How Republican-Led Budget Cuts Could Impact Californians in Every Congressional District

May 2025 | By the California Budget & Policy Center

Access to affordable health care, housing, and nutritious food is necessary for all Californians to thrive. But Republican federal budget proposals would pave the way for deep and harmful cuts that would take health coverage, nutrition assistance, and other essentials away from millions of Californians who are already struggling to make ends meet in the face of persistently high inflation and the high cost of living. These cuts would increase poverty and hardship, widen race and ethnic inequities, and make it harder for workers to maintain their jobs in exchange for funding huge tax giveaways for the wealthy.

This resource shows how many residents in each of California’s congressional districts benefit from vital programs at risk of being cut to illustrate the potentially wide-reaching impact cuts could have in communities across the state.

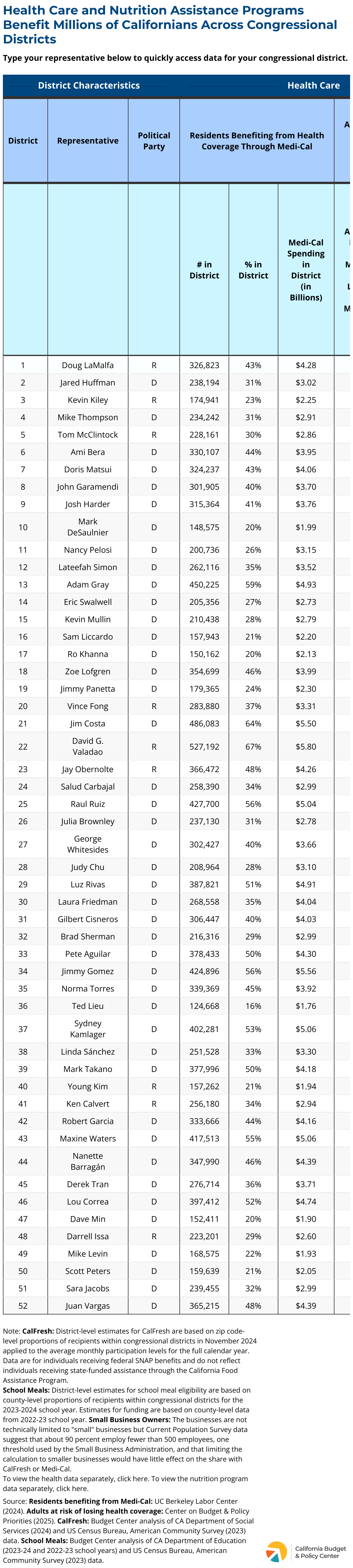

Medi-Cal saves lives. It’s a lifeline that provides free or low-cost health coverage for nearly 15 million Californians — over one-third of the state’s population — including children, pregnant individuals, seniors, and people with disabilities. Cutting Medi-Cal funding would mean taking critical care away from residents who need it the most in every congressional district in the state. Without access to health coverage, Californians will face impossible choices that put their health and economic security at risk while also driving up long-term costs for the state. Communities that would be particularly harmed by cuts include those in CA-22 (Valadao), where 67% of residents are enrolled in Medi-Cal, as well as in CA-21 (Costa) and CA-13 (Gray), where roughly 60% of residents or more are enrolled.

What is medi-cal?

Medi-Cal, California’s Medicaid program, provides free or low-cost health care to over one-third of the state’s population. This program covers a wide range of services to Californians with modest incomes, and many children, seniors, people with disabilities, and pregnant individuals rely on it.

Nutrition

CalFresh nutrition assistance helps over 5 million Californians each month, including workers with low-paying jobs, buy the food they need to support their households. It brings billions of federal dollars into the state each year that Californians spend in their communities helping to boost local businesses and jobs. In early 2023, CalFresh kept 1.1 million state residents out of poverty, reducing California’s poverty rate by 3 percentage points, according to the Public Policy Institute of California. Cutting CalFresh funding would increase poverty and hunger, making it harder for residents in every California congressional district to maintain their jobs, and hurting local businesses as families spend less on groceries. Cuts could also reduce students’ access to free meals at school, putting additional pressure on family budgets. Note that data for small business owners refers to the use of CalFresh and Medi-Cal, given the compounding effects of these threats for many Californians. Communities that would be especially harmed by cuts include those in CA-21 (Costa) and CA-22 (Valadao), where more than one-quarter of residents benefit from CalFresh.

What is calfresh?

CalFresh — California’s name for the Supplemental Nutrition Assistance Program (SNAP) — is the state’s most powerful tool to fight hunger. CalFresh provides modest monthly cash-like assistance to over 5 million Californians with low incomes to purchase food.

H.R. 1 and the Federal Budget

H.R. 1, the harmful Republican mega bill passed in July 2025, will deeply harm Californians by cutting funding for essential programs like health care, food assistance, and education.

See how California leaders can respond and protect vital supports.

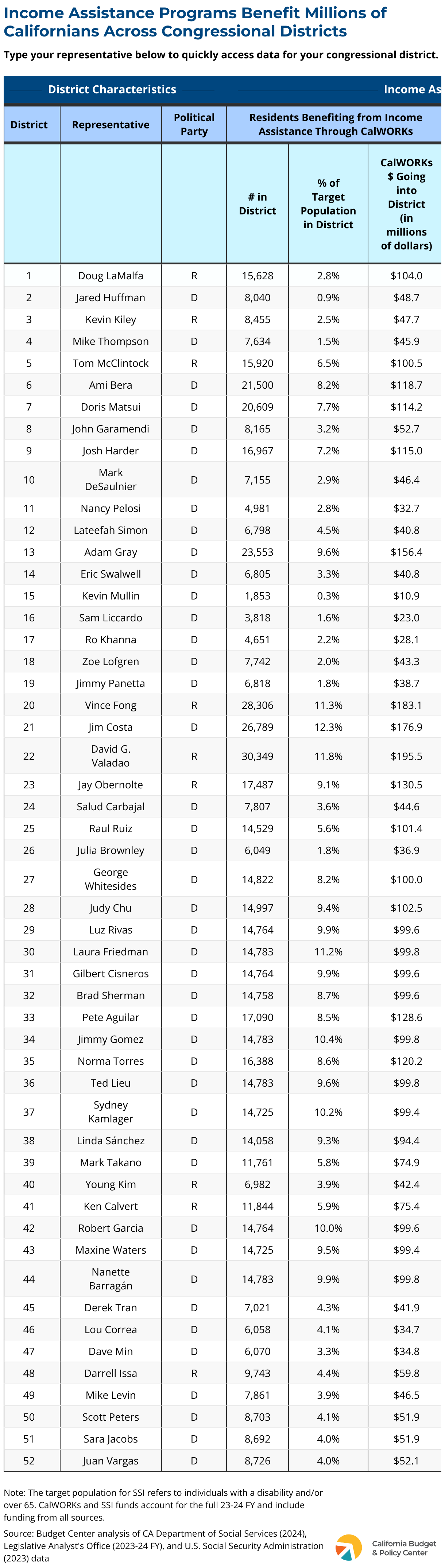

Income supports like CalWORKs and SSI help Californians with very low incomes, including people who are blind and individuals with disabilities, pay the rent and buy essentials for their families, like diapers and school supplies. These and other safety net supports lifted 3.2 million Californians out of poverty in early 2023, according to the Public Policy Institute of California. Cutting vital income supports would increase poverty and hardship for low-income families with children, seniors, and disabled children and adults. Cuts would also reduce the spending power of residents in every California congressional district, hurting local businesses and the local economy. Districts that would be particularly harmed by cuts to CalWORKs include CA-21 (Costa), CA-22 (Valadao), and CA-20 (Fong), and those especially harmed by cuts to SSI include CA-37 (Kamlager), CA-21 (Costa), and CA-22 (Valadao).

what is calworks?

The California Work Opportunity and Responsibility to Kids (CalWORKs) program, California’s TANF program, is a core component of California’s safety net for families with low incomes. The program helps over 650,000 children and their families, who are predominantly people of color, with modest cash grants, employment assistance, and critical supportive services.

what is ssi?

The Supplemental Security Income (SSI) program is a critical lifeline that assists over 1 million low-income individuals with disabilities and adults age 65 or older in California by covering expenses such as housing, food, and other essential living costs. California provides a modest supplement to SSI recipients with its own state-funded State Supplementary Payment (SSP) program.

Refundable Tax Credit Programs

Refundable Tax Credits

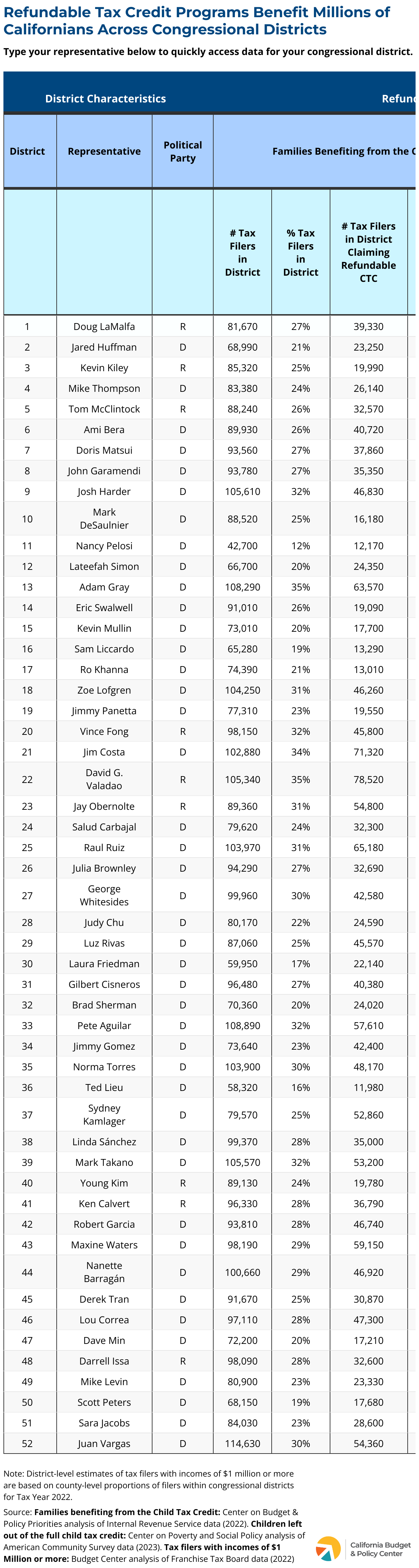

Credits like the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) are proven tools for improving economic security among Californians with low and moderate incomes, and they’ve been linked to long-term benefits for children, including better health and school achievement. Cutting these credits would take away income that families in every California congressional district count on to make ends meet, reducing their spending power and hurting local businesses and the economy. Districts that would be especially harmed by cuts to the CTC include CA-22 (Valadao), CA-21 (Costa), and CA-13 (Gray), where more than one-third of residents currently benefit from the credit, and CA-22 (Valadao), CA-21 (Costa), and CA-25 (Ruiz), where one-quarter or more residents benefit from the EITC.

In sharp contrast, the tax breaks Republican leaders want to provide through the budget will overwhelmingly enrich millionaires and billionaires, potentially providing a tax break of $72,800 to California’s richest 1%, who have incomes of roughly $1 million or more. This means just a sliver of the population in California’s congressional districts will reap the majority of the benefits of federal budget proposals, including just 0.14% of tax filers in CA-33 (Aguilar) and 0.16% of those in CA-23 (Obernolte) and CA-22 (Valadao) – roughly 500 tax filers in each of those three districts.

What is the eitc?

