect health care, food assistance, and education for all Californians. Because a wealth tax is untested at a state level in the United States, it carries real uncertainty: courts may strike down the measure or portions of it, conflicting measures could lead to years of litigation, and no one can say how the location decisions of billionaires might change and what that would mean for California’s long-term finances.

California voters will need to decide if the benefits of the revenue generated by a tax on billionaires outweigh the concerns about the uncertain future fiscal and economic effects of the billionaires tax.

Prop. 40 Supporters and Opponents

Prop. 40 is sponsored by Service Employees International Union — United Healthcare Workers West (SEIU-UHW), a local union representing health care workers. It has been endorsed by labor organizations including AFSCME California and Teamsters California, organizations including Our Revolution and California Democratic Socialists of America, and policymakers including US Senator Bernie Sanders, US Representative Ro Khanna, and State Superintendent of Public Instruction and former gubernatorial candidate Tony Thurmond.

Prop. 40 is opposed by labor organizations including the California Teachers Association and the State Building and Construction Trades Council of California, organizations including the California Business Roundtable, the California Medical Association, Planned Parenthood Affiliates of California, policymakers including Governor Gavin Newsom and US Representative Kevin Kiley, and gubernatorial candidates Xavier Becerra and Steve Hilton.

The California Budget & Policy Center is a nonpartisan research and analysis nonprofit and does not endorse or oppose ballot measures. This analysis reflects the institutional position of the Budget Center, developed and reviewed by our policy leadership team.

Kayla Kitson and Nishi Nair contributed to this publication.

Forbes tracks the daily wealth of billionaires with its “Real-Time Billionaires” list, and the California-specific data was compiled in connection with Jasper Boll, Emmanuel Saez, and Gabriel Zucman, California Billionaires: Wealth, Taxes, and Wealth Tax Revenue Estimates (NBER Working Paper 35218, May 2026). Note: Saez is an author of Prop. 40.

2

Specifically, the 5% rate would be reduced by 0.1 percentage point for each $2 million that the household’s net worth falls below $1.1 billion.

3

Tangible personal property is excluded from the net worth calculation if it is held outside of California for at least 270 days during 2026 unless it was temporarily relocated for the purpose of tax avoidance.

4

Tax avoidance reflects legal avenues to reducing tax liability, such as redirecting wealth holdings to exempted assets or relocating, whereas tax evasion encompasses illegal tactics to avoid taxes, such as hiding assets in tax havens, underreporting of asset values, or falsely claiming residency outside of the tax jurisdiction.

Department of Finance, Tax Expenditure Report: 2025-26, p. 24. Note that the estimated annual cost of the provision is not equivalent to the revenue that could be generated from repealing it, and for this provision the revenue gains from repeal would start in the low hundreds of millions and increase with time, potentially reaching $5 billion annually in the future.

While some studies have found statistically significant effects of taxes on migration rates among high-income tax filers, this translates to small changes in the stock of high-income people in a state. For example, Young et al. (2016) examined federal tax return data for all tax filers with incomes of at least $1 million across all states for 1999 to 2011 and estimated that a one percentage point increase in the income tax rates is associated with an 8% reduction in the net migration flows into the state — people moving in minus people moving out — but this only translates to only a 0.1% change in the population of millionaires. They also find that while millionaires are somewhat more sensitive to tax rates than the general population, they are also less likely to move between states overall. Rauh and Shyu (2024) examined the impacts of California’s income tax increases on high-income households enacted by Prop. 30 (2012) and estimated that the the tax increase was associated with a one-time increase in the outmigration rate of top-tax bracket filers of 0.8% — translating to around 535 out of the nearly 67,000 tax filers in the new top tax bracket. Notably, since the enactment of these top tax rates established by Prop. 30 and extended by Prop. 55 (2016), the numbers of tax filers with incomes placing them in these top tax brackets has grown significantly, along with the incomes of this group and the state revenue collections from the top rates. Additionally, there is evidence that state differences in tax rates have more significant effects on the choice of location among movers than on the probability of moving. For example, a study by Young and Lurie (2025) suggests millionaires in higher-tax states were no more likely to move than the general public in response to a 2017 federal tax change that impacted higher-income taxpayers in higher-tax states, but those that did move were more likely to move to lower-tax states.

9

Young and Lurie (2025) did find an elevated migration of millionaires out of higher-tax states during the COVID pandemic when in-person social and business networks were disrupted, but this effect had generally subsided by the beginning of 2023.

10

Washington State Department of Revenue, Wealth Tax Study Report(November 2024); PwC, Worldwide Tax Summaries: Net wealth/worth tax rates (Accessed July 6, 2026). Italy levies a 0.2% tax on foreign financial assets, and Belgium levies a 0.15% tax on securities accounts of at least 1 million euros.

11

Note that this finding is specific to the ultra-wealthy Forbes 400 group, so it cannot be generalized to a broader group of wealthy households. Previous research examining the effect of estate and inheritance taxes on state migration rates of older adults and the locations of wealthy older adults estimated insignificant or modest effects.

You may also be interested in the following resources:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

Proposition 37 on the November 2026 ballot would establish a “middle-class” homebuyer downpayment assistance program, funded with up to $25 billion in revenue bonds. This assistance could only be used to purchase newly built homes or newly created housing units converted from nonresidential buildings, where the buyer is the first purchaser. The program is intended to be self-sustaining because participating homebuyers — not the state — would ultimately repay the bonds through their mortgage payments.

Supporting homeownership is an important strategy for promoting economic security and wealth building. However, it is unclear whether Prop. 37 would meaningfully help “middle class” Californians who face the greatest barriers to homeownership to afford a home.

As Prop. 37 would be financed through revenue bonds — which do not require voter approval — the program proposed by this initiative could have been enacted legislatively or a comparable program could have been established by the California Finance Housing Agency. Prop. 37 is a citizens’ initiative spearheaded by former California Senate Majority Leader and Assembly Speaker Bob Hertzberg.

What Would Prop. 37 Do?

The Middle Class Homeownership and Family Home Construction Act of 2026 would direct the California Housing Finance Agency (CalHFA) to establish a middle-class homebuyer downpayment assistance program, funded with up to $25 billion in revenue bonds. The new program would: Key components of the program include:

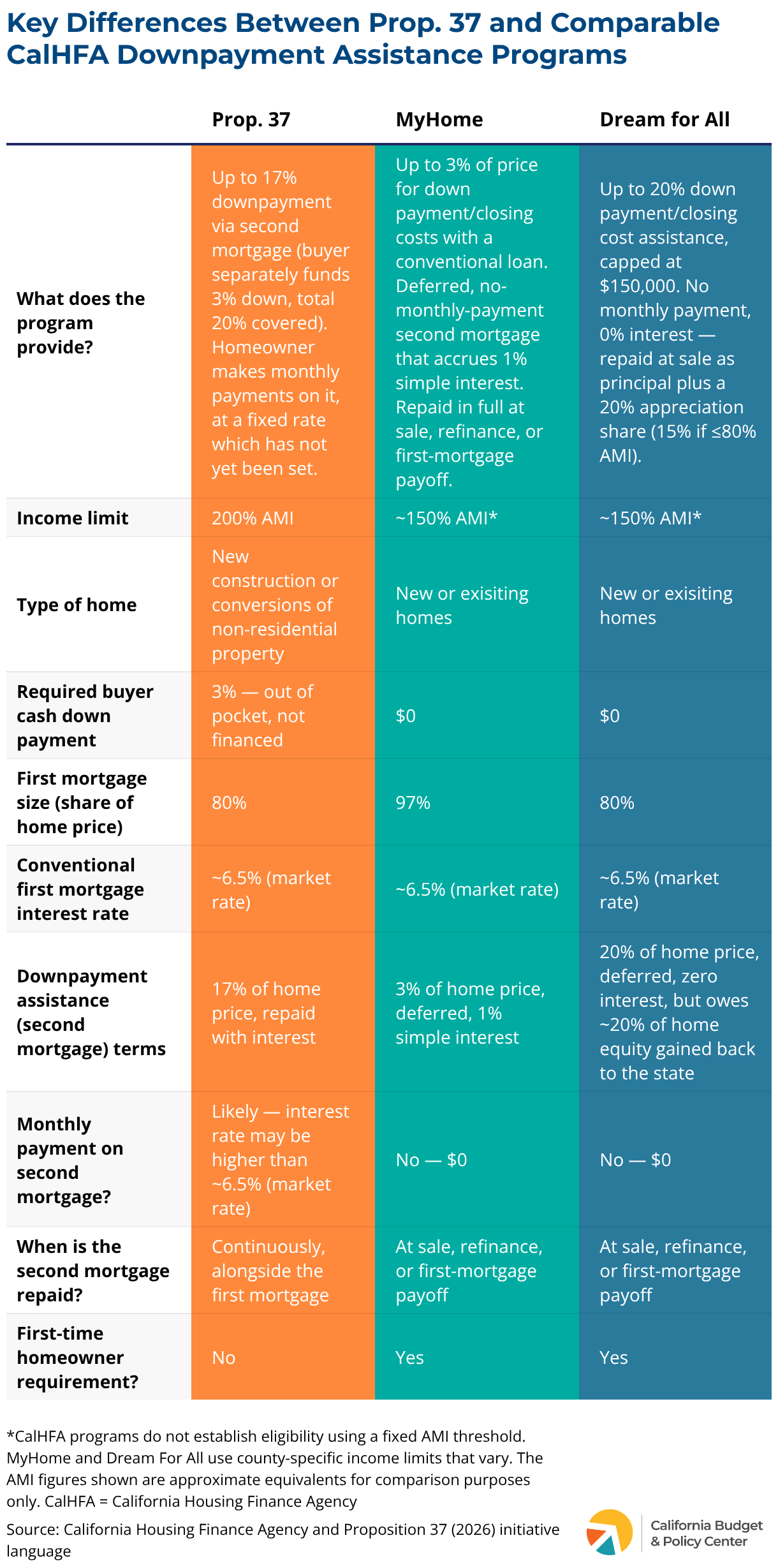

Provide up to 17% of the purchase price toward the down payment, which could only be used to purchase new homes or newly created housing units converted from nonresidential buildings, where the buyer is the first purchaser.