The Earned Income Tax Credit (EITC) is a federal tax credit that provides hundreds to thousands of dollars as a tax refund to about 2.5 million working families and individuals with low or moderate incomes in California. Families mostly use the EITC to pay for necessities such as food and housing, and the credit lifts millions of people out of poverty across the US each year.

what is the ctc?

The Child Tax Credit (CTC) is a federal tax credit that provides up to $2,000 per child to about 4.6 million families in California. When the credit was significantly increased and expanded to families with low incomes for one year during the pandemic it cut the US child poverty rate to an historic low and substantially reduced California’s child poverty rate.

Early Care and Education

Subsidized early care and education programs allow parents with low incomes to work or go to school, feeling secure that their children have a safe space to learn and grow. However, early care and education programs in California remain unaffordable for many families across the state. For example, a single mother in California with an infant and a school-age child will spend 61% of her income on child care. Additionally, only 14% of California’s children eligible for state-administered child care actually receive care due to inadequate state and federal funding.

The federal Head Start, Early Head Start, Migrant/Seasonal Head Start, and American Indian/Alaska Native Head Start (collectively, Head Start) programs provide critical early care and education for more than 73,000 children ages zero to 5 for families living in poverty in California, plus homeless, foster, and disabled children. Federal Head Start funding flows directly to local programs and is not a part of state-administered subsidized child care programs. Given the tremendous gap in the number of children eligible and the number of children enrolled in state-administered programs, Head Start provides a lifeline for families with low incomes looking for affordable child care. Additionally, the California Department of Social Services administers a child care program for CalWORKs participants called “Stage 1.” Stage 1 CalWORKs child care helps a family access immediate child care as the parent/guardian participates in the CalWORKs program. The Stage 1 CalWORKs child care program is funded through federal Temporary Assistance for Needy Families (TANF) dollars and serves over 53,000 children in California.

Without Head Start and CalWORKs Stage 1 child care, thousands more families in California would be stuck on child care waiting lists, making it even harder for them to make ends meet. This strain not only burdens families but also negatively impacts the state’s economy by reducing workforce participation and spending as parents struggle to find affordable child care options. Early care and education programs also provide an economic benefit for the community. For example, research shows that every one dollar invested in Head Start generates at least seven dollars in benefits.

Districts that would be particularly harmed by cuts to Head Start programs include CA-13 (Gray), CA-21 (Costa), CA-22 (Valadao), CA-31 (Cisneros), and CA-52 (Vargas).

Housing

Safe, affordable housing provides the foundation for families and individuals to thrive, supporting strong communities, better health, career and educational success, and economic mobility. However, California’s housing shortage, combined with wages that have not kept pace with the cost of living, forces millions into economic hardship and unstable housing situations. More than half of all California renters struggle with unaffordable housing costs, leaving them vulnerable to financial crises, displacement, and even homelessness.

High housing costs push Californians out of their homes and communities while stretching budgets so thin that basic necessities like food, child care, gas, and medical expenses become out of reach. Federal housing programs—such as rental assistance, homelessness prevention and mitigation, and affordable housing development—support Californians in every congressional district by helping people pay rent, secure stable homes, and stay in their communities. In California, federal housing programs support 920,437 people and 507,463 households. Still, these programs don’t meet the demand—Housing Choice Vouchers, for example, reach only 1 in 4 eligible households, leaving many without the support they need. Since housing programs are not entitlements, limited funding leaves many without support even though they qualify, and further cuts could put even more Californians at risk of losing their homes. Districts where renters face particularly high rental costs compared to their income include CD-27 (Whitesides), CA-29 (Rivas), CA-33 (Aguilar), CA-49 (Levin), and CA-51 (Jacobs).

Federal Policy

The federal government plays a major role in shaping California’s budget, economy, and the well-being of its people.

Learn how federal policies shape California’s budget, economy, and vital programs — and how state leaders can respond to protect and support Californians.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

Republican federal budget proposals would significantly widen California’s already extreme income inequality by slashing essential programs like Medi-Cal and CalFresh while delivering massive tax breaks to the wealthy. State leaders must take action to protect Californians by preventing harmful cuts.

The gap between the rich and poor in California is vast, and the majority of Californians believe this is a problem that policymakers should address. However, Republican federal budget proposals would significantly widen inequities by taking health care, nutrition assistance, and other essentials away from millions of people to fund massive tax breaks for the wealthy. These proposals would also deepen racial and ethnic inequities, with cuts falling hardest on Californians of color and tax benefits predominantly enriching white Californians.

California’s leaders should do everything possible to combat inequality and protect their communities from these federal threats by first working to prevent or mitigate harmful cuts, while also developing strategies to protect their communities if those cuts are enacted. State policymakers can safeguard essential services if they equitably raise new state revenue by ending costly tax breaks that further enrich the wealthy and corporations who will be the primary beneficiaries of federal tax cuts.

California’s Stark Income Inequality

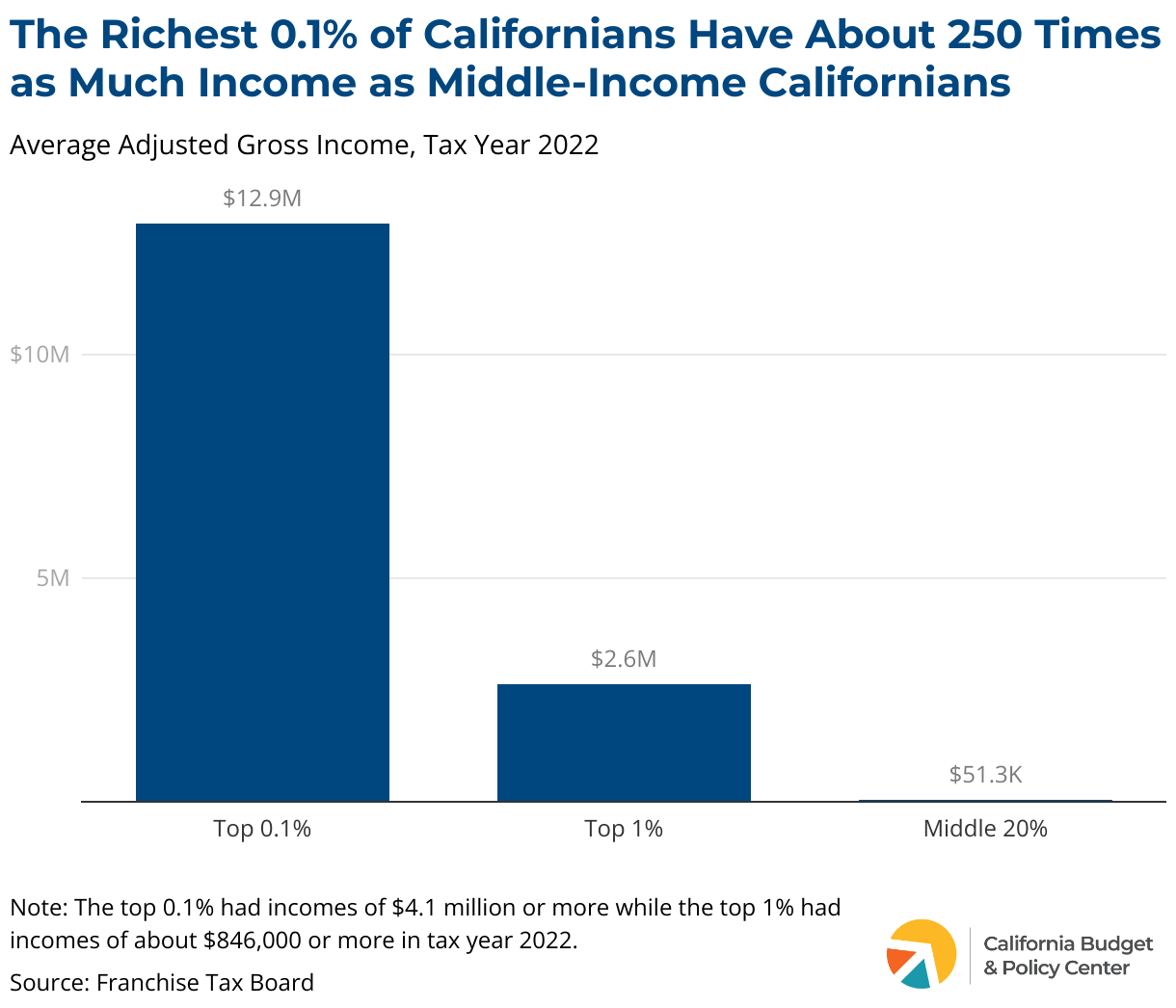

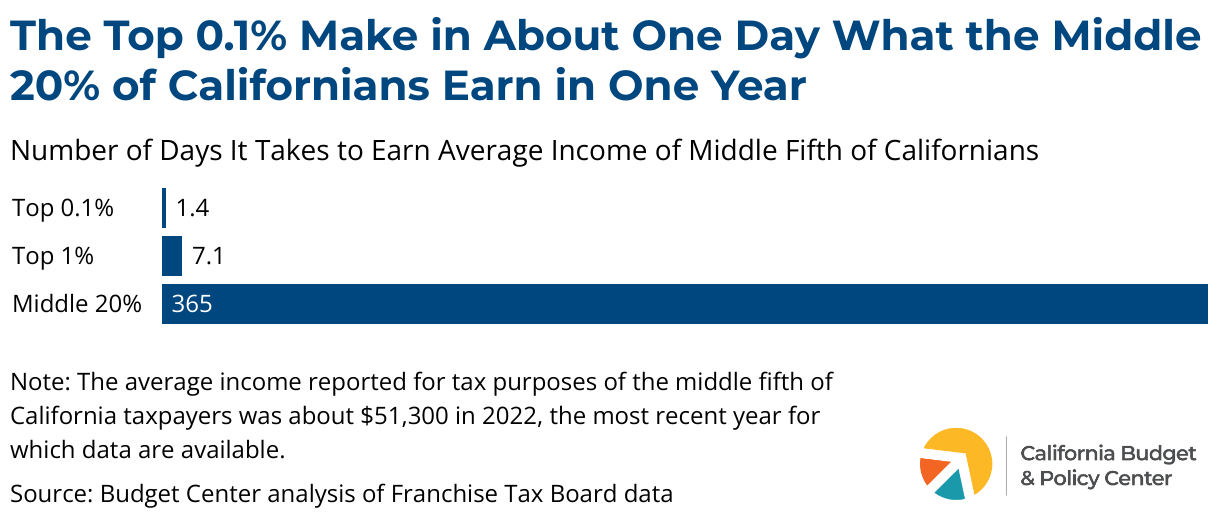

While millions of Californians struggle to afford food, housing, and other necessities as the state’s affordability crisis worsens, a tiny sliver of the population enjoys extreme income and wealth. The richest 0.1% of Californians had an average income of $12.9 million in 2022 (the most recent year for which data are available) — about 250 times the average income of middle-income Californians ($51,300). The top 0.1% earn in just over a day what the average middle-income Californian makes in an entire year. The richest 1% of Californians, with an average income of $2.6 million in 2022, can make in about one week what the average middle-income Californian earns in a year.