Require the buyer to put down at least 3% of the purchase price toward the down payment. Combined with the 17% state downpayment assistance, this would reach 20% of the home’s purchase price and eliminates the need for private mortgage insurance. A conventional first mortgage would cover the remaining amount.

Require the downpayment assistance to be provided as a loan, not a grant, which recipients are likely to pay back monthly as a fixed-rate second mortgage. This would be in addition to the homebuyer’s monthly payments on their conventional first mortgage.

Allow applicants to have incomes up to 200% of the Area Median Income (AMI), which varies by region.

Cap the maximum home purchase price at roughly $1 million to $1.5 million, depending on the county and other factors. This is equivalent to a $170,000-$255,000 downpayment assistance cap per home.

Not require applicants to be first-time or first-generation home buyers, nor would recipients owe the state any equity gained in their home. These are requirements of comparable state downpayment assistance programs the state currently operates.

Allow home builders to become “qualified builders,” and have their developments automatically qualify for the program if they meet specified labor and enforcement standards.

How Would Income Eligibility for Prop. 37’s Downpayment Assistance Vary Across California Counties?

Prop. 37 would make a broad group of Californians eligible for downpayment assistance by allowing family incomes not exceeding 200% of Area Median Income (AMI) to qualify, a threshold that extends well beyond established downpayment assistance programs.

AMI represents the midpoint of family incomes in a specific area, adjusted for household size. In other words, half of households in an area have incomes that exceed 100% AMI and half have incomes below that level, so 200% AMI is roughly double what a typical family makes in the area. The limit is tied to local incomes, so whether a family income would qualify for Prop. 37’s downpayment assistance would vary significantly across California.

For example, a Budget Center analysis of Census Bureau data shows that a family of four earning up to $166,800 annually in Madera County or up to $375,800 annually in Santa Clara County could each qualify for assistance. However, the final dollar amounts would be set by CalHFA if Prop. 37 is approved by voters.

How Is Prop. 37 Different from California’s Existing Downpayment Assistance Programs?

California operates several statewide homeownership programs through CalHFA, but Prop. 37 would take a different approach that could hit family budgets harder, as participants are likely to pay back the downpayment assistance monthly as a fixed-rate second mortgage.

For example, CalHFA’s MyHome Assistance Program and the Dream for All Shared Appreciation Loan program both provide downpayment assistance through deferred “silent second” loans (also known as silent second mortgages). MyHome charges 1% simple interest on the assistance; Dream for All accrues no interest, but requires a 15% or 20% share of the home’s appreciation to go to the state. Under both programs, nothing is due on these silent second mortgages until the homeowner sells, refinances, or pays off the first mortgage. This ensures that the downpayment assistance doesn’t compete with the first mortgage, groceries, utility bills, or other basic needs in a family’s monthly budget.

Prop. 37’s approach is likely to require monthly payments. This is because CalHFA would issue up to $25 billion in revenue bonds, and by law those bonds must be repaid from the proceeds of the program itself — meaning the principal and interest of the second mortgages CalHFA issues. The second mortgages would need to generate steady, ongoing revenue to pay the debt from the revenue bonds. Language in the measure also states “a borrower may request a temporary hardship deferral of monthly interest payments on its middle-class homeownership loan,” further alluding to its intended structure.

Curious About Other Ballot Propositions?

Browse our collection of resources covering California’s statewide ballot measures to help you understand what’s at stake for California this November.

Under Prop. 37, the second mortgage payment could also likely carry higher interest rates above conventional first mortgage rates. Although the measure states the intent to provide below-market downpayment assistance financing, it doesn’t guarantee it. The interest rate on the second mortgages would ultimately depend on the terms under which the bonds are issued and market conditions at the time of implementation, which are largely outside CalHFA’s control.

Revenue bonds that finance second mortgages are inherently riskier for investors because if a homeowner defaults, the first mortgage gets repaid before the second, leaving the bond investors more exposed to loss. Investors may therefore require a higher return to compensate for that additional risk, which could increase the interest rate on the second mortgage. This means Prop. 37’s second mortgage rate could land above the roughly 6.5% conventional first-mortgage rates buyers already face today. CalHFA wouldn’t set the actual rate or terms on the second mortgage until implementation, so the interest rate cannot be known before voters decide on Prop. 37.

Ultimately, while Prop. 37 could help get homebuyers to a 20% downpayment to avoid private mortgage insurance, the monthly repayment costs for the second mortgage could erode much of the benefit the downpayment assistance was meant to provide.

Would Prop. 37 Reach “Middle-Class” Californians Facing the Greatest Barriers to Homeownership?

Prop. 37 would make a broad range of households eligible for downpayment assistance, but income eligibility alone does not determine who can realistically purchase a home. Racial and ethnic disparities in income, wealth, credit access, and housing affordability mean that not all eligible families across California may be positioned to benefit from the program as proposed.

Prop. 37 would require the buyer to put down at least 3% of the purchase price, which would still be unattainable for many Californians. For example:

A house that costs $500,000 would require a 3% down payment of $15,000.

A house that costs $700,000 would require a 3% down payment of $21,000.

These upfront costs could be out of reach for many families, with the result that Prop. 37’s assistance could largely benefit families with incomes toward the higher end of the eligibility range. According to the Public Policy Institute of California, the median amount in Californians’ checking and savings accounts was just over $18,000 in 2025 dollars. This means that a 3% down payment could still almost or entirely clear out most or all of what an average family has in checkings and savings.

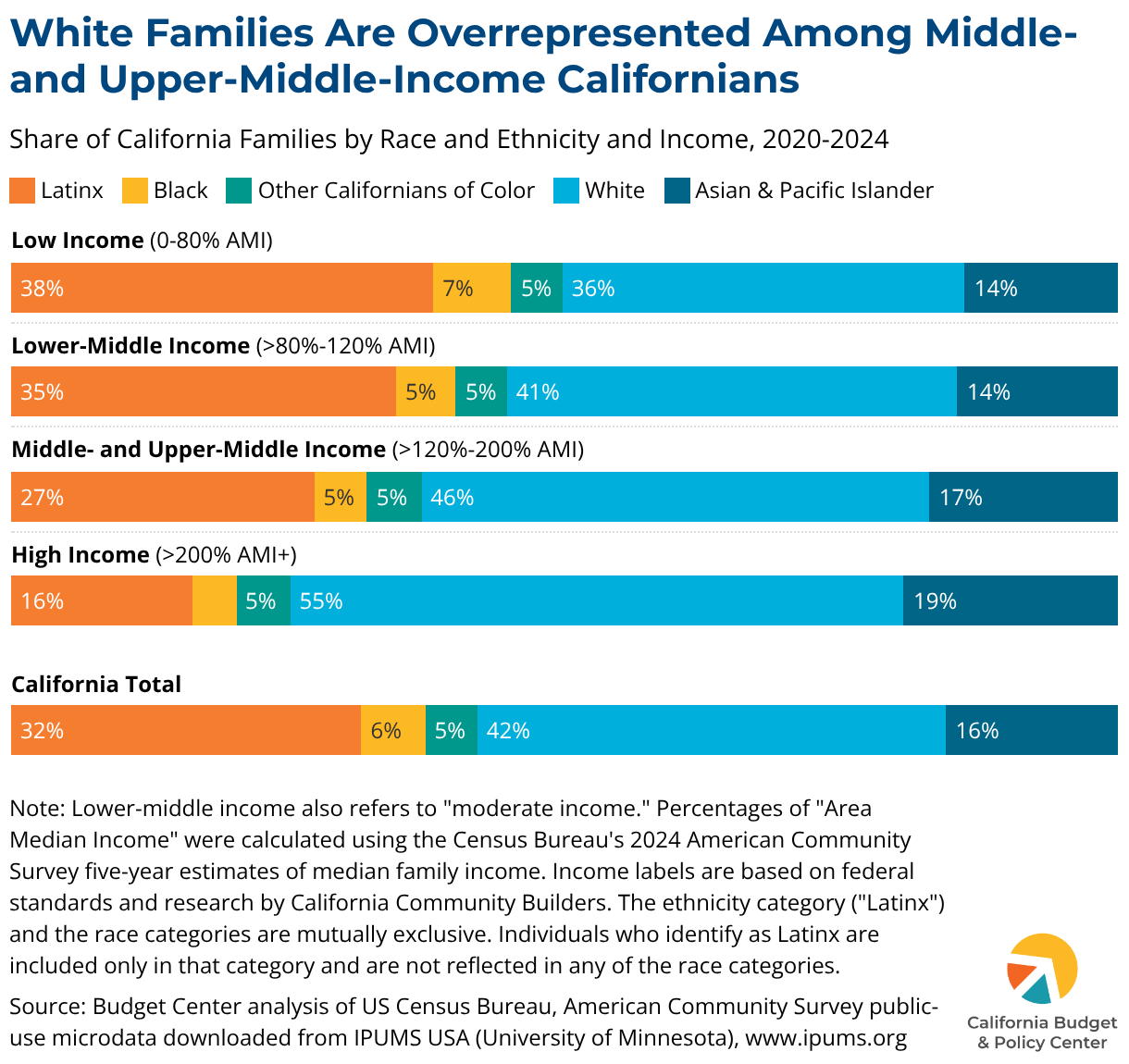

Prop. 37 could also reinforce economic, racial, and ethnic inequities in homeownership. The measure is intended to help “middle class” Californians, roughly defined as those with incomes between 80% to 200% AMI. White families are overrepresented among middle- and upper-middle-income Californians (46%), compared to their share of all California families (42%).