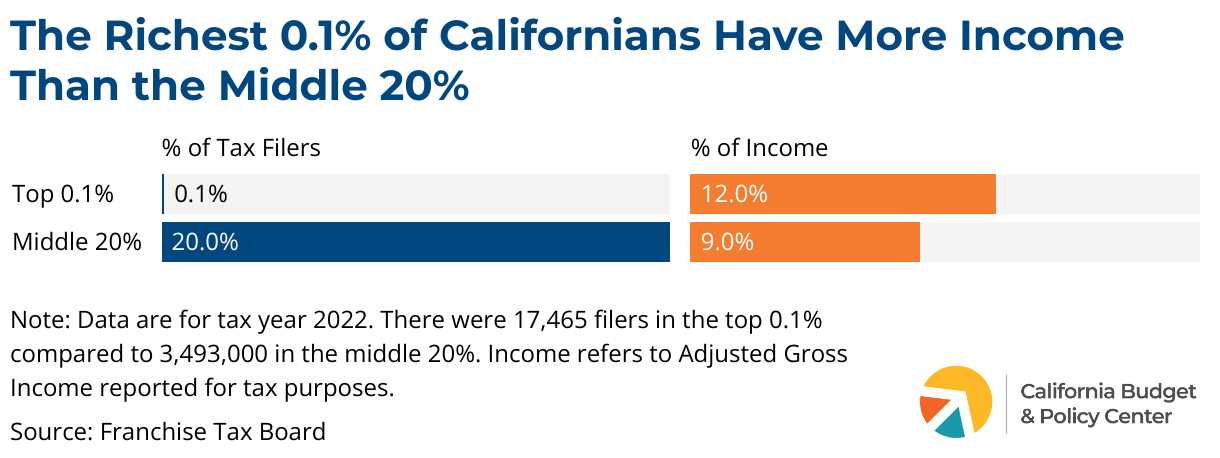

Collectively, the richest 0.1% of Californians — nearly 17,500 households — have more income than the roughly 3.5 million households in the middle fifth. In other words, a population roughly the size of the city of Los Angeles is out-earned by a group small enough to fit inside a sports arena. Specifically, the top 0.1% had 12% of all income reported for state tax purposes in 2022, while the middle fifth had 9% of all income. Altogether, the richest 0.1% of Californians reported about $226 billion in income for state tax purposes that year.

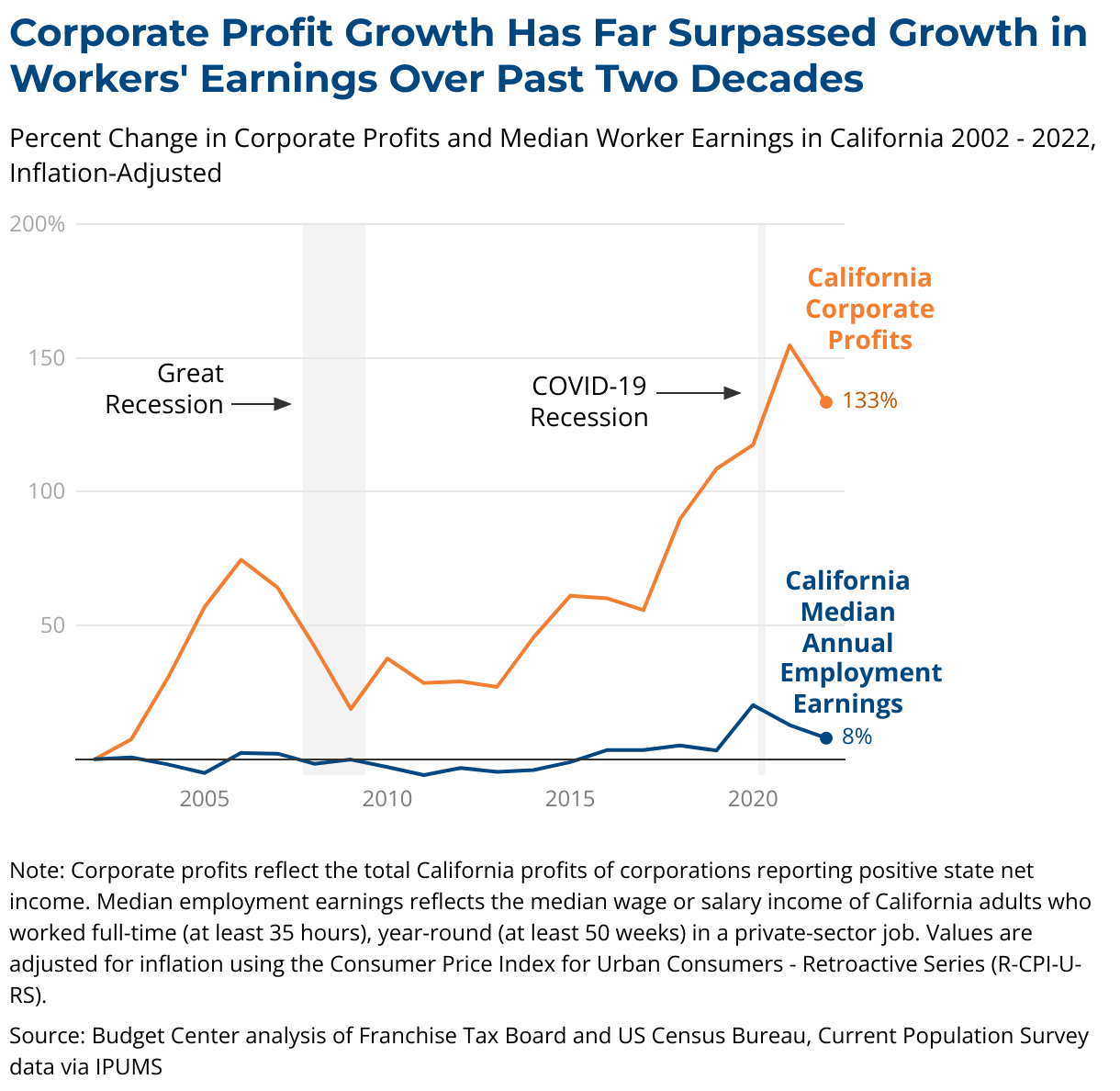

Corporate Profit Growth Far Outpaces Workers’ Wage Increases

Corporations have seen skyrocketing profits in recent years, but these gains have failed to trickle down to the workers who help make those profits possible. California corporate profits reached $365 billion in 2022, reflecting a 133% increase since 2002 in inflation-adjusted terms. In contrast, the typical Californian’s earnings have barely kept up with inflation. Median annual earnings for a full-time, year-round worker rose by just 8% during that period, after accounting for inflation. While data on California profits after 2022 is not yet available, corporate profits nationally have continued to rise.

Corporations with state profits of at least $10 million — which represent just around 0.5% of all profitable corporations in the state — saw their profits in California more than double from 2017 to 2022, soaring from $113 billion to $220 billion. In contrast, Californians’ purchasing power declined during this period due to high inflation, a phenomenon that someresearcherssuggest has been amplified by corporations keeping prices high even as their costs declined following pandemic-era cost spikes due to supply chain issues. Households with low incomes have been hit hardest by inflation because prices have risen more for necessities that make up a larger share of their spending.

Republican Federal Budget Proposals Would Worsen Income Inequality

Proposed federal budget and tax cuts would greatly exacerbate the already stark inequalities in the state by slashing assistance that helps millions of Californians meet their basic needs while extending and potentially expanding tax breaks that primarily benefit wealthy people and corporations.

While the details of these cuts have yet to be determined, the budget resolution passed by Congress in April instructs the House committee with jurisdiction over Medicaid (Medi-Cal in California) to make cuts on of at least $880 billion over ten years and instructs the committee with jurisdiction over the Supplemental Nutrition Assistance Program (SNAP, known as CalFresh in California) to make cuts of at least $230 billion. These cuts would be roughly equal to the share of the proposed tax cuts that would go to the richest 1% of Americans. Federal cuts could also target other programs that help people meet their basic needs, such as income support for families, older adults, and people with disabilities.

what is medicaid?

Medicaid, known as Medi-Cal in California, provides free or low-cost health coverage for nearly 15 million Californians — over one-third of the state’s population — including children, pregnant individuals, seniors, and people with disabilities. Cutting Medi-Cal funding would mean taking critical care away from residents who need it the most.

what is snap?

SNAP, known as CalFresh in California, provides modest monthly assistance to over 5 million Californians with low incomes to purchase food. Proposals to cut this powerful anti-poverty program and implement harsh work requirements would make it harder for millions of people with low incomes to put food on the table.

Families with low incomes would be worse off, while wealthy households would get a windfall if Congress makes the deep cuts to Medicaid and SNAP included in the budget resolution instructions for the House and extends provisions of the 2017 federal tax law. Specifically, the top 1% of Americans would gain $43,500 a year on average while the bottom fifth of Americans would lose $1,125 annually from the combined impact of the deep cuts to Medicaid and nutrition assistance and the extension of the 2017 tax law that mainly benefits wealthy people and corporations. In California, the reduction in Medi-Cal benefits alone could be akin to losing $1,948 in income, or about 8.7% of the average income of the bottom fifth of households.

Republican Federal Budget Proposals Would Worsen Racial Inequality

Proposed cuts to Medicaid (Medi-Cal) and SNAP (CalFresh) paired with massive tax breaks for the wealthy would also widen already stark racial inequities both nationally and in California. Cuts to health and food assistance would overwhelmingly harm Californians of color, who are more likely to benefit from these programs due to the long legacy of racist policies and practices that have excluded them from income and wealth-building opportunities. About 8 in 10 Californians who are enrolled in Medi-Cal are people of color, including 57% who are Latinx, 12% who are Asian, 7% who are Black.1Center on Budget and Policy Priorities analysis of US Census Bureau, American Community Survey data 2022-23. Latinx includes all individuals who identify as Latinx, regardless of race. 20% of Medi-Cal enrollees are white (not Latinx), while another 5% are multiracial or identify with another race not elsewhere specified. More than 7 in 10 Californians who head households enrolled in CalFresh are people of color, including 43% who are Latinx, 13% who are Asian, and 11% who are Black.2Center on Budget and Policy Priorities analysis of US Census Bureau, American Community Survey data 2022-23. Latinx includes all individuals who identify as Latinx, regardless of race. 27% of CalFresh heads of household are white (not Latinx), while another 5% are multiracial or identify with another race not elsewhere specified. In contrast, because racial income and wealth gaps are already vast due to centuries of structural racism, any tax policy that redistributes benefits to people with high incomes or wealth will disproportionately benefit white people. Nationally, in 2018 white households received 80% of the benefits of federal tax cuts enacted during the first Trump Administration even though they comprised 67% of households. In addition, research finds that white households generally receive 88% of the benefits of any corporate tax break, while Black and Latinx households receive just 1%.3This excludes the share of benefits of corporate tax breaks that go to foreign investors.

Federal Republican Tax Proposals Would Provide a Massive Windfall for the Wealthy

The details on what tax cuts will ultimately be included in the federal budget package is still uncertain, but the centerpiece will be extending or making permanent all or most of the provisions of the 2017 tax law enacted in the first Trump administration that are set to expire at the the end of 2025. Republican leaders are also considering additional tax cuts on top of extending the expiring provisions.

Increase or Elimination of State and Local Tax Deduction (SALT) Cap

One provision of the 2017 tax law that federal lawmakers may not fully extend is a limitation on the amount of state and local taxes that households can deduct for federal tax purposes (the “SALT” cap). Some federal leaders have indicated they would eliminate or raise the cap, which would result in a larger federal tax break for the top 1%. In California, extending all of the 2017 law’s provisions except for the SALT cap could provide an annual tax cut of nearly $73,000 to the state’s richest 1%.

Additional Tax Breaks for Corporations

In addition to extending the expiring individual provisions, Republican leaders also want to provide additional tax cuts for corporations, which would primarily benefit corporate shareholders, who are disproportionately wealthy and white, as well as foreign investors. Proposals include restoring already expired provisions of the 2017 law that provided more generous tax treatment for corporations, and cutting the corporate tax rate — reduced from 35% to 21% in the 2017 law — even further.

Tax Exemptions for Tip, Overtime and Social Security Income

The tax proposals Trump has put forward to exempt income from tips, overtime pay, and Social Security benefits from taxation would disproportionately benefit higher-income people. Additionally, tax exemptions for tip and overtime income would invite more worker exploitation and create gaming opportunities for employers and high-income employees.

Trump Tariffs

While not directly a part of the federal budget negotiations, Trump has suggested revenue from tariffs could offset the costs of extending and increasing tax cuts for wealthy people and corporations. The impacts of tariffs will exacerbate harms for people already struggling most with high costs of living. Tariffs largely increase the prices of goods, and these price hikes fall hardest on lower-income households relative to their incomes.

Republican Federal Budget Proposals Would Widen Inequality in Every California Congressional District

Across California, the federal budget and tax cuts would represent a large upward redistribution of resources from families already struggling with the costs of living to the wealthy who barely notice when the cost of essentials increases. Millionaires, who stand to benefit most from the proposed tax cuts, represent just between 0.2% and 2.8% of residents in each of California’s Congressional Districts. In contrast, large shares of residents in these districts could be harmed by cuts to Medi-Cal or CalFresh. In the majority of California’s districts, at least one-third of residents receive critical health coverage through Medi-Cal. Half to two-thirds of residents in 10 districts rely on Medi-Cal for health care. Additionally, at least 10% of residents in most districts count on CalFresh to buy groceries, with at least 20% using CalFresh to feed their households in eight districts.

State Leaders Should Protect Californians From Increased Hardship and Inequality

Policymakers should invest in the well-being of everyday people, not just the wealthy. But federal Republicans are pushing forward with plans to slash health care and other vital services that millions of people count on every day — all to further enrich the top 1%. These proposals would widen the already extreme income inequality in California, deepening racial and ethnic inequities and making it even more difficult for all Californians to prosper. State leaders should do everything they can to protect their communities from these threats, including ending costly tax breaks that further enrich the wealthy and corporations who will reap the majority of the benefits of these federal proposals. This would allow California to equitably raise new state revenue to shield communities from federal threats this year and beyond and safeguard essential services that promote the health and economic well-being of all Californians.

Federal Policy

The federal government plays a major role in shaping California’s budget, economy, and the well-being of its people.

Learn how federal policies shape California’s budget, economy, and vital programs — and how state leaders can respond to protect and support Californians.

Center on Budget and Policy Priorities analysis of US Census Bureau, American Community Survey data 2022-23. Latinx includes all individuals who identify as Latinx, regardless of race. 20% of Medi-Cal enrollees are white (not Latinx), while another 5% are multiracial or identify with another race not elsewhere specified.

2

Center on Budget and Policy Priorities analysis of US Census Bureau, American Community Survey data 2022-23. Latinx includes all individuals who identify as Latinx, regardless of race. 27% of CalFresh heads of household are white (not Latinx), while another 5% are multiracial or identify with another race not elsewhere specified.

3

This excludes the share of benefits of corporate tax breaks that go to foreign investors.

You may also be interested in the following resources:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

TK enrollment in California has doubled since 2021-22, with growth across all student groups and high-poverty schools. To ensure all children benefit, the state must address disparities in access for students of color and those from low-income families.

Early childhood education is foundational for young children’s development and their long-term outcomes, and preschool programs provide essential opportunities for 3- and 4-year-olds.1For example, see “Predictor: Access to Preschool,” Urban Institute (webpage), accessed March 1, 2025, https://upward-mobility.urban.org/framework/education/preschoolRecognizing the importance of early learning, California policymakers chose in 2021 to embark on a significant expansion of Transitional Kindergarten (TK), a specialized preschool program for 4-year-old children offered at public schools. To ensure this expansion benefits all children, it is crucial to track participation for student groups that have historically faced barriers, namely students of color and those from families with low incomes, as the challenges these students face may continue throughout their education. Given these ongoing patterns of inequity, this report highlights TK enrollment trends from 2021-22, before the age-eligibility expansion began to 2023-24, the second year of expansion and the most recent data available for these student groups.

Enrollment Increased Across All Race and Ethnicity Groups

TK enrollment has grown substantially across all racial and ethnic groups between the 2021-22 and 2023-24 school years. Overall enrollment increased by 101%, from 75,410 to 151,336 students. In 2023-24, TK enrolled 59% of eligible four-year-olds in California. While all student groups experienced significant growth, the percentage growth varied. Multi-racial students experienced the highest percentage growth (130%), followed by Asian students, who also had substantial increases (117%). Latinx students had the highest enrollment number in both years, 42,702 in 2021-22 and 83,362 in 2023-24, reflecting a percentage increase of 95%. American Indian or Alaska Native students had the lowest enrollment numbers (314 in 2021-22 and 571 in 2023-24) and the smallest percentage growth (82%).

Moving forward, the state should track take-up rates among the groups with the lowest percentage growth, including American Indian or Alaska Native, Latinx, and Black students. Additionally, ensuring equitable access to TK will require a focus on understanding and addressing potential barriers to participation among these students.

High-Poverty Elementary Schools Have Significantly Increased Their Enrollment

Elementary schools with higher poverty levels had the largest increases in TK enrollment between 2021-22 and 2023-24. Growth in the number of students varied across schools by their overall share of students eligible for Free and Reduced Price Meals (FRPM), a proxy to identify students from low-income families.2Free and reduced-price meal eligibility (FRPM) is a measure of need based on poverty levels that the state uses as a proxy to identify students from families with low incomes. Children from households with incomes below 185 percent of the federal poverty level are considered eligible. Eligibility is based on household size and income; for example, for the 2024-25 school year, a student in a household composed of three members with an annual income at or below $47,767 would be deemed eligible and counted as low income. Complete household size and income scale: https://www.cde.ca.gov/ls/nu/rs/scales2425.asp Schools in the highest FRPM category (76-100%) grew their enrollment by nearly 30,000 students, compared to about 10,000 students in schools with the lowest share of FRPM-eligible students (0-25%). The differences are primarily because there are far more schools in the highest FRPM category (1,982) than in the lowest (409).

Elementary schools in higher-poverty areas also had a significant increase in new TK programs. The following table displays the number of schools that added new TK programs — those that did not have any TK enrollment in 2021-22 — by FRPM categories. As shown in the table, 387 schools in the 76-100% FRPM category initiated new TK programs compared to 151 in the lowest FRPM category (0-25%). This shows that expansion efforts have primarily supported high-poverty schools by enabling them to establish and offer TK programs.

A higher share of children from low-income families participate in TK. Due to the lack of publicly available data, it is challenging to accurately determine the exact number of low-income children enrolled in TK.3The California Department of Education does not publicly report counts of students eligible for FRPM by grade level. The following table displays the estimated number of students from low-income families in TK, calculated based on the overall proportion of FRPM-eligible students at each elementary school. The estimate reveals that 90,754 children from low-income families are enrolled in TK, representing 64% of total enrollment.4Only schools classified as “public elementary schools” are included in this estimate. The increasing role of TK in supporting low-income families also highlights the need to monitor how families utilize the program and address any potential barriers.

Overall, TK enrollment has expanded significantly, with substantial growth across all racial and ethnic groups and a notable increase in TK programs in high-poverty schools. These trends demonstrate TK’s growing role in providing early learning opportunities to more children. However, more research is needed to understand local challenges. For example, TK uptake rates from 2021-22 to 2023-24 show faster growth in low-poverty schools (79%) compared to high-poverty schools (58%), suggesting potential barriers to access that warrant further investigation to ensure equity.

To build on this significant progress, the state should prioritize equity by addressing disparities in growth and ensuring that all children, particularly those from low-income families and children of color, can benefit from TK. This includes assessing and strengthening how the broader mixed delivery preschool system supports children and their families. By focusing on these areas, the state can continue to expand access to early learning opportunities, ensuring that children from low-income families have the strong foundation they need to succeed in school and beyond.

Free and reduced-price meal eligibility (FRPM) is a measure of need based on poverty levels that the state uses as a proxy to identify students from families with low incomes. Children from households with incomes below 185 percent of the federal poverty level are considered eligible. Eligibility is based on household size and income; for example, for the 2024-25 school year, a student in a household composed of three members with an annual income at or below $47,767 would be deemed eligible and counted as low income. Complete household size and income scale: https://www.cde.ca.gov/ls/nu/rs/scales2425.asp

3

The California Department of Education does not publicly report counts of students eligible for FRPM by grade level.

4

Only schools classified as “public elementary schools” are included in this estimate.

You may also be interested in the following resources:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

California is expanding Transitional Kindergarten to all four-year-old children by 2025-26, supported by state investments to improve access, staffing, and equity in public preschool programs.

Early learning is foundational for young children’s development, and preschool programs provide essential opportunities for 3- and 4-year-olds. Recognizing this, in 2021, California policymakers embarked on a significant expansion of Transitional Kindergarten (TK), a specialized preschool program for 4-year-old children offered at public schools. This ambitious expansion is backed by substantial state investment, reflecting a commitment to broaden access to preschool education. To support the multi-year plan, the state has allocated billions of dollars in one-time and ongoing funding. Through these investments, TK will be universally available to all four-year-old children in California by the 2025-26 school year.

How Policy Decisions Shaped the Expansion of Transitional Kindergarten

The TK program has been in place since 2012.1Senate Bill 1381 (Simitian, Chapter 705, Statutes of 2010), https://leginfo.legislature.ca.gov/faces/billTextClient.xhtml?bill_id=200920100SB1381 Its original purpose was to provide preschool education for four-year-old children who, based on the month they were born, were no longer eligible to enroll in kindergarten after the state adjusted the age cutoff for kindergarten admission — creating TK also allowed school districts to continue claiming Average Daily Attendance (ADA) for these students.2SB 1381 (Simitian) Essentially, this policy change prevented four-year-olds from being admitted to kindergarten if they turned five later in the year after enrolling in kindergarten.3Assembly Committee on Education analysis of Senate Bill 1381 (Simitian), June 1, 2010, https://leginfo.legislature.ca.gov/faces/billAnalysisClient.xhtml?bill_id=200920100SB1381# After a gradual implementation of this policy, during the 2014-15 school year, four-year-old children had to turn five on or before September 1st to be admitted into kindergarten. At the same time, certain four-year-olds no longer eligible for kindergarten were admitted into TK. Specifically, from 2014-15 until 2022-23, four-year-old children were eligible for TK if they had their fifth birthday between September 2nd and December 2nd.

In 2021-22, state leaders initiated another multi-year policy through the state budget to significantly grow the TK program, implementing a five-year plan that gradually increases age eligibility based on the month a child was born.4This expansion is part of a broader initiative, Universal PreKindergarten (UPK), aimed at bringing together preschool programs to ensure all children have access to early learning experiences the year before they start kindergarten. The increase in eligibility is primarily backed by allocating additional funding to school districts to implement the expansion. By the end of the expansion plan, in 2025-26, the program will be open to all four-year-old children who turn four by September 1.

The State Has Invested Billions of Dollars to Support Transitional Kindergarten

To carry out the expansion plan, state leaders agreed to provide the needed resources to initiate the expansion and sustain the program going forward. So far, the state budget has provided a mix of both one-time and ongoing resources. Those are outlined below:

One-time resources have been allocated to build foundational elements of the program. The state has provided more than $1 billionsince 2021-22 in one-time dollars for TK planning and implementation grants, facilities, and efforts to support the preschool teacher workforce — some of this funding was also available to support the California State Preschool Program (CSPP) and kindergarten.