In contrast, Black and Latinx families are underrepresented in this “middle class” income range. This means that white families could disproportionately benefit from this program — even though white households already make up the largest share of homeowners in the state, while Black and Latinx renter households face disproportionately high housing costs.

Prop. 37 does not require applicants to be first-time or first-generation home buyers, further exacerbating equity concerns. Black and brown communities have been historically excluded from building wealth and accumulating assets, making the barrier to entering the housing market even more pronounced. Families of color face occupational segregation that pushes them into lower-paying jobs. They are also less likely to inherit generational wealth, and are more likely to be renters. These factors make it substantially more difficult to save for a down payment, even at similar income levels. Additionally, data limitations often mask significant disparities in homeownership access across racial and ethnic groups, especially among Asian American, Native Hawaiian, and Pacific Islander Californians.

Could Prop. 37 Encourage Sprawl and Harm the Environment?

By restricting downpayment assistance to newly built homes or newly created housing units converted from nonresidential buildings, Prop. 37 could push more “middle-class” housing onto land that’s not well suited for housing. Much of the land in California best suited for housing has already been developed, leaving remaining areas that are often far from job centers, prone to wildfire,environmentally sensitive, or important for agriculture.

While existing state down payment assistance programs are not immune to these concerns because they can also be used to purchase new homes, Prop. 37 goes further by limiting assistance exclusively to newly constructed homes. As a result, Prop. 37 could further direct “middle-class” housing demand toward suburban and exurban areas. This is a critical deviation from infill development — building on denser, already developed land — which has been the focus of state affordable housing and environmental efforts.

This pattern of building housing on the periphery of cities is known as urban sprawl and carries various environmental and equity considerations. Development in more suburban and inland areas can push Californians further from job centers, increasing their commute times and making it difficult to travel without a car. It may also encourage development in areas on the outskirts of cities that may cause new homes to infringe upon natural habitats and important agricultural lands, especially in areas like the Central Valley. Sprawl can also lead to divestment from urban areas, which are often composed of communities of color, and concentrate investment in higher-income, suburban neighborhoods, further exacerbating racial and income inequality across the state.

What Other Homeownership Costs Could Come with Prop. 37’s New-Construction Requirement?

Prop. 37’s new construction requirement could steer homebuyers toward housing with higher out-of-pocket costs on top of their monthly mortgage payments. Unlike existing state down payment assistance programs, which can be used to purchase both new and existing homes, Prop. 37 would limit assistance to newly constructed homes. New construction homes are more likely to come with homeowners association (HOA) dues, Mello-Roos assessments, and home insurance challenges.

HOA fees are far more common in new homes as nearly 70% of newly built homes listed for sale nationally in 2024 were subject to HOA dues, compared with about 38% of existing homes. In California, more than a third of residents live in an HOA — including about 65% of all California homeowners. The average monthly fee is $280, and fees can rise up to 20% annually without a homeowner vote under current state law.

New construction in undeveloped areas of California also often comes with Mello-Roos special tax assessments, which fund infrastructure like roads, schools, and utilities in newly developed areas and are layered on top of regular property taxes — typically adding another monthly fee to new-build homes for years.

California’s home insurance market also compounds the problem. Some state insurers have stopped providing coverage in many of the wildfire-prone areas where new homes are being built which has statewide ramifications. California’s state-run insurer of last resort, known as the FAIR Plan, is likely to be overburdened to the extent that more insurers drop coverage across the state.

While home insurance challenges are not unique to Prop. 37, they remain acute in the wildland-urban interface — where almost 45% of the houses built in California have been located over the last 30 years. Though these areas tend to have less expensive real estate, they are also particularly susceptible to wildfires. That exposure could mean higher premiums, more difficulty securing a loan, or dependence on the FAIR Plan, driving additional costs on top of the repayments of Prop. 37.

Altogether, these compounding factors could undercut the affordability gains the measure is purported to provide for Californians. As a result, the benefits of Prop. 37 may skew toward eligible families with greater financial resources who were already better positioned to cover the costs of homeownership.

Various carpentry-focused unions and realty organizations — like the California Association of Realtors and the Northern California Carpenters Regional Council — have also expressed support for the measure. Gubernatorial candidate Xavier Becerra has also expressed support for this measure.

The California Budget & Policy Center is a nonpartisan research and analysis nonprofit and does not endorse or oppose ballot measures. This analysis reflects the institutional position of the Budget Center, developed and reviewed by our policy leadership team.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

Proposition 1, appearing on the November 2026 ballot, would provide funding for affordable housing and accessible homeownership. Prop. 1 asks voters to authorize a $11.25 billion general obligation bond to fund programs that support the creation and preservation of affordable housing, expand homebuying opportunities for low- and moderate-income Californians and veterans, and invest in permanent solutions to solve homelessness. If Prop. 1 is approved, it would replenish funding for several successful state programs that have exhausted their resources. Prop. 1 was placed on the ballot by the Legislature through passage of Senate Bill 417 (2026).

How Has California Expanded Affordable Housing & What Gaps Remain?

Over the past six years, California has nearly tripled the number of new affordable homes it funds. Yet the state continues to face a severe shortage of affordable housing, particularly for Californians with the lowest incomes. California needs more than 2.5 million new homes, including at least 1 million homes that are affordable to lower-income households. Housing cost pressures fall hardest on California renters as nearly half pay unaffordable rents — a hardship that disproportionately impacts Black and Latinx renters with low incomes, older adults, mixed-status families, and people with disabilities.

Unlike market-rate or luxury housing, affordable housing projects typically cannot be built without subsidies because affordable rents do not generate enough revenue to cover development or operating costs. As a result, affordable housing projects rely on multiple funding streams to close financing gaps. Currently, more than 46,000 affordable homes across California (491 developments) are waiting for the last bit of state funding needed to break ground. Prop. 1 would provide funding for various programs that help bridge the financial gap to keep affordable housing construction moving.

Why Is Affordable Housing Funding Running Out & How Would Prop. 1 Help?

Despite the ongoing housing affordability challenges Californians are facing, state funding for affordable housing has largely disappeared. Over the past several years, affordable housing programs have relied on one-time General Fund investments to supplement voter-approved housing bonds, but those investments have drastically declined. The 2026 Budget Act only includes one-time investments in two significant affordable housing programs: $500 million for state Low Income Housing Tax Credits and $200 million for the Multifamily Housing Program, effectively leaving multiple programs without additional funds. Beyond these investments, there is no meaningful ongoing or one-time investment from the state General Fund for affordable housing development.

The state’s remaining modest affordable housing funding sources, including the Affordable Housing and Sustainable Communities Program (AHSC), funded through Cap-and-Invest; state and federal Low-Income Housing Tax Credits; and SB 2 planning funds are insufficient to meet the demand and often require additional funding to be fully leveraged. The AHSC program was expected to receive nearly $800 million per year for affordable housing, but recent changes by the California Air Resources Board put that funding at risk.

Curious About Other Ballot Propositions?

Browse our collection of resources covering California’s statewide ballot measures to help you understand what’s at stake for California this November.

The funding approved by voters through the 2018 Veterans and Affordable Housing Bond Act has been fully committed — exhausted within five years, by the end of 2023, due to overwhelming demand. The state’s flagship Multifamily Housing Program, which relied on funding from the bond and one-time General Fund investments, is routinely oversubscribed by roughly 9 to 1. Together these signal that the barrier to building more affordable housing in California isn’t a lack of will or projects — it’s a lack of sustainable funding.

Without new state investments, affordable housing production will stall just as California is making meaningful progress and as federal cuts threaten to make it even more difficult for Californians to make ends meet, which is why state lawmakers placed Prop. 1 on the ballot.

What Affordable Housing and Homeownership Programs Would Prop. 1 Fund?

Prop. 1 asks voters to authorize $11.25 billion in general obligation (GO) bonds that would support the construction and preservation of affordable rental homes, expand homeownership assistance for low- and moderate-income homebuyers, including veterans, and provide permanent housing for people at risk of or experiencing homelessness. Within these categories, it would provide some funding for programs that serve distinct populations, such as California tribes, farmworkers, unhoused youth, and college students. The bond funds would be allocated as follows:

Affordable Housing Development and Preservation

$5.1 billion for the Multifamily Housing Program (MHP), which supports the construction, rehabilitation, or preservation of affordable rental housing. At least 10% of units in a MHP development must be available for extremely low-income households who are at the highest risk of facing homelessness. This is one of California’s model affordable housing development programs.