The state is increasing ongoing funding for TK to accommodate the substantial growth in attendance resulting from the expansion. TK is supported by the Local Control Funding Formula (LCFF), which uses attendance to generate funding allocations to school districts (more details are provided in the “How Proposition 98 and the LCFF Support Transitional Kindergarten” section below). As of 2024-25 the state has provided an estimated $1.4 billion to account for the growth in attendance — this number tends to change when districts update and report their attendance numbers throughout the school year. Under current attendance projections the state would provide an additional $876 million in 2025-26, which would mark full expansion of the program. Attendance projections in prior years have overestimated TK uptake and attendance. Therefore, for 2025-26, the projected funding may be lower than currently proposed once attendance is collected and reported.

The state is increasing ongoing funding to improve staffing ratios in TK. As shown in the chart, an estimated $517 million has been allocated in 2024-25 to maintain a 1:12 adult-to-student ratio in TK classrooms. The 2025-26 budget proposes an additional $952 million to reduce ratios to 1:10, which would grow to a total of nearly $1.5 billion for this purpose. These dollars help maintain current staffing levels and would bring thousands of additional teachers and instructional aides to TK classrooms.5Districts that fail to meet staffing ratios face penalties that result in loss of funding. There are also penalties for not meeting class size requirements or teacher education requirements.

California has dedicated significant funding to schools to support the expansion of TK, including resources for planning grants, staffing, and attendance growth. This investment has facilitated substantial enrollment growth. However, realizing the full potential of this expansion requires addressing several key challenges. Securing and retaining a qualified TK workforce is essential, as staffing challenges could hinder the program’s effectiveness. Additionally, a continued focus on equitable access and consistent student attendance, particularly among low-income families is crucial. By addressing these key areas, California can maximize the impact of its investments and ensure four-year-olds benefit from this expansion.

Proposition 98 and the Local Control Funding Formula

How do state resources support TK expansion?

TK is funded through the LCFF, the same mechanism that funds K-12 grades. Funding for LCFF originates from Proposition 98, which guarantees a minimum annual funding amount for TK-12 schools and community colleges. The state fulfills this guarantee using General Fund dollars and local property taxes.

To support the growing costs of TK expansion, policymakers have gradually increased the Prop. 98 minimum guarantee. This adjustment, driven by increased student attendance through the LCFF, results in a larger share of state revenue being dedicated to education. This process of adjusting Prop. 98 is commonly known as “rebenching.” The chart below illustrates the year-over-year growth in Prop. 98 since 2022-23 based on current and projected attendance through the 2025-26 fiscal year. The orange bar reflects total growth across 2022-23 to 2025-26.

What is the role of the LCFF in distributing resources to local communities for TK expansion?

The LCFF uses an attendance measure, average daily attendance (ADA), to calculate funding. The base grant for TK (and grades K-3) in 2024-25 is $10,025, as shown in the table below, and is adjusted if districts meet average class sizes of 24 students or less. Districts also receive an add-on per TK ADA to maintain class ratios of 1:12 per classroom.

Additionally, the TK-3 base grant — and the base grant for all other grade levels — is “weighted” to provide additional funding to districts that enroll students classified as English learners, are eligible to receive a free or reduced-price meal, or are foster children. The LCFF provides a “supplemental” grant of 20% of the base grant for each of these students. When the number of these high-need students (TK and all other grade levels combined) exceeds 55% of a school district’s enrollment, a “concentration” grant of 65% of the base grant is applied for students above that threshold. These two grants are the key variables that ensure a more equitable distribution of funding to the highest-need districts.

This expansion is part of a broader initiative, Universal PreKindergarten (UPK), aimed at bringing together preschool programs to ensure all children have access to early learning experiences the year before they start kindergarten.

5

Districts that fail to meet staffing ratios face penalties that result in loss of funding. There are also penalties for not meeting class size requirements or teacher education requirements.

You may also be interested in the following resources:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

Republican budget proposals would impose harsh and ineffective “work requirements” that restrict access to health care, food, and other necessities for millions of Americans. These “work requirements” are just paperwork barriers, not solutions. Federal policymakers should reject them.

All Californians, no matter their race, gender, or zip code, deserve to have affordable health care, housing, food, and other necessities that allow them to thrive in their communities. But Republican federal budget proposals would pave the way for deep and harmful cuts that would take health coverage, nutrition assistance, and other essentials away from millions of Californians struggling to make ends meet due to persistently high inflation and the state’s long-standing housing affordability crisis. These cuts would increase poverty and widen racial and ethnic inequities in exchange for funding huge tax giveaways for the wealthy.

One way Republican leaders may implement this deeply inequitable agenda is by making access to vital services contingent upon complying with rigid “work requirements” — rules that require regular documentation of work hours. Such proposals are ineffective, punitive, counterproductive, and a waste of federal funds. Research shows that these requirements don’t meaningfully or sustainably increase employment or earnings. Instead, they take health care, food, and other vital resources away from families and individuals in need — disproportionately Black people and other people of color — by adding unnecessary paperwork and work reporting hurdles to receive the support they need. “Work requirements” — more accurately, paperwork or work reporting requirements — increase hardship and make it even more challenging to maintain or find jobs. Policymakers should reject all proposals to impose work reporting requirements, recognizing them for what they are — harmful cuts that threaten the health and well-being of the communities they represent.

what are “work requirements?”

“Work requirements” — more accurately, paperwork or work reporting requirements — withhold essential services and support unless individuals can regularly document time spent working or engaged in certain activities, or else prove they are exempt from these requirements. These rigid reporting rules often trip people up on red tape, causing them to lose access to health care, food, and other essential human needs that they are otherwise eligible for and that all people deserve. To refer to these rules, this report interchangeably uses the term “work reporting requirements” and the more common term “work requirements” (in quotations to indicate that such requirements largely impose paperwork burdens).

“Work Requirements” Are Unnecessary, Ineffective, Punitive, Counterproductive, and a Waste of Money

Republican-led proposals to impose new or harsher work reporting requirements are simply harmful cuts by another name. Rather than fostering economic mobility as proponents claim, these requirements threaten to push families and individuals deeper into poverty by withholding health care, food assistance, and other vital support. This report makes clear that “work requirements” are:

Unnecessary. Most people who are likely to be targets of such requirements already do work for pay, while the remainder are engaged in valuable — but unpaid — caregiving work, attending school to improve their employment prospects, or are ill, disabled, retired, or between jobs.

Ineffective. They fail to meaningfully or sustainably increase employment or earnings. Instead, their main effect is to take vital assistance away from people in need. Consequently, they have little to no effect on economic mobility, and may even drive some families and individuals deeper into poverty.

Punitive. Forcing workers to regularly document work hours increases administrative bureaucracy and often trips people up on red tape, causing them to lose access to vital benefits. Complying with these onerous requirements can be especially difficult for workers paid low wages who lack control over fluctuating work hours or have employers who are unwilling to verify their employment.

Counterproductive. They fail to address the fundamental barriers that prevent so many people from meeting basic needs, including a racially discriminatory labor market rife with low-paying jobs and the lack of affordable child care that is necessary to work. Plus, taking away people’s health care or ability to afford food only makes it harder for them to maintain employment and make ends meet.

A waste of money. Implementing and enforcing “work requirements” is costly and wastes funds that would be far better spent on services and supports that actually improve the lives of all people.

Research Shows that “Work Requirements” Simply Don’t Work

“Work requirements” are already part of several social safety net programs, but research into those policies has consistently shown that they do not increase employment opportunities in the long run or decrease “program dependence.” Instead, these policies lead to participants being pushed out of programs and are tied to increases in deep poverty. Specifically, research finds that “work requirements:”

Don’t meaningfully or sustainably increase employment or earnings.

Several studies have documented that employment gains when work reporting requirements are imposed are modest and do not have long-lasting effects. A 2015 in-depth review of the impact of public programs that provide assistance to families with low incomes noted that typical increases due to “work requirements” ranged from $300 to $600 in a year, but the effect quickly faded out. This earnings increase amounts to about one additional hour of work per week at the federal minimum wage, low enough to not impact labor decisions. Another review of the welfare reform shift in the 1990s toward “work requirements” found that recipients had documented flat earning trajectories due to the sporadic employment spells common for low-wage work. This shows that work reporting requirements may be successful in pushing some people to find paid work quickly to keep assistance, but without addressing the quality of jobs or the barriers to employment responsible for people not being able to work in the first place, these gains were quickly eroded. Furthermore, research shows that work reporting requirements do not lead to any employment gains for people with significant barriers. Most recipients who do not work simply cannot work.

Cause people to lose access to vital assistance.

Research also shows that while work reporting requirements do not sustainably increase employment and earnings, they lead to reductions in program participation by screening out people in need. A recent study found a 53 percent overall reduction in program participation among adults who are subject to “work requirements,” with homeless adults disproportionately affected. Work reporting requirement policies require categorizing participants into those who can and can’t work, an imperfect process that leaves people at the margin at risk of losing out the most due to inequitable treatment and bias. Additionally, documented race and gender discrimination in the labor market adds another barrier to sustainable employment, pushing people off assistance through no fault of their own.

Fail to address the root causes of poverty and, particularly, deep poverty.

The premise of “work requirements” has shifted the purpose of safety net programs and, therefore, the target population. Tying assistance to jobs means that aid is more likely to be provided to people who are in moderate poverty, taking away aid from the poorest households. A longitudinal study of “work requirement” implementation showed that overall deep poverty increased in some communities as a result of this shift. Work reporting requirements don’t address the fundamental problems making it difficult for families and individuals to make ends meet – that many jobs fail to pay enough to cover the cost of living; and that women, people of color, and other marginalized Californians face barriers to good jobs, including discrimination and the lack of affordable child care. Approaches that prioritize human capital investments, such as job training and educational programs, have a longer-term impact on labor and earnings and ultimately pay for themselves.

Adding More Hurdles for Accessing Medicaid Would Harm People’s Health and the Economy

Medi-Cal is California’s Medicaid program that provides free or low-cost health care to over one-third of the state’s population. The program serves individuals with modest incomes, including children, seniors, people with disabilities, and pregnant individuals. Medi-Cal is a lifeline for millions, ensuring access to essential health services that support public health and economic stability.

Medi-Cal coverage is essential to building and sustaining a stable workforce in California, especially because many low-wage jobs do not offer employer-sponsored health insurance and do not pay enough for people to afford coverage through Covered California, the state’s health insurance marketplace established under the Affordable Care Act. Ensuring access to Medi-Cal not only promotes individual health but also strengthens the state’s economy by supporting worker productivity.

Despite the critical role Medi-Cal plays, Congressional Republicans and the Trump administration have pushed for Medicaid “work requirements,” a policy that would make it harder for people to stay covered by tying health insurance to employment. Medicaid work reporting requirements are essentially cuts that would cause significant health coverage losses. Such proposals would require Medicaid beneficiaries to prove they are working, looking for work, or participating in job training programs in order to maintain coverage. Imposing such requirements in Medicaid would be:

Unnecessary: Most Medicaid enrollees under age 65 are already working (for pay). In California, over 3 in 5 adults work full-time or part-time (for pay). Among those who are not employed for pay, many are providing unpaid care for family members — an essential form of labor that sustains families and communities, yet is often overlooked by work reporting requirements. Others are managing illness or disability, or are enrolled in school.

Ineffective: Research consistently shows work reporting requirements are an ineffective policy tool that fail to increase employment. Instead, they create bureaucratic hurdles that cause people to drop off Medicaid — particularly people with disabilities, caregivers, and those working in unstable or low-wage jobs. Many enrollees who meet the work criteria still risk losing coverage due to administrative barriers, such as difficulty completing complex paperwork, missing deadlines, or lacking the necessary documents to prove eligibility.