$1.15 billion for supportive housing through the MHP program. Supportive housing provides stable homes with wrap-around services for people who were chronically homeless or at risk of becoming so. These funds can be used for operating subsidy reserves, which are critical to the longevity and sustainability of permanent supportive housing.

Up to 15% — $150 million — would be allocated as grants to acquire or build permanent supportive housing among other specified uses.

Another $150 million is carved out for the capital development or acquisition of youth housing through MHP. This would serve current or former foster youth, homeless minors or youth, or youth at risk of homelessness.

$750 million for the Portfolio Reinvestment Program, which provides funding to rehabilitate and extend the long-term affordability of state-funded rental multifamily housing projects that are at risk of conversion to market-rate housing.

$500 million for the Infill Infrastructure Grant Program. This would provide incentive grants to assist with new construction and rehabilitation of infrastructure that supports high-density affordable and mixed-income housing in locations designated as infill.

$450 million for the Joe Serna, Jr. Farmworker Housing Program to fund grants or loans for the construction or rehabilitation of housing for agricultural employees and their families.

$350 million for affordable student housing projects to be split evenly between the University of California and the California State University.

$200 million for a new Community Anti-Displacement and Preservation Program, which helps protect unsubsidized housing that may naturally be affordable and requires long-term affordability regulations.

$200 million for the Tribal Housing Grant Program which finances housing and housing-related activities to enable tribes to rebuild and reconstitute their communities.

$200 million to the Affordable Housing Innovation Fund for the Local Housing Trust Fund Matching Grant Program. This would fund competitive grants or loans to local housing trust funds that develop, own, lend, or invest in affordable housing and would be used to create pilot programs to demonstrate innovative approaches to creating or preserving affordable housing.

Homeownership

$1.25 billion for the CalVet Home Loan Programto help veterans and their families purchase homes. This portion of the bond would be repaid through mortgage (principal and interest) payments.

$600 million for the CalHome program. CalHome provides forgivable loans for lower-income households in self-help homeownership projects, including subdivisions and manufactured homes.

$500 million for the My Home downpayment assistance program to fund low-to-moderate income home purchase assistance programs.

What Benefits Would Prop. 1 Create for California’s Economy & Communities?

Prop. 1 would help expand and preserve California’s affordable housing supply while generating economic benefits and advancing the state’s housing goals. The bond would help close the financing gap for affordable rental homes, which serve lower-income California families and include seniors, people with disabilities, farmworkers, college students, and unhoused youth. According to legislative analyses, the bond is expected to:

Produce more than 40,000 new affordable homes for lower-income families and individuals.

Preserve more than 5,500 existing affordable homes, ensuring they remain affordable for future generations.

Create more than 53,000 construction jobs through building new housing across the state.

Generate $1.3 billion in state and local tax revenue that supports local communities and public services.

Together, these investments would expand housing opportunities, reduce housing instability, strengthen local economies, and help California meet its long-term housing needs.

How Would Prop. 1 Be Repaid?

Prop. 1 asks voters to authorize a total of $11.25 billion in GO bonds, divided as follows:

A $10 billion GO bond for affordable housing and homeownership programs that would be repaid from the state’s General Fund, and

A $1.25 billion veterans’ bond, a type of tax-exempt GO bond, for the CalVet Home Loan program that would be repaid through mortgage payments, with the General Fund as a backstop.

California voters often pass GO bonds to fund infrastructure projects that are designed to serve the public over many generations, as has been the case with affordable housing. Voters have also historically passed veterans’ bonds for CalVet to support homeownership opportunities for veterans.

GO bonds are repaid from the state’s General Fund. Repaying the $10 billion bond would cost $580 million per year for the next 30 years, for a total estimated cost of $17.4 billion ($10 billion in principal and $7.39 billion in interest). As of the governor’s proposed 2026-27 budget, California had $6.3 billion in General Fund debt service for GO bonds, or roughly 2.6% of General Fund expenditures.

In contrast, veterans bonds are generally self-supporting because they are repaid through principal and interest payments made by CalVet Home Loan Program borrowers. However, they are still GO bonds and are ultimately backed by the state’s General Fund. If program revenues were insufficient to cover the debt service, the General Fund would be responsible for the difference. It is unclear how often, if ever, the General Fund has had to backfill debt payments for previous veterans bonds.

Prop. 1 bond dollars would replenish depleted affordable housing programs. But bond dollars alone will not solve the housing shortage, nor would they replace the need for ongoing investments to meet the state’s substantial housing needs.

Prop. 1 and Prop. 38 Draw From Same Bonding Capacity, Face Important Trade Offs

Voters face two GO bond measures on the November 2026 ballot: Prop. 1 and Proposition 38. Prop. 38 would authorize $8.4 billion in GO bonds to support research and development in immunology and immunotherapy. Voters should weigh how each proposal addresses the state’s most pressing needs, fits within California’s limited borrowing capacity, and affects the state’s ability to invest in services that help families today and in the future.

Like all GO bonds, Prop. 38 would require long-term General Fund debt-service payments — estimated at $500 million annually for 25 years — reducing budget and bonding capacity for other state priorities. If both Prop. 1 and Prop. 38 are approved, it would reduce General Fund dollars by roughly $1.1 billion annually.

Public sector investment in scientific research is needed, particularly given federal cuts, but Prop. 38 raises important fiscal and policy considerations. GO bonds are conventionally used to finance infrastructure projects — like roads, bridges, or housing — that can be used over decades, roughly matching the time it takes to repay the bond itself.

Funding research through GO bonds does not work the same way. Bond-funded research gets most of the dollars upfront for grants, salaries, and operating costs, but are not guaranteed to be built into a lasting asset. Research findings do compound overtime, but the bond dollars themselves are depleted after a few years. The state then spends years or decades paying interest on bonds that stopped directly funding work long ago. So while scientific research needs funding, a GO bond is not the appropriate funding mechanism. Plus, half of Prop. 38’s funding would be concentrated on a limited set of health conditions, even though California already has multiple public and private research institutions conducting work in these areas.

Prop. 1 doesn’t confront these same challenges. While previous affordable housing bond dollars were also used up quickly, they left behind affordable homes that will continue to serve numerous families for decades. Affordable housing developments that use state dollars must have affordability requirements for at least 55 years — way beyond the repayment of the bonds with which they’re financed. The community benefits and capital assets outlast the debt, which is the intended purpose of GO bonds.

Prop. 1 Supporters and Opponents

Prop. 1 is supported by a broad coalition of organizations representing housing, business, labor, local government, older adults, tenants, homelessness, urban planning, construction, environmental, and civil rights interests, among others.

Official opposition has been limited. The primary opponents on record include a few Republican state legislators who voted against placing the measure on the ballot.

The California Budget & Policy Center is a nonpartisan research and analysis nonprofit and does not endorse or oppose ballot measures. This analysis reflects the institutional position of the Budget Center, developed and reviewed by our policy leadership team.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

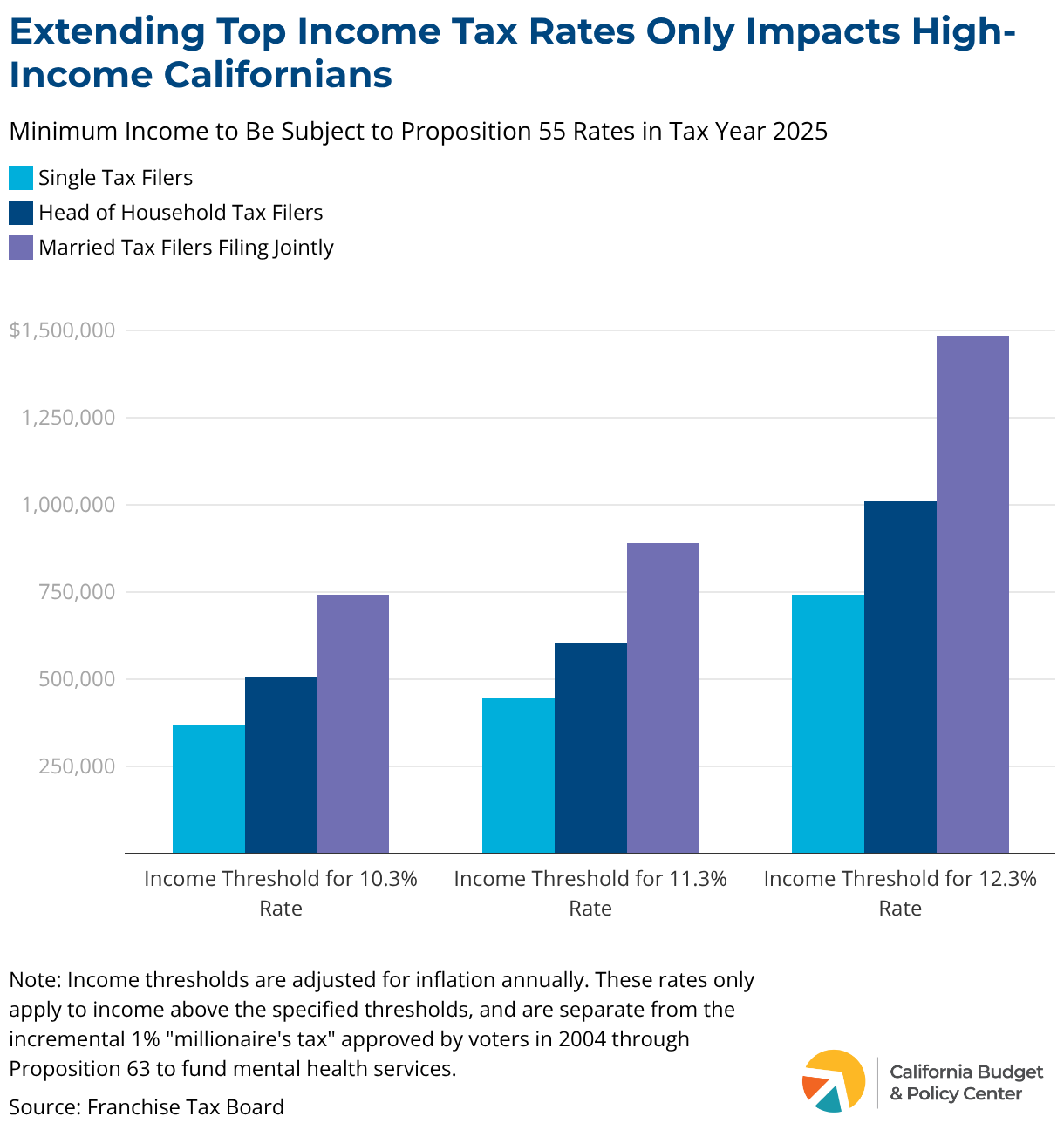

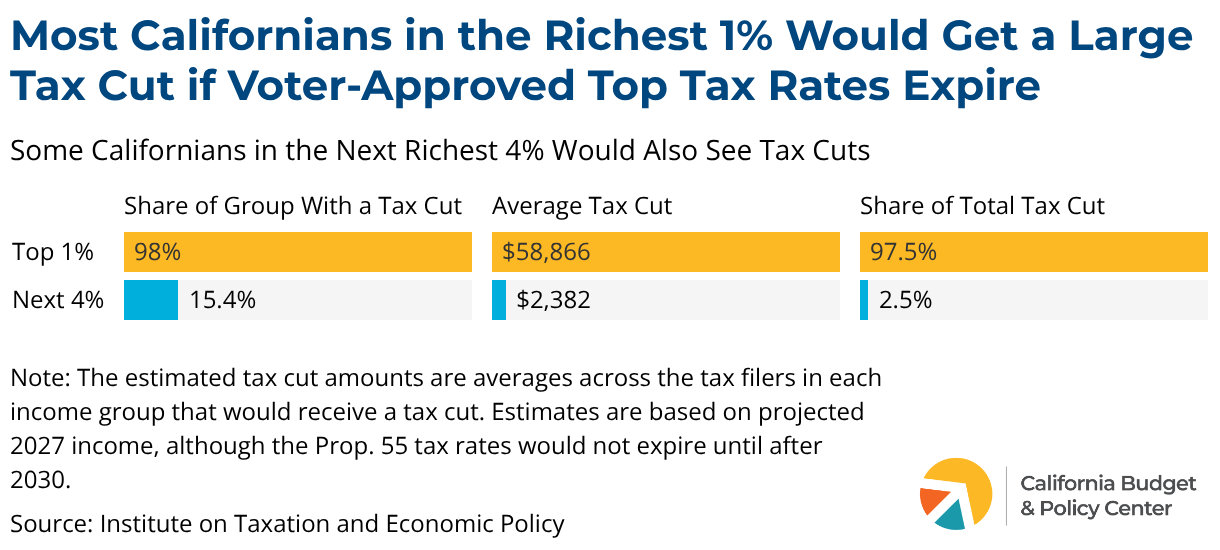

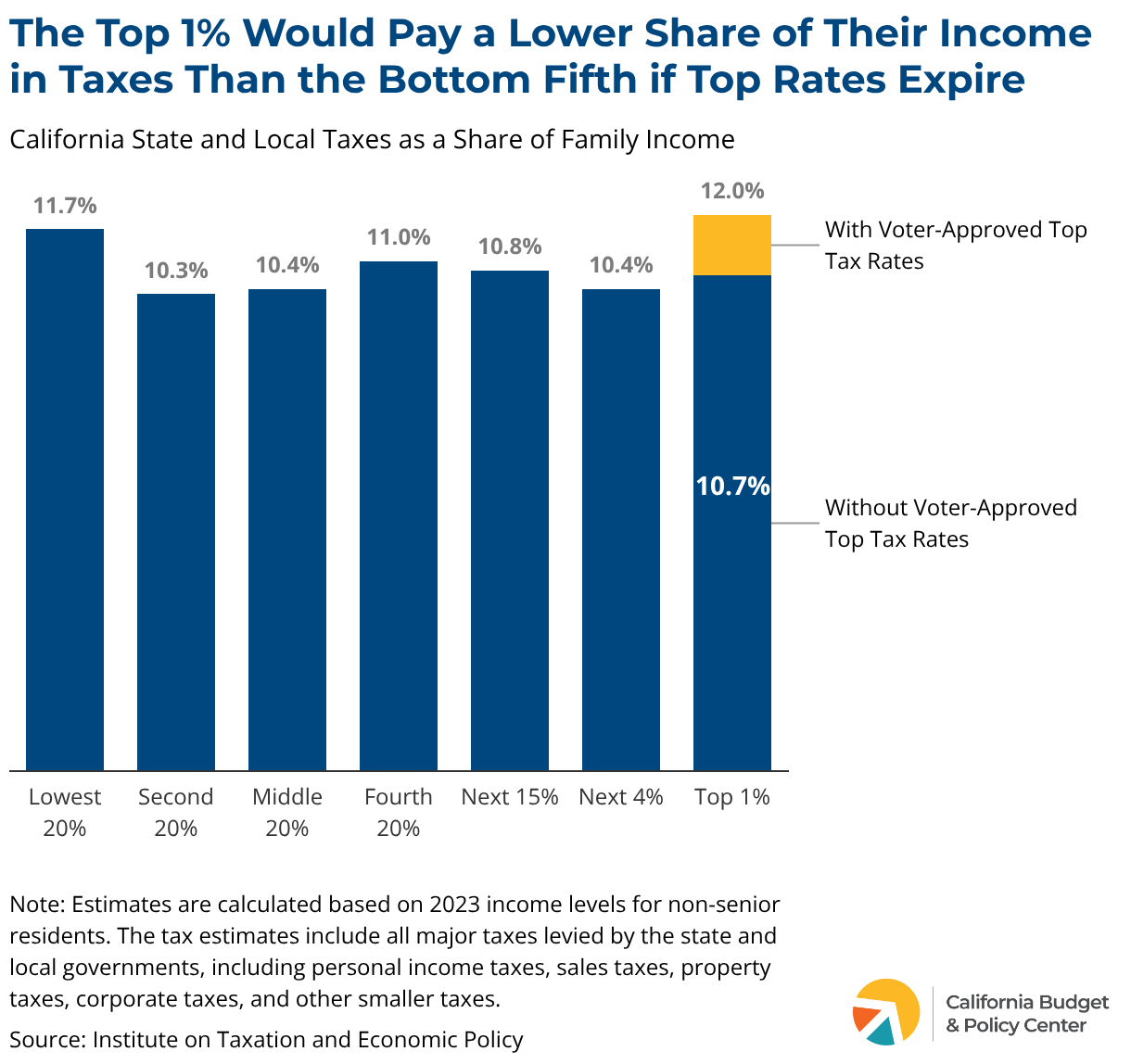

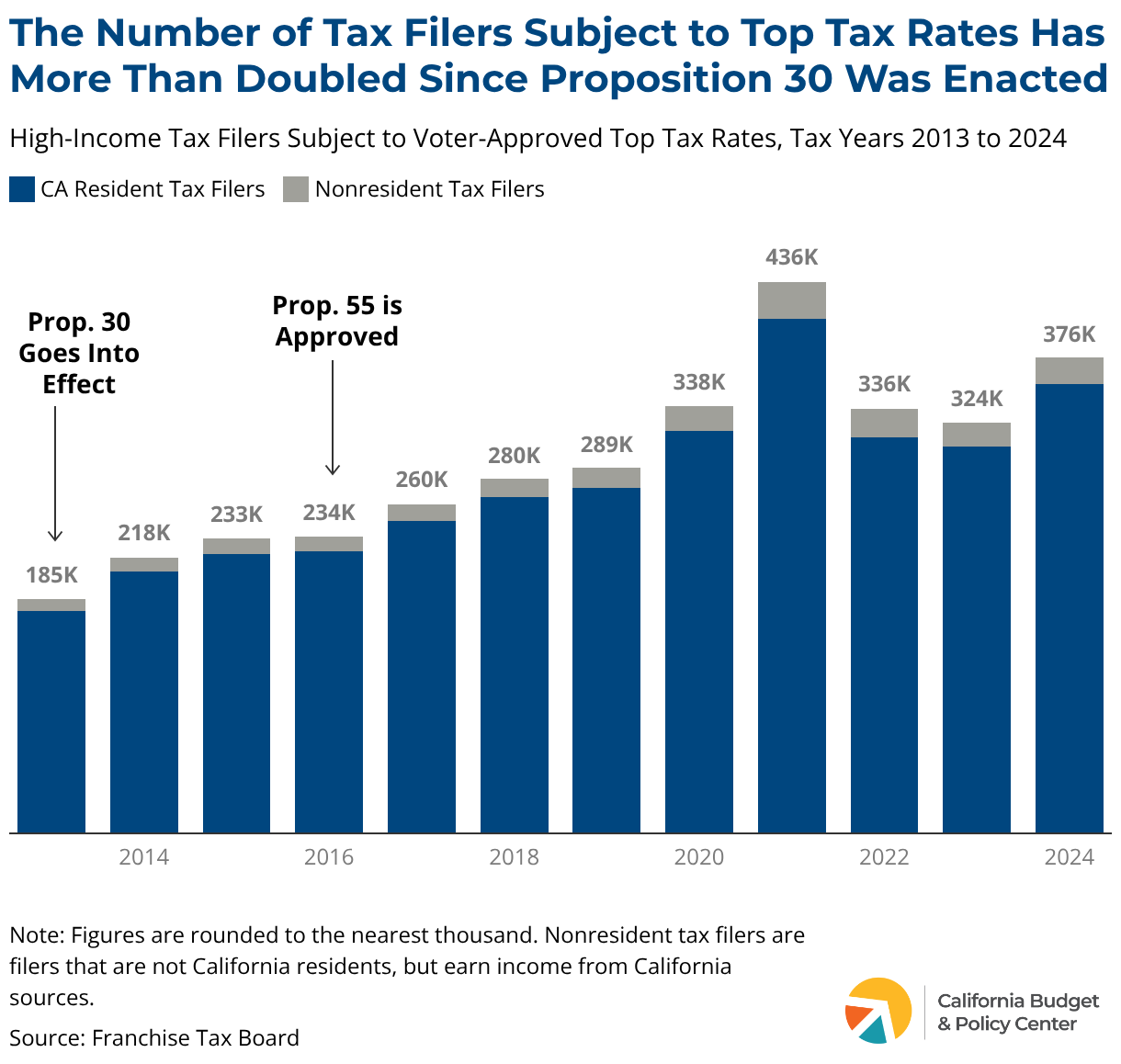

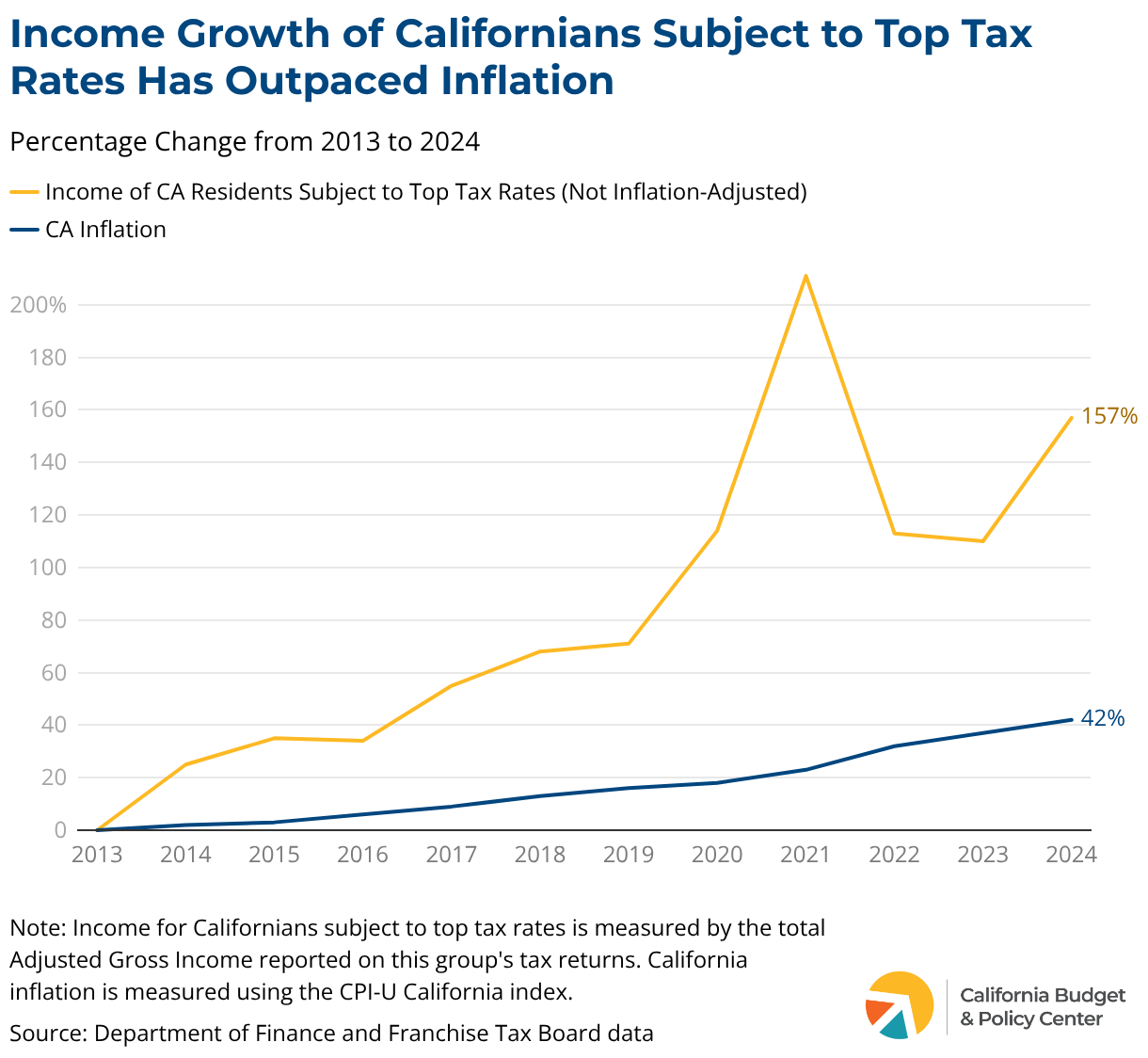

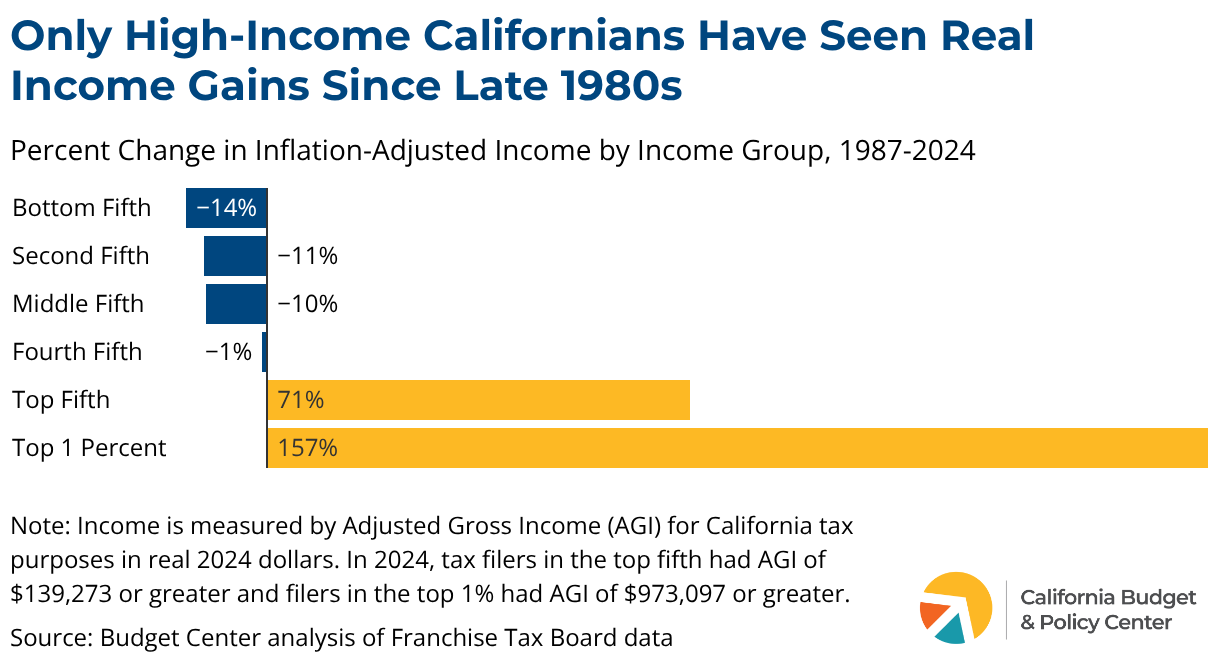