Counterproductive: Without coverage, people would struggle to see doctors, get medications, and access preventive care, leading to more severe health problems and even medical debt. At the same time, hospitals and clinics, especially in low-income and rural areas, would face higher costs for unpaid care, putting financial strain on local health systems. Imposing “work requirements” would also make it harder for people to maintain employment, particularly people with chronic illnesses, such as diabetes and heart disease, who need regular access to health care to manage their conditions.

A Waste of Money: Implementing and enforcing work reporting requirements in Medicaid would be costly. The Government Accountability Office estimates that administrative costs can range from millions to hundreds of millions per state. These funds would be better spent on improving access to health care services in Medi-Cal rather than on unnecessary bureaucratic hurdles that take health coverage away.

“Work requirements” undermine the very purpose of Medicaid: it is health insurance, not a jobs program.

Federal Policy

The federal government plays a major role in shaping California’s budget, economy, and the well-being of its people.

Learn how federal policies shape California’s budget, economy, and vital programs — and how state leaders can respond to protect and support Californians.

Imposing Harsher Time Limits in SNAP/CalFresh Would Cut Benefits for Many and Increase Hunger

CalFresh, California’s name for the Supplemental Nutrition Assistance Program (SNAP), provides program participants with modest monthly noncash benefits to buy food and is the state’s most powerful tool to fight hunger. At the federal level, SNAP requires participants between the ages of 18 and 54 who do not qualify for limited exemptions to meet work reporting requirements in order to receive aid beyond a very limited window of time. In effect, this policy imposes a harsh time limit on access to SNAP that pushes participants off benefits after three months.

Despite the extensive body of research showing that “work requirements” take food away from those who need it and do not have lasting effects on employment, Republican leaders continue to push forward proposals to expand already rigid time limits enforced through work reporting requirements for SNAP recipients. Recent proposals for harsher time limits would specifically target older adults, people experiencing homelessness, foster youth who have aged out of the system, and veterans, increasing hardship among these communities who already face disproportionate challenges to meet work reporting requirements and struggle to make ends meet. “Work requirements” for SNAP are a failed experiment that have proven to be:

Unnecessary: The majority of SNAP recipients who can work already do. Over 3 in 4 adults who participated in CalFresh in a given month had recent paid employment. Those who cannot work are limited by significant barriers to employment, such as disability or macroeconomic conditions outside their control, like a lack of job opportunities. Additionally, many recipients who did not have paid employment reported having unpaid caretaking responsibilities that prevented them from working in a traditional setting, highlighting the limitations of work reporting requirement policies in recognizing essential unpaid labor.

Punitive: Proposals to impose harsher time limits via “work requirements” and limit key exemptions are grounded on the false narrative that people should earn the right to eat. Many SNAP recipients have low-wage and unstable jobs that are characterized by irregular schedules. This type of precarious work means that sometimes people may not be able to meet specific work hour requirements if their hours are cut or they miss work due to illness. Work reporting requirements punish recipients for not having quality jobs with predictable hours and benefits, without addressing the root causes of these issues.

Counterproductive: Food assistance is a key support for people to work and contribute to their communities. Being well-fed and having access to adequate nutrition is essential to staying healthy, reducing the risk of chronic illness, and increasing academic achievement and labor productivity. SNAP benefits also provide significant economic benefits to local economies, with each dollar in benefits generating a $1.54 return and helping fund jobs, as well as helping to reduce poverty. Harsher time limits would diminish the effectiveness of one of the strongest antipoverty programs and have long-term economic consequences for everyone.

Rejecting the expansion of already stringent SNAP time limits is necessary to ensure low-income families will continue to be able to access the healthy food they need.

False Narratives Rooted in Racism and Sexism Are Used to Justify “Work Requirements” and Only Further Entrench Inequities

Policymakers have long justified the need for “work requirements” based on false narratives rooted in racism and sexism, including the belief that people are not inherently deserving of support because deservedness must be earned through paid labor. This idea can be traced back to slavery — “the original work requirement” — where it was used to “justify a racialized system exploiting the labor of Black families.” For centuries, it has perpetuated the notion that unpaid caregiving work for one’s own family is not “real work,” despite its importance to society, contributing to the “persistent denigration of care work performed by women, especially women of color.” Today, the belief that people’s worth comes from paid work has become deeply embedded in social policies, inflicting broad harm by justifying the withholding of vital resources from families and individuals with low incomes. The end result is to further entrench existing inequities in poverty and hardship, as research finds that Black and Latinx people are at greater risk of having food assistance and other benefits taken away as a result of these policies.

The Evidence Is Clear: “Work Requirements” Are a Failed Experiment

Evidence from two programs that provide work-based cash assistance makes clear that “work requirements,” while touted as a way to encourage “self-sufficiency,” often exacerbate poverty rather than alleviate it. In the Temporary Assistance for Needy Families (TANF) program, the rigid demands for documented employment or work-related activities, often without access to necessary support systems, leave many parents in low-wage, unstable jobs that are not enough to lift them out of poverty. By contrast, the recent expansion of the Child Tax Credit (CTC) to families with minimal earned income had the opposite effect. This policy change contributed to a historic drop in child poverty. These two contrasting policy approaches highlight how “work requirements,” rather than fostering economic mobility, serve as a barrier to escaping poverty, making clear they are a failed experiment.

Imposing “Work Requirements” Locks TANF Participants Into a Cycle of Poverty

The California Work Opportunity and Responsibility to Kids (CalWORKs) program, or TANF as it’s known federally, helps support families with children with the lowest incomes, who are predominantly people of color, with modest cash grants, employment assistance, and critical supportive services. Since its inception, the primary goal of TANF has been to quickly push people into paid employment via punitive “welfare to work” training and employment requirements instead of addressing the root causes of poverty. The emphasis on “work requirements” has inhibited the program from truly lifting families out of poverty.

For many families, receiving cash assistance is conditional on narrowly defined work reporting requirements. Families who are not able to comply with all the requirements set forth by the state can be subject to a financial sanction that reduces their monthly cash grant, pushing them deeper into poverty. CalWORKs participants face significant barriers to employment and personal well-being due to limited education and disproportionate levels of poor mental health, domestic abuse, and substance use disorder. Program participants are also significantly put at a disadvantage because of who they are in an economy that discriminates against parents, women, and people of color.

Punitive “work requirements” do not improve long-term employment opportunities for CalWORKs recipients but make them subject to harsh sanctions, taking away assistance that barely puts families over the deep poverty threshold, or pushing them into jobs similar to the ones they lost, leading up to their TANF participation, creating an ineffective cycle of moving people between low-wage unstable employment and CalWORKs benefits. Investments into a holistic approach that addresses barriers to employment, as California has moved toward in recent years, and recognizes the value of unpaid caregiving work will have a more meaningful impact on poverty reduction than ineffective and costly “work requirements.”

Ending the Child Tax Credit’s “Work Requirement” Contributed to An Historic Drop in Child Poverty

Evidence from recent temporary changes to the federal Child Tax Credit suggests that children, families, and our broader society stand to benefit significantly when rules that make financial support contingent upon earnings or work are eliminated.

The federal Child Tax Credit supports childrens’ health, well-being, and development by helping families pay for child-related expenses, like food, diapers, and school supplies. Historically, however, families with the lowest earnings from work have been blocked from the full credit. This rule — essentially a “work requirement” — excludes about 2 million children living in low-income families in California from vital support.

In 2021, federal policymakers temporarily expanded the Child Tax Credit and ended its “work requirement,” allowing families with low earnings from work to receive the full credit for the first time in its history. This change contributed to a dramatic reduction in child poverty. The US child poverty rate fell to an historic low and California’s child poverty rate dropped by more than 40%. The improved credit was also associated with substantial reductions in racial income inequities, particularly among families with very low incomes, and with declines in food insufficiency and food insecurity. This suggests that increasing low-income families’ access to the full credit improved child and family well-being — improvements that researchers believe could also produce broader benefits to society, if sustained, given the high costs associated with childhood poverty.

Policymakers Should Reject Proposals to Impose “Work Requirements” that Just Add Bureaucratic Burdens

As Republicans in Congress push to make it more difficult for Californians to access health care, nutrition assistance, and other anti-poverty programs, it’s important to call these what they are: harmful bureaucratic burdens. Rather than fostering economic mobility, these layers of paperwork threaten to take away health care, food, and other essentials that all people need to thrive. These Republican proposals fail to improve affordability and, combined with the proposed tax cuts for the wealthy, will only deepen inequality across the country. Policymakers should reject these proposals, recognizing them for what they are — harmful cuts that jeopardize the health and well-being of the communities they represent.

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

key takeaway

Expanding the Child Tax Credit would help millions of children thrive by reducing poverty, addressing racial inequities, and ensuring families with the lowest incomes receive the full support they need.

All children deserve to grow up with the resources needed to be healthy and thrive. Yet millions of families across California struggle to afford food and other necessities because many jobs fail to pay enough to make ends meet, particularly in the face of persistently high inflation and rising housing costs.

Growing up in poverty can have dire consequences for children’s futures, but research shows that policymakers can mitigate or prevent this harm by giving families with low incomes more resources, like the Child Tax Credit. This is why federal policymakers must ensure that children who are currently excluded from the full federal Child Tax Credit because their families’ income is too low or because of their immigration status are provided this vital credit. With several provisions of the Child Tax Credit slated to expire at the end of 2025, Congress has an opportunity to improve the credit to promote a thriving childhood and a strong future for all children.

Policies Like the Child Tax Credit Can Improve Children’s Outcomes

Research shows that increasing financial resources for families with low incomes, including through refundable tax credits, has the potential to improve children’s health, educational attainment, and earnings prospects as adults.1A refundable income tax credit is a type of credit that benefits families and individuals with very low incomes. The credit provides the same value regardless of how much tax filers owe in personal income taxes. For example, a family who qualifies for a $500 refundable credit and owes $200 in taxes will get the full $500 credit, with $200 covering their taxes and $300 as a cash refund. If the family owes no tax, they will get the full $500 as a cash refund. Additional evidence from the recent one-year expansion of the federal Child Tax Credit shows the powerful immediate effects of targeting sizeable financial resources to families with low incomes. In 2021, for the first time in the Child Tax Credit’s history, nearly all families with low incomes became eligible for $3,600 per child ages 0 to 5 and $3,000 per child ages 6 to 17. This significantly boosted families’ incomes, bringing the national child poverty rate to an historic low and cutting California’s child poverty rate by more than 40%.

The federal Child Tax Credit currently provides families with $2,000 per dependent child under age 17, but families with low incomes — who are most in need of additional income to meet basic needs — are excluded from the full credit.2Additionally, the $2,000-per-child Child Tax Credit begins to “phase out” (gradually decline) for single parents with incomes over $200,000 and married couples with incomes over $400,000. For example, a single parent with one child must have an income of about $25,000 or more to qualify for the full Child Tax Credit, while a single parent with two children must earn about $28,000 or more. Families with income below these thresholds qualify for less than the full credit, and those with the lowest incomes – $2,500 or less – are completely excluded from the Child Tax Credit.

In addition, certain children are excluded from the Child Tax Credit based on their immigration status.3Specifically, children who have Individual Taxpayer Identification Numbers (ITINs) have been excluded from the Child Tax Credit since 2018. ITINs are issued by the Internal Revenue Service (IRS) to individuals who do not have Social Security Numbers to use for tax filing purposes. Several changes to the Child Tax Credit that took effect in 2018 are scheduled to expire after 2025, providing Congress with the opportunity to end the exclusion of children from the credit based on their families’ low income or immigration status.4If the Child Tax Credit reverts to its pre-2018 form, the maximum credit will decline from $2,000 per child to $1,000 per child and children age 17 will no longer be eligible, among other changes. For more information, see Urban-Brookings Tax Policy Center, The Tax Policy Briefing Book: What Is the Child Tax Credit?(updated February 2025).

Millions of Children Across California Are Blocked from Accessing the Credit Because Their Families’ Incomes Are Too Low

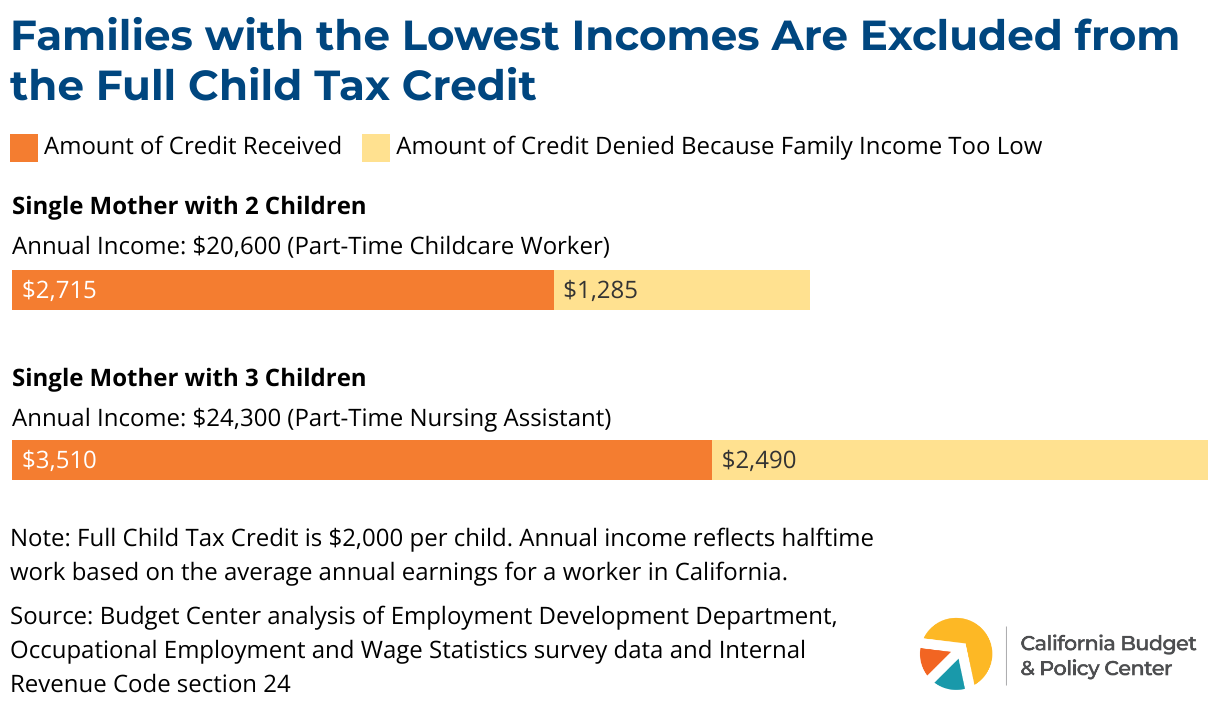

Despite the significant reduction in poverty brought about by the expanded Child Tax Credit in 2021, federal policymakers failed to extend the expanded credit beyond one year. Consequently, about 2 million children under the age of 17 across California are excluded from receiving the full Child Tax Credit because their families’ incomes are too low.

Families that don’t earn enough to qualify for the full credit include parents working part-time in order to go to school to pursue their career goals. For example, a single mother working halftime as a childcare worker and going to school to get her teaching credential makes just $20,600 per year — well below what is needed to make ends meet and support her two children in California. Yet she would qualify for only two-thirds of the full tax credit based on her low income — just $2,715 instead of $4,000. The $1,285 she is denied could have helped her buy about two months of groceries. A single parent working part-time to support three children would qualify for an even smaller share of the full Child Tax Credit. For example, if they earned $24,260 in annual wages as a part-time nursing assistant, they would receive just over half of the full tax credit — $3,510 instead of $6,000.

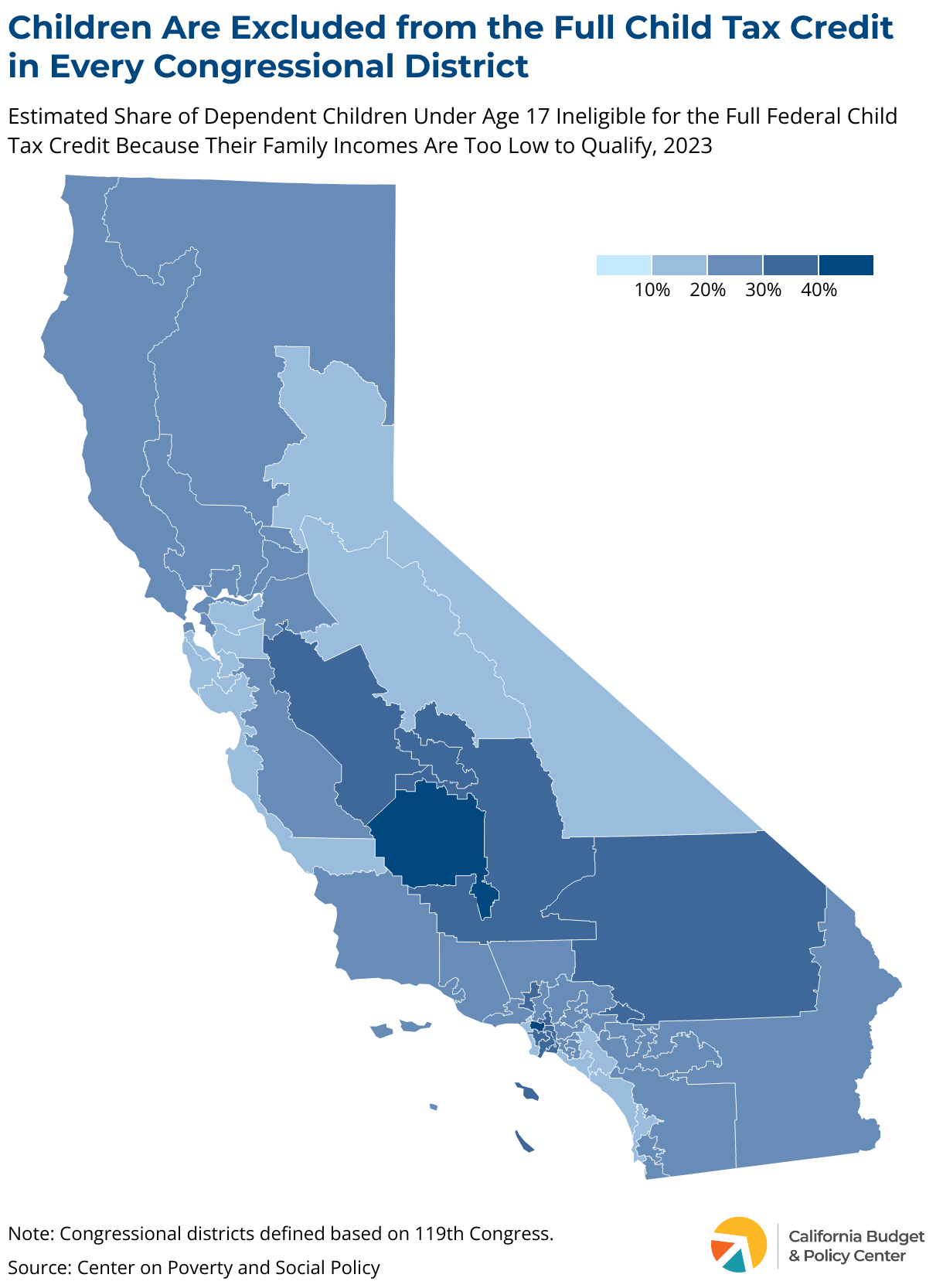

Children Are Excluded from the Full Child Tax Credit in Every California Congressional District

Statewide roughly one-quarter of children under age 17 are excluded from the full Child Tax Credit. However, in 20 of the state’s 52 congressional districts even more than a quarter of children are left out. The two districts where the most children are excluded are CA-37 (Kamlager) and CA-22 (Valadao), where over 40% of children are left out of the full credit because their families earn too little.

The districts where most children are excluded from the full Child Tax Credit based on their low family income are located largely in southern California, mainly in the Los Angeles region, with a few in the Central Valley. However, as highlighted in the map, districts across California leave out children who stand to benefit the most from receiving the maximum payment.

Built-In Barriers: How the Child Tax Credit Disproportionately Excludes Children of Color

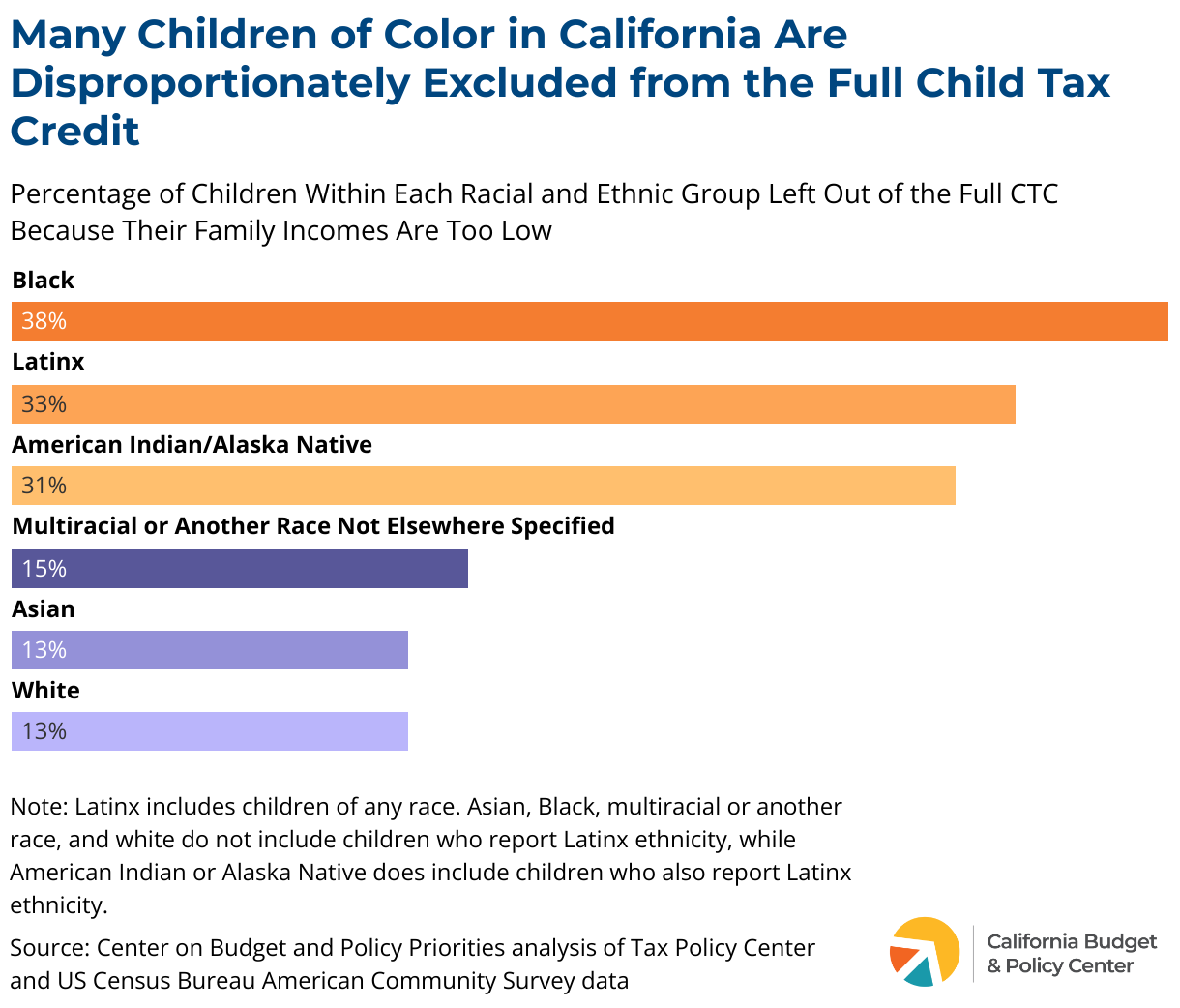

Of all the major racial and ethnic groups, Black, Latinx, and American Indian/Alaska Native children are disproportionately blocked from the full Child Tax Credit because their families earn too little, reflecting past and present discrimination as well as long-standing inequities in opportunity. Nearly 4 out of 10 Black children (38%) and roughly one-third of Latinx children and American Indian/Alaska Native children are excluded from the full Child Tax Credit due to their families’ low earnings, compared to around 13% to 15% of Asian, white, and multiracial and other children of color. This disproportionate exclusion of many children of color reinforces long-standing barriers that have continuously blocked families and children of color from escaping poverty and being able to afford basic necessities.