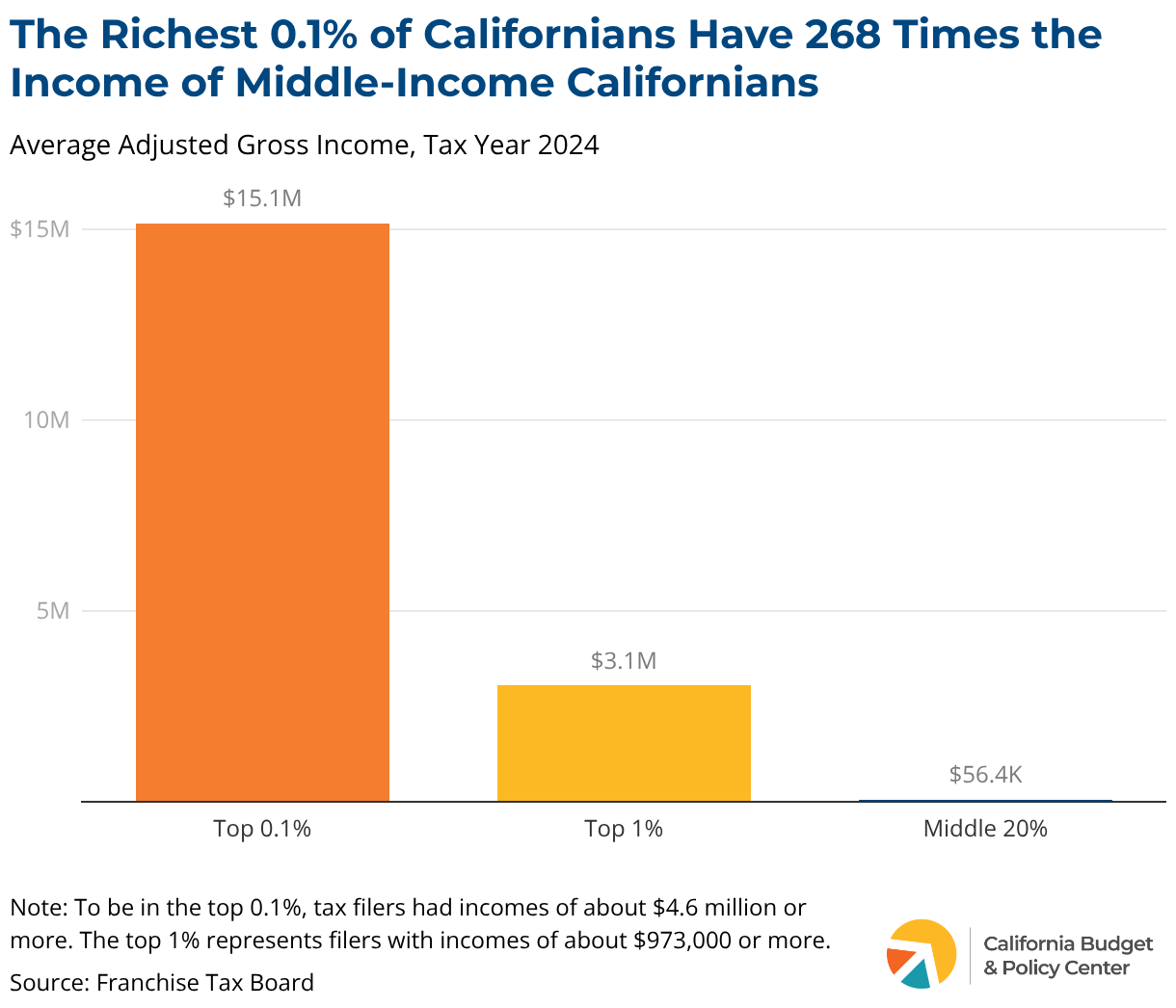

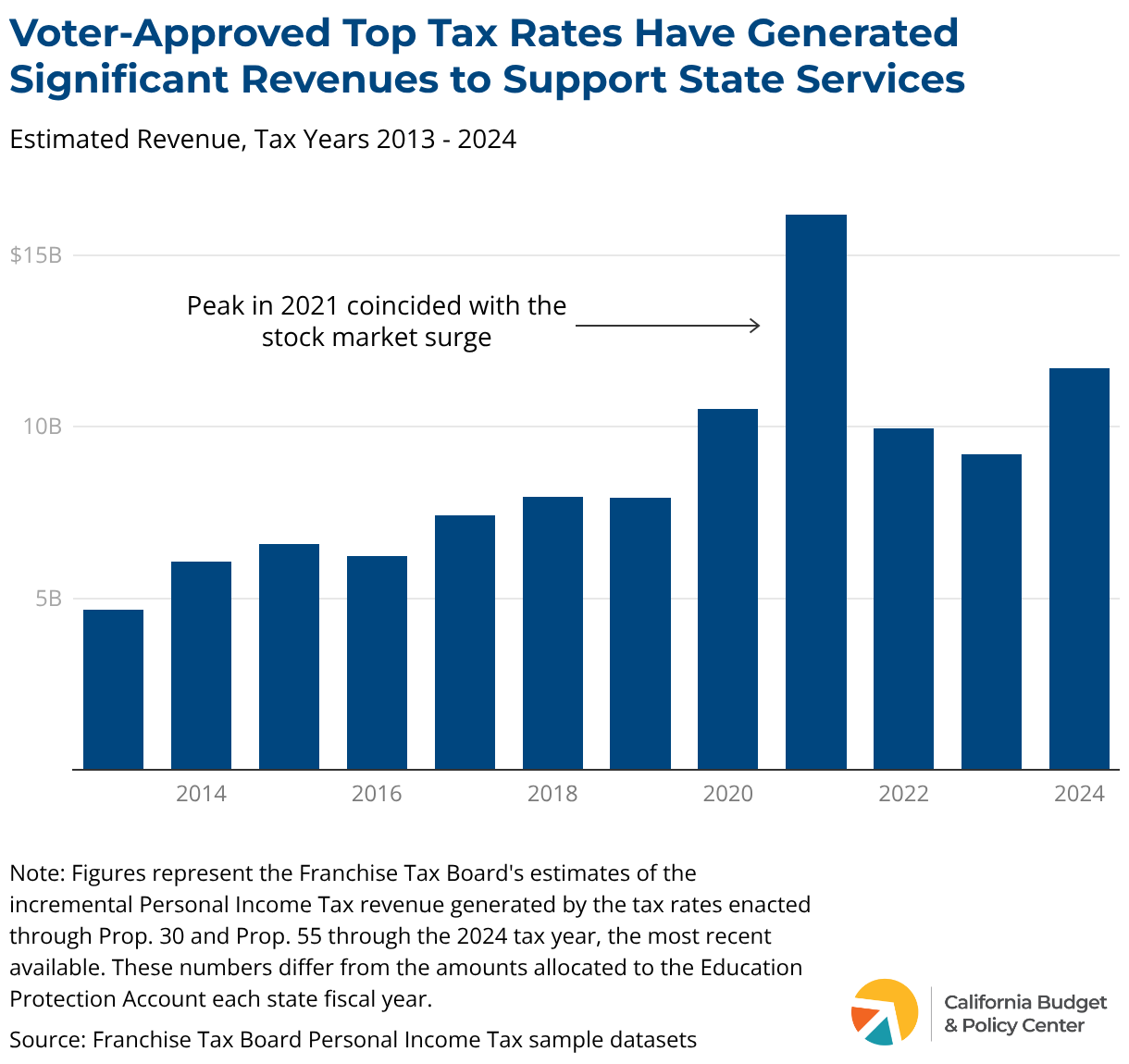

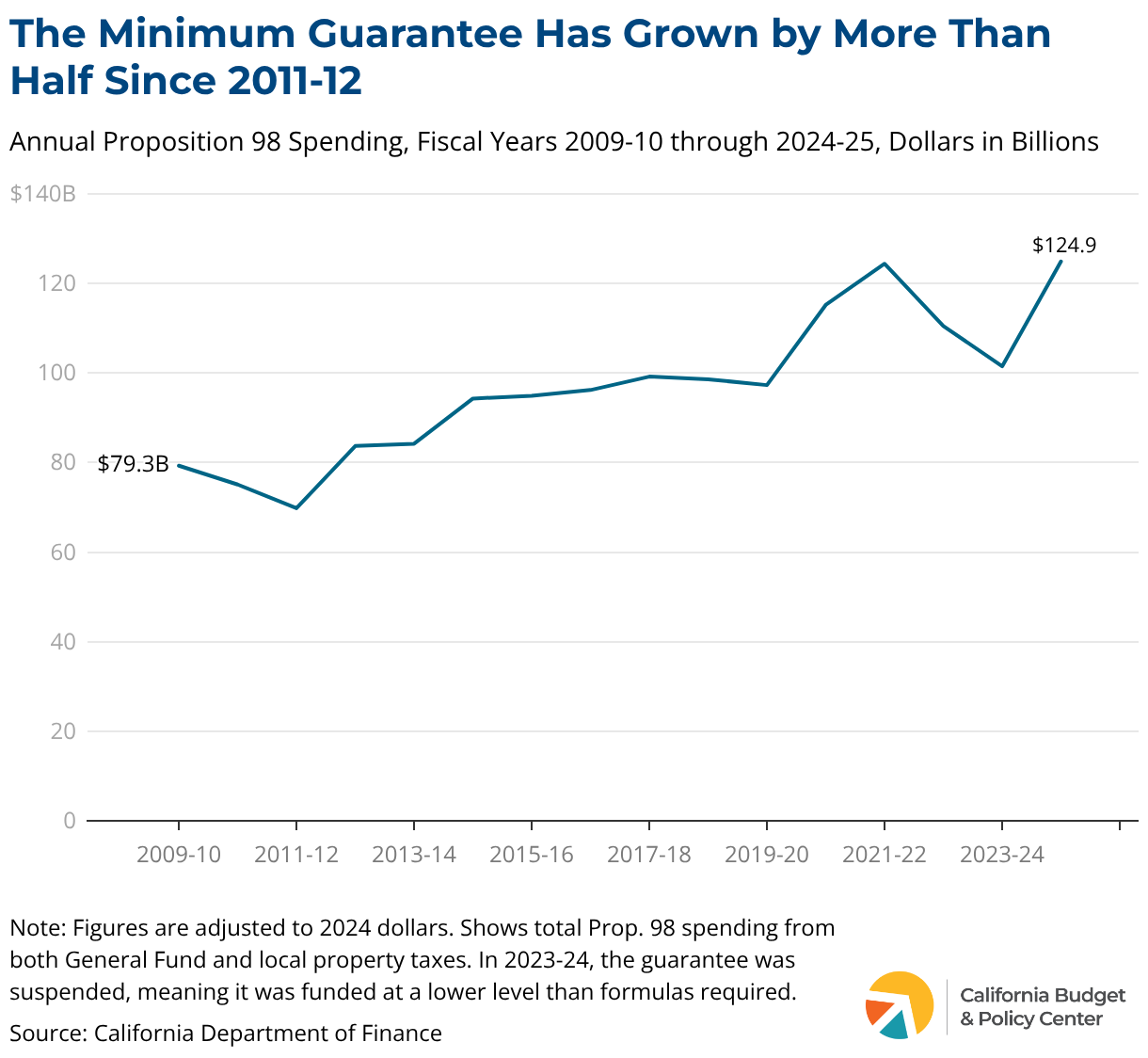

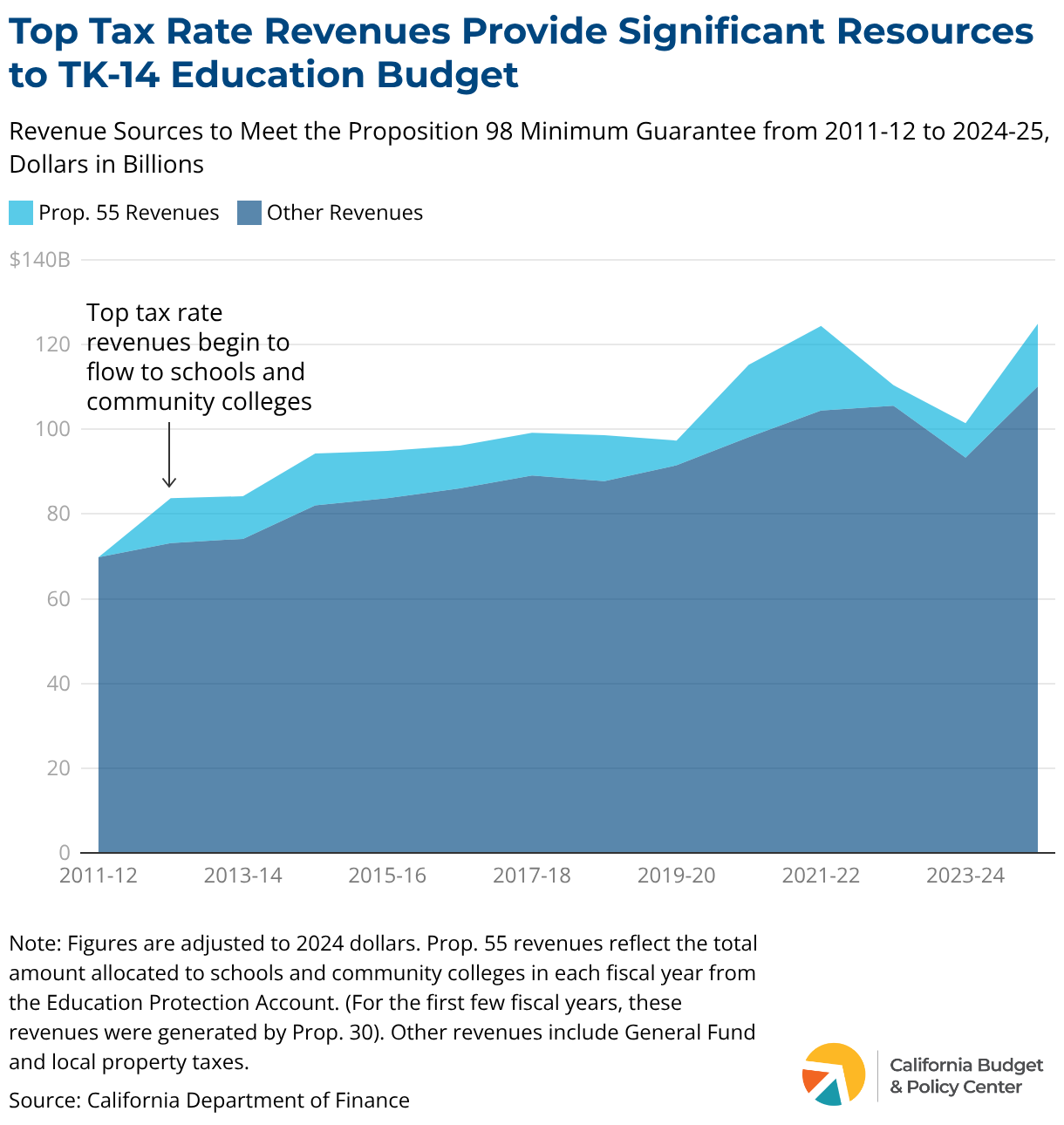

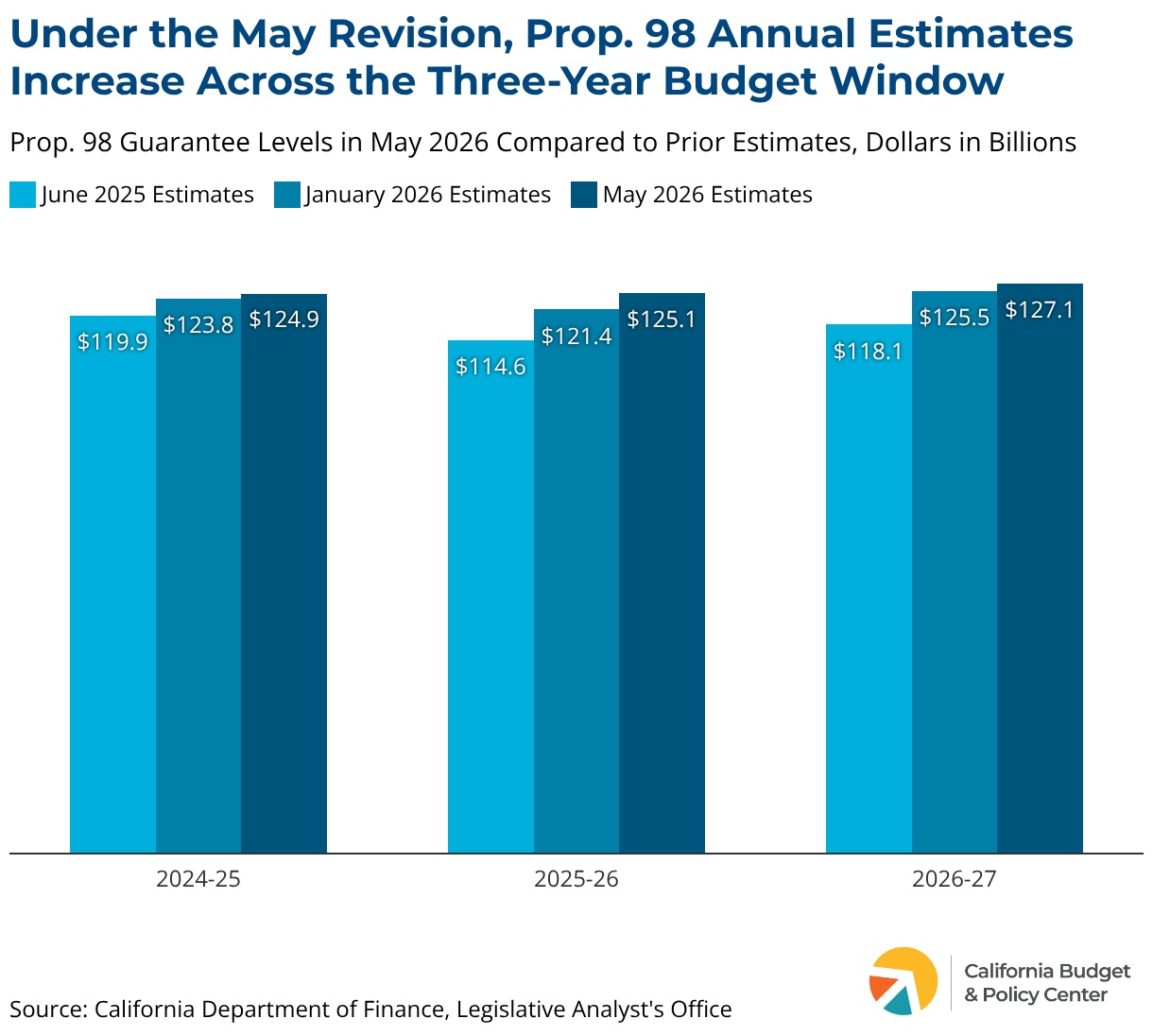

Proposition 3 will appear on the November 2026 statewide ballot, asking California voters whether to make permanent the higher-income tax rates on the state’s highest earners. These top tax rates were first enacted by voters in 2012 and renewed in 2016 to help fund schools, health care, and other supports for working families. Without action, the current rates are set to expire after 2030, reducing state revenues by billions of dollars annually and threatening funding for schools and state programs and services that support Californians every day.