Many Children Are Denied the Child Tax Credit Based on Their Immigration Status

Hundreds of thousands of dependent children nationwide have been outright excluded from the Child Tax Credit since 2018 because of their immigration status even though their families pay taxes. Policies that discriminate against people based on immigration status are deeply harmful to families and communities. The vast majority of undocumented individuals live in mixed status families and many children who are excluded from the Child Tax Credit based on their status likely live in California given the large share of immigrants in the state. This exclusion has put families and children at greater risk of hunger, poverty, and other severe hardships. Federal Republican budget proposals under consideration include further restricting access to the Child Tax Credit by taking it away from US citizen children based on their parents’ immigration status.

All families that pay taxes should be eligible for tax benefits like the Child Tax Credit. Undocumented residents nationwide paid $96.7 billion in taxes in 2022, including $19.5 billion in federal income taxes. These contributions help support public services even as undocumented residents are excluded from benefiting from many of those same services. In California, undocumented residents paid $8.5 billion in state and local taxes in 2022.

Ending Exclusions Would Promote a Strong Future for All Children

With provisions of the Child Tax Credit slated to expire soon, Congress has an opportunity this year to strengthen the credit by ending the exclusion of children based on their families’ low income or immigration status. Making the credit more inclusive would lift additional families out of poverty, reduce racial and ethnic inequities, and promote a strong future for all children — both in California and the nation.

A refundable income tax credit is a type of credit that benefits families and individuals with very low incomes. The credit provides the same value regardless of how much tax filers owe in personal income taxes. For example, a family who qualifies for a $500 refundable credit and owes $200 in taxes will get the full $500 credit, with $200 covering their taxes and $300 as a cash refund. If the family owes no tax, they will get the full $500 as a cash refund.

2

Additionally, the $2,000-per-child Child Tax Credit begins to “phase out” (gradually decline) for single parents with incomes over $200,000 and married couples with incomes over $400,000.

3

Specifically, children who have Individual Taxpayer Identification Numbers (ITINs) have been excluded from the Child Tax Credit since 2018. ITINs are issued by the Internal Revenue Service (IRS) to individuals who do not have Social Security Numbers to use for tax filing purposes.

4

If the Child Tax Credit reverts to its pre-2018 form, the maximum credit will decline from $2,000 per child to $1,000 per child and children age 17 will no longer be eligible, among other changes. For more information, see Urban-Brookings Tax Policy Center, The Tax Policy Briefing Book: What Is the Child Tax Credit?(updated February 2025).

You may also be interested in the following resources:

There was a problem processing your signup. Please try again. Or contact us

Please check your email to confirm your signup.

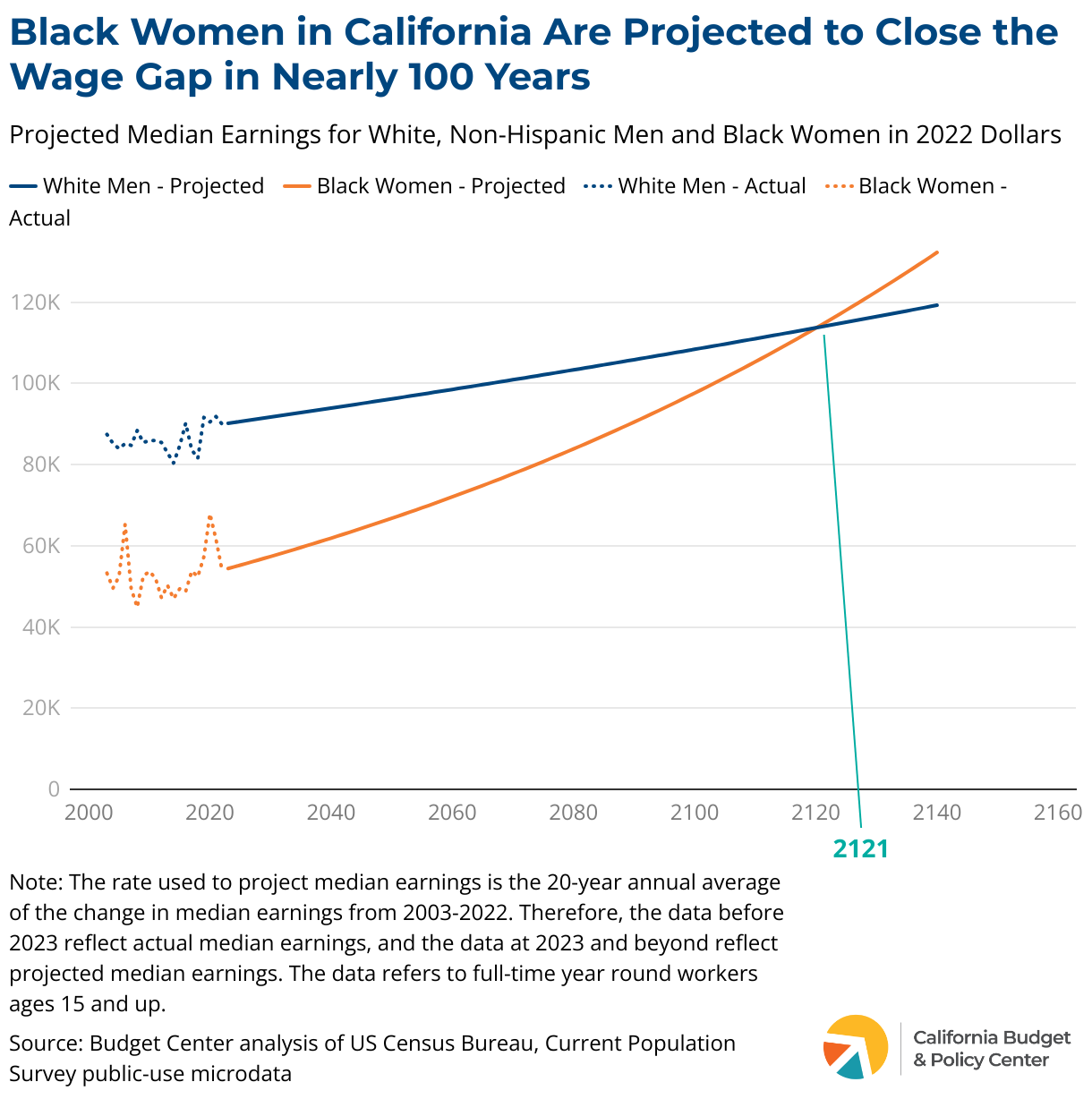

Women in California deserve the opportunity to thrive and access the same economic opportunities as their male counterparts. When women thrive, their families and communities prosper. However, women in California continuously encounter structural barriers that prevent them from doing so. Black women and Black single mothers in California, in particular, regularly confront policies rooted in racism and sexism that block them from accessing state funded programs and even stifle their earnings.

According to the latest Women’s Well-Being Index, Black women’s average wages are lower than white and Asian women and significantly lower than white men’s. This wage gap is persistent and closing at such a slow rate that wage equality will not be achieved in the lifetime of the youngest Californians. Additionally, in California, 67% of Black households are headed by single mothers. Consequently, Black single mothers face the additional financial burden of being the sole earners of their household and working while supporting their families, resulting in an even larger wage gap. While there has been progress in closing the wage gap, the state can implement policies that do much more to address the barriers to economic prosperity for Black women and Black single mothers in California.

About This Report

This report was co-authored with the California Black Women’s Collective Empowerment Institute. The Institute is dedicated to uplifting Black women and girls; CABWCEI fosters strategic partnerships, amplifies voices, and drives systemic change to eliminate barriers and advance social and economic equity across California.

As the anchor organization for the California Black Women’s Think Tank at CSU Dominguez Hills, CABWCEI works to strengthen representation, mobilize collective influence, and advocate for policies that secure social and economic safety nets.

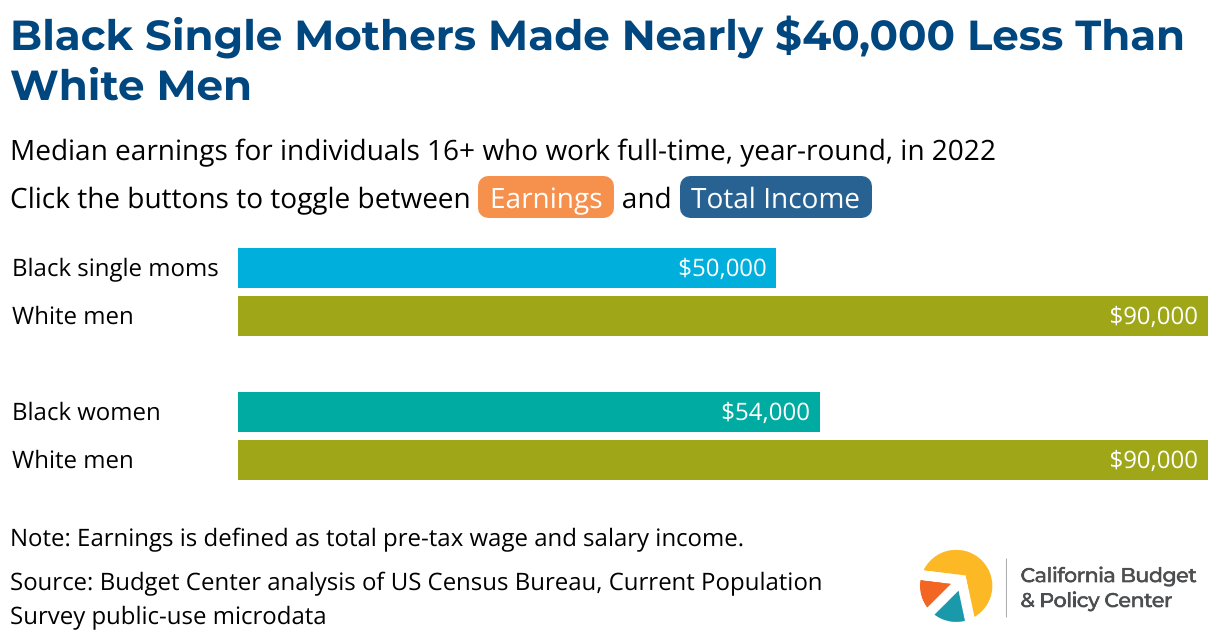

What is the Gap in Earnings Between Black Women and White Men